- Medical Devices

- Ingestible Smart Pills Market

Ingestible Smart Pills Market Size, Share, Trends, Growth, and Regional Forecast, 2026 - 2033

Ingestible Smart Pills Market by Component (Smart Pills, Workstation), Application (Imaging, Monitoring) End-user (Hospitals, Clinics, Research Institutes, Home Healthcare) and Regional Analysis from 2026 - 2033

Ingestible Smart Pills Market Share and Trends Analysis

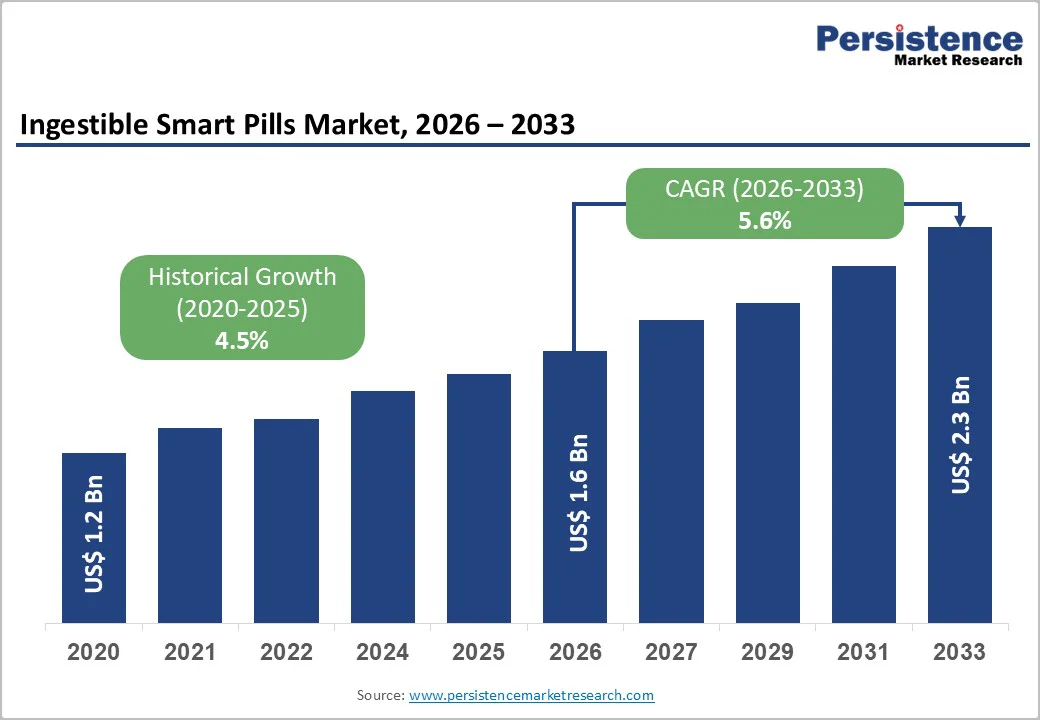

The global ingestible smart pills market size is estimated to grow from US$ 1.6 billion in 2026 to US$ 2.3 billion by 2033. The market is projected to record a CAGR of 5.6% from 2026 to 2033.

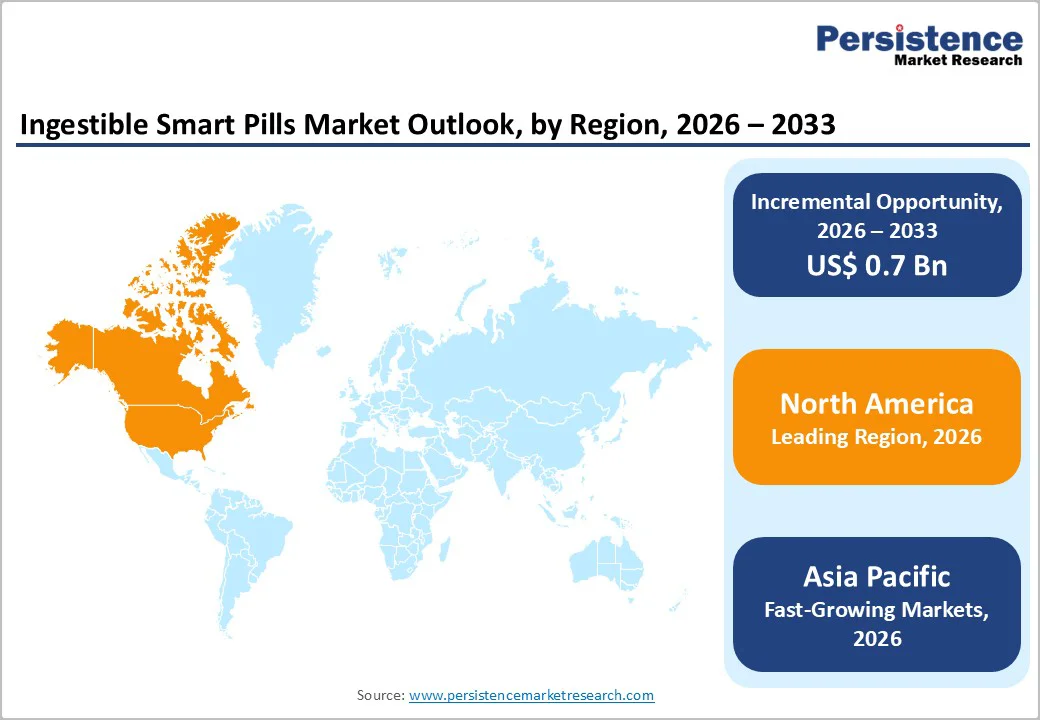

The market is growing steadily, fueled by rising hospital-acquired infections, increasing patient admissions, and stricter infection control regulations. North America leads due to advanced healthcare IT, early adoption of digital platforms, and strong regulatory oversight. Asia Pacific is the fastest-growing region, driven by healthcare digitization, expanding hospital capacity, government initiatives, and growing awareness of data-driven monitoring solutions.

Key Industry Highlights:

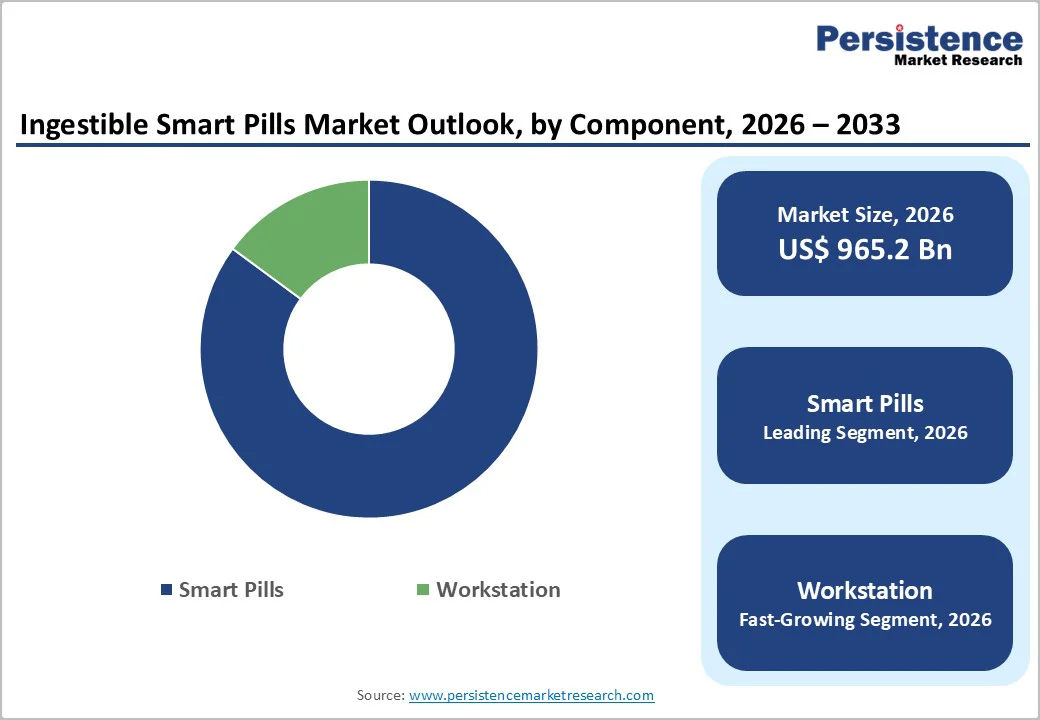

- Dominant Segment: Smart pills lead the market with an estimated 85.1% share in 2025, driven by demand for capsule endoscopy, ingestible sensors for physiological monitoring, and growing adoption of minimally invasive diagnostic and monitoring solutions across hospitals and clinics.

- Dominant Region: North America dominates with 44.1% share in 2025, supported by advanced healthcare IT infrastructure, early adoption of digital health technologies, and strong regulatory oversight. Asia Pacific is the fastest-growing region, fueled by healthcare digitization, hospital expansion, and increasing awareness of patient safety and data-driven monitoring.

- Market Drivers: Growth is fueled by the rising incidence of gastrointestinal and chronic diseases, increasing hospital admissions, demand for minimally invasive diagnostics, and the adoption of data-driven monitoring and adherence solutions.

- Market Opportunity: Key opportunities include AI-enabled and cloud-integrated capsule systems, predictive analytics for patient monitoring, expansion into emerging healthcare markets, integration with remote care platforms, and increasing demand for scalable smart pill solutions among small and mid-sized hospitals.

| Key Insights | Details |

|---|---|

|

Ingestible Smart Pills Market Size (2026E) |

US$ 1.6 Bn |

|

Market Value Forecast (2033F) |

US$ 2.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Dynamics

Driver - Increasing Hospital Admissions and Outpatient Procedures

The increasing utilization of hospital services is a key driver for the Ingestible Smart Pills Market, as higher patient volumes heighten the demand for advanced diagnostics and monitoring technologies. In the United States, data from the National Hospital Care Survey (NHCS) show that hospital inpatient and outpatient care activity is systematically tracked to monitor use patterns, reflecting sustained engagement with hospital services nationally. While precise annual admission counts vary, indicators such as the persistence of hospital care utilization and robust ED and inpatient reporting frameworks demonstrate ongoing demand for hospital-based diagnostics and care delivery platforms, underscoring the need for innovative minimally invasive tools like ingestible smart pills to improve patient outcomes.

Outpatient visits have shown significant historical growth in the United States, exemplified by trends in the National Hospital Ambulatory Medical Care Survey (NHAMCS), where outpatient department (OPD) visits increased from approximately 83.3 million in 2000 to an estimated 125.7 million by 2011, indicating rising outpatient service utilization over time. Such expansion of outpatient procedures and diagnostic encounters places a premium on less invasive and ambulatory-friendly technologies. Technologies like ingestible smart pills, which support remote monitoring and non-invasive diagnostic workflows, align with this shift toward outpatient care delivery, enabling clinicians to manage rising patient loads and procedural demands without increasing inpatient burdens.

Restraints - High Cost of Smart Pill Devices and Associated Systems

The high cost of ingestible smart pills and associated systems is a significant restraint on broader market adoption. Real-world data show that advanced capsule endoscopy procedures, a core component of the ingestible smart pills category, can cost between $500 and $2,800 per procedure in healthcare systems across Asia and the West, substantially higher than many traditional diagnostic tests. In some regions, the total average cost, including device, monitoring, and analysis, can exceed $1,700 to $2,400 per procedure, reflecting the premium pricing of these technologies compared to conventional alternatives like standard endoscopy or imaging. These elevated prices often exceed patient and facility budget thresholds, especially where insurance coverage is limited or inconsistent, constraining uptake.

Government and payer data further illustrate financial barriers: in the U.S., historical Medicare reimbursement rates for capsule endoscopy procedures have ranged around $750–$1,189 for combined physician and technical components, indicating that even public payers recognize higher costs relative to simpler services. Many healthcare systems in low and middle-income countries lack comprehensive reimbursement mechanisms for these advanced diagnostics, requiring patients to pay out of pocket, which reduces accessibility and deters clinicians from recommending them. The cumulative effect of high device costs, additional equipment investment, and uncertain reimbursement policies limits the market’s growth in price-sensitive regions and among smaller healthcare providers.

Opportunity - Development of AI-Enabled and Cloud-Integrated Capsule Systems

The development of AI-enabled and cloud-integrated capsule systems represents a major growth opportunity for the Ingestible Smart Pills Market by enhancing diagnostic accuracy and efficiency. In traditional capsule endoscopy, reviewing full video datasets can take clinicians 30–90 minutes. In contrast, AI algorithms can reduce this review time to under 30 minutes, improving workflow and freeing physician time for higher-value activities. AI-enhanced systems are being increasingly researched and implemented to assist in lesion detection and diagnostic interpretation, supporting faster, more reliable clinical decisions and reducing the burden of manual analysis.

Cloud integration expands the utility of ingestible smart pills by enabling real-time transmission and secure storage of patient data, which supports remote monitoring and longitudinal analysis. Health systems adopting AI and cloud platforms have documented improvements in operational outcomes. For example, combining advanced computing with cloud infrastructure has been linked to up to 58% improvement in patient outcome predictions and a 51% reduction in preventable hospital readmissions in broader healthcare contexts. These capabilities allow ingestible smart pill systems to move beyond diagnostic snapshots toward continuous, analytics-driven patient care, creating opportunities for predictive monitoring and personalized medicine.

Category-wise Analysis

By Component Insights

Smart pills dominate with an 85.1% share in 2025, as they are the central product that provides direct clinical benefits through non-invasive diagnostics and monitoring. Capsule endoscopy devices allow detailed visualization of the gastrointestinal tract without sedation or invasive procedures, making them highly preferred by both patients and clinicians. These smart pills incorporate miniaturized cameras, sensors, and wireless technology to capture and transmit real-time physiological data such as pH levels, pressure, or medication adherence, enabling continuous internal monitoring. With the rising prevalence of gastrointestinal disorders and chronic diseases, hospitals increasingly rely on these devices for accurate, patient-friendly diagnostics, reinforcing the dominance of smart pills over workstations or peripheral systems in clinical practice.

By Application Insights

The imaging application dominates the ingestible smart pills market because it provides a critical, non-invasive diagnostic solution that traditional procedures often cannot achieve. Capsule endoscopy, the main imaging use of smart pills, allows visualization of the entire gastrointestinal tract, including areas beyond the reach of standard endoscopes. As the capsule travels through the digestive system, it captures thousands of high-resolution images, helping detect conditions such as obscure gastrointestinal bleeding, Crohn’s disease, and small intestine tumors. Clinical studies show that capsule endoscopy often yields a higher diagnostic yield than traditional imaging techniques. Its non-invasive nature, lack of sedation, and ability to provide comprehensive internal visualization with minimal patient discomfort have made imaging the dominant application in this market.

Regional Insights

North America Ingestible Smart Pills Market Trends

North America dominates the ingestible smart pills market with 44.1% share in 2025, due to its advanced healthcare infrastructure, high technology adoption, and strong clinical demand. Hospitals and specialty clinics in the United States and Canada widely implement electronic health records, digital health platforms, and non-invasive diagnostic tools, facilitating the adoption of smart pills. Approximately 60 million U.S. adults experience digestive disorders annually, driving the need for capsule endoscopy and ingestible sensors. The region benefits from well-established reimbursement frameworks, supportive regulatory policies, and physician preference for minimally invasive procedures, enabling broader patient access. Combined with continuous investment in medical research, robust hospital networks, and high patient awareness, these factors reinforce North America’s leadership, making it the largest and most mature market for ingestible smart pills globally.

Europe Ingestible Smart Pills Market Trends

Europe is an important region in the ingestible smart pills market because of its high burden of gastrointestinal (GI) diseases and strong healthcare infrastructure, which drive demand for advanced diagnostics. Digestive disorders affect over 300 million people across Europe, and incidence and mortality from digestive cancers have risen substantially over recent years, increasing the need for effective, non-invasive diagnostic tools like smart pills.

Europe’s healthcare systems, including universal coverage in many countries, support early disease detection and non-invasive procedures, promoting technologies such as capsule endoscopy. Nations like Germany, France, and the United Kingdom actively integrate advanced GI diagnostics into clinical practice, reflecting Europe’s emphasis on precision imaging and preventive care for digestive diseases.

Asia Pacific Ingestible Smart Pills Market Trends

Asia Pacific is the fastest-growing region in the ingestible smart pills market, largely due to its expanding healthcare infrastructure, rising chronic disease burden, and rapid adoption of digital health technologies. The region’s large and aging population, with over 3.7 billion residents and growing elderly cohorts, creates strong demand for advanced diagnostics and monitoring solutions that reduce the need for invasive procedures and improve patient outcomes. Health systems across China, India, and Southeast Asia are integrating digital tools such as telemedicine, mobile health, and AI diagnostics, driven by government initiatives to modernize care and expand access, which supports the uptake of smart pill technologies. Internet and smartphone penetration are high, enabling remote monitoring and patient engagement. Overall, increasing hospital expansion, digitization efforts, and rising disease incidence position the Asia Pacific as a dynamic growth hub for ingestible smart pills.

Competitive Landscape

Leading smart pill providers focus on device innovation, real-time monitoring, and clinical training, collaborating with hospitals and healthcare systems. By enabling continuous internal diagnostics, seamless data transmission, and integration with electronic health records, they improve patient outcomes, support early disease detection, enhance workflow efficiency, and drive adoption, fueling growth in the global ingestible smart pills market.

Key Industry Developments:

- In February 2024, BodyCAP developed an ingestible thermometer that connects to smartphones, enabling real-time monitoring of core body temperature. The device allows for users and healthcare professionals to continuously and remotely track temperature, enhancing patient monitoring during medical procedures, athletic training, or critical care scenarios.

- In January 2024, AnX Robotica announced FDA clearance for ProScan™, an AI-assisted reading tool designed for small bowel video capsule endoscopy. The tool provided automated analysis of capsule endoscopy images, enhancing diagnostic accuracy and reducing review time for clinicians.

Companies Covered in Ingestible Smart Pills Market

- Medtronic plc

- CapsoVision, Inc.

- Olympus Corporation

- IntroMedic Co., Ltd.

- BodyCap‑Medical

- Philips Healthcare / Koninklijke Philips N.V.

- AnX Robotics

- Bio‑Images Research Limited

- Others

Frequently Asked Questions

The global ingestible smart pills market is projected to be valued at US$ 1.6 Bn in 2026.

Rising gastrointestinal disorders, demand for non-invasive diagnostics, hospital admissions growth, healthcare digitization, and adoption of real-time monitoring drive market growth.

The global ingestible smart pills market is poised to witness a CAGR of 5.6% between 2026 and 2033.

AI-enabled capsule systems, cloud integration, predictive analytics, telehealth integration, emerging markets expansion, and scalable solutions for hospitals present key market opportunities.

Medtronic plc, CapsoVision, Inc., Olympus Corporation, IntroMedic Co., Ltd., BodyCap‑Medical, Koninklijke Philips N.V.