- Food Packaging

- Soft Drinks Packaging Market

Soft Drinks Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Soft Drinks Packaging Market by Packaging Type (Bottles, Slim Cans, Others), Material (Plastic, Paper & Paperboard, Others), Capacity, Soft Drink Type, and Regional Analysis for 2026 - 2033

Soft Drinks Packaging Market Size and Trends Analysis

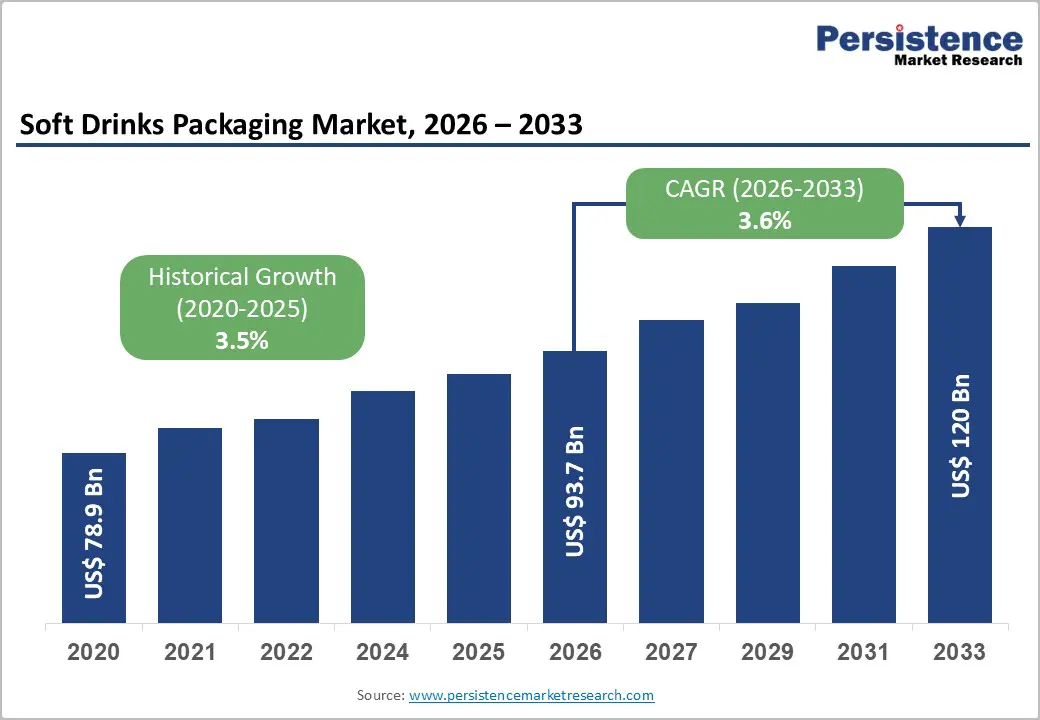

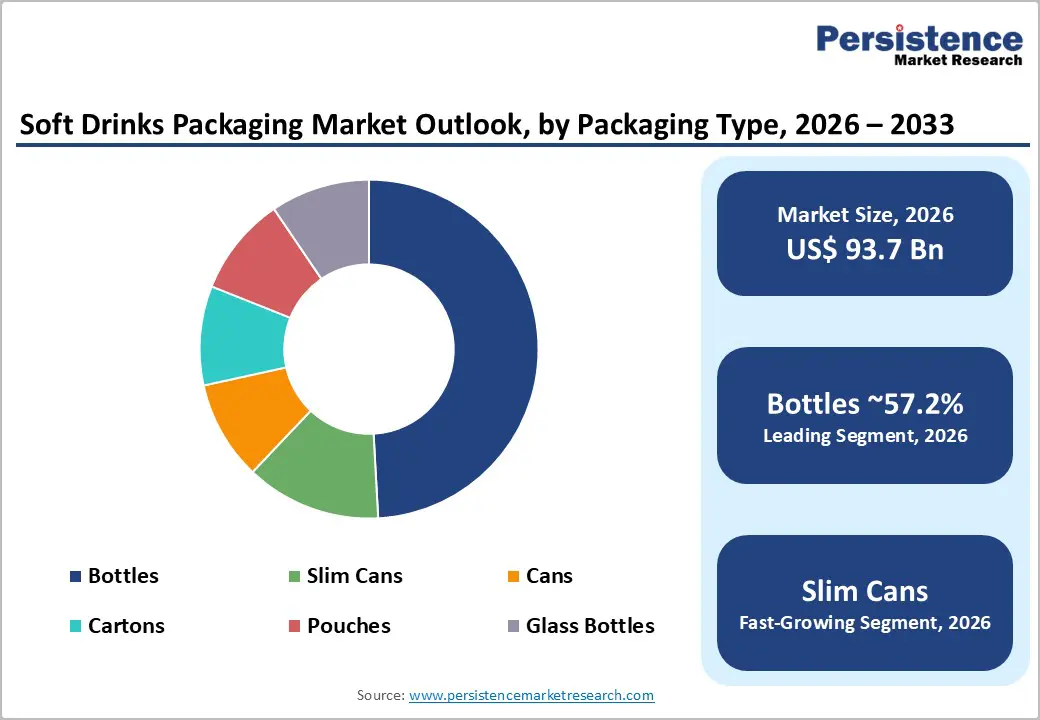

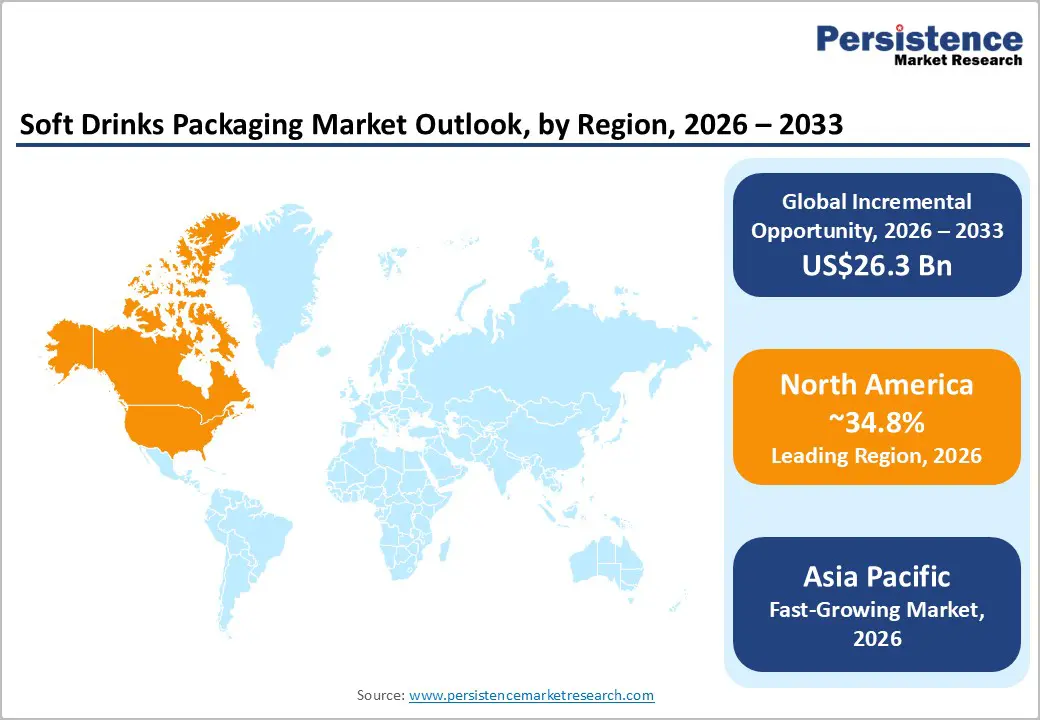

The global soft drinks packaging market size likely to be valued at US$93.7 billion in 2026 and is expected to reach US$120.0 billion by 2033, growing at a CAGR of 3.6% between 2026 and 2033, driven by tightening sustainability regulations, increasing adoption of recyclable and recycled-content packaging, and sustained demand for convenient, single-serve formats.

Packaging innovation, particularly lightweighting, adoption of slim cans, and alternative fiber barriers, remains central to competitive differentiation. Structural risks persist due to raw material price volatility and constraints in recycling infrastructure.

Key Industry Highlights:

- Leading Region: North America is projected to hold over 34.8% market share, driven by high per-capita consumption, advanced recycling infrastructure, and strong adoption of aluminum cans and high-recycled-content PET bottles.

- Fastest-growing Region: Asia Pacific, driven by rapid urbanization, rising disposable incomes, and expanding convenience retail, which are fueling strong demand for single-serve bottles, cans, and pouches.

- Investment Plans: Focus on aluminum can expansion, recycled PET capacity, fiber-based barrier technologies, and digitalization of packaging across North America, Europe, and the Asia-Pacific.

- Dominant Packaging Type: Bottles are projected to account for 57.2% of the market in 2026, led by PET bottles for carbonated and non-carbonated beverages.

- Leading Material: Plastic is anticipated to account for 69.3% market share in 2026, with PET dominating bottles and flexible formats.

| Key Insights | Details |

|---|---|

| Soft Drinks Packaging Market Size (2026E) | US$93.7 Bn |

| Market Value Forecast (2033F) | US$120 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability Regulation and Recycled-Content Mandates

Regulatory intervention is a primary force reshaping soft drinks packaging design and procurement strategies. Governments across North America, Europe, and parts of Asia Pacific are enforcing stricter recyclability standards, recycled-content thresholds, and extended producer responsibility (EPR) frameworks. These measures compel brand owners to shift toward mono-material packaging, higher recycled PET content, and aluminum formats with proven recycling rates. Compliance requirements increase short-term costs but structurally favor suppliers with circular-economy capabilities. Over the medium term, companies that secure recycled feedstock supply and demonstrate verified lifecycle performance gain preferred supplier status with multinational beverage producers.

Shift Toward On-the-Go Consumption and Premium Formats

Consumer behavior continues to favor portability, convenience, and portion control. Single-serve and medium-capacity packaging formats are increasingly preferred across urban and convenience retail channels. At the same time, premiumization trends, particularly in functional beverages, energy drinks, and limited-edition launches, are driving demand for differentiated formats such as slim cans and premium glass bottles. These formats support higher price realization and create incremental value through enhanced printing, branding, and shelf impact. Packaging suppliers benefit from increased per-unit revenue and more frequent SKU refresh cycles linked to innovation-driven beverage categories.

Material and Process Innovation Supporting Circularity

Technological progress in packaging materials and recycling processes is enabling lower environmental impact without compromising performance. Advances in lightweight PET bottles, higher-yield aluminum recycling, and paper-based barrier technologies are expanding the range of viable packaging options for soft drinks. Investments in recycling capacity and materials science improve feedstock availability and regulatory compliance while reducing life-cycle emissions. These innovations directly influence procurement decisions by global beverage companies that increasingly integrate packaging sustainability metrics into supplier selection and long-term contracting frameworks.

Barrier Analysis - Raw Material Price Volatility and Cost Pressures

The soft drinks packaging industry remains exposed to volatility in resin, aluminum, and paper pulp prices. Supply disruptions, energy costs, and geopolitical uncertainty affect input pricing and freight expenses. As demand for food-grade recycled materials increases, price premiums for recycled inputs persist, particularly during periods of constrained supply. Smaller converters face margin pressure due to limited bargaining power and capital-intensity requirements, which slow the adoption of circular materials in the absence of long-term offtake agreements.

Recycling Infrastructure and Feedstock Availability Gaps

Despite regulatory mandates, recycling collection and sorting infrastructure remains uneven across regions. Insufficient recovery rates and limited processing capacity for food-grade recycled materials restrict the practical availability of recycled inputs. These structural gaps elevate compliance risk and increase procurement costs for packaging manufacturers. In markets where infrastructure development lags policy ambition, packaging suppliers must balance regulatory expectations with operational feasibility, often relying on transitional solutions that dilute sustainability gains.

Opportunity Analysis - Closed-Loop and Recycled-Content Partnerships

Strategic investments in closed-loop recycling systems represent a high-impact growth pathway for soft drinks packaging suppliers as sustainability requirements move from voluntary commitments to enforceable standards. By integrating recycling, material recovery, and packaging production into a single value chain, suppliers can reduce dependence on volatile virgin raw materials while improving long-term cost predictability. These partnerships also support compliance with recycled-content mandates and extended producer responsibility frameworks that are increasingly shaping procurement decisions by beverage manufacturers. Direct participation in recycling infrastructure, either through joint ventures, long-term offtake agreements, or technology partnerships, allows packaging producers to secure consistent access to food-grade recycled materials, which remain structurally constrained in many regions. This access strengthens supplier credibility during contract negotiations and reduces exposure to supply disruptions. Over time, closed-loop models enable verified sustainability performance, improved lifecycle metrics, and deeper integration with brand owners’ environmental targets, creating a durable competitive advantage beyond short-term cost considerations.

Commercialization of Paper-Based Barrier Solutions

Paper and paperboard packaging formats are gaining traction as fiber-based barrier technologies improve. These innovations reduce reliance on plastic and metal while maintaining shelf-life performance for many soft drink applications. As commercialization accelerates, paper-based solutions are poised to capture market share from complex laminates, particularly in markets with strong preferences for renewable materials. Early adopters benefit from alignment with public procurement standards and retailer sustainability targets.

Format Innovation in Functional and Energy Beverages

The rapid growth of functional and energy drinks creates sustained demand for innovative packaging formats. Slim cans and small-capacity bottles support portability, premium branding, and controlled consumption. Packaging suppliers that align format innovation with beverage product development can enhance value capture through customization, premium finishes, and fast turnaround times, particularly in Asia Pacific and emerging urban markets.

Category-wise Analysis

Packaging Type Insights

Bottles are anticipated to account for 57.2% of market share in 2026, driven primarily by the widespread adoption of PET formats across carbonated and non-carbonated beverages. PET bottles offer a favorable balance of lightweight construction, cost efficiency, and strong barrier performance, enabling high-volume production and efficient long-distance distribution. Their compatibility with a wide range of filling technologies and closure systems further reinforces their dominance across both multinational beverage brands and regional bottlers. Bottles remain central to the distribution of mainstream soft drinks in modern retail, convenience stores, and foodservice channels, where shelf stability and logistical efficiency are critical. Large-scale bottled water, carbonated soft drinks, and flavored beverages continue to rely on PET bottles for their scalability and design flexibility, including resealability and shape customization. Ongoing lightweighting initiatives and increasing integration of recycled PET are expected to sustain the segment’s leadership despite rising regulatory scrutiny.

Slim cans are likely to be the fastest-growing packaging type, supported by strong adoption in energy drinks, functional beverages, and premium ready-to-drink formulations. Their narrow profile enhances shelf differentiation and aligns with contemporary branding strategies that emphasize portability and modern aesthetics. Slim cans are particularly favored for single-serve and impulse-purchase categories, where visual impact directly influences consumer choice. From a sustainability perspective, slim cans benefit from aluminum’s high recycling rates and established recovery infrastructure in many markets. Beverage brands increasingly deploy slim cans for low-sugar, functional, and limited-edition launches, reinforcing their premium positioning. Efficient stacking and transportation characteristics further improve supply chain economics, strengthening their role in both sustainability-focused and margin-accretive product portfolios.

Material Insights

Plastic packaging is anticipated to account for 69.3% of market share in 2026, reflecting the continued dominance of PET in bottles and flexible packaging formats. Plastic’s low production cost, durability, and strong barrier properties make it the preferred material for high-volume soft drink categories, including bottled water and carbonated beverages. Its adaptability to various shapes, sizes, and labeling techniques supports brand differentiation at scale. Despite increasing regulatory pressure, plastic remains integral to soft drink packaging due to its unmatched efficiency across manufacturing, transportation, and retail handling. In both developed and emerging markets, PET bottles continue to underpin mass-market distribution strategies. Ongoing investments in recycled plastic content, improved collection systems, and lightweighting technologies are helping to mitigate environmental concerns while preserving plastic’s economic advantages.

The paper and paperboard segment is likely to be the fastest-growing, supported by rising demand for renewable and recyclable packaging solutions. Advances in fiber-based barrier coatings and multilayer carton technologies are improving moisture resistance and shelf-life performance, enabling broader application in soft drink packaging. These materials are increasingly used for still beverages, juices, and select flavored drinks. Regulatory encouragement for recyclable and renewable materials, particularly in Europe and parts of the Asia Pacific, is accelerating adoption. Beverage manufacturers are incorporating paper-based cartons and composite paper solutions to align with sustainability commitments and respond to environmentally conscious consumers. As barrier performance continues to improve, paper and paperboard are expected to capture incremental share from traditional plastic formats in targeted applications.

Regional Insights

North America Soft Drinks Packaging Market Trends - Aluminum and rPET-Led Innovation in Soft Drinks Packaging

North America is projected to lead the market with over 34.8% share in 2026, supported by high per-capita soft drink consumption, a mature retail ecosystem, and early adoption of sustainability-driven packaging innovations. The U.S. anchors regional performance due to its scale, brand concentration, and advanced recycling infrastructure relative to other regions. Beverage manufacturers in the U.S. have increasingly shifted toward aluminum cans and high-recycled-content PET bottles to align with recyclability mandates and retailer sustainability scorecards.

Regulatory frameworks at the state level emphasize material transparency, recyclability, and extended producer responsibility, thereby influencing procurement decisions across the value chain. These policies have accelerated investment in aluminum can capacity and recycled PET processing. Major beverage brands have expanded the use of lightweight bottles and cans across carbonated soft drinks, flavored waters, and energy drinks, reinforcing demand for standardized, high-throughput packaging formats. Packaging suppliers have responded by scaling domestic manufacturing and recycling partnerships to reduce reliance on imported materials.

Capital allocation in North America increasingly targets packaging digitalization, including smart labeling, lightweighting technologies, and advanced filling compatibility. Investments by can manufacturers in new production lines and by packaging converters in recycled-material sourcing have strengthened regional supply resilience. As a result, North America continues to function as a testbed for packaging innovation, with successful formats often replicated across other global markets.

Europe Soft Drinks Packaging Market Trends - Regulation-driven Lightweight and Closed-Loop Packaging

Europe is a structurally advanced soft drinks packaging market, shaped by stringent environmental regulations and harmonized sustainability standards across member states. Countries such as Germany, the U.K., France, and Spain demonstrate strong adoption of recyclable, lightweight, and low-carbon packaging formats, driven by both regulatory pressure and consumer expectations. Deposit return schemes and recycled-content requirements have significantly influenced material selection, accelerating the shift toward mono-material plastics, aluminum cans, and fiber-based cartons.

Compliance with regional sustainability directives has driven beverage companies to redesign packaging portfolios, reducing material complexity and increasing recycled content. Cartons and paper-based packaging solutions have gained traction in still beverages and juices, supported by improvements in barrier technologies. Aluminum cans continue to expand their footprint in carbonated soft drinks and energy drinks due to high collection rates and established recycling loops across Europe.

Investment activity in the region focuses on recycling infrastructure, material innovation, and closed-loop systems. Packaging manufacturers have increased capital expenditure in local recycling facilities and material recovery operations to ensure compliance and cost stability. These investments strengthen supplier credibility with multinational beverage brands operating across multiple European markets, reinforcing Europe’s role as a regulatory and sustainability benchmark for global packaging strategies.

Asia Pacific Soft Drinks Packaging Market Trends - Regulation-Driven Lightweight and Closed-Loop Packaging

Asia Pacific is likely to be the fastest-growing regional market for soft drinks packaging, driven by rapid urbanization, rising disposable incomes, and the continued expansion of modern retail and convenience store networks. China, India, Japan, and ASEAN economies contribute substantial incremental demand, particularly in single-serve packaging formats aligned with on-the-go consumption. Bottles, cans, and flexible pouches dominate volume growth, reflecting price sensitivity and high consumption frequency across densely populated urban centers.

Beverage brands operating in the region are expanding local production and tailoring packaging formats to regional preferences. Smaller-capacity bottles and cans are increasingly favored in urban markets, while multi-pack and family-size formats remain relevant in suburban and semi-urban areas. Energy drinks, flavored waters, and functional beverages are key growth drivers, supporting demand for slim cans and differentiated bottle designs. Asia Pacific also benefits from manufacturing cost advantages and expanding packaging capacity, attracting investment from global packaging suppliers seeking proximity to high-growth beverage markets. Regulatory frameworks governing packaging waste and recyclability are evolving, particularly in China and parts of Southeast Asia, with a gradual increase in emphasis on material recovery and sustainable design. While regulatory enforcement remains uneven, growing policy attention and corporate sustainability commitments are expected to raise standards over the medium term, aligning the region more closely with global packaging sustainability trends.

Competitive Landscape

The global soft drinks packaging market exhibits moderate global concentration, with several large multinational packaging suppliers complemented by numerous regional players. Global leaders dominate aluminum cans, PET bottles, and cartons, while flexible packaging remains more fragmented. Competitive positioning increasingly depends on sustainability credentials, geographic reach, and the ability to secure recycled material supply.

Recent developments include expanded aluminum recycling capacity investments, consolidation among global packaging suppliers to enhance scale and sustainability capabilities, and beverage brand commitments to higher recycled-content usage. These moves reinforce long-term supplier alignment with regulatory and consumer sustainability expectations. Leading strategies emphasize circular-material innovation, capacity expansion in high-growth regions, and long-term partnerships with beverage producers. Differentiation centers on sustainability performance, cost stability, and speed to market.

Key Industry Developments

- In January 2025, Coca-Cola announced the launch of its first 100% recycled PET (rPET) bottles in Singapore, marking a major step in its sustainability strategy to increase recycled content in its soft drink packaging across Southeast Asia and align with global environmental goals.

Companies Covered in Soft Drinks Packaging Market

- Amcor

- Ball Corporation

- Crown Holdings

- Tetra Pak

- Novelis

- Ardagh Group

- Berry Global

- SIG Combibloc

- Plastipak Holdings

- Smurfit Kappa

- WestRock

- O-I Glass

- AptarGroup

- ALPLA Group

- Huhtamaki

- Graham Packaging

- Visy Industries

- Toyobo

Frequently Asked Questions

The global soft drinks packaging market size is likely to be valued at US$93.7 billion in 2026.

By 2033, the soft drinks packaging market is expected to reach US$120.0 billion.

Key trends include the shift toward recyclable and recycled-content packaging, rapid adoption of slim cans and single-serve formats, investments in closed-loop recycling systems, and growing use of fiber-based and lightweight packaging to meet regulatory and sustainability requirements.

Bottles are expected to be the leading packaging type, accounting for 57.2% market share in 2026, while plastic remains the dominant material with 69.3% market share, driven primarily by PET bottle usage in high-volume soft drink applications.

The soft drinks packaging market is projected to grow at a CAGR of 3.6% between 2026 and 2033.

Major players include Amcor, Ball Corporation, Crown Holdings, Tetra Pak, and Novelis.