- Advanced Materials

- Soft Magnetic Materials Market

Soft Magnetic Materials Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Soft Magnetic Materials Market by Material Type (Soft Magnetic Composites (SMC)(Pure Iron/Iron Powder, Silicon Ferrite, Supermalloy, Permalloy), Soft Ferrites, Iron-Based Alloys, Amorphous Alloys, Electrical Steel, Others), by Application, End-user, by Regional Analysis, 2026 - 2033

Soft Magnetic Materials Market Size and Trend Analysis

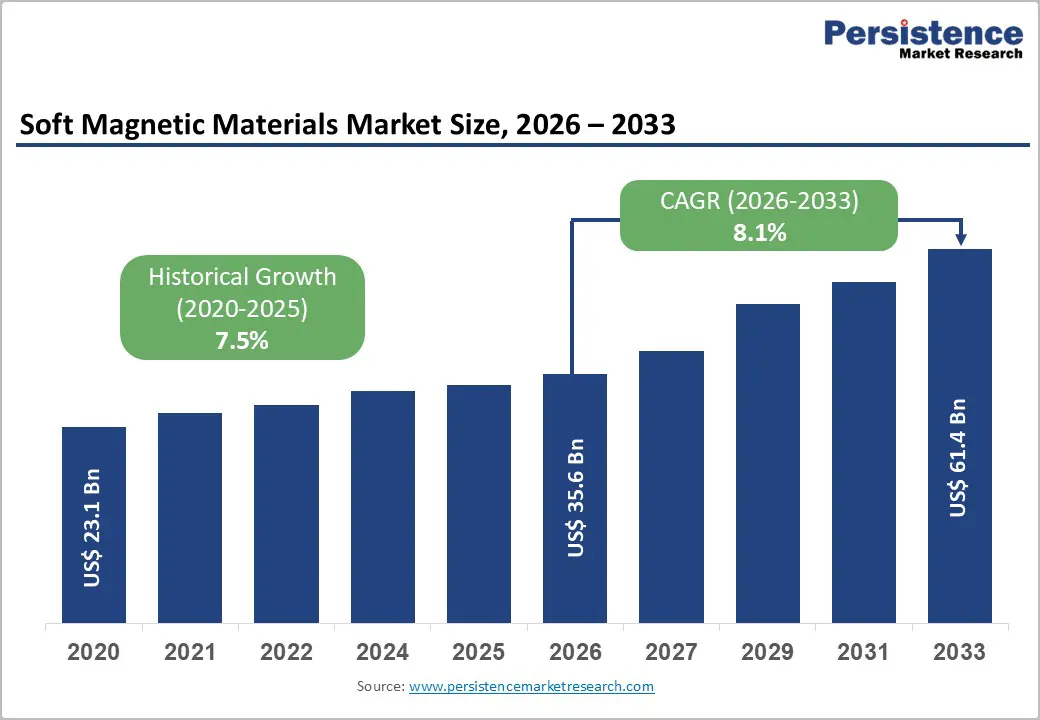

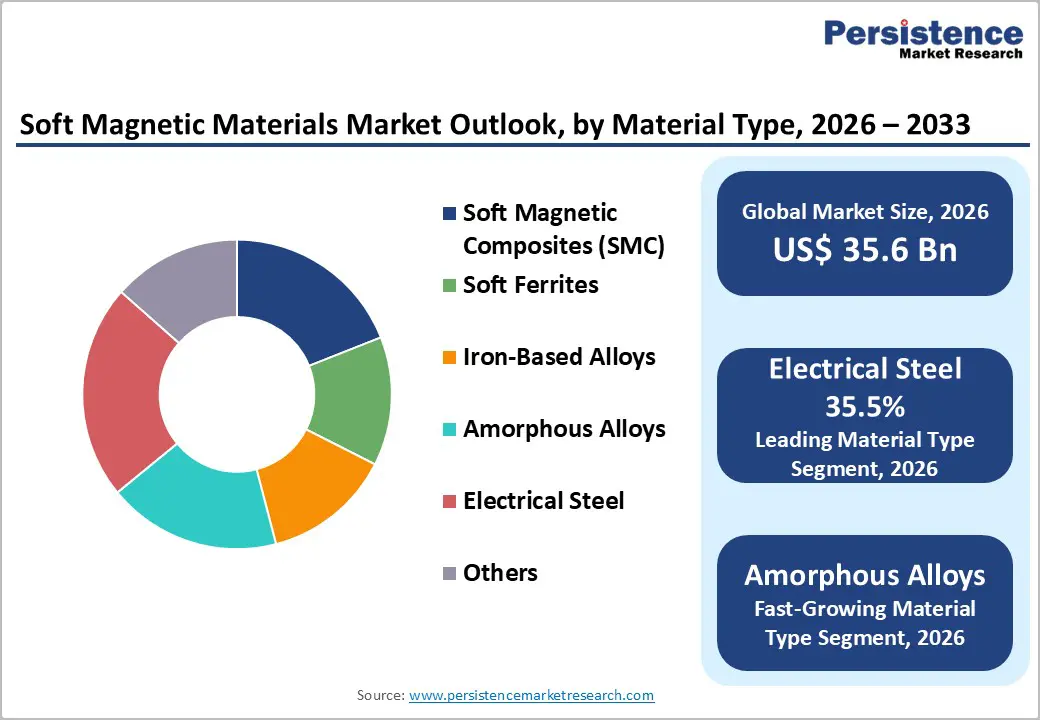

The global soft magnetic materials market size is expected to be valued at US$ 35.6 billion in 2026 and projected to reach US$ 61.4 billion by 2033, growing at a CAGR of 8.1% between 2026 and 2033.

This growth is primarily driven by rising adoption of electric vehicles and accelerating investments in renewable energy systems, both of which require efficient energy conversion and power management. Increasing use of high-performance magnetic cores in motors, generators, transformers, and inductors is strengthening demand. With global electric vehicle sales exceeding 14 million units in 2024 and renewable energy capacity additions reaching 510 GW, the market outlook remains strongly positive.

Key Market highlights:

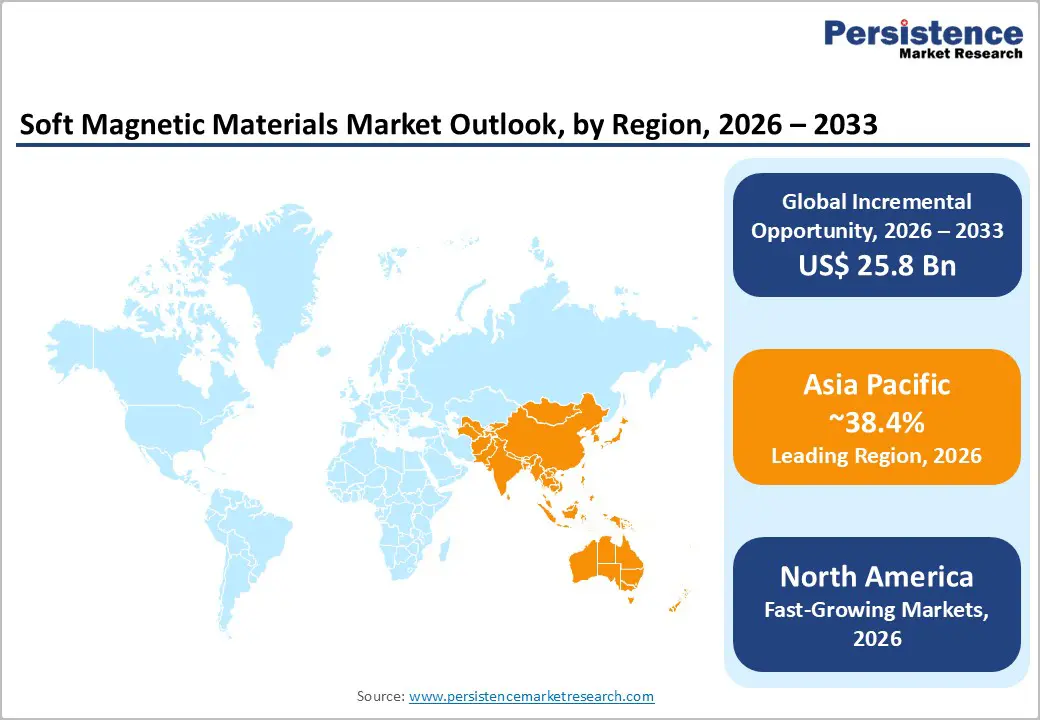

- Leading Region: Asia Pacific commands 38.4% share in 2025, driven by China’s manufacturing dominance and renewable energy expansion.

- Fastest-Growing Region: Asia Pacific shows rapid growth, fueled by EV production and cost efficiencies across India and Japan.

- Leading Material Category: Electrical steel leads the material type segment with 35.5% share in 2025, critical for transformers due to low core losses.

- Fastest-Growing Material Category: Amorphous and nanocrystalline materials are the fastest-growing, offering high-frequency efficiency and energy savings in EV and telecom applications.

- Key Opportunity: Automotive electrification is driving demand, with global policies and the EU’s 30 million EV target by 2030 increasing traction motor requirements.

| Key Insights | Details |

|---|---|

| Soft Magnetic Materials Size (2026E) | US$ 35.6 billion |

| Market Value Forecast (2033F) | US$ 61.4 billion |

| Projected Growth CAGR(2026 - 2033) | 8.1% |

| Historical Market Growth (2020 - 2025) | 7.5% |

Market Dynamics

Drivers - Rising Electric Vehicle Adoption Accelerating Demand for High-Performance Soft Magnetic Materials

The accelerating transition toward electric vehicles (EVs) is a major driver for the soft magnetic materials market, as these materials are crucial for the efficient operation of motors, alternators, and power electronics. Global EV production continues to rise sharply, supported by favorable government policies, emission reduction targets, and consumer demand for energy-efficient transportation. Soft-magnetic materials enable compact motor designs, reduced core losses, and improved power density, thereby directly enhancing vehicle range and overall performance.

Advanced materials, such as non-oriented electrical steel, amorphous alloys, and nanocrystalline materials, are increasingly being adopted in traction motors and onboard charging systems. These materials reduce energy losses, improve thermal stability, and support higher rotational speeds. As automakers focus on lightweight architectures and greater efficiency to remain competitive, demand for high-quality soft-magnetic materials is expected to grow steadily over the forecast period.

Expansion of Renewable Energy Infrastructure Increasing Demand for Transformers and Generators

The rapid expansion of renewable energy infrastructure is another key driver supporting the growth of the soft magnetic materials market. Wind turbines, solar inverters, and grid-connected transformers rely heavily on soft magnetic materials to ensure efficient power conversion and minimal energy losses. Rising investments in clean energy projects worldwide, supported by government mandates and decarbonization goals, are accelerating the deployment of renewable power systems.

Materials such as electrical steel, amorphous alloys, and nanocrystalline cores play a vital role in improving efficiency under high-frequency and variable-load conditions. Their ability to reduce hysteresis and eddy current losses enhances grid stability and lowers operational costs. Continued growth in renewable capacity additions, particularly in the Asia Pacific and Europe, is expected to sustain long-term demand.

Restraints - Supply Chain Volatility and Raw Material Price Fluctuations Impacting Cost Structures

Volatility in the supply chain for key raw materials, such as iron, nickel, and rare-earth elements, remains a significant constraint on the soft magnetic materials market. Sharp price fluctuations, driven by supply disruptions, export controls, and geopolitical uncertainties, increase production costs and reduce margin stability. Alloy-based materials, including permalloy and specialized iron-nickel compositions, are particularly susceptible to fluctuations in raw material prices.

Rising input costs limit the ability of manufacturers to scale production efficiently and pass on costs to end users, especially in price-sensitive applications. Smaller and mid-sized producers face greater challenges due to higher import dependence and limited supplier diversification. Persistent supply instability may slow capacity expansion and delay project timelines across the automotive and energy sectors.

Stringent Environmental and Emissions Regulations Increasing Compliance Burdens

Stringent environmental regulations governing emissions, energy consumption, and waste management are restraining market growth by increasing compliance and operational costs. Policies targeting carbon-intensive manufacturing processes, particularly in steel and alloy production, are placing additional financial pressure on producers. Regulatory mechanisms such as carbon tariffs and border adjustment measures raise the cost of exporting high-emission materials into regulated markets.

In addition, stricter waste-disposal and chemical-handling requirements for ferrite and alloy processing increase capital and operating expenditures. These regulatory constraints discourage rapid capacity expansion and slow adoption in cost-sensitive end-use applications. Manufacturers must invest heavily in cleaner technologies, which can impact short-term profitability and market penetration.

Opportunities - Advancements in High-Frequency Applications Creating New Market Opportunities

The increasing deployment of 5G infrastructure, advanced power electronics, and high-speed data systems is driving demand for soft-magnetic materials optimized for high-frequency performance. Nanocrystalline cores, soft-magnetic composites (SMCs), and amorphous alloys exhibit low core losses, high permeability, and thermal stability, making them suitable for base stations, inductors, and transformers. Global telecommunication investments reached US$ 1.2 trillion in 2025, fueling the adoption of these materials.

Amorphous alloys, for example, reduce energy losses by up to 70% compared to traditional silicon steel, enhancing system efficiency and reliability. This trend opens opportunities for premium products, technology-driven differentiation, and strategic partnerships with telecom and electronics manufacturers worldwide.

Growth in Automotive Electrification Driving Demand for Soft Magnetic Materials

The electrification of the automotive sector presents significant opportunities for soft magnetic materials, particularly in EV motors, inverters, and power electronics. Europe alone aims to achieve 30 million EVs by 2030 under the Fit for 55 policy, boosting demand for high-performance electrical steel and soft ferrites in stators, rotors, and traction motors. Advanced materials help reduce core losses, improve thermal performance, and enable lighter, more efficient designs.

Manufacturers like thyssenkrupp are scaling production, with new lines producing 200,000 tons of non-oriented steel annually for e-mobility. Amorphous and nanocrystalline alloys are increasingly adopted due to their ability to reduce inverter losses by 15%, supporting long-term adoption in automotive electrification and related high-performance applications.

Category-wise Analysis

Material Type Insights

Electrical steel leads the material type segment with a 35.5% market share in 2025, driven by its high magnetic permeability and extensive use in large-scale power equipment. Within this segment, grain-oriented electrical steel (GOES) holds dominance, primarily for transformers, as its aligned grain structure reduces core losses by 30-50%, according to IEA efficiency standards. Reliable performance in high-flux applications, such as generators, further strengthens its market position.

While electrical steel dominates, amorphous and nanocrystalline materials are emerging as the fastest-growing categories. These materials excel in high-frequency and precision applications, including advanced inverters, EV traction motors, and telecom equipment. Their low core losses, thermal stability, and compact form factors make them ideal for modern high-efficiency systems, creating significant growth opportunities as industries increasingly demand lightweight and energy-efficient magnetic solutions.

Application Insights

Motors lead the application segment with a 45.2% share in 2025, driven by their critical role in electric vehicle traction systems and industrial drives. Non-oriented electrical steel improves motor efficiency and supports a range of motor types, from brushed DC to induction motors, reinforcing its dominance in the automotive and industrial sectors.

Transformers and inductors are emerging as the fastest-growing applications. Increasing deployment of renewable energy systems, EV charging infrastructure, and smart grid modernization is boosting demand for low-loss, high-performance cores. These materials improve energy efficiency, support variable-frequency operation, and enable compact, lightweight designs, positioning them for rapid adoption across power and industrial sectors.

Industry Insights

The automotive industry is the leading Industry, with a 40.1% share in 2025, driven by EV adoption, electrification policies, and government incentives. High-performance magnetic cores in drive units, motors, and inverters solidify the sector’s market dominance, particularly in regions pursuing zero-emission targets and large-scale EV deployment.

Renewable energy and industrial automation are the fastest-growing end-use sectors. Expanding wind, solar, and industrial projects increase the demand for soft-magnetic materials in transformers, generators, and motor drives. Low-loss, high-efficiency materials enhance system reliability, reduce operational costs, and meet modern efficiency and sustainability standards, supporting long-term adoption across energy and industrial applications.

Regional Insights

North America Soft Magnetic Materials Market Trends

North America accounts for approximately 34.2% of the global soft magnetic materials market in 2025, led by the U.S. with a mature manufacturing base and substantial EV investments exceeding US$ 100 billion. Incentives under the Inflation Reduction Act are accelerating renewable energy projects, with solar capacity up 30%, while innovation hubs like Oak Ridge National Lab advance soft magnetic composites (SMCs) for high-efficiency motors and inverters.

Regulatory frameworks emphasize energy efficiency, with EPA standards reducing losses in appliances and industrial equipment by up to 25%. A robust R&D ecosystem supports the development of next-generation alloys and nanocrystalline materials. Growing adoption of EVs, smart grids, and industrial automation ensures sustained demand for soft magnetic materials across the region, reinforcing North America’s leadership position.

Europe Soft Magnetic Materials Market Trends

Europe’s soft magnetic materials market is growing steadily, with a forecasted CAGR of 7.2%, driven by automotive electrification and renewable energy expansion. Germany leads automotive applications, producing millions of EVs annually and using electrical steel extensively in e-drives. France and the UK align with the EU Green Deal, targeting 40 GW of offshore wind capacity by 2030, while Spain strengthens supply chains to support regional production.

Manufacturers like thyssenkrupp expand capacity to meet rising demand, producing high-quality electrical steel for motors, transformers, and industrial equipment. Harmonized regulations reduce trade barriers, encouraging investment in clean energy and e-mobility projects. Continued emphasis on energy efficiency and sustainability drives the adoption of advanced soft magnetic materials across automotive, energy, and industrial sectors.

Asia Pacific Soft Magnetic Materials Market Trends

Asia-Pacific dominates the global soft-magnetic materials market, accounting for approximately 38.4% of the market in 2025, with China accounting for 55% of rare-earth supply and producing over 10 million EVs. Japan leads in innovations in amorphous and nanocrystalline technologies through companies such as Hitachi, while India and ASEAN countries are growing as manufacturing hubs, leveraging cost advantages and industrial expansion.

The region benefits from renewable energy investments, with India adding 25 GW of solar capacity in 2025, supporting transformer and inductor demand. Low manufacturing costs, government incentives, and strong EV adoption strengthen the market. Japan, China, and India drive regional leadership in high-efficiency motors, inverters, and power electronics, ensuring Asia Pacific remains the largest and fastest-evolving soft magnetic materials market.

Competitive Landscape

The soft magnetic materials market is highly consolidated, with leading players leveraging vertical integration, proprietary technologies, and extensive R&D to maintain competitiveness. Companies focus on expanding production capacity and innovating advanced materials, such as low-loss alloys and high-efficiency cores, to meet growing demand across automotive, energy, and industrial sectors.

Key market differentiators include material performance, energy efficiency, and reliability under high-frequency and high-flux applications. Emerging strategies emphasize sustainability, environmentally compliant sourcing, and regulatory alignment to address evolving global standards, ensuring that manufacturers remain competitive while catering to evolving industry needs and high-performance application requirements.

Key Market Developments

- In January 2025, thyssenkrupp launched a new annealing line in Bochum with a capacity of 200,000 tons of non-oriented electrical steel, specifically aimed at supporting the growing electric vehicle mobility sector and enhancing production efficiency for e-mobility applications.

- In July 2024, VACUUMSCHMELZE formed a strategic alliance with Aclara to secure rare earth supply for magnetic alloys production, strengthening its supply chain, ensuring material availability, and supporting high-performance applications in automotive, renewable energy, and industrial electronics.

- In January 2023, Daido Steel introduced the STARPAS-50PC2S permalloy foil, designed for low-frequency electromagnetic shielding in autonomous vehicles, improving protection, reducing interference, and enabling reliable operation in next-generation EV and advanced automotive electronics systems.

Companies Covered in Soft Magnetic Materials Market

- Hitachi Metals

- VACUUMSCHMELZE GmbH & Co. KG

- TDK Corporation

- Arnold Magnetic Technologies

- Daido Steel Co., Ltd.

- Toshiba Materials Co., Ltd.

- ATI Metals

- GKN Powder Metallurgy

- Magnetics

- Ferroxcube

- Hengdian Group DMEGC Magnetics

- AT&M (Advanced Technology & Materials Co., Ltd.)

- Qingdao Yunlu Energy Technology Co., Ltd.

- China Amorphous Technology Co., Ltd.

- Henan Zhongyue Amorphous New Materials Co., Ltd.

Frequently Asked Questions

The global soft magnetic materials market is expected to reach US$ 35.6 billion in 2026.

Rising EV adoption drives demand, with global sales exceeding 14 million units in 2024 per IEA.

Asia Pacific leads with 38.4% share in 2025, powered by China’s manufacturing dominance and renewable energy expansion.

Automotive electrification presents major potential, supported by the EU’s 30 million EV target by 2030.

Leading players include Hitachi Metals, VACUUMSCHMELZE GmbH & Co. KG, TDK Corporation, Arnold Magnetic Technologies, and Daido Steel Co., Ltd.