- Technology

- Smart Data Center Market

Smart Data Center Market Size, Share, and Growth Forecast, 2026 – 2033

Smart Data Center Market by Component Type (Hardware, Software, Services), Data Center Type (Enterprise Data Centers, Colocation Data Centers, Hyperscale Data Centers, Cloud Data Centers), End-User (IT & Telecom, BFSI, Healthcare, Government & Defense, Retail & E-commerce, Energy & Utilities, Media & Entertainment), and Regional Analysis for 2026-2033

Smart Data Center Market Share and Trends Analysis

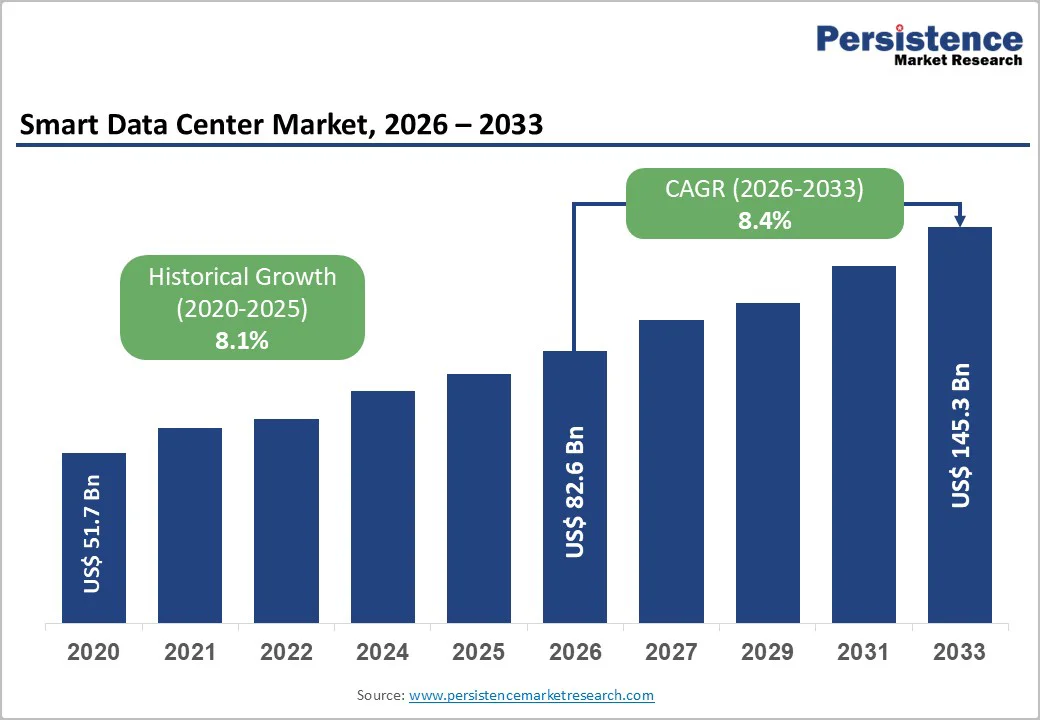

The global Smart Data Center market size is likely to be valued at US$ 82.6 billion in 2026 and is estimated to reach US$ 145.3billion by 2033, growing at a CAGR of 8.4% during the forecast period 2026−2033. Rising adoption of cloud computing, artificial intelligence (AI), and high-performance computing workloads is driving a structural transformation in the market, as enterprises and cloud service providers increasingly prioritize automation, energy efficiency, and intelligent infrastructure management to handle exponential data growth. The growing need for software-defined, sensor-enabled, and analytics-driven environments is reshaping data center operations. Governments and regulatory bodies are enforcing stricter energy-efficiency and carbon-reduction mandates, accelerating investments in smart power management, cooling optimization, and real-time monitoring solutions. Hyperscale and colocation operators are deploying intelligent systems to enhance asset utilization and lower operational expenditure, improving return on investment. Emerging economies are also expanding digital infrastructure to support e-governance, financial inclusion, and digital commerce initiatives.

Key Industry Highlights

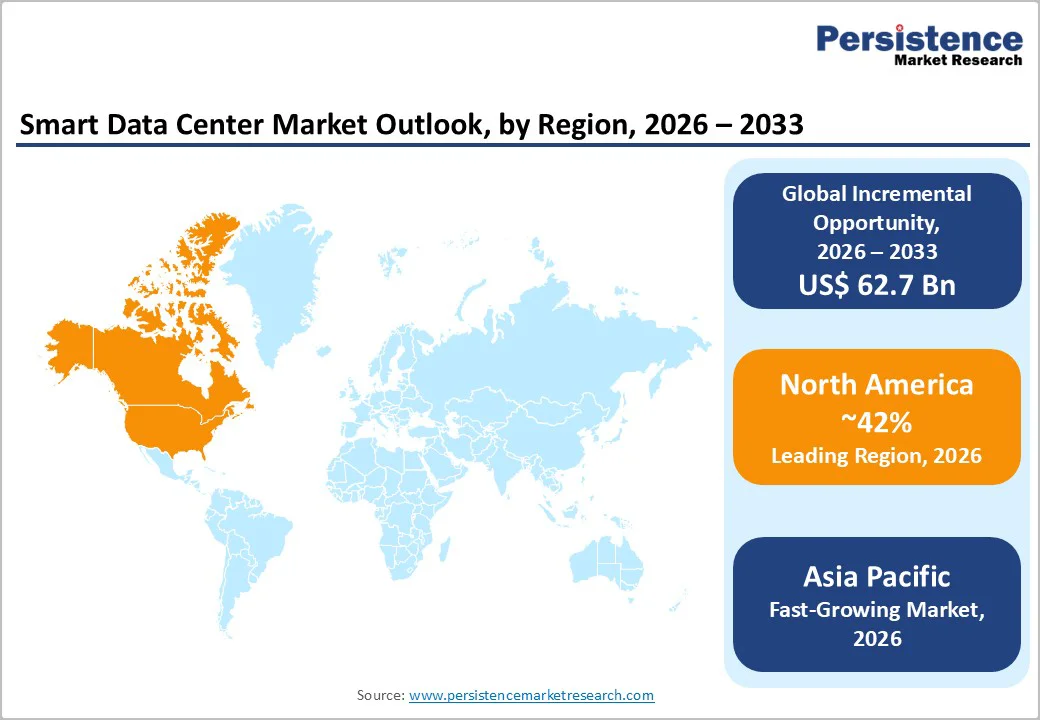

- Dominant Region: North America is set to lead in 2026 with 42% market share, propelled by the strong presence of hyperscale cloud leaders.

- Fastest-growing Regional Market: Asia Pacific is expected to be the fastest-growing market from 2026 to 2033, supported by rapid digitalization, cloud and edge adoption, hyperscale investments, and AI-enabled efficient, resilient infrastructures.

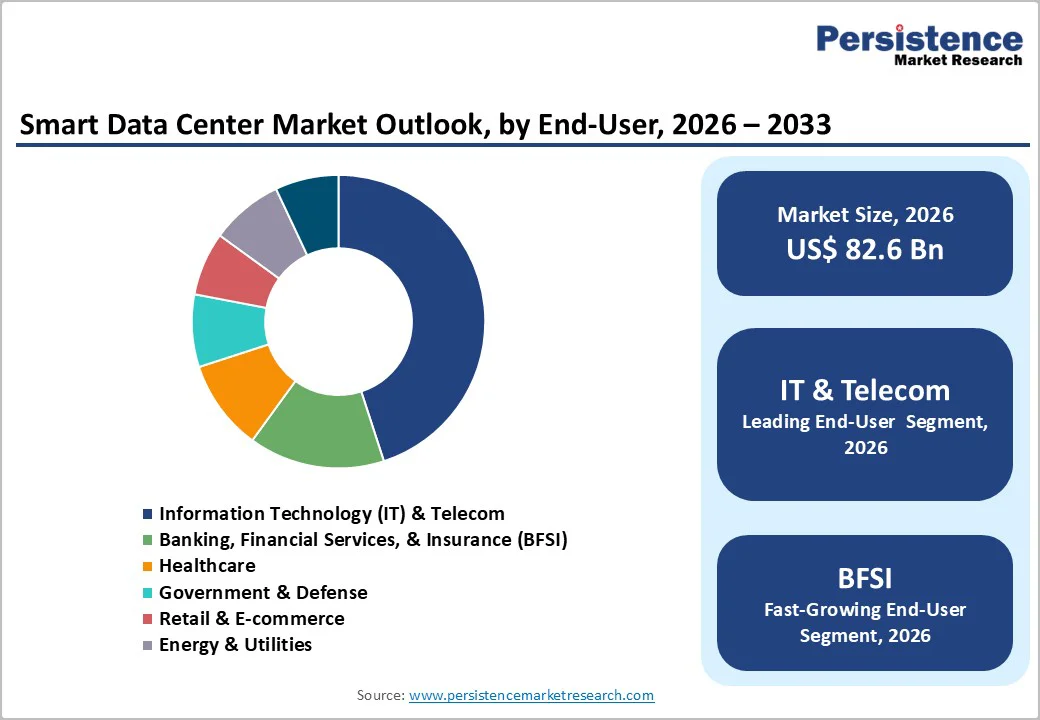

- Leading End-User: The IT and telecommunications segment is set to lead with 45% of 2026 revenues, propelled by cloud expansion, edge adoption, and high-demand scalable infrastructure.

- Fastest-growing End-User: The BFSI segment is expected to grow fastest from 2026 to 2033, fueled by a consistent need for regulatory compliance.

- June 2025: Foxconn and TECO Electric & Machinery partnered to jointly develop modular AI data center (AIDC) solutions combining Foxconn's server manufacturing expertise with TECO's electromechanical engineering and green energy capabilities.

| Key Insights | Details |

|---|---|

| Smart Data Center Market Size (2026E) | US$ 82.6 Bn |

| Market Value Forecast (2033F) | US$ 145.3Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Adoption of AI and Automation Technologies

The widening adoption of AI and automation technologies is a primary driver of the smart data center market growth due to the increasing complexity and scale of modern IT infrastructure. Increasing volumes of data from cloud services, IoT devices, and high-performance computing workloads require continuous monitoring, rapid decision-making, and predictive maintenance. AI algorithms optimize power usage, cooling efficiency, and workload distribution, reducing operational costs and improving energy efficiency. For example, a study by Stanford University found that AI-based cooling management reduced data center energy consumption by up to 40%, demonstrating tangible operational gains. Automation further enables real-time orchestration of servers, storage, and networking equipment, ensuring high availability and minimizing downtime across distributed environments.

Intelligent systems also enhance scalability and operational resilience. By automating repetitive tasks such as firmware updates, resource allocation, and anomaly detection, operators can focus on strategic planning and infrastructure expansion. AI-driven analytics provide actionable insights into equipment performance, network bottlenecks, and predictive failure risks, supporting proactive decision-making. Enterprises increasingly integrate these technologies to maintain service-level agreements, optimize capital expenditures, and meet sustainability goals. Deployment of AI and automation establishes a competitive advantage by improving efficiency, reliability, and responsiveness in high-demand computing environments.

Cybersecurity and Data Privacy Concerns

Cybersecurity and data privacy concerns represent significant restraints for smart data center adoption. The integration of AI-driven monitoring, automated management systems, and cloud-native orchestration increases exposure to potential cyber threats. Sensitive information processed across geographically distributed facilities, including financial records, healthcare data, and proprietary enterprise information, requires stringent protection. Research from IBM indicates that the average cost of a data breach reached US$ 4.45 million in 2023, demonstrating the high financial risk associated with inadequate security measures. Operational disruptions and reputational damage make organizations cautious in implementing fully automated infrastructure solutions.

Compliance with the evolving General Data Protection Regulation (GDPR) of the European Union (EU) and other sector-specific mandates further complicates operations. Smart systems collect, analyze, and transmit large volumes of operational data, which must adhere to legal frameworks such as GDPR and sector-specific regulations. Enterprises face potential penalties, litigation, and erosion of customer trust if data handling practices are insufficient. Investments in advanced encryption, identity and access management (IAM), and continuous monitoring increase capital and operational expenditure.

Emergence of Edge Computing and 5G Networks

Edge computing and 5G networks create significant demand for distributed, low-latency infrastructure that can process data close to the source. Data volumes generated by connected devices, industrial IoT, and autonomous applications are increasing rapidly, requiring intelligent systems for real-time analytics and workload optimization. Studies indicate that global data traffic from edge devices is expected to exceed 175 zettabytes annually by 2025, highlighting the need for high-performance, energy-efficient computing nodes near end-users. Smart data centers can host micro-modular and edge facilities, enabling enterprises and service providers to reduce latency, enhance network reliability, and support mission-critical operations.

Integration of edge computing with 5G networks transforms data management strategies for telecom operators, enterprises, and cloud providers. Low-latency connectivity allows interactive applications, augmented reality, and industrial automation to operate at peak efficiency. Smart data centers offer centralized orchestration for distributed edge nodes, allowing scalable deployment of AI-driven monitoring, predictive maintenance, and automated resource allocation. Investment in edge-enabled infrastructure positions operators to capture emerging revenue streams from next-generation digital services while maintaining operational efficiency and reducing network congestion.

Category-wise Analysis

Component Type Insights

The hardware segment is projected to lead with an estimated 55% revenue share in 2026. Dominance of this segment is supported by extensive deployment of intelligent power distribution units, advanced cooling systems, high-speed networking equipment, and sensors that ensure efficient operation of large-scale data centers. Hyperscale and colocation operators continue to prioritize infrastructure expansion and modernization. Investments in modular and prefabricated hardware solutions enable rapid deployment while optimizing energy consumption. For example, leading data center operators integrate AI-enabled cooling units to enhance efficiency and maintain consistent operational performance.

The software segment is anticipated to be the fastest-growing between 2026 and 2033, fueled by adoption of data center infrastructure management platforms, AI-based analytics, and automation tools. Software provides enhanced operational visibility, predictive maintenance, and real-time workload optimization, generating higher margins and recurring revenue streams. Enterprises increasingly deploy software-defined environments to orchestrate large-scale compute and storage resources. For instance, cloud operators leverage AI-driven software to dynamically balance workloads across geographically distributed data centers, improving efficiency and reducing downtime.

Data Center Type Insights

The hyperscale data center segment is likely to lead with a projected 48% of the smart data center market revenue share in 2026. Leadership is supported by rapid expansion from global cloud service providers supporting large-scale digital services, artificial intelligence workloads, and high-performance computing applications. These facilities integrate advanced automation, energy optimization, and AI-driven monitoring systems to manage massive computing loads efficiently. High-density power and cooling deployments, combined with modular infrastructure, allow operators to scale capacity rapidly while maintaining operational reliability, positioning hyperscale data centers as the primary backbone of enterprise and cloud-driven digital ecosystems.

The colocation data center segment is expected to be the fastest-growing through 2033, fueled by enterprises outsourcing infrastructure to reduce capital expenditure while supporting scalable and flexible operations. Growth is driven by demand for smart, energy-efficient environments with predictive maintenance and advanced monitoring systems. Providers differentiate offerings through uptime guarantees, security compliance, and sustainability certifications. Enterprises increasingly leverage colocation facilities to enable cloud adoption, hybrid IT architectures, and edge computing deployments, supporting rapid digital transformation while minimizing operational risk and maximizing efficiency across distributed infrastructure.

End-User Insights

The IT and telecommunications segment is slated to hold a dominant position, with an anticipated 45% of the smart data center market revenues in 2026. Leadership is powered by rapid expansion of cloud services, rollout of edge computing infrastructure, and adoption of AI-enabled network management. Enterprises and service providers increasingly leverage data-driven orchestration and automated fault detection to optimize network performance and maintain low-latency connectivity. The segment benefits from high-volume digital traffic, subscription-based service models, and continuous demand for scalable, reliable, and secure infrastructure across enterprise and consumer-facing applications.

The BFSI segment is predicted to be the fastest-growing from 2026 to 2033, boosted by regulatory mandates for real-time fraud detection, data sovereignty, and secure transaction processing. Smart data centers enable rapid deployment of mission-critical applications while maintaining strict compliance and business continuity. Integration of predictive analytics, encryption technologies, and high-availability systems allows financial institutions to manage large-scale workloads efficiently. This drives investment in scalable, secure, and automated data center infrastructure for financial services.

Regional Insights

North America Smart Data Center Market Trends

North America is positioned to dominate in 2026, projected capture an estimated 42% of the smart data center market share, reflecting structural advantages across enterprise technology ecosystems. Leadership is fueled by a high concentration of hyperscale cloud providers, financial institutions, and technology enterprises demanding advanced, scalable, and secure infrastructure. Advanced data center density, AI-driven monitoring, and modular designs support large-scale, high-performance workloads. Early adoption of software-defined environments and predictive maintenance systems accelerates deployment for production operations. Strong collaboration between multinational vendors and enterprise clients enables rapid transfer of innovation into commercial applications, strengthening sustained demand and operational efficiency.

The region is home to an advanced power management infrastructure, while boasting wide-scale adoption of software-defined environments and robust connectivity networks enabling high-speed data transfer. Enterprises increasingly integrate modular and prefabricated data center designs to reduce deployment timelines while improving resilience and scalability. Strong venture capital inflows and corporate investments in sustainable and carbon-neutral operations accelerate the shift toward fully automated and analytics-driven data center ecosystems, sustaining North America as the global benchmark for smart data center adoption and performance.

Europe Smart Data Center Market Trends

Europe represents a technologically advanced market for smart data centers, with growth fueled by stringent regulatory requirements around energy efficiency, carbon neutrality, and data privacy. Widespread adoption of AI-powered monitoring, predictive maintenance, and intelligent power management systems enhances operational efficiency and reliability. High deployment of modular and prefabricated data center designs allows operators to optimize space utilization and accelerate infrastructure rollout in urban and high-density areas. Strong integration between industrial, financial, and research sectors enables cross-industry utilization of cloud-native platforms, edge computing architectures, and high-performance computing workloads.

Expansion is reinforced by investment incentives for green data centers and renewable energy integration, including support for low-carbon power and advanced cooling solutions. Strategic placement of hyperscale and colocation facilities across Germany, France, the Netherlands, and the Nordics ensures high connectivity and operational resilience. European technology vendors emphasize cybersecurity, compliance, and sustainable operations, positioning the continent as a benchmark for environmentally responsible, resilient, and regulatory-compliant smart data center adoption. Rising demand from enterprise, government, and cloud operators drives continued modernization and innovation throughout Europe.

Asia Pacific Smart Data Center Market Trends

Asia Pacific is projected to emerge as the fastest-growing regional market for smart data centers during the 2026-2033 forecast period, powered by rapid digitalization, expanding cloud adoption, and rising demand for edge computing infrastructure. Growth is fueled by large-scale investments in hyperscale and colocation facilities across China, India, and Singapore to support e-commerce, 5G rollout, financial services, and government digital initiatives. Enterprises increasingly adopt modular and prefabricated data center designs to accelerate deployment timelines while ensuring operational resilience. Early-stage adoption of AI-driven monitoring, predictive maintenance, and software-defined environments enhances energy efficiency and reliability in high-density deployments.

Regional market expansion is further reinforced by strong public-private collaboration, including national data center programs, smart city initiatives, and industry-specific infrastructure policies. Technology vendors and service providers actively expand footprints and customize solutions to address local power, cooling, and connectivity requirements. Adoption of high-performance computing workloads, cloud-native orchestration platforms, and analytics-driven operations positions Asia Pacific as a critical growth engine for next-generation, intelligent data center ecosystems. Rising demand from enterprises, hyperscale operators, and government agencies ensures sustained investment in scalable, energy-efficient, and automated infrastructure solutions.

Competitive Landscape

The global smart data center market landscape is moderately consolidated, with key players such as Vertiv Group Corp., Schneider Electric, Eaton, DAIKIN INDUSTRIES, Ltd., Rittal Pvt. Ltd., Siemens, ABB, Cisco Systems Inc., Dell Technologies, IBM Corporation, and Hewlett Packard Enterprise Development LP controlling a significant share through integrated hardware-software portfolios. Market leaders leverage global supply chains, strong research and development capabilities, and long-term enterprise contracts to maintain competitive positioning.

These companies offer end-to-end solutions combining power management, cooling, networking, and intelligent monitoring systems, driving innovation through AI-driven automation, predictive analytics, and modular infrastructure. Their focus on energy efficiency, resilience, and scalability addresses growing enterprise demands, hyperscale operations, and edge computing requirements, while strategic partnerships and global expansion strengthen market influence and support digital transformation and sustainability initiatives.

Key Industry Developments

- In December 2025, Delta Electronics and the National University of Singapore (NUS) signed a three-year Memorandum of Understanding (MOU) to develop advanced sustainable data center technologies, focusing on smart energy systems, thermal management, and modular infrastructure for tropical environments..

- In July 2025, ABB introduced the SACE Emax?3 circuit breaker to enhance resilience and energy efficiency in AI data centers and advanced manufacturing.

- In June 2025, Siemens launched a prefabricated, turnkey modular data center module with customizable, plug?and?play units to accelerate deployment and flexibility for edge and enterprise infrastructure.

Companies Covered in Smart Data Center Market

- Vertiv Group Corp.

- Schneider Electric

- Eaton.

- DAIKIN INDUSTRIES, Ltd.

- Rittal Pvt. Ltd.

- Siemen

- ABB

- Cisco Systems Inc.

- Dell Technologies

- IBM Corporation

- Hewlett Packard Enterprise Development LP

Frequently Asked Questions

The global smart data center market is projected to reach US$ 82.6 billion in 2026.

Surging AI and cloud workloads, explosive data growth, and the growing need for energy-efficient, automated infrastructure to support low-latency digital services and 5G-enabled applications drive the market.

The market is poised to witness a CAGR of 8.4% from 2026 to 2033.

Key market opportunities include AI-optimized and hyperscale infrastructure, edge data centers for low-latency applications, and sustainability-focused retrofits integrating renewables and advanced energy management solutions.

Some of the key market players include Vertiv Group Corp., Schneider Electric, Eaton, and DAIKIN INDUSTRIES.