- Retail

- Department Store Retailing Market

Department Store Retailing Market Size, Share, and Growth Forecast 2025 - 2032

Department Store Retailing Market by Store Type (Upscale Department Store, Mid-Range Department Store, Discount Department Store, Others), Product Category (Food & Beverage, Clothing, Footwear, Sports Apparels & Equipment, Toiletries, Home Appliances, Cosmetics & Personal Care, Watch & Jewelry, Others), and Regional Analysis for 2025 - 2032

Department Store Retailing Market Share and Trends Analysis

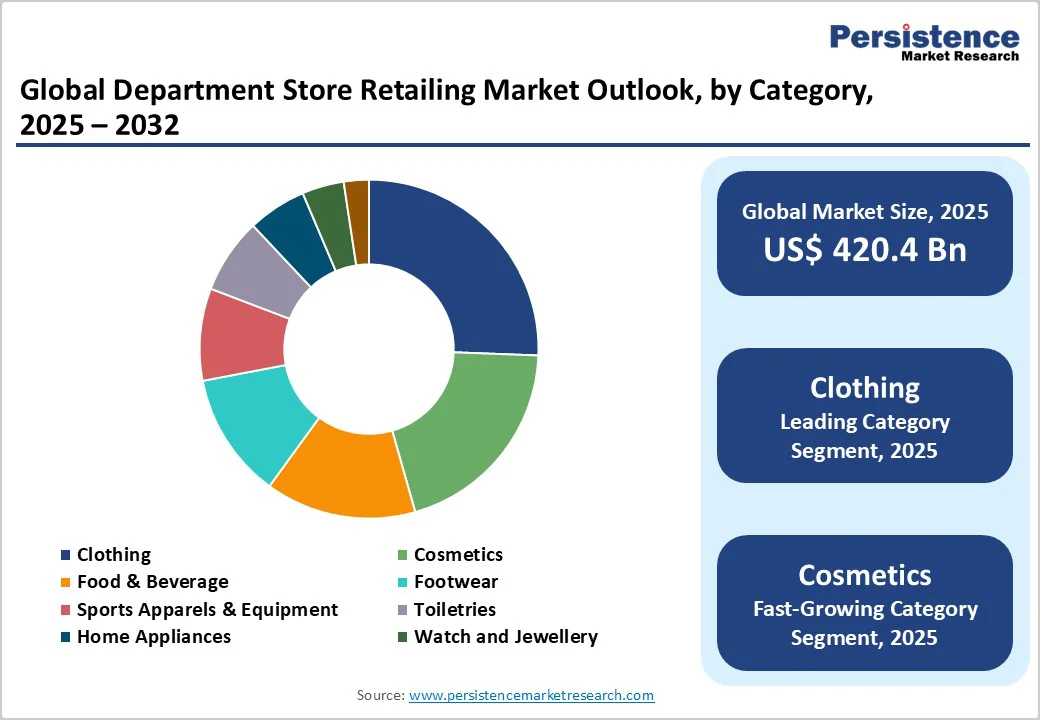

The global department store retailing market size is likely to be valued at US$420.4 billion in 2025. It is projected to reach US$611.5 billion by 2032, growing at a CAGR of 5.5% during the forecast period 2025-2032. The market is experiencing robust growth driven by rising disposable incomes across emerging economies, the accelerating adoption of omnichannel retail strategies, and sustained consumer preference for convenient one-stop shopping solutions.

Rising urbanization, particularly in Asia Pacific regions such as India, China, and Southeast Asia, is expanding the customer base for organized retail formats. Consumers are also increasingly valuing integrated shopping experiences that combine physical stores with digital touchpoints, creating significant momentum for department store operators that successfully implement these hybrid strategies.

Key Industry Highlights

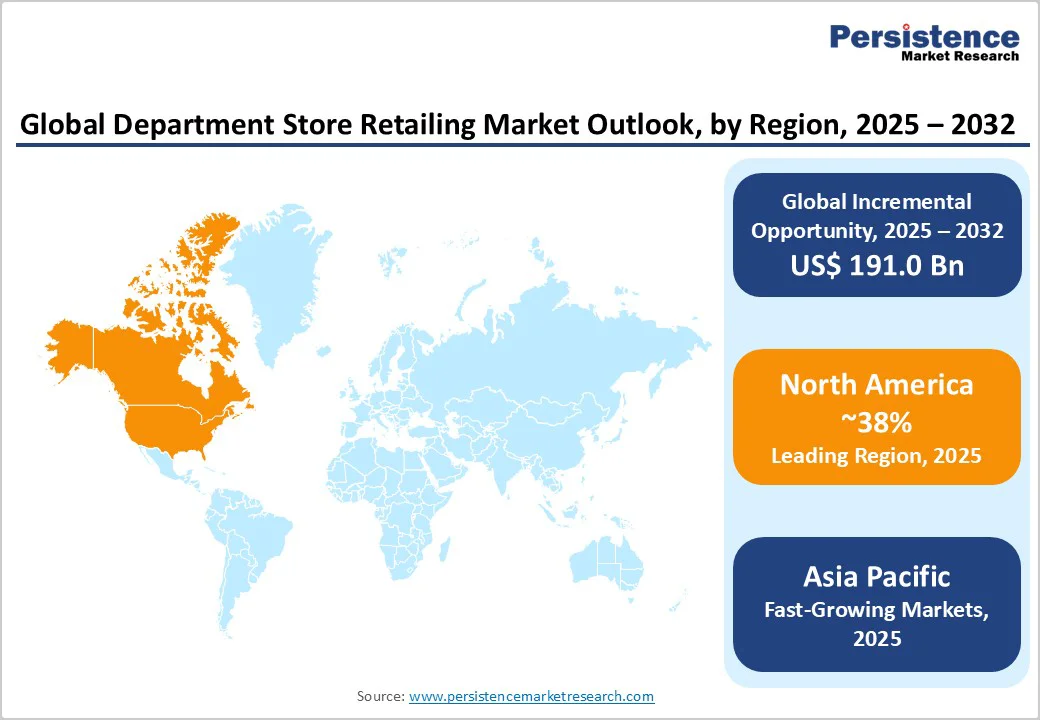

- Leading Region: North America is slated to hold the largest share, around 38%, in 2025, driven by mature retail infrastructure, high consumer spending, and strong omnichannel retail transformation initiatives.

- Fastest-growing Regional Market: Asia Pacific is likely to remain the fastest-growing regional market through 2032, supported by urbanization, middle-class expansion, and digital commerce integration.

- Leading Category: The apparel & accessories segment is expected to dominate with about 48% revenue share in 2025, propelled by fashion trends, widespread influencer culture, and continuous product renewals across major department stores.

- Fastest-growing Product Category: The cosmetics & personal care segment is poised to emerge as the fastest-growing category from 2025 to 2032 due to rising wellness consciousness and immersive in-store beauty experiences.

- Key Market Opportunity: AI-driven personalization technologies are being actively adopted by a large number of organized department store operators globally, enhancing customer engagement, loyalty, and conversion efficiency across physical and digital channels.

| Key Insights | Details |

|---|---|

|

Department Store Retailing Market Size (2025E) |

US$420.4 Bn |

|

Market Value Forecast (2032F) |

US$611.5 Bn |

|

Projected Growth CAGR (2025-2032) |

5.5% |

|

Historical Market Growth (2019-2024) |

4.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Surging Middle-Class Consumption and Rising Disposable Incomes

The expansion of middle-class populations and rising wages in emerging markets are key growth catalysts for the department store retailing industry. India’s retail sector, for example, reached INR 82 lakh crore (around US$ 980 billion) in 2024 and is projected to more than double by 2034, supported by government initiatives promoting digital infrastructure and formal commerce. Consumers in these economies are increasingly purchasing luxury and branded products once confined to developed markets. This shift fuels the demand for full-service department store formats that offer curated assortments under one roof, especially among younger and affluent urban consumers who prioritize convenience and product variety.

Department store retailers are also transforming operations through omnichannel integration that unites physical and digital shopping experiences. Advanced tools such as AI, AR mirrors, and real-time inventory tracking enable hyper-personalized engagement and higher conversion rates. Nordstrom’s AI-powered app, for instance, offers real-time style recommendations and store-wide inventory checks, reflecting this digital evolution. Industry data shows that omnichannel shoppers spend 1.5 times more per month than single-channel shoppers, underscoring the revenue potential for retailers that execute integrated strategies effectively and optimize both online and offline consumer touchpoints.

Declining Mall Foot Traffic and Store Closures

Traditional department store formats are facing severe structural challenges due to changing consumer behavior and real estate pressures. As of April 2025, around 1,200 malls remained operational in the U.S., with forecasts suggesting only 900 will survive by 2028, indicating a 25% decline in just three years. The erosion of mall foot traffic has intensified challenges for anchor department stores, with consumers shifting toward off-price formats, e-commerce, and alternative shopping venues. Persistent issues such as high real estate costs, declining tenant variety, and fundamental shifts in retail consumption continue to restrict recovery and weaken the traditional department store ecosystem.

Furthermore, the growing dominance of off-price and direct-to-consumer (DTC) retail models is disrupting the profitability and brand relevance of traditional department stores. Off-price retailers’ share of total apparel retail visits increased from 36.4% in 2021 to 41.5% in 2024, reflecting consumers’ sustained preference for value-driven shopping amid inflationary conditions. These low-cost, high-turnover formats attract price-conscious shoppers who once frequented full-line department stores. DTC brands are leveraging social media and digital platforms to gain greater control over branding, pricing, and consumer engagement, placing pressure on multi-brand retailers. Cross-visitation trends reveal that premium department store customers are increasingly turning to off-price competitors, highlighting rising price sensitivity and diminishing brand loyalty across core shopper segments.

Experiential Retail and Luxury Segment Expansion in Emerging Markets

Emerging luxury markets are unlocking major growth opportunities for department store retailing as affluent populations in the Asia Pacific and Latin America expand their premium spending. India’s luxury market, valued at around US$17 billion in 2024, is projected to reach new heights by 2030, driven by rising disposable incomes and aspirational consumerism. The entry of Galeries Lafayette in India through its 90,000 sq. ft. Mumbai flagship featuring over 250 luxury brands exemplifies this strategic expansion. Department stores are increasingly integrating experiential features, such as exclusive boutiques, personal shopping, and curated cultural events, to reinforce their premium positioning.

Advanced technologies such as artificial intelligence (AI), augmented reality (AR), and smart mirrors are reshaping department store retailing by creating hyper-personalized, immersive experiences. Smart mirrors equipped with AI and computer vision enable virtual try-ons for apparel and cosmetics. For example, L’Oréal’s smart mirror solution allows virtual testing of complete product ranges, bridging inventory gaps while enhancing customer satisfaction. Retailers are increasingly employing data-driven store design optimization and AI-based inventory management to reduce stockouts and optimize shelf layouts. The adoption of AI in retail operations is expected to rise sharply, as hyper-personalization and smart retail tools help physical department stores strengthen differentiation from e-commerce competitors.

Category-wise Analysis

Store Type Insights

Upscale department stores are poised to dominate the global landscape, capturing around 42% market share in 2025, supported by premium brand portfolios, personalized customer services, and luxury in-store experiences that strengthen loyalty. Mid-range department stores follow closely with approximately 34% share, driven by affordability-focused assortments and accessibility across urban centers. These formats remain central to aspirational consumers balancing quality and price expectations.

Discount department stores are emerging as the fastest-expanding segment, projected to advance at a CAGR of about 6.8% from 2025 to 2032. Their success stems from inflation-induced value consciousness, strong private-label offerings, and digital channel integration.

Category Insights

Clothing remains the largest product segment, accounting for around 48% of department store retailing market revenues in 2025, supported by seasonal fashion cycles, influencer-driven marketing, and rapid product turnover. Cosmetics and personal care account for approximately 14% of the market share, benefiting from rising beauty consciousness, luxury brand diversification, and experiential retailing in urban malls.

Home appliances and electronics represent around 10% of total revenue, bolstered by the rise of connected smart homes and lifestyle upgrades. Footwear and sports apparel continue to grow healthily as consumers embrace active-living trends. Food & beverage, toiletries, and jewelry segments collectively enhance basket value, reflecting evolving consumer preferences for holistic shopping experiences under one roof.

Regional Insights

North America Department Store Retailing Market Trends

North America is anticipated to capture around 38.4% of the department store retailing market share in 2025, led by the United States with its established retail infrastructure and high consumer expenditure. The region is home to retail giants such as Macy’s, Nordstrom, and Kohl’s, which are transitioning toward smaller, experience-oriented formats and strengthening luxury-focused sub-brands. For instance, Macy’s initiated closure of underperforming stores and expansion of compact outlets through 2025, while Bloomingdale’s continues to scale its luxury presence. Retailers are also aligning with sustainability goals through energy-efficient operations and transparent sourcing practices.

The region also leads in omnichannel innovation, integrating digital tools to enable seamless inventory visibility and personalized customer journeys. Retail media networks and automated fulfillment systems enhance operational efficiency and profitability, positioning North America as the benchmark for data-driven, hybrid retail models that merge digital convenience with elevated in-store engagement.

Europe Department Store Retailing Market Trends

Europe is forecasted to account for nearly 30% of the department store retailing market in 2025, supported by strong brand heritage and well-established retail traditions. Germany and France will dominate, reflecting the strength of their luxury and mid-range department store operations. Leading retailers such as Galeries Lafayette and Carrefour are focusing on premium brand collaborations, store modernizations, and curated assortments targeting high-value customers.

Strict implementation of sustainability directives, such as the European Union (EU) Corporate Sustainability Reporting Directive, is driving major investments in circular-economy initiatives, ethical sourcing, and energy efficiency. Retailers are integrating cultural, culinary, and fashion experiences to maintain relevance amid shifting consumer values, with growing preference for ethically produced goods and experiential store environments over purely transactional shopping formats.

Asia Pacific Department Store Retailing Market Trends

Asia Pacific is expected to capture approximately 26.1% of the market in 2025 and emerge as the fastest-growing regional hub through 2032, driven by urbanization, digital retail integration, and middle-class expansion. China remains the dominant contributor, supported by robust live commerce activity, while India’s expanding retail infrastructure continues to attract global department store brands. Regional chains such as Isetan Mitsukoshi are pursuing cross-border expansion and localized store concepts tailored to evolving consumer lifestyles.

Social commerce platforms such as TikTok Shop, Lazada Live, and Shopee Live are redefining product discovery and engagement. Retailers, including David Jones and Myer, are accelerating digital transformation through mobile platforms and integrated fulfillment systems. Asia Pacific’s dynamic demographics, rising discretionary spending, and advanced retail innovation ensure sustained regional momentum in global department store development.

Competitive Landscape

The global department store retailing market structure demonstrates moderate consolidation, with a balanced mix of multinational and regional players maintaining dominant positions across major economies. Competitive differentiation increasingly focuses on experiential retail formats, luxury collaborations, and exclusive merchandise assortments rather than price competition. Operators are emphasizing enhanced in-store experiences and curated product strategies to sustain consumer engagement amid changing shopping preferences.

Strategic focus has shifted toward omnichannel integration, digital transformation, and investment in micro-fulfillment infrastructure to improve operational efficiency. Emerging business models such as off-price extensions, compact urban outlets, and AI-driven personalization are reshaping traditional formats, enabling retailers to capture both premium and value-conscious customer segments.

Key Industry Developments

- In October 2025, Galeries Lafayette opened its first flagship store in Mumbai, India, featuring 90,000 sq. ft. of retail space and over 250 luxury brands. The expansion marks the retailer’s strategic entry into Asia’s high-growth luxury retail landscape, targeting India’s rapidly expanding affluent consumer base.

- In September 2025, David Jones completed a AU$22 million transformation of its Bondi Junction flagship store, introducing 31 new designer brands and enhancing its omnichannel capabilities.

- The revamp aligns with its Vision 2025+ strategy, which aims to strengthen premium positioning and modernize 40% of its national retail footprint by 2027.

- In May 2025, Ruby Liu Commercial Investment acquired leases for up to 28 Hudson’s Bay stores across Ontario, Alberta, and British Columbia following Hudson’s Bay’s March 2025 bankruptcy. The purchasing affiliate also already owns three leased locations in British Columbia. Ruby Liu plans to launch a new department store concept targeting a broad, multicultural Canadian audience. This transaction is part of Hudson’s Bay’s approved lease monetization strategy during its restructuring under the Companies’ Creditors Arrangement Act (CCAA) in Canada.

Companies Covered in Department Store Retailing Market

- Marks & Spencer

- Macy's

- Kohl's

- Nordstrom

- Isetan Mitsukoshi

- Takashimaya

- Galeries Lafayette

- Hudson's Bay Company

- Dillard's

- Falabella

- Liverpool

- Myer

- Shoppers Stop

- David Jones

- Lotte Department Store

- Walmart

- Target

- Costco

Frequently Asked Questions

The global department store retailing market is projected to reach US$ 420.4 billion in 2025.

The market is poised to witness a CAGR of 5.5% from 2025 to 2032.

Key opportunities lie in luxury market expansion, AI-based personalization, experiential retailing, and social commerce integration, especially across Asia Pacific.

Some of the major market players include Walmart, Target, Macy’s, Kohl’s, Nordstrom, and Marks & Spencer, among others.