- Smart Packaging

- Retail E-Commerce Packaging Market

Retail E-Commerce Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Retail E-Commerce Packaging Market by Packaging Type (Corrugated Boxes, Protective Packaging, Others), Material Type (Fiber-Based/Paper & Corrugated, Bio-Based Materials, Others), Application, and Regional Analysis for 2026 - 2033

Retail E-Commerce Packaging Market Size and Trends Analysis

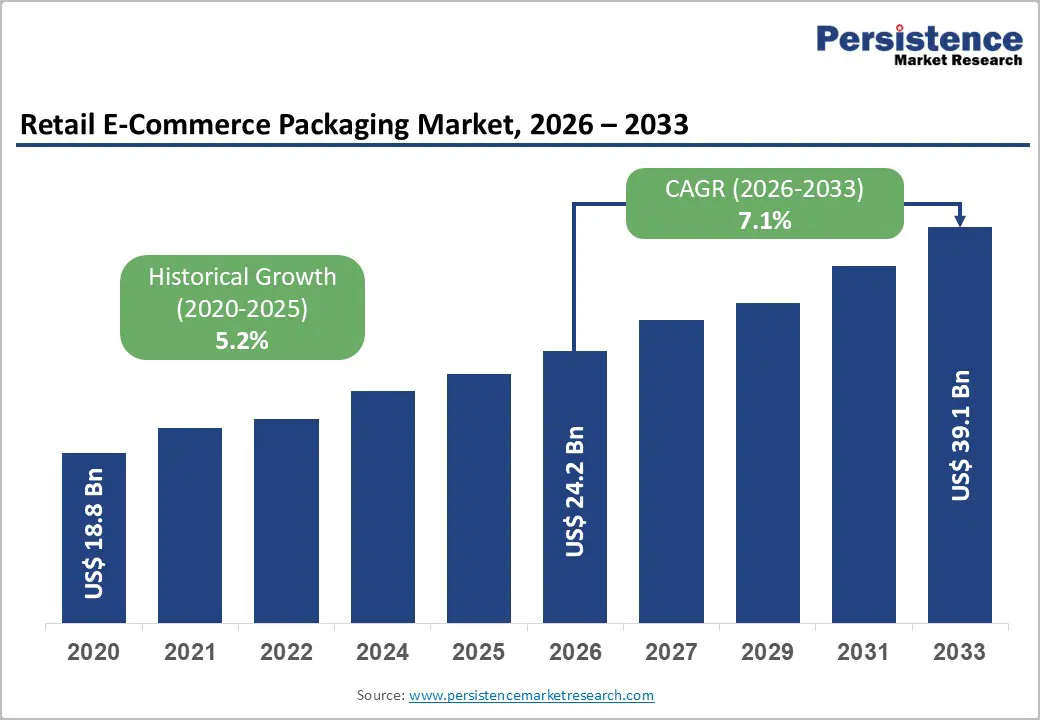

The global retail e-commerce packaging market size is likely to be valued at US$24.2 billion in 2026 and is expected to reach US$39.1 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033, driven by sustained growth in online retail volumes, regulatory pressure to improve recyclability and recycled content, and rising adoption of protective and sustainable packaging formats.

Structural demand growth in Asia Pacific, combined with regulatory-driven value premiumization in Europe, is shaping global investment flows, capacity expansions, and consolidation strategies. Cost volatility in raw materials and last-mile delivery efficiency remains a defining constraint influencing product design and supplier selection.

Key Industry Highlights

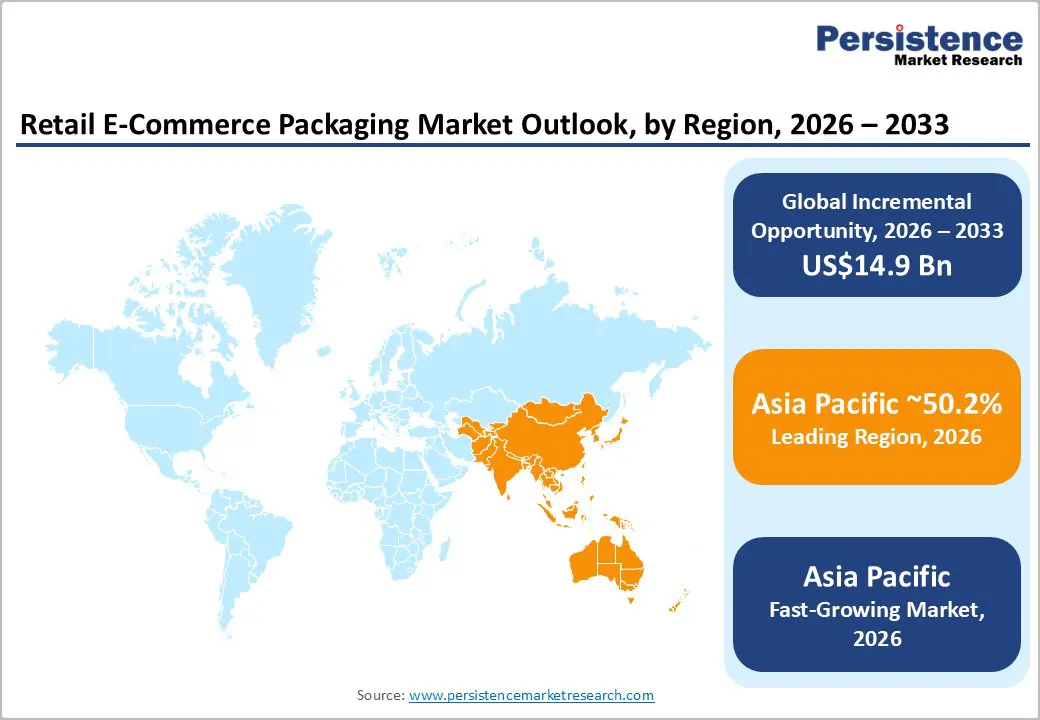

- Leading Region: Asia Pacific is projected to dominate the market with an estimated 50.2% share, supported by high parcel volumes, dense manufacturing ecosystems, and rapid expansion of domestic e-commerce platforms across China, India, and ASEAN economies.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, driven by accelerating online retail adoption, fulfillment network expansion, and increasing demand for cost-efficient corrugated and protective packaging formats.

- Investment Plans: Capital investment is focused on automation, recycling integration, and sustainable material conversion, particularly in fiber-based packaging, protective systems, and fulfillment-adjacent production facilities to improve cost efficiency and regulatory compliance.

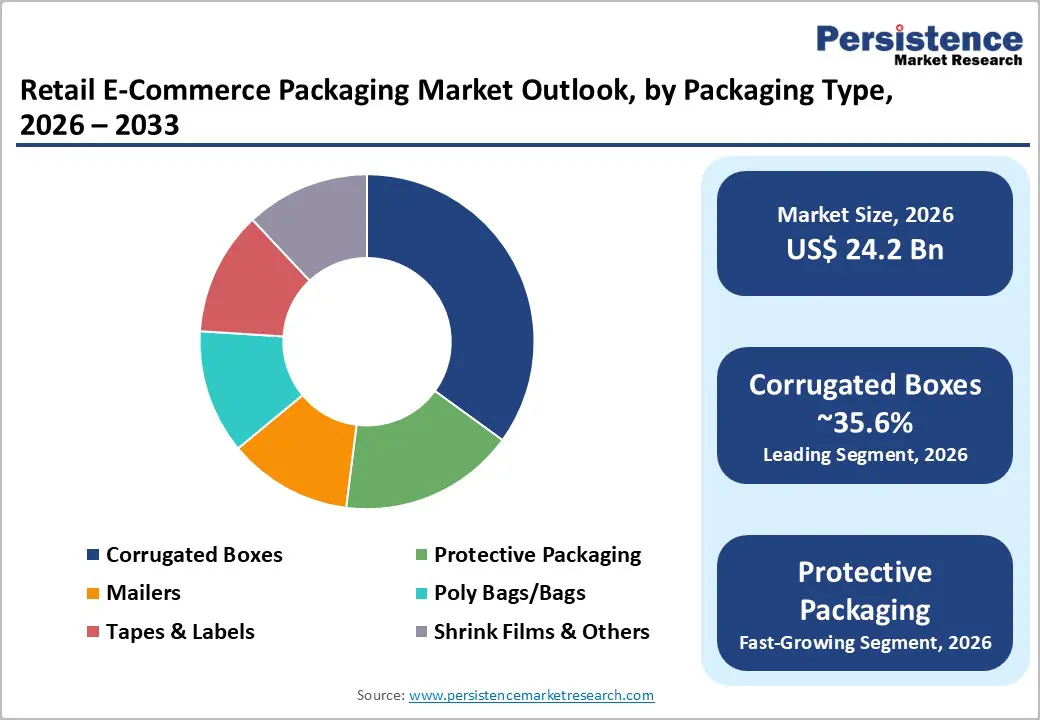

- Dominant Packaging Type: Corrugated boxes are anticipated to remain the dominant packaging type, accounting for approximately 35.6% of market share in 2026, supported by structural strength, automation compatibility, and widespread use across electronics, apparel, and home goods shipments.

- Leading Application: Fashion & apparel is estimated to represent the leading application segment with an estimated 30.8% share in 2026, driven by high shipment volumes, return intensity, branding requirements, and demand for lightweight, resealable packaging solutions.

| Key Insights | Details |

|---|---|

| Retail E-Commerce Packaging Market Size (2026E) | US$24.2 Bn |

| Market Value Forecast (2033F) | US$39.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Structural Expansion of Online Retail and Parcel Volumes

Retail is undergoing a long-term structural rebalancing toward online channels across both developed and emerging economies. E-commerce continues to outpace physical retail growth, leading to a sustained increase in parcel shipments and packaging consumption per transaction. The expansion of direct-to-consumer models, subscription commerce, and online grocery has materially changed fulfillment patterns, shifting demand toward individual parcel packaging rather than palletized or bulk formats. This evolution increases the use of corrugated boxes, mailers, and protective components on a per-order basis, even when overall product volumes remain stable. Higher shipment frequency, greater SKU diversity, and rising average order values further elevate packaging complexity. As a result, packaging demand grows not only in volume terms but also in value, as retailers adopt more customized, fit-for-purpose, and damage-resistant solutions. Structural parcel growth reinforces baseline demand for transit packaging while accelerating adoption of customized and protective formats, supporting market expansion beyond simple shipment growth.

Regulatory Mandates on Recyclability and Recycled Content

Governments across major markets are tightening packaging regulations to reduce waste and improve material circularity. Requirements related to recyclability, recycled content inclusion, and clearer labeling are driving widespread redesign of retail e-commerce packaging. These mandates encourage a shift away from virgin plastics toward fiber-based, recycled, and bio-enabled materials, particularly in secondary and tertiary packaging applications. Compliance increasingly requires verified sourcing, certified material streams, and documented traceability, raising the technical and operational bar for suppliers. While this increases complexity, it also reshapes competitive dynamics by favoring companies with access to recycling infrastructure, fiber conversion capacity, and compliance expertise. Regulatory compliance elevates packaging specifications and increases average selling prices, redistributing value toward suppliers that can deliver certified, audit-ready solutions at scale.

Barrier Analysis - Raw-Material and Logistics Cost Volatility

Retail e-commerce packaging producers operate in an environment of persistent cost volatility across pulp, paper, polymers, and freight. Rapid swings in input costs are particularly challenging for high-volume, standardized products where price pass-through mechanisms are limited. This volatility compresses margins and reduces earnings visibility, especially during periods of sharp cost escalation. Smaller converters and regional suppliers are disproportionately affected, as they often lack long-term contracts or financial hedging capabilities. In response, capital allocation decisions are frequently delayed or scaled back. Margin pressure slows investment in innovation and sustainable materials, reinforcing scale advantages for larger, better-capitalized suppliers.

Recycling Infrastructure Gaps and Standard Fragmentation

Despite increasing regulatory emphasis on recycled content, recycling infrastructure remains uneven across regions. Collection systems, sorting standards, and material quality vary significantly, limiting the availability of consistent post-consumer recycled feedstock. These constraints are especially pronounced for applications requiring high purity or regulatory compliance, such as food-contact packaging. Fragmented standards complicate certification and sourcing, increasing procurement complexity and cost for packaging producers and brand owners alike. Infrastructure limitations delay large-scale material substitution and increase unit costs, slowing the pace of circular packaging adoption.

Opportunity Analysis - Asia Pacific Scale and Fulfillment Modernization

Asia Pacific represents the most significant growth opportunity in retail e-commerce packaging due to its unmatched shipment volumes and rapidly modernizing fulfillment infrastructure. Expanding domestic e-commerce platforms, improving logistics networks, and proximity to manufacturing hubs create favorable economics for packaging production and deployment. As fulfillment centers adopt higher levels of automation and standardization, demand rises for packaging formats compatible with high-speed processing and cost-efficient distribution. Strategic investment in fulfillment-adjacent packaging capacity and automation positions suppliers to capture sustained, high-volume growth.

Premiumization of Sustainable and Bio-Based Packaging

Sustainable and bio-based packaging solutions are gaining traction as retailers and brands prioritize verified environmental performance. Fiber-based cushioning, molded pulp inserts, and bio-derived materials increasingly command price premiums, particularly when supported by credible certifications and lifecycle transparency. Rather than competing solely on cost, suppliers are differentiating through sustainability credentials, design efficiency, and regulatory alignment. Early investment in scalable sustainable materials supports long-term margin expansion and strengthens competitive positioning as regulatory and consumer expectations continue to rise.

Category-wise Analysis

Packaging Type Insights

Corrugated boxes are anticipated to account for 35.6% of market share in 2026, making them the dominant packaging type throughout the forecast period. Their leadership is driven by a combination of structural strength, cost-efficiency, and high compatibility with automated fulfillment and sorting systems used by large-scale e-commerce warehouses. Corrugated formats provide reliable protection for a wide range of products, including consumer electronics, home goods, and apparel, while supporting high stacking strength during long-distance shipping and last-mile delivery. From an operational standpoint, corrugated boxes align well with automated box-making and right-sizing technologies that reduce void fill and dimensional weight charges. Major e-commerce platforms increasingly deploy on-demand box-sizing systems to optimize shipping efficiency and lower logistics costs, reinforcing demand for standardized corrugated materials. Corrugated packaging also offers strong branding potential through high-quality print surfaces, enabling retailers to enhance unboxing experiences without compromising recyclability. Continuous investments in lightweight corrugated grades, recycled fiber content, and parcel-optimization tools are expected to sustain this segment’s leadership over the medium to long term.

Protective packaging is projected to be the fastest-growing packaging type. Growth is closely linked to the rising average value of e-commerce shipments and declining tolerance for product damage among both retailers and consumers. As online sales of fragile, high-value, and precision products increase, demand for engineered protection solutions has intensified. Protective formats such as molded fiber inserts, paper-based cushioning, inflatable systems, and hybrid protection designs are increasingly used to reduce breakage rates, minimize returns, and lower reverse logistics costs. For example, consumer electronics shipments rely heavily on drop-tested inserts and anti-shock structures to meet transit durability standards, while subscription-based commerce favors integrated protective designs that balance protection with presentation. Although protective packaging often increases material usage per shipment, its ability to reduce product loss and improve customer satisfaction results in lower total fulfillment costs. This value-based adoption model is expected to drive sustained above-market growth.

Application Insights

Fashion and apparel are anticipated to represent approximately 30.8% of market share in 2026, positioning the segment as the largest application area. High shipment volumes, frequent product returns, and strong emphasis on brand presentation underpin this dominance. Apparel packaging prioritizes lightweight materials, resealable designs, and visually appealing formats that support both outbound delivery and reverse logistics. Mailers, slim corrugated boxes, and flexible paper-based packaging are widely adopted due to their ability to reduce shipping weight while maintaining adequate protection. Leading apparel retailers increasingly integrate resealable closures and dual-strip adhesive systems to simplify returns, which directly influences packaging design choices. Brand differentiation through customized prints, sustainable material claims, and premium unboxing experiences also plays a critical role in packaging selection. These functional and branding requirements collectively sustain the fashion and apparel segment’s leading market position.

Consumer electronics packaging is likely to be the fastest-growing application segment. Growth is driven by increasing online penetration of smartphones, laptops, wearables, and smart home devices, all of which require high-performance packaging solutions. The high unit value of these products elevates the importance of damage prevention, compliance testing, and secure transit performance. Packaging solutions for consumer electronics increasingly incorporate anti-static materials, molded fiber or foam alternatives, and multi-layer protective systems designed to withstand vibration, compression, and drop impact. Sustainability considerations are also reshaping the segment, with manufacturers shifting from plastic-based cushioning to recyclable or fiber-based protective formats that meet regulatory and retailer sustainability criteria. These performance-driven and compliance-oriented requirements enable electronics packaging to command premium pricing, supporting faster revenue growth relative to lower-value e-commerce categories.

Regional Insights

North America Retail E-Commerce Packaging Market Trends - Premium, Automation-Driven, and Compliance-Focused E-Commerce Packaging

North America remains a high-value market for retail e-commerce packaging, driven by above-average packaging spend per parcel and a focus on performance-driven solutions. The U.S. leads regional demand, bolstered by mature e-commerce adoption, high disposable income, and the rise of direct-to-consumer (D2C) business models. Unlike volume-focused regions, North American retailers prioritize damage reduction, brand presentation, and sustainability, elevating packaging value per shipment.

Growth is supported by advanced fulfillment automation, with significant investments in robotic picking, right-sizing, and inline packaging systems. For instance, Amazon's deployment of automated packaging technologies has boosted demand for corrugated formats compatible with on-demand box making and paper-based protection, reducing dimensional weight costs.

The regulatory landscape also shapes the market, with U.S. state policies on recycled content, labeling, and extended producer responsibility (EPR) influencing material choices. California’s Plastic Pollution Prevention Act has driven a shift toward recycled fiber, paper cushioning, and PCR plastics. As a result, suppliers with robust recycling infrastructure and traceability capabilities, such as International Paper and WestRock, have a competitive edge. Technology-driven packaging firms are also partnering with logistics providers to optimize packaging efficiency, reinforcing North America's position as a premium, innovation-led market.

Europe Retail E-Commerce Packaging Market Trends - Regulatory-Led Circular Packaging and Pan-EU Compliance

Europe’s retail e-commerce packaging market is primarily driven by regulatory harmonization and circular economy mandates, influencing material selection, design, and supplier strategies. Core demand centers include Germany, the U.K., France, and Spain, with high online retail penetration and strong consumer focus on sustainability. Unlike North America, where logistics efficiency is key, Europe’s growth is fueled by regulatory compliance, particularly the EU’s packaging and waste framework, which promotes recyclable, reusable, and fiber-based packaging.

Germany’s VerpackG and similar extended producer responsibility (EPR) schemes require producers to finance packaging waste collection and recycling, increasing costs for non-compliant materials. This has driven sustained demand for corrugated boxes, paper mailers, and molded fiber formats, especially for cross-border e-commerce shipments requiring EU-wide compliance.

Leading European retailers and logistics providers are actively shaping packaging standards, with initiatives such as reusable mailer pilots and mono-material packaging to meet circularity targets. Packaging suppliers with multi-country manufacturing capabilities benefit, offering standardized solutions across EU markets. Investment trends focus on material innovation and compliance-ready infrastructure, with major players investing in recycled fiber processing, barrier-coated papers, and lightweight corrugated grades. These developments strengthen Europe’s position as a sustainability-led market, where regulatory alignment and environmental performance are critical for long-term competitiveness and market share.

Asia Pacific Retail E-Commerce Packaging Market Trends - Volume-Dominated, Manufacturing-Scale and Innovation-Intensive Growth

Asia Pacific is projected to dominate the market with a 50.2% share and remains the fastest-growing regional market, driven by unmatched shipment volumes, rapid digital adoption, and manufacturing scale advantages. China represents the largest contributor by volume, while Japan leads in packaging quality, precision engineering, and automation compatibility. India and ASEAN economies provide incremental growth through expanding internet penetration and mobile-first e-commerce ecosystems.

China’s leadership is underpinned by its massive e-commerce infrastructure and integrated packaging supply base. Large platforms have influenced packaging demand toward lightweight corrugated boxes, mailers, and protective systems designed for high-speed fulfillment. Regulatory efforts to reduce excessive packaging have also pushed suppliers toward optimized designs and recyclable materials, increasing innovation intensity rather than suppressing demand.

Japan’s market emphasizes quality assurance, damage prevention, and precision packaging, particularly for electronics and high-value consumer goods. Packaging solutions in Japan frequently incorporate engineered inserts, anti-static materials, and compact designs compatible with automated sorting systems. This focus on performance sets quality benchmarks that influence premium segments across the broader region.

India and ASEAN markets contribute the fastest incremental growth, supported by rising online retail adoption, expanding logistics networks, and increasing consumer expectations for reliable delivery. Regional manufacturing density and cost advantages enable competitive pricing, while growing sustainability awareness encourages a gradual shift toward paper-based and recycled materials. Collectively, Asia Pacific’s scale, cost efficiency, and innovation capacity reinforce its long-term dominance in the retail e-commerce packaging market.

Competitive Landscape

The global retail e-commerce packaging market exhibits moderate concentration at the global level and high fragmentation among regional converters. Large integrated players benefit from scale, recycling access, and fulfillment partnerships, while local firms compete on speed and customization. Consolidation activity continues to increase market concentration.

Key strategies include vertical integration, sustainable product innovation, automation, and selective geographic expansion. Differentiation increasingly depends on verified circularity, performance validation, and total cost-of-ownership reduction.

Key Industry Developments

- In December 2025, ProAmpac announced the acquisition of TC Transcontinental Packaging, expanding its presence in flexible packaging formats used in retail e-commerce and protective applications.

- In October 2025, NPAC, in partnership with Ranpak Holdings, launched the FillPak Mini automated paper fill solution in Asia Pacific, offering compact, sustainable void fill for e-commerce fulfillment stations.

Companies Covered in Retail E-Commerce Packaging Market

- Smurfit Westrock

- International Paper

- Amcor

- Mondi Group

- Sealed Air

- Huhtamaki

- Sonoco Products Company

- DS Smith

- Berry Global

- WestRock

- Packaging Corporation of America

- Nippon Paper Industries

- Oji Holdings Corporation

- Stora Enso

- Georgia-Pacific

- Mayr-Melnhof Karton

- Tetra Pak

- CCL Industries

Frequently Asked Questions

The global retail e-commerce packaging market size is likely to be valued at US$24.2 billion in 2026.

By 2033, the retail e-commerce packaging market is expected to reach US$39.1 billion.

Key trends include the shift toward fiber-based and recyclable materials, growing use of engineered protective packaging to reduce damage and returns, automation-compatible packaging designs, and increasing adoption of sustainable and bio-based formats in response to regulatory and brand sustainability commitments.

Corrugated boxes represent the leading packaging type, accounting for approximately 35.6% of market share, due to their strength, versatility, cost efficiency, and compatibility with automated fulfillment and last-mile delivery systems.

The retail e-commerce packaging market is projected to grow at a CAGR of 7.1% between 2026 and 2033.

Major players include Smurfit Westrock, International Paper, Amcor, Mondi Group, and Sealed Air.