- Automation & Robotics

- Smart Pneumatics Market

Smart Pneumatics Market Size, Share, and Growth Forecast, 2026 - 2033

Smart Pneumatics Market by Type (Valve, Actuator, and Module), Component (Hardware and Software), Industry (Automotive, Oil & Gas, Food & Beverages, Energy & Power, and Others), and Regional Analysis for 2026 - 2033

Smart Pneumatics Market Size and Trends Analysis

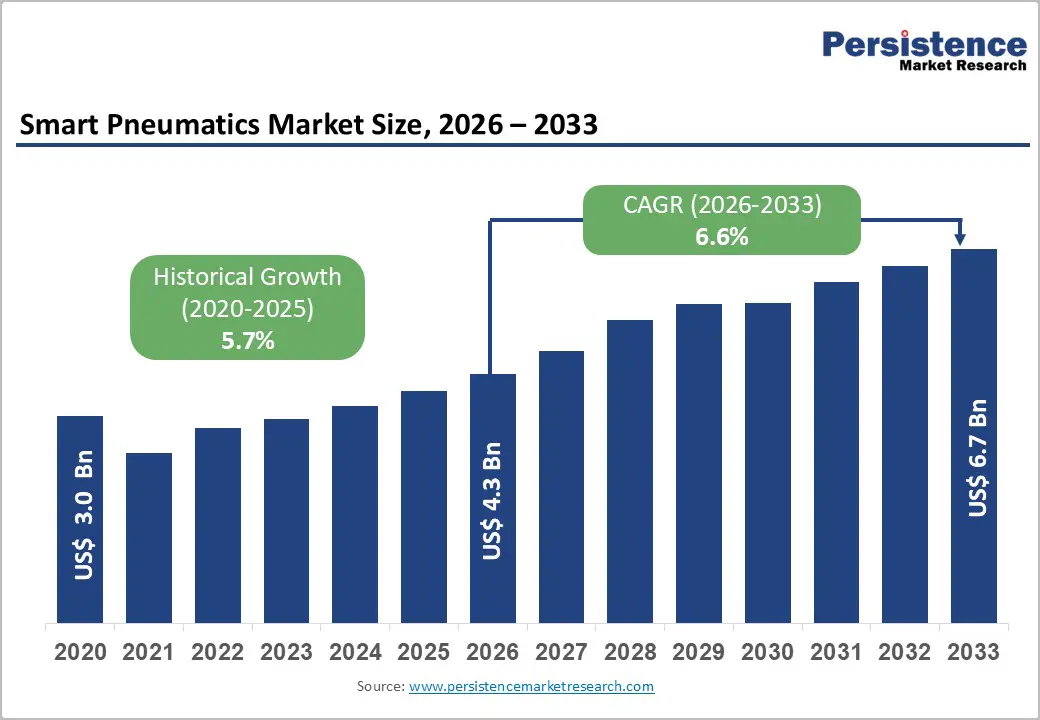

The global smart pneumatics market size is likely to be valued at US$ 4.3 billion by 2026, with further expansion to US$ 6.7 billion by 2033, growing at a CAGR of 6.6% during the forecast period from 2026 to 2033. This acceleration reflects intensifying industrial automation adoption, digital transformation initiatives across manufacturing sectors, and heightened demand for energy-efficient pneumatic solutions.

The market is propelled by increasing industrial IoT integration, stringent environmental regulations mandating operational efficiency, and the proliferation of Industry 4.0 technologies across developed and emerging economies. Strategic investments in smart factory infrastructure and the convergence of pneumatic systems with advanced control technologies underscore sustained growth momentum.

Key Industry Highlights:

- Dominant Segments and Growth Leaders: Valves command 40%+ revenue share with 5.8% CAGR; actuators fastest-growing at 7.5% CAGR. Hardware dominates at 65%+ share; software accelerates at 7.2% CAGR driven by analytics and IoT convergence.

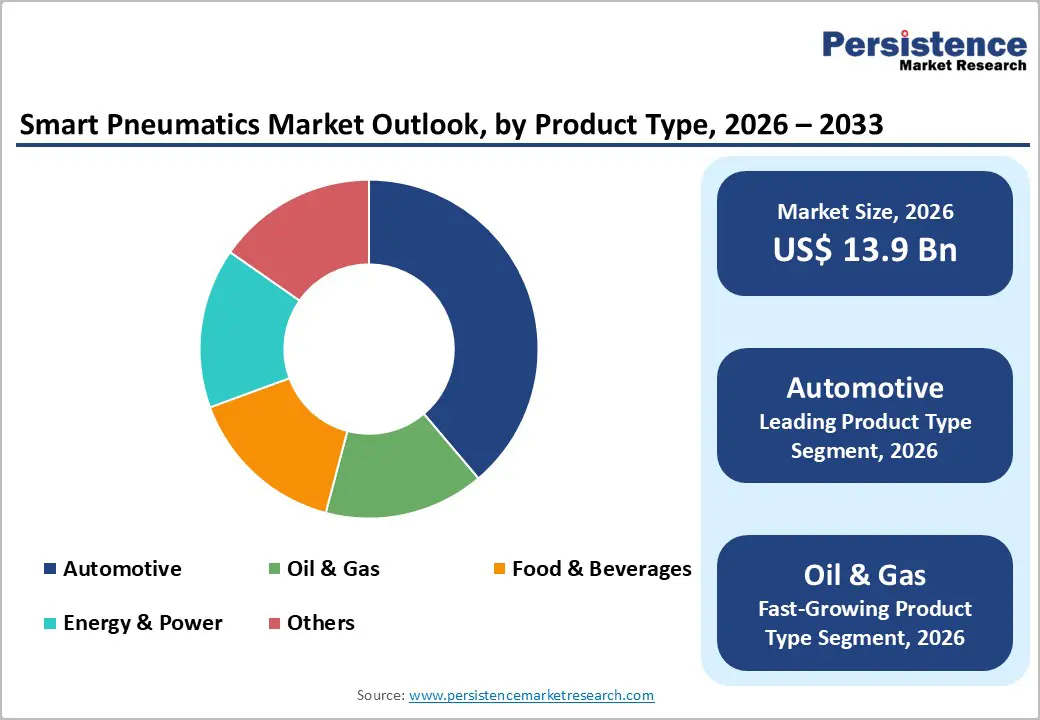

- End-Use Industry Leadership: Automotive maintains 30%+ revenue dominance; oil & gas fastest-growing at 7.5% CAGR reflecting operational intensity and regulatory compliance drivers across energy sector.

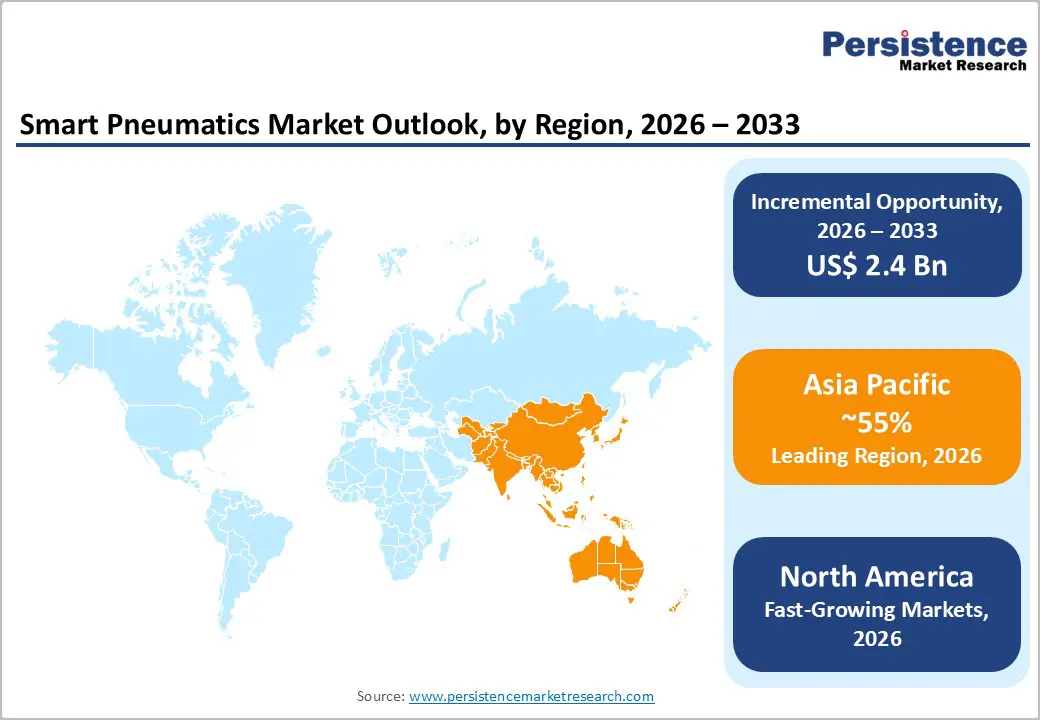

- Regional Market Dynamics: Asia Pacific dominance with 55%+ global revenue share, expanding by 7.2% CAGR. North America (28-30%) grows 6.2% CAGR amid technology leadership; Europe (22-24%) expands 5.8% CAGR through regulatory compliance drivers.

- Strategic Competitive Developments: Major players investing in digital integration, software capabilities, and geographic expansion; post-2023 initiatives prioritize predictive analytics, ecosystem partnerships, and emerging manufacturing footprints driving innovation-led market evolution.

- Market Opportunities and Investment Drivers: Emerging market manufacturing expansion (US$ 1.2-1.5 Bn opportunity), AI analytics convergence (US$800M-1.2B opportunity), and aftermarket services expansion (US$ 450-600M opportunity) represent key growth vectors for industry participants and technology investors.

- Critical Market Restraints Requiring Attention: High capital investment barriers (US$50K-500K+ deployment costs) and cybersecurity vulnerabilities pose adoption constraints, particularly affecting SMEs and developing market manufacturers requiring innovative financing and security solutions.

| Key Insights | Details |

|---|---|

|

Smart Pneumatics Market Size (2026E) |

US$ 4.3 Bn |

|

Market Value Forecast (2033F) |

US$ 6.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.7% |

Market Dynamics

Drivers - Industrial Automation and Industry 4.0 Adoption

The global industrial automation market is experiencing unprecedented growth, with manufacturers increasingly transitioning toward smart factory ecosystems and connected operational environments. According to World Economic Forum and McKinsey & Company analytics, approximately 60-70% of large manufacturing enterprises across OECD nations have initiated Industry 4.0 transformation programs. Smart pneumatic systems integrating sensors, IoT connectivity, and real-time monitoring capabilities have become foundational components within automated production lines. This technological shift is particularly pronounced in automotive manufacturing, where production lines demand precision, speed, and predictive maintenance capabilities. The integration of smart pneumatics enables real-time asset tracking, predictive maintenance scheduling, and optimization of compressed air systems, reducing operational downtime by 15-25% compared to conventional pneumatic systems. As manufacturing enterprises prioritize operational excellence and data-driven decision-making, smart pneumatic solutions have transitioned from optional upgrades to essential infrastructure, driving consistent market expansion across developed industrial economies and emerging manufacturing hubs.

Energy Efficiency Regulations and Sustainability Imperatives

Global energy consumption within industrial sectors accounts for approximately 32% of total final energy demand, with pneumatic systems consuming 10-15% of industrial electricity in manufacturing facilities. Major regulatory frameworks, including the EU Energy Efficiency Directive, US Department of Energy guidelines, and ISO 50001 standards, mandate systematic energy audits and efficiency improvements across industrial operations. Smart pneumatic systems deliver measurable energy conservation, reducing compressed air waste by 20-35% through intelligent pressure optimization, leak detection, and demand-responsive operation. Organizations implementing smart pneumatics report operational cost savings ranging from 15-25% annually, directly correlating with regulatory compliance objectives and sustainability performance metrics. This regulatory momentum has intensified post-2022, with governments implementing carbon pricing mechanisms and efficiency mandates that economically incentivize the adoption of smart pneumatic technologies. The convergence of climate commitments, operational cost pressures, and regulatory compliance requirements creates sustained demand for drivers across industrial sectors.

Restraint - High Initial Capital Investment and Implementation Complexity

Smart pneumatic system deployment requires significant upfront capital investment, with integrated solutions ranging from US$ 50,000–US$ 500,000+ depending on facility scale and automation scope. This represents a substantial financial commitment for small and medium-sized enterprises (SMEs), which constitute approximately 99% of manufacturing businesses globally but operate with constrained capital budgets. Implementation complexity, including system integration with legacy equipment, cybersecurity infrastructure development, and workforce training requirements, creates additional cost barriers and extends deployment timelines by 12-24 months. Organizations operating with shorter payback period requirements (3-5 years) may hesitate to commit capital to smart pneumatics given extended ROI realization timelines. This capital intensity disproportionately affects emerging market manufacturers and resource-constrained organizations, limiting market penetration within developing economies and smaller industrial segments.

Smart Pneumatics Market Trends and Opportunities

Smart pneumatics deployment establishes recurring revenue opportunities through aftermarket services, software licensing, predictive maintenance contracts, and system optimization services. Industrial enterprises increasingly prefer operational expenditure (OpEx) models over capital expenditure (CapEx) structures, creating demand for performance-based service contracts. Service and subscription-based models for smart pneumatic systems represent approximately 25-30% of total solution value, with recurring revenue streams growing at 8-10% CAGR. Market opportunities for smart pneumatics aftermarket services and optimization contracts is estimated at US$ 450-600 million by 2033, representing higher-margin business opportunities compared to equipment sales and driving vendor consolidation toward integrated solutions and services providers.

Smart Pneumatics Market Insights and Trends

Product Type Insights - Valves Dominate Smart Pneumatics Revenue While Actuators Drive Fastest Market Growth

Valves continue to hold a commanding position in the global smart pneumatics market, contributing more than 40% of overall revenue. As essential control elements in pneumatic systems, directional, flow, and pressure regulation valves are universally deployed across industrial applications, ensuring stable and recurring demand. The shift toward smart valves enabled with real-time flow tracking, pressure optimization, and predictive diagnostics has significantly improved system performance, yielding 20–25% gains in energy efficiency and 30–35% lower maintenance expenditures. The automotive industry remains the largest consumer, accounting for approximately 28–32% of total valve demand, as manufacturers increasingly standardize intelligent valve systems within automated production lines. Ongoing industrial modernization and capacity expansion in emerging markets are expected to support steady growth, with valve revenues forecast to increase from US$ 1.2 billion in 2026 to US$ 1.8 billion by 2033.

Conversely, actuators represent the fastest-growing segment, advancing at a 7.5% CAGR over the forecast period. Smart pneumatic actuators featuring integrated sensing, motion feedback, and performance diagnostics are gaining momentum in applications requiring high precision and flexibility, including collaborative robotics, pharmaceutical processing, and advanced automotive assembly. Accelerated automation investments are projected to lift actuator revenues from US$ 900 million in 2026 to US$ 1.5 billion by 2033, reinforcing their role as a key growth engine within the market.

Component Insights - Hardware Dominates Smart Pneumatics Revenue While Software Drives Accelerated Digital Growth

The smart pneumatics market is currently led by hardware components, which account for over 65% of total revenue. Core elements such as sensors, controllers, actuators, and valves form the physical backbone of smart pneumatic systems, driving sustained demand through replacement cycles, capacity expansions, and technology upgrades across industrial facilities. Although high upfront integration costs remain a key adoption barrier particularly for cost-sensitive manufacturers hardware revenue continues to grow steadily at a projected CAGR of 5.8% from 2026 to 2033. Competitive pressures, including commoditization and pricing constraints, are pushing manufacturers to focus on integrated hardware solutions with enhanced performance, reliability, and connectivity. Hardware revenue is expected to reach approximately US$ 2.8 billion by 2033, ensuring its continued market dominance despite rising digital alternatives.

In contrast, software represents the fastest-growing component segment, expanding at a robust 7.2% CAGR. Growth is driven by rising demand for real-time monitoring, predictive maintenance, advanced analytics, and IoT-enabled system intelligence. The increasing adoption of Software-as-a-Service (SaaS) models is lowering capital barriers and accelerating uptake among mid-sized manufacturers. Software revenue is projected to nearly double from US$ 430 million in 2026 to US$ 880 million by 2033, underscoring its growing strategic importance within smart pneumatic ecosystems.

Industry Insights - Automotive Dominates Smart Pneumatics Demand, While Oil & Gas Emerges Fastest-Growing

The automotive industry remains the dominant end-use segment in the smart pneumatics market, accounting for over 30% of total revenue. This leadership reflects the sector’s heavy reliance on pneumatic systems across assembly lines, paint shops, welding stations, and material handling operations. Automotive manufacturers are among the earliest adopters of Industry 4.0 technologies, with OEMs such as Volkswagen, Toyota, and General Motors actively integrating smart valves, actuators, and sensors to improve production efficiency, uptime, and quality control. The rapid expansion of electric vehicle manufacturing further strengthens demand by introducing new pneumatic applications and accelerating replacement cycles for legacy systems. As a result, automotive-related smart pneumatics revenue is projected to rise from approximately US$ 1.3 billion in 2026 to US$ 2.0 billion by 2033, ensuring the segment’s continued market leadership.

In contrast, oil & gas represents the fastest-growing end-use industry, expanding at an estimated 7.5% CAGR. Complex offshore and onshore operations rely on highly reliable pneumatic systems for actuation, safety, and subsea control, while stringent regulatory frameworks increasingly mandate advanced monitoring and predictive maintenance. Additionally, energy transition initiatives, including wind energy and hydrogen production, are creating new application opportunities. Collectively, food & beverages, energy & power, and other industries account for 35–38% of market revenue, supported by steady adoption across diverse industrial environments.

Regional Insights and Trends

Asia Pacific Dominates Smart Pneumatics Market Through Manufacturing Scale and Accelerating Automation

Asia Pacific dominates the global smart pneumatics market, accounting for more than 55% of total revenue, supported by rapid manufacturing expansion, accelerating industrial automation, and strong technology adoption across emerging economies. The region’s smart pneumatics revenue is estimated at approximately US$ 2.3 billion in 2026 and is projected to reach around US$ 3.9 billion by 2033, registering a robust CAGR of about 7.2%, well above the global average. China is the regional anchor, contributing roughly 48–52% of Asia Pacific revenue and expanding at nearly 7.8% CAGR, driven by its large automotive manufacturing base, electronics assembly operations, and sustained investments in industrial automation.

India and Southeast Asian countries including Vietnam, Thailand, and Indonesia are emerging as high-growth markets, together expanding at 8.5–9.2% CAGR, reflecting greenfield manufacturing investments and rising adoption of Industry 4.0 technologies. Japan and South Korea add stable demand through advanced manufacturing and precision automation. Growth is reinforced by government initiatives such as China’s “Made in China 2025” and India’s “Make in India,” alongside supply chain diversification toward cost-efficient production hubs. While regulatory frameworks differ across countries, gradual harmonization around energy efficiency and automation standards supports broader adoption. Intense competition characterizes the region, with domestic suppliers offering cost advantages and global players focusing on integrated, technology-led solutions.

North America Smart Pneumatics Market Driven by Innovation, Regulation, and Advanced Manufacturing Leadership

North America holds a strong and mature position in the global smart pneumatics market, accounting for approximately 30% of total revenue. The United States dominates the regional landscape, contributing nearly 65–70% of North American market value, supported by its advanced manufacturing ecosystem, strong innovation culture, and regulatory focus on energy efficiency. Key demand centers include automotive manufacturing hubs in Michigan, Ohio, and Tennessee, alongside aerospace, pharmaceutical, and high-value industrial production clusters. Industrial automation penetration in the region exceeds 55–60%, significantly higher than global averages, creating a favorable environment for smart pneumatic system adoption.

The North American smart pneumatics market is valued at around US$ 1.2 billion in 2026 and is projected to reach US$ 1.8 billion by 2033, registering a CAGR of 6.2%. While growth is slightly below the global average due to market maturity, the US remains the primary growth engine, with Canada and Mexico providing incremental expansion through manufacturing investments.

Growth is driven by Industry 4.0 initiatives, stringent EPA energy-efficiency and carbon-reduction regulations, and competitive pressures in automotive and aerospace sectors. Compliance with NFPA, OSHA, and efficiency standards further accelerates system modernization. The competitive landscape is characterized by established players such as Parker Hannifin, Eaton, and Bosch Rexroth, competing through innovation-led, integrated, premium solutions.

Smart Pneumatics Market Competitive Landscape

The smart pneumatics market exhibits moderate concentration with a fragmented competitive structure, leading 10 manufacturers commanding approximately 45-50% market share, while the remaining 50-55% distributed across 150-200+ competitors, including regional players, component specialists, and technology startups. Market dominance concentrates among multinational industrial conglomerates, including Parker Hannifin, Eaton, Bosch Rexroth, Festo, and SMC Corporation, which leverage established customer relationships, comprehensive product portfolios, and global distribution networks. These market leaders maintain competitive advantages through technological innovation, integrated solutions capabilities, and aftermarket service depth. Mid-tier competitors, including Aventics, Norgren, and CKD Corporation, compete through specialized solutions, regional expertise, and cost optimization strategies. Emerging competitors and startups focus on software platforms, IoT connectivity, and predictive analytics solutions, creating competitive dynamics around digital capabilities and software-enabled differentiation.

Key Industry Developments:

- In October 2025, Nomo has signed an agreement to acquire the Bosch Rexroth Customizing Center in Helsingborg and has announced the launch of a new business unit, Nomo Automation. This strategic acquisition strengthens Nomo’s position by establishing one of the most comprehensive and technically advanced offerings in linear technology and industrial automation across the Nordic region, including assembly technology capabilities.

Companies Covered in Smart Pneumatics Market

- Parker Hannifin Corporation

- Eaton Hydraulics

- Bosch Rexroth

- SMC Corporation

- Festo

- Aventics Group

- CKD Corporation

- NINGBO SMART PNEUMATIC CO., LTD.

- Norgren (IMI Precision Engineering)

- ARON Pneumatic

- Dexcraft Industrial Technology

- Ross Controls

- Pneulog Technologies

- Donghee Hydraulics

- Other Market Players

Frequently Asked Questions

The Smart Pneumatics market is estimated to be valued at US$ 4.3 Bn in 2026.

The key demand driver for the Smart Pneumatics market is the rapid adoption of industrial automation and Industry 4.0 technologies across manufacturing and process industries.

In 2026, the Asia Pacific region will dominate the market with an exceeding 55% revenue share in the global Smart Pneumatics market.

Among end-use industries, automotive has the highest preference, capturing beyond 30% of the market revenue share in 2026, surpassing other end-use industries.

Parker Hannifin Corporation, Eaton Hydraulics, Bosch Rexroth, SMC Corporation, Festo, and Aventics Group are a few leading players in the Smart Pneumatics market.