- Advanced Materials

- Silicon Wafer Reclaim Market

Silicon Wafer Reclaim Market Size, Share, and Growth Forecast, 2026 - 2033

Silicon Wafer Reclaim Market by Wafer Diameter (150 mm (legacy), Others), End-use Application (Foundries, IDMs, Automotive Electronics, Others), Reclaim Process Technology (Chemical Stripping, Others), and Regional Analysis for 2026 - 2033

Silicon Wafer Reclaim Market Share and Trends Analysis

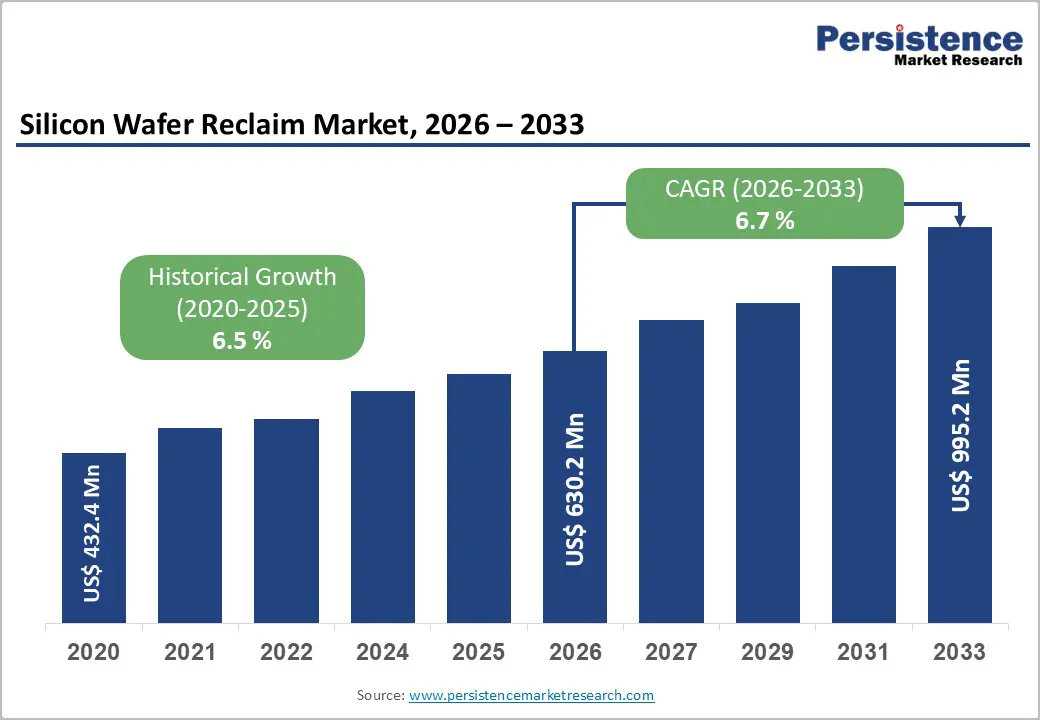

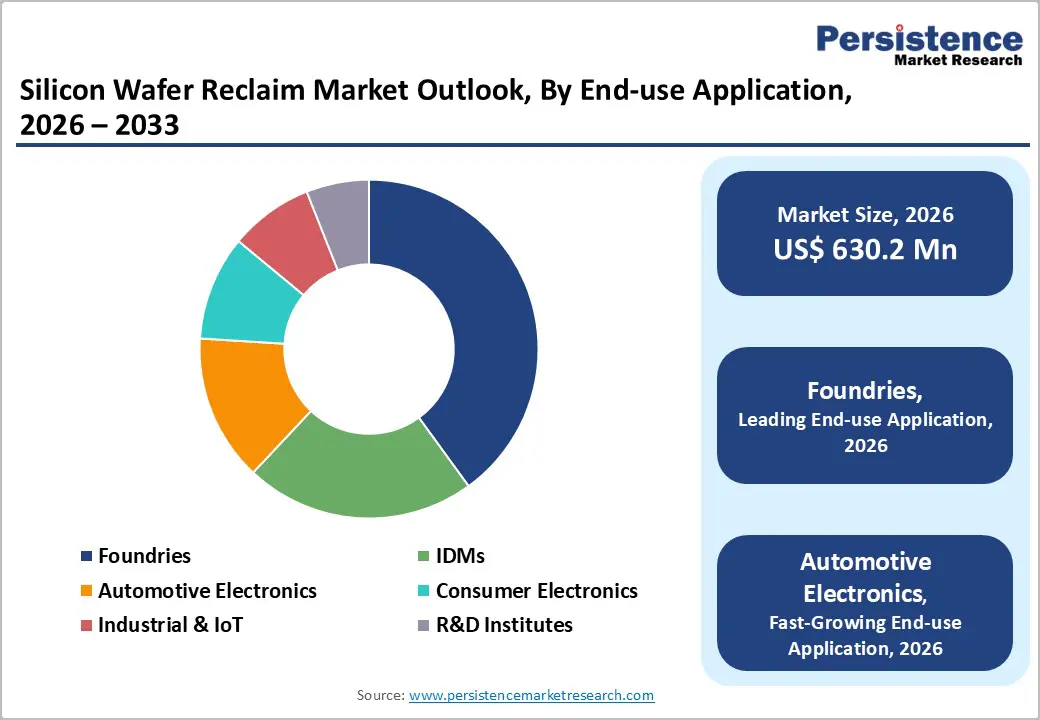

The global silicon wafer reclaim market size is likely to be valued at US$630.2 million in 2026 and is projected to reach US$995.2 million by 2033, growing at a CAGR of 6.7% during the forecast period 2026 - 2033, driven by rising demand for cost-efficient semiconductor manufacturing and sustainability-led initiatives across fabs. Increasing adoption of wafer reclaim services in foundries and integrated device manufacturers (IDMs) is improving operational efficiency.

Additionally, growth in advanced semiconductor nodes, coupled with rising silicon wafer consumption in automotive electronics and IoT applications, is accelerating reuse cycles. The industry benefits from circular economy adoption and semiconductor supply chain optimization.

Key Industry Highlights:

- Wafer Diameter Leadership: The 200 mm wafers are set to lead with 50% share in 2026, while 300 mm wafers are expected to be the fastest-growing at 7.2% CAGR through 2033, driven by advanced-node semiconductor production.

- End-use Application Split: Foundries are projected to dominate with 40% share in 2026, whereas automotive electronics will be the fastest-growing at 6.9% CAGR from 2026 to 2033, supported by EV and ADAS semiconductor demand.

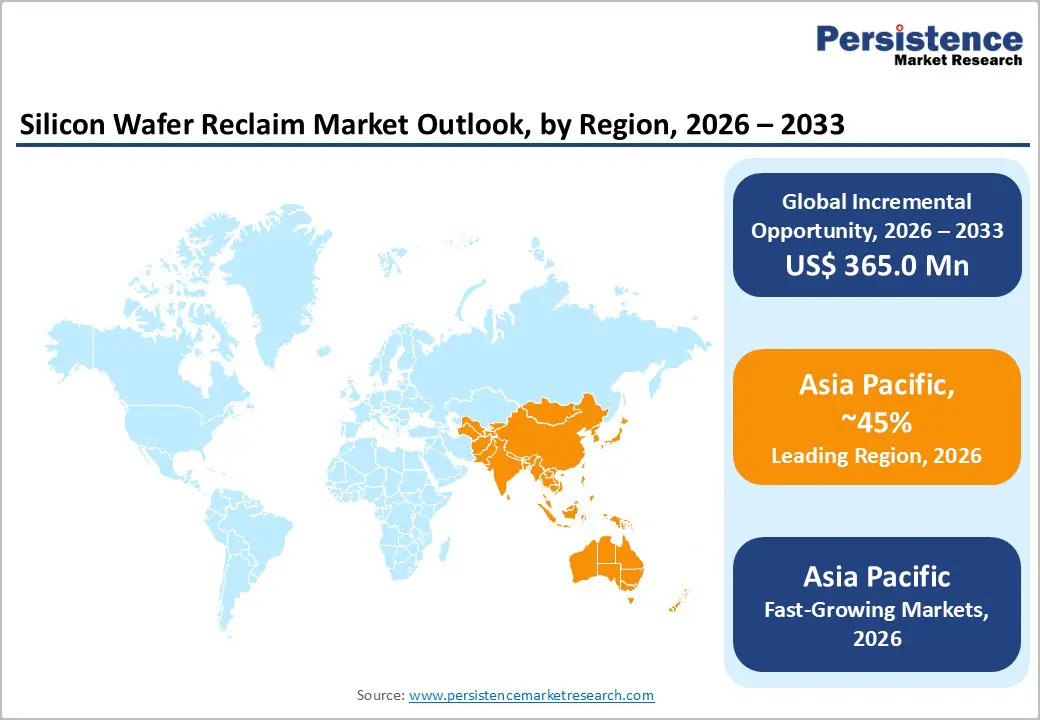

- Regional Leadership: Asia Pacific is expected to hold 47% share in 2026, while also registering the fastest growth at 7.1% CAGR through 2033, led by Taiwan, China, and Japan's semiconductor manufacturing strength.

- Technology Trend: Chemical stripping & CMP processes will lead with 42% share in 2026, while plasma etching is projected as the fastest-growing segment at 7.3% CAGR due to precision and sustainability needs.

- Industry Transformation: Increasing shift toward circular semiconductor manufacturing and closed-loop wafer reuse is reshaping long-term industry structure, improving material efficiency and ESG compliance across global supply chains.

DRO Analysis

Driver - Rising Semiconductor Demand and Cost Optimization in Fabrication Ecosystems

The global semiconductor industry, valued at over US$500 billion according to the Semiconductor Industry Association (SIA), continues to expand due to AI, 5G, and automotive electrification. Wafer manufacturing is capital-intensive, with silicon wafer costs accounting for a significant portion of fabrication expenses.

As a result, manufacturers are increasingly adopting silicon wafer reclaim processes to reuse test wafers and monitor wafers. This reduces raw material consumption by up to 30-40% in certain production environments. Foundries and IDMs are actively integrating reclaim cycles into production lines to control costs and improve sustainability metrics. This shift is significantly boosting demand for wafer reclaim services, especially in Asia Pacific manufacturing hubs.

Restraint - High Process Complexity and Yield Loss Risks in Reclaim Operations

Despite its benefits, wafer reclaiming involves complex chemical, mechanical, and plasma-based processes that can introduce surface defects or contamination risks if not controlled precisely. Yield loss remains a key concern, particularly for advanced node wafers used in 300 mm production. Equipment costs for chemical stripping and CMP polishing systems are high, limiting adoption among smaller fabs.

Additionally, stringent quality requirements from semiconductor OEMs restrict the reuse of reclaimed wafers in high-performance applications, limiting market penetration in advanced nodes. These constraints reduce scalability and increase dependency on highly specialized service providers.

Opportunities - Expansion of Circular Semiconductor Manufacturing and Sustainable Fab Models

The semiconductor industry is increasingly aligning with ESG frameworks and circular manufacturing principles. According to global sustainability initiatives supported by organizations such as the International Energy Agency (IEA), semiconductor fabs are under pressure to reduce material waste and carbon footprint. This creates a significant opportunity for silicon wafer reclaim market growth, particularly in Asia and North America.

Emerging fabs are expected to increase reclaim utilization rates by 20-25% by 2030. Additionally, government-backed semiconductor localization programs in India, the U.S., and the EU are expected to expand demand for cost-efficient wafer reuse systems, creating a long-term market opportunity exceeding US$250-300 million in incremental value potential.

Category-wise Analysis

Wafer Diameter Insights

The 200 mm wafer segment is expected to lead the silicon wafer reclaim market with an estimated 50% share in 2026, supported by its strong utilization in analog, power devices, and MEMS applications. Its dominance is likely driven by mature fabrication ecosystems and cost-efficient reclaim cycles, particularly across established semiconductor hubs in Japan and Taiwan. In many legacy and specialty fabs, 200 mm lines are still expected to remain operational due to stable demand in automotive and industrial electronics, sustaining consistent wafer reuse requirements.

In contrast, the 300 mm wafer segment is estimated to be the fastest-growing at around 7.2% CAGR through 2033, driven by accelerating demand for AI chips, high-performance computing, and advanced logic nodes. Industry expansion in data centers and AI accelerator production is expected to increase reliance on 300 mm wafers for advanced manufacturing. Leading-edge foundries are likely to expand the reuse of monitor wafers to optimize cost structures, thereby strengthening demand for precision-based reclaim technologies capable of supporting ultra-sensitive advanced nodes.

End-use Application Insights

Foundries are expected to remain the dominant end-use segment with an estimated 40% market share in 2026, driven by large-scale outsourced semiconductor manufacturing activities. This leadership is likely supported by the continuous expansion of global fabrication capacity, particularly across Asia Pacific and the U.S. ecosystem, supported by policy incentives such as semiconductor localization programs. Foundries are expected to increasingly depend on reclaimed wafers for process calibration, yield optimization, and equipment testing, making wafer reuse an integral part of cost management strategies.

Automotive electronics is projected to be the fastest-growing segment at an estimated 6.9% CAGR through 2033, supported by rapid EV penetration and ADAS integration trends. The increasing semiconductor content per vehicle is expected to significantly expand wafer consumption cycles across automotive supply chains. Ongoing EV manufacturing scale-up initiatives in Europe, China, and the U.S. are likely to further reinforce this demand. Additionally, industrial IoT and consumer electronics are expected to maintain steady growth, driven by device miniaturization and higher testing intensity requirements.

Reclaim Process Technology Insights

Chemical stripping technology is expected to dominate the wafer reclaim process segment with an estimated 42% market share in 2026, owing to its established efficiency in removing dielectric and metal layers while preserving wafer integrity. Its widespread adoption is likely supported by long-standing integration into high-volume manufacturing environments across Asia Pacific semiconductor fabs. This method is expected to remain the preferred choice for cost-effective reclaim operations across both mature and advanced wafer nodes.

In contrast, plasma etching technology is projected to be the fastest-growing segment at approximately 7.3% CAGR through 2033, driven by rising demand for ultra-precise wafer surface preparation in advanced semiconductor nodes below 7nm. The ongoing global expansion of AI, HPC, and advanced logic chip production is expected to accelerate the adoption of high-precision etching solutions. CMP polishing and cleaning & inspection technologies are also likely to gain gradual traction as fabs increasingly focus on defect minimization, sustainability compliance, and reduction of chemical waste in line with evolving ESG expectations.

Regional Insights

North America Silicon Wafer Reclaim Market Trends

North America is expected to hold an estimated 22% share of the global silicon wafer reclaim market in 2026, driven by a mature semiconductor ecosystem and strong policy support. Growth is supported by rising adoption of wafer reclaim services to reduce fabrication costs and strengthen supply chain resilience. The CHIPS and Science Act is likely to further accelerate domestic semiconductor expansion. Demand is also increasing for high-precision reclaim systems aligned with AI and advanced-node manufacturing needs.

U.S. Silicon Wafer Reclaim Market Trends

The U.S. is estimated to account for 45% of the North American market in 2026, supported by large-scale semiconductor investments in Arizona, Texas, and Oregon. Expansion of advanced fabs is expected to increase wafer reuse intensity. Recent fab localization initiatives and AI chip production scale-ups are reinforcing reclaim demand. Strong innovation hubs in Silicon Valley and Austin are also driving automation-led wafer reclaim technology adoption.

Canada Silicon Wafer Reclaim Market Trends

Canada is projected to hold around 10% share within North America in 2026, supported by semiconductor R&D and design-focused activities. Growth is gradual but steady, driven by increasing participation in advanced materials and photonics research. Collaboration in AI hardware development is expected to support incremental demand. However, limited large-scale fabrication restricts broader reclaim market penetration compared to the U.S.

Europe Silicon Wafer Reclaim Market Trends

Europe is estimated to account for approximately 18% of the global silicon wafer reclaim market in 2026, supported by automotive semiconductor demand and sustainability regulations. Growth is driven by increased adoption of wafer reuse strategies to reduce environmental impact. The EU Chips Act is expected to strengthen regional semiconductor manufacturing and reclaim infrastructure. EV expansion and industrial automation further support demand growth.

Germany Silicon Wafer Reclaim Market Trends

Germany is projected to represent around 40% of the European market in 2026, driven by its strong automotive semiconductor ecosystem. EV manufacturing growth is increasing wafer consumption and reuse cycles. Ongoing investments in semiconductor fabs are reinforcing demand for reclaim services. Industrial automation trends are also supporting the adoption of advanced wafer processing technologies.

Netherlands Silicon Wafer Reclaim Market Trends

The Netherlands is estimated to hold around 20% share within Europe in 2026, supported by its semiconductor equipment and precision engineering ecosystem. Its role in lithography and tooling supports indirect reclaim demand. Expansion in high-tech manufacturing clusters is strengthening its position. Recent semiconductor equipment growth is expected to enhance wafer processing integration.

Asia Pacific Silicon Wafer Reclaim Market Trends

Asia Pacific is expected to dominate the global market with an estimated 45% share in 2026, driven by large-scale semiconductor manufacturing and foundry concentration. Growth is supported by cost-efficient production infrastructure and strong government incentives. Rising adoption of circular semiconductor manufacturing is further boosting wafer reclaim demand. The region continues to lead advanced chip fabrication globally.

China Silicon Wafer Reclaim Market Trends

China is projected to account for around 40% of the Asia Pacific market, driven by rapid semiconductor capacity expansion. Government initiatives for self-sufficiency are accelerating wafer usage and reclaim adoption. Investments in advanced fabs are strengthening demand for reuse systems. Growth in consumer electronics and industrial IoT is further supporting market expansion.

Taiwan Silicon Wafer Reclaim Market Trends

Taiwan is estimated to hold approximately 20% share within Asia Pacific, supported by its leadership in advanced foundry services. High demand for 300 mm wafer production is driving reclaim adoption. Expansion in AI and high-performance computing chips is reinforcing this trend. Strong focus on process optimization and sustainability is strengthening wafer reuse integration.

Competitive Landscape

The global silicon wafer reclaim market is moderately consolidated, with key players such as Shin-Etsu Chemical, Sumco, Siltronic AG, GlobalWafers, and Pure Wafer estimated to hold 55% share in 2026. Their leadership is driven by strong foundry relationships, high-precision reclaim capabilities, and integration of chemical stripping, CMP, and plasma etching technologies. Continuous R&D investment and process reliability remain key differentiators in advanced semiconductor supply chains.

Regional and niche players such as Silicon Quest International, Ultrasil Corporation, and Wafer Works focus on specific wafer sizes and localized demand, particularly in 200 mm ecosystems. High entry barriers limit new competition, but sustainability-led circular semiconductor manufacturing is opening selective opportunities. The market is expected to gradually consolidate through partnerships and capacity expansion, especially in 300 mm wafer reclaim services supporting AI and advanced-node applications.

Key Industry Developments

- In March 2026, GlobalWafers announced an additional US$4 billion investment to expand its Sherman, Texas campus, building on its initial US$3.5 billion 300 mm wafer facility. The expansion, supported by US$406 million CHIPS Act funding, aims to strengthen U.S. semiconductor reshoring and secure local supply chains amid rising demand and tariff risks.

Companies Covered in Silicon Wafer Reclaim Market

- Sumco Corporation

- Shin-Etsu Chemical Co., Ltd.

- Silicon Quest International

- Pure Wafer plc

- Wafer Works Corporation

- GlobalWafers Co., Ltd.

- Siltronic AG

- MEMC Electronic Materials

- Okmetic

- Ultrasil Corporation

- NXP Semiconductors

- Texas Instruments

- TSMC

- Samsung Electronics

- Intel Corporation

Frequently Asked Questions

The global silicon wafer reclaim market is projected to reach US$630.2 million in 2026.

The silicon wafer reclaim market grows due to rising semiconductor demand, cost optimization needs, and sustainability-led wafer reuse initiatives.

The silicon wafer reclaim market is expected to grow at a 6.7% CAGR from 2026 to 2033.

Key opportunities include expansion of 300 mm wafer reclaim, AI-driven semiconductor manufacturing, and circular fabrication models.

Key players include Shin-Etsu Chemical, Sumco Corporation, Siltronic AG, GlobalWafers, and Pure Wafer.