- Renewable Energy

- Sustainable Energy Management Software Market

Sustainable Energy Management Software Market Size, Share, and Growth Forecast, 2025 - 2032

Sustainable Energy Management Software Market By Deployment (Cloud-based, On-premise), Application (Utility Data Management, Others), End-user Industry (Energy & Utilities, Building Automation, Manufacturing, Others), and Regional Analysis for 2025 - 2032

Sustainable Energy Management Software Market Share and Trends Analysis

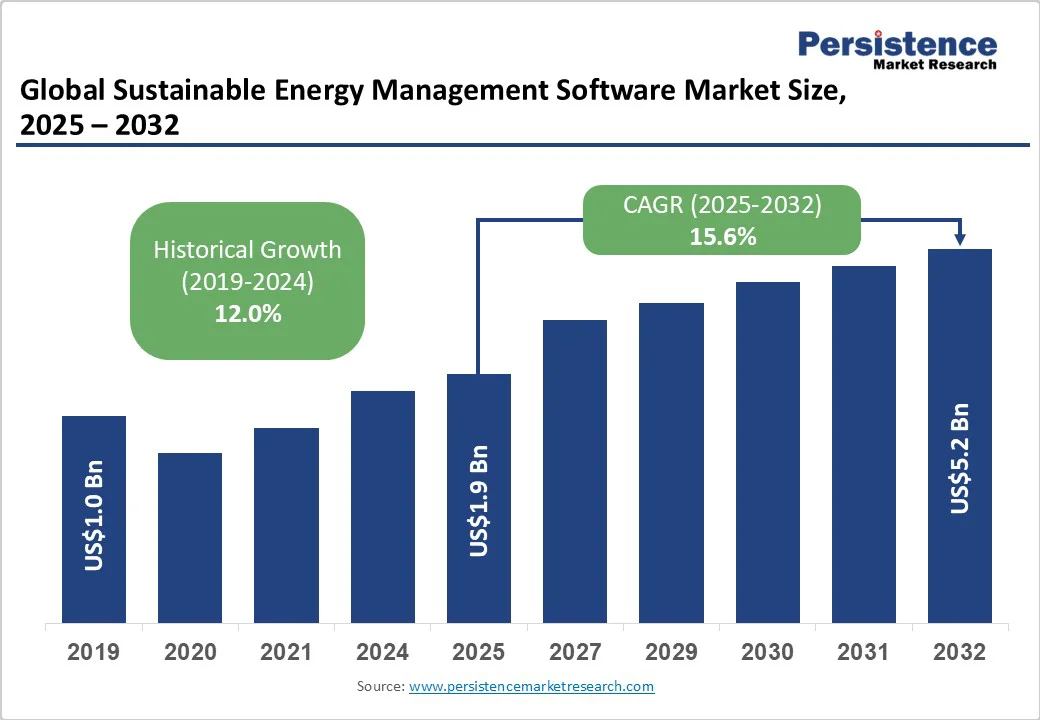

The global sustainable energy management software market is expected to be valued at US$1.9 billion by 2025. It is estimated to reach US$5.2 billion by 2032, growing at a CAGR of 15.6% during the forecast period from 2025 to 2032, driven by tightening regulatory mandates on carbon emissions, the rising integration of digital technologies in energy systems, and the accelerating adoption of sustainability management practices across industries.

The enhanced demand for carbon reporting, demand response capabilities, and energy optimization modules further supports market expansion. Sustainable energy management software has rapidly emerged as a crucial enabler of energy efficiency and compliance in the evolving global energy landscape.

Key Industry Highlights

- Leading & Fastest-growing Deployment: Cloud-based deployment is set to capture nearly 65% of the market in 2025, with on-premise solutions growing the fastest through 2032.

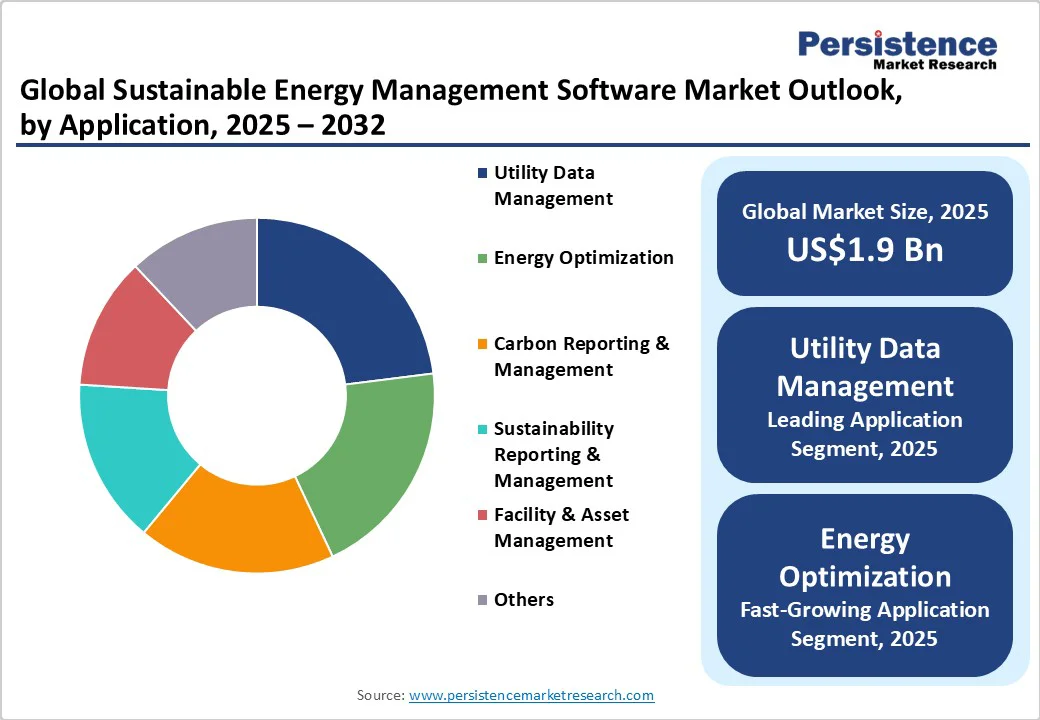

- Leading & Fastest-growing Applications: Utility data management is anticipated to dominate with approximately 23% market share in 2025, while energy optimization spearheads growth over the forecast period 2025-2032.

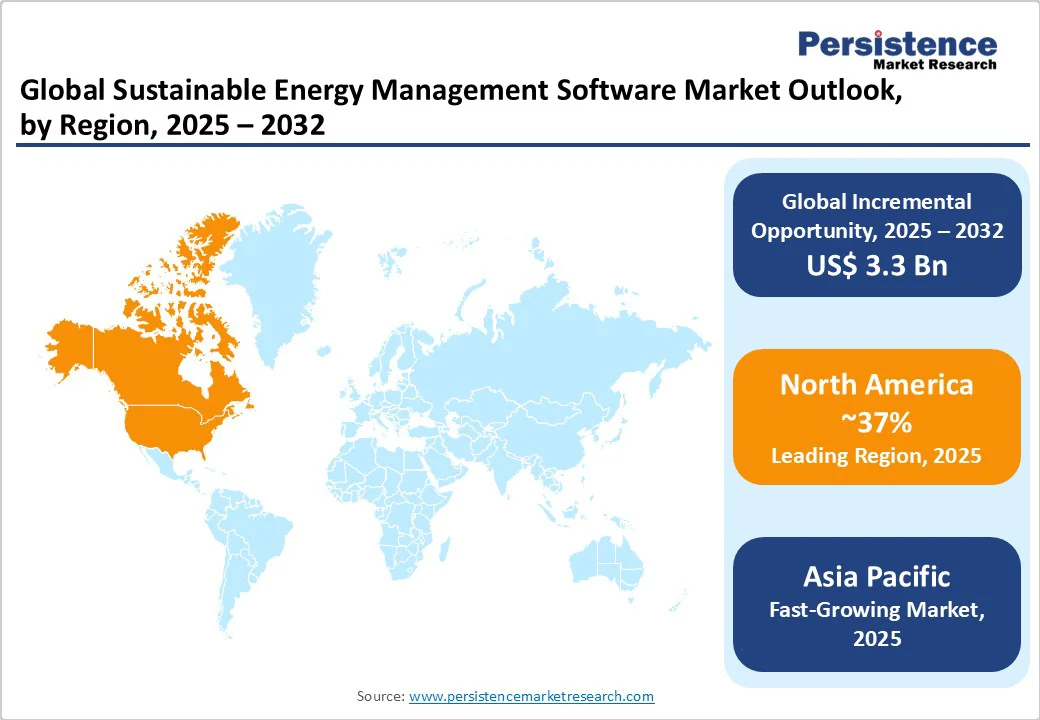

- Dominant Region: North America is expected to be the largest regional market, holding a 37% share in 2025, driven by stringent environmental and reporting regulations.

- Fastest-growing Regional Market: Asia Pacific is the fastest-growing regional market through 2032, supported by industrialization and supportive policies.

- April 2025: OneStream introduced a new ESG Reporting and Planning platform designed to integrate ESG metrics, including Scope 1, 2, and 3 emissions, with core financial processes, supporting scenario modeling, forecasting, and governance in alignment with EU and global regulations.

| Key Insights | Details |

|---|---|

|

Sustainable Energy Management Software Market Size (2025E) |

US$1.9 Bn |

|

Market Value Forecast (2032F) |

US$5.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

15.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

12.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Regulatory Momentum to Stoke the Uptake of Compliance and Reporting Solutions

Global bodies such as the International Energy Agency (IEA) and national government agencies, including the U.S. Environmental Protection Agency (EPA) and the European Commission (EC), are intensifying regulations mandating sustainability reporting and carbon emission reductions. For instance, the Green Deal of the European Union (EU) sets legally binding climate neutrality targets by 2050, propelling corporate investments in energy management software that facilitates compliance and transparent reporting. These legislative frameworks are fostering the demand for advanced carbon management modules, creating a structural market pull and compelling adoption by utilities and industrial sectors due to escalating penalties and incentives that tie financial benefits to environmental performance.

Rapid advancements in cloud computing, AI, and IoT are propelling the market growth. These technologies enable real-time monitoring, predictive maintenance, and automated controls, improving operational efficiency. Cloud-based models are projected to account for 65% of the market by 2025, driven by their scalability and cost benefits. AI-driven analytics can boost energy savings by up to 20% in pilot programs. This tech convergence is attracting wider adoption across manufacturing and commercial sectors, evolving the software into more adaptive, user-focused solutions.

Fragmented Supply Chain and Vendor Ecosystem Elevate Uncertainty

The market is marked by a fragmented vendor landscape, with numerous small and mid-sized players alongside major incumbents. This fragmentation leads to inconsistent software standards, interoperability issues, and variable product quality. Supply chain disruptions, exacerbated by geopolitical tensions and semiconductor shortages, have delayed the delivery of critical integrated hardware components, resulting in approximately 18% of project delays. These delays result in cost overruns and reduce client confidence. Without ecosystem standardization and collaborative frameworks, uncertainty will persist, prolonging customer acquisition and raising support costs.

The high upfront investment needed for deploying advanced energy management systems remains a significant barrier, particularly for SMEs. Integration with legacy infrastructure often requires substantial capital, ranging from $ 100,000 to $ 500,000, depending on the scale and level of customization. This financial burden extends ROI periods, deterring early adoption. Limited in-house expertise further increases implementation risks, driving reliance on specialized vendors and adding to service expenses.

Technological Synergies to Unlock Untapped Market Potential

The convergence of sustainable energy management software with adjacent technologies such as blockchain for energy trading, edge computing for decentralized analytics, and 5G for enhanced connectivity is creating novel business models and revenue streams. Pilot projects incorporating blockchain-enabled peer-to-peer energy transactions demonstrate potential to reduce operational costs by up to 12%, while edge analytics facilitate near real-time demand response services, enhancing grid resilience. These technological synergies are projected to generate a sub-market exceeding $ 500 million in value terms by 2030. Long-term investment in R&D and partner ecosystems focused on these converging technologies can position firms as market leaders, capturing share from traditional software incumbents and creating competitive moats through innovation.

In the Asia Pacific, Latin America, and parts of Africa, governments are aligning their national energy policies with the UN Sustainable Development Goals (SDGs), thereby fueling the demand for integrated energy management solutions. For example, India’s National Solar Mission and China’s carbon neutrality target for 2060 are propelling investments in sustainable infrastructure. The increasing electrification, integration of renewable energy, and deployment of smart grids in large economies are creating highly lucrative business opportunities for market players. Companies targeting these geographies will have novel avenues to capitalize on unmet needs through tailored offerings that address cost sensitivity, local regulatory compliance, and infrastructural heterogeneity.

Category-wise Analysis

Deployment Insights

The cloud-based deployment segment is leading, commanding an estimated 65% share in 2025. This dominance stems from the scalability, agility, and lower upfront costs associated with cloud infrastructure, which enable enterprises to rapidly implement and upgrade solutions across multiple sites. Cloud adoption is particularly prominent among medium-to-large enterprises and utilities, as it facilitates integration with advanced technologies such as IoT and AI. This integration supports real-time data collection and analytics, enabling more efficient energy usage and compliance with evolving regulatory requirements. Moreover, cloud platforms support subscription-based pricing models that reduce initial capital expenditure, improving accessibility for diverse end-user segments.

The on-premise deployment segment is expected to register the fastest CAGR during 2025-2032. This surge is driven by industries with stringent data security, privacy, and customization requirements, such as the oil & gas, pharmaceutical, and manufacturing sectors, which rely on proprietary processes. Organizations anticipating complex integration needs with legacy or proprietary systems frequently favor on-premise solutions to maintain control over data governance and operational continuity. Despite higher capital and operational costs, the growing demand for tailored, secure, and compliant solutions is fueling investments in on-premise deployments. This provides a strong growth trajectory anchored by regulatory scrutiny and internal risk management strategies.

Application Insights

Utility data management is poised to maintain a commanding lead, with an estimated market revenue share of approximately 23% by 2025. This predominance is attributed to the substantial data volumes processed by utility companies as they optimize generation, transmission, and distribution operations. Utility firms are increasingly integrating software platforms to enhance asset efficiency, predict equipment failures, and implement demand response protocols. The critical role of data accuracy and operational reliability ensures that investments in this segment remain a top priority.

Energy optimization is identified as the fastest-growing application segment with a robust CAGR between 2025 and 2032. This growth trajectory is largely propelled by rapid advancements in AI and machine learning (ML) algorithms, which enable precise forecasting of energy consumption patterns and facilitate automated control across diverse operational environments. Such sophisticated software capabilities enable organizations to dynamically adjust their energy use in response to real-time data inputs, thereby optimizing efficiency and minimizing unnecessary waste. The deepening focus on cost reduction and carbon footprint minimization directly incentivizes the deployment of energy optimization tools, which are increasingly valued for delivering both immediate and measurable financial and environmental benefits.

End-user Industry Insights

The energy & utilities sector is the largest end-user vertical by market share, expected to capture approximately 35% in 2025. This leadership position is reinforced by the continued rollout of smart grid infrastructure and the imperative to integrate large shares of renewable energy sources into grids while maintaining reliability. The strong focus of stakeholders in this sector on reducing carbon emissions and complying with regulations drives the sustained adoption of advanced energy management systems. Furthermore, utilities are benefiting from government incentives that promote energy efficiency and decarbonization, which in turn boost software investments.

Building automation is poised to emerge as the fastest-growing vertical during the forecast period from 2025 to 2032. Accelerating digitization and smart building initiatives aimed at reducing energy consumption and improving occupant comfort are driving demand. Technologies such as real-time energy monitoring, automated HVAC controls, and IoT-based occupancy sensors enable building owners to optimize energy use and meet certification standards, including Leadership in Energy and Environmental Design (LEED) and the Building Research Establishment Environmental Assessment Method (BREEAM).

Regional Insights

North America Sustainable Energy Management Software Market Trends

North America, led predominantly by the U.S., is slated to hold the largest portion of the market share, estimated at around 37% in 2025. This dominance is supported by a mature regulatory landscape featuring stringent environmental regulations administered by entities such as the EPA and state-level climate mandates. U.S. federal initiatives such as the Inflation Reduction Act further incentivize sustainable energy investments and software adoption for enhanced energy management and carbon tracking. The region boasts a highly competitive and innovative ecosystem, characterized by significant technological leadership in cloud computing, AI, and IoT, which underpins the rapid development and deployment of energy management solutions.

The U.S. is home to major utilities and corporate sustainability leaders that are aggressively adopting advanced energy management systems to meet aggressive carbon neutrality goals. Growth prospects for the North America market are also bolstered by increasing investments in grid modernization and smart city projects. Regulatory clarity, combined with the large-scale deployment of renewable energy capacity and corporate commitments, will continue to drive demand for software. The competitive landscape is characterized by intense innovation and strategic partnerships, with a focus on cybersecurity and data privacy to ensure compliance and operational resilience.

Europe Sustainable Energy Management Software Market Trends

Europe is expected to account for nearly 29% of the market share by 2025. Countries such as Germany, the U.K., France, and Spain are well-positioned to be key contributors, driven by comprehensive policy frameworks like the European Green Deal and the Renewable Energy Directive II, which are harmonizing sustainability standards across the region. These policies are mandating accelerated decarbonization by mid-century, enhanced energy efficiency, and transparent environmental, social, & governance (ESG) reporting, stimulating industry uptake of energy management solutions.

Germany stands out with its leadership in renewable energy integration and smart grid technologies, while the U.K. is advancing demand response and carbon accounting initiatives through its sustainability roadmap. This region is also home to strong collaborative networks among technology providers, utilities, and research institutions, which foster innovation and the diffusion of best practices. Competitive dynamics are influenced by stringent compliance requirements and a trend toward software standardization, which enhances market transparency and facilitates easier adoption.

Asia Pacific Sustainable Energy Management Software Market Trends

Asia Pacific is anticipated to be the fastest-growing regional market for sustainable energy management software, driven primarily by developments in China, India, Japan, and the ASEAN countries. The meteoric expansion of urban areas, economic growth, and surging electricity demand in the region are necessitating the modernization of energy infrastructure. Notable policy initiatives include China's 2060 carbon neutrality pledge and India’s ambitious renewable energy targets, alongside ASEAN's regional sustainability frameworks, which collectively mandate the adoption of innovative energy management technologies.

The manufacturing prowess and cost advantages in the Asia Pacific support localized software deployment and customization, enabling competitive pricing and rapid market penetration. Industrial users and utilities across the region are increasingly adopting software to manage complex energy flows and meet emerging environmental compliance standards. Investment trends also highlight growing interest from international technology firms forming partnerships and joint ventures with local businesses to capitalize on the expanding market opportunities. The competitive environment in Asia Pacific is dynamic, characterized by increasing digital infrastructure investments and evolving regulatory oversight that will underpin rapid sector growth.

Competitive Landscape

The global sustainable energy management software market exhibits a moderately concentrated structure, dominated by a handful of global technology firms ruling the market. Leading players include multinational software providers specialized in utility data management, energy analytics, and sustainability reporting solutions.

Alongside these incumbents, a vibrant ecosystem of niche startups and regional vendors contributes to competitive diversity and innovation. Market fragmentation persists at lower tiers due to variable regional adoption rates and specialized use cases, but consolidation trends are evident via strategic acquisitions and partnerships aimed at portfolio expansion and geographic reach enhancement.

Key Industry Developments

- In August 2025, Hanwha Qcells launched Geli Predict, an AI-driven platform for optimizing clean energy projects. `It offers advanced design, performance optimization, and real-time monitoring, supporting efficient distributed energy management and expanding to more markets soon.

- In August 2025, Honeywell acquired SparkMeter’s Praxis, GridScan, and GridFin platforms, enhancing Honeywell Forge Performance+ for Utilities. These tools offer real-time grid insights, asset optimization, and financial management, supporting utility modernization. The acquisition aligns with Honeywell’s strategy of portfolio simplification, growth, and energy transition innovation.

- In July 2025, Mercedes-Benz partnered with SAP to embed sustainability metrics into ERP systems, enabling real-time ESG reporting. Using SAP’s analytics and cloud, Mercedes-Benz improves environmental monitoring, transforming ESG from compliance into a strategic business function.

Companies Covered in Sustainable Energy Management Software Market

- Siemens AG

- Schneider Electric SE

- Honeywell International Inc.

- ABB Ltd.

- Johnson Controls International plc

- Oracle Corporation

- IBM Corporation

- SAP SE

- Enablon (Wolters Kluwer)

- Schneider Electric EcoStruxure

- EnergyCAP Inc.

- DEXMA Energy Intelligence

- Utilidata Inc.

- Urjanet

- EnergyHub

Frequently Asked Questions

The sustainable energy management software market is projected to reach US$1.9 Billion in 2025.

Tightening regulatory mandates on carbon emissions, rising integration of digital technologies in energy systems, and the accelerating adoption of sustainability management practices across industries are driving the market.

The sustainable energy management software market is poised to witness a CAGR of 15.6% from 2025 to 2032.

Elevated demand for carbon reporting, demand response capabilities, and energy optimization modules, and increasing adoption of AI- and ML-powered sustainability reporting solutions are key market opportunities.

Siemens AG, Schneider Electric SE, and Honeywell International Inc. are some of the key players in the sustainable energy management software market.