- Retail

- Food & Grocery Retail Market

Food & Grocery Retail Market Size, Share, and Growth Forecast, 2026 - 2033

Food & Grocery Retail Market by Product Type (Fresh Food, Frozen Food, Food Cupboard, Beverages, Cleaning & Household, Others), Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Others), and Regional Analysis for 2026 – 2033

Food & Grocery Retail Market Size and Trends Analysis

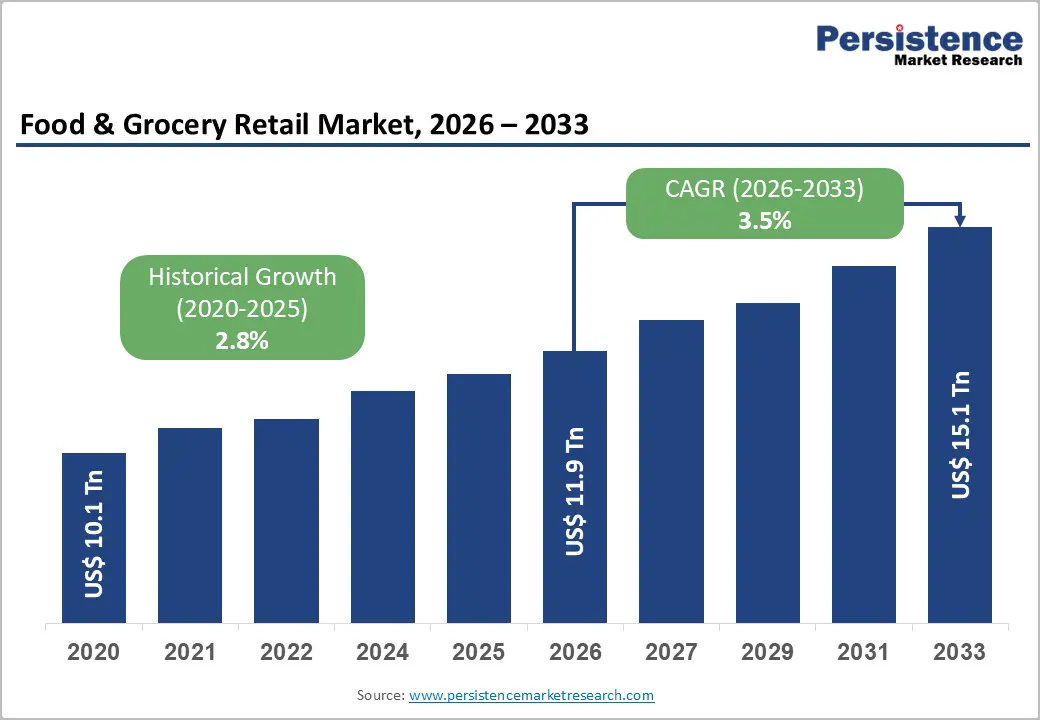

The global food & grocery retail market size is likely to be valued at US$11.9 trillion in 2026, and is expected to reach US$15.1 trillion by 2033, growing at a CAGR of 3.5% during the forecast period from 2026 to 2033, driven by steady population growth, rising demand for fresh and convenient food products, increasing urbanization supporting modern retail formats, and gradual shift toward online grocery shopping post-pandemic.

Increasing recognition of food & grocery retail as an essential, recession-resilient sector with stable demand in emerging convenience, health-conscious, and digital-shopping markets remains a major driver of market growth.

Key Industry Highlights:

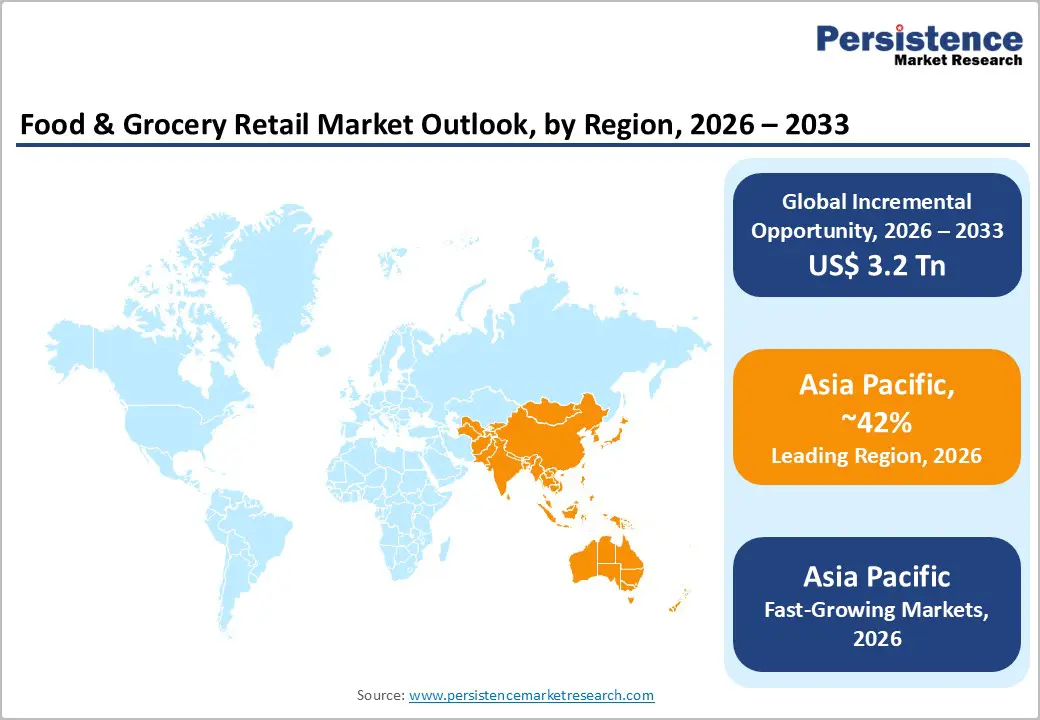

- Leading Region: Asia Pacific, anticipated to account for a 42% market share in 2026, driven by a large population base, rapid modern retail expansion, and strong demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by urbanization, rising middle-class consumption, and the explosive growth of online & quick-commerce channels.

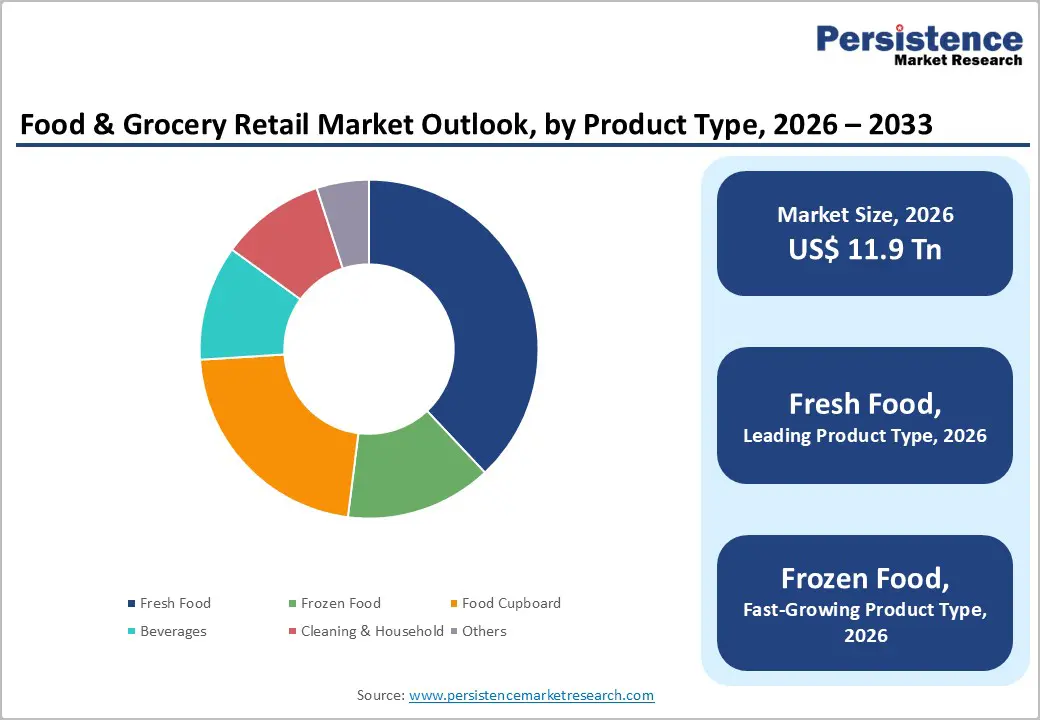

- Dominant Product Type: Fresh food, to hold approximately 38% of the market share, as it remains the highest-volume and most frequently purchased category.

- Leading Distribution Channel: Supermarkets & hypermarkets, contributing nearly 55% of the market revenue, due to one-stop shopping dominance.

| Key Insights | Details |

|---|---|

|

Food & Grocery Retail Market Size (2026E) |

US$11.9 Tn |

|

Market Value Forecast (2033F) |

US$15.1 Tn |

|

Projected Growth CAGR (2026-2033) |

3.5% |

|

Historical Market Growth (2020-2025) |

2.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Fresh Food Demand and Modern Retail Expansion

The growing consumer preference for convenience, quality, and variety has significantly transformed the fresh food landscape. Urban populations are increasingly seeking ready-to-cook, pre-packaged, and organic fresh food options that align with busy lifestyles and health-conscious choices. Supermarkets, hypermarkets, and specialty stores have responded by expanding their fresh food sections, offering a broader range of fruits, vegetables, dairy, meat, and seafood products with improved packaging and extended shelf life. The integration of cold chain logistics has played a crucial role in maintaining product freshness, ensuring food safety, and reducing wastage.

The rapid expansion of modern retail formats has made fresh food more accessible to consumers across both metropolitan and emerging urban areas. Retailers are leveraging technology-driven solutions such as inventory management systems, e-commerce platforms, and mobile delivery apps to enhance convenience and availability. Loyalty programs, personalized promotions, and in-store experiences further drive consumer engagement. Partnerships with local farmers and suppliers allow retailers to offer seasonal and locally sourced produce, meeting the rising demand for sustainability and traceability.

Online Grocery Penetration and Convenience Formats

Consumers are increasingly turning to digital platforms for grocery shopping, driven by the desire for time-saving solutions and seamless convenience. Online grocery platforms offer a wide assortment of products, from fresh produce to packaged goods, allowing customers to compare prices, read reviews, and schedule deliveries according to their needs. This shift is particularly prominent among urban, tech-savvy populations who prioritize flexibility and contactless transactions.

Convenience formats, including neighborhood express stores, click-and-collect outlets, and automated vending solutions, complement the online experience by bridging the gap between digital access and physical availability. Retailers are strategically placing smaller-format stores in high-density areas to provide quick access to essential groceries and ready-to-eat meals. These formats reduce the need for long commutes to larger stores and support impulse and frequent purchases. Technology plays a central role in enhancing efficiency, from AI-driven inventory management to predictive analytics that ensure stock availability and minimize wastage. Mobile apps, subscription services, and personalized offers strengthen consumer engagement while fostering loyalty.

Barrier Analysis – Food Inflation and Thin Retail Margins

Rising food prices have created significant challenges for retailers, as the cost of raw materials, transportation, and storage continues to climb. Retailers face pressure to maintain competitive pricing for consumers while absorbing increasing operational expenses, which often compresses profit margins. Perishable goods, in particular, are highly sensitive to price fluctuations, making inventory management and waste reduction critical for profitability.

Thin margins force retailers to optimize every aspect of the supply chain, from sourcing to distribution, often leading to strategic partnerships with local suppliers and investment in efficient logistics and cold chain infrastructure. Promotional strategies and discounting become a balancing act, as excessive offers can erode margins further, while limited promotions risk reducing footfall.

Supply Chain Volatility and Labor Shortages

Disruptions in supply chains have increasingly affected the flow of goods, causing delays, higher transportation costs, and uncertainty in inventory availability. Global events, logistical bottlenecks, and fluctuating demand patterns contribute to this volatility, forcing retailers and suppliers to adapt quickly to maintain consistent product availability. Perishable and fresh items are particularly vulnerable, requiring robust cold chain solutions and agile distribution networks to minimize losses.

Labor shortages add another layer of complexity, as an insufficient workforce in warehouses, logistics, and retail outlets hampers operations and slows delivery timelines. Recruiting, training, and retaining skilled workers has become a strategic priority, with many companies turning to automation, robotics, and technology-driven solutions to bridge gaps.

Opportunity Analysis – Growth in Private-Label Fresh and Quick-Commerce Models

Retailers are increasingly focusing on private-label fresh products to strengthen brand identity, improve margins, and offer consumers cost-effective alternatives to national brands. These products, ranging from fresh produce and dairy to ready-to-eat meals, allow retailers to control quality, sourcing, and packaging while responding quickly to changing consumer preferences. By promoting private-label options, retailers can differentiate themselves in a competitive market, build customer loyalty, and optimize profitability, as these products typically carry higher margins than branded goods.

Quick-commerce models are reshaping consumer expectations by offering ultra-fast delivery of groceries and fresh food items, often within 30 to 60 minutes. This approach leverages micro-fulfillment centers, strategically located dark stores, and technology-driven order management systems to ensure speed, accuracy, and product freshness. Customers increasingly favor this convenience, particularly for urgent or last-minute needs, driving adoption across urban centers. The combination of private-label offerings and quick-commerce enables retailers to provide value, convenience, and differentiated experiences.

Expansion in Online-to-Offline Integration

Retailers are increasingly blending digital and physical shopping experiences to create seamless consumer journeys. Online-to-offline (O2O) integration allows customers to browse and purchase products through e-commerce platforms while leveraging offline touchpoints for collection, returns, or in-person assistance. This approach enhances convenience, builds trust, and encourages repeat engagement by combining the speed and accessibility of digital channels with the tactile experience of physical stores.

Click-and-collect services, curbside pickups, and in-store digital kiosks are becoming common features, allowing shoppers to save time and reduce delivery costs while maintaining flexibility. Retailers are also using O2O strategies to drive foot traffic, offering online promotions redeemable in-store, personalized recommendations based on browsing history, and loyalty programs that span both channels. Technology underpins the integration, with inventory management systems, AI-driven demand forecasting, and real-time stock visibility ensuring that consumers receive accurate product availability information. Partnerships with logistics providers and local fulfillment centers enable faster deliveries and improved service levels.

Category-wise Analysis

Product Type Insights

Fresh food is anticipated to dominate the market, accounting for 38% of the market share in 2026. Its dominance is driven by rising consumer demand for healthy, high-quality, and convenient food options. Urban lifestyles, increasing health awareness, and preference for organic and minimally processed products are driving this growth. Retailers are expanding fresh food sections, improving packaging, and enhancing cold chain logistics to maintain product quality and extend shelf life. Seasonal and locally sourced offerings further appeal to consumers seeking freshness and sustainability.

Sprouts Farmers Market is a U.S. supermarket chain with a strong focus on fresh produce, natural foods, and perishable items such as meat, dairy, and seafood. The company’s strategy centers on offering a broad assortment of high?quality fresh products from organic fruits and vegetables to fresh deli and bakery options to attract health?conscious consumers and differentiate itself from traditional grocery stores.

Frozen food represents the fastest-growing product type, due to its convenience, long shelf life, and ability to preserve nutritional value. Busy lifestyles and increasing demand for ready-to-cook meals have driven consumers to rely on frozen vegetables, seafood, meat, and prepared dishes. Advances in freezing technology ensure taste and quality are maintained, making frozen products more appealing. Retailers are expanding frozen food sections and integrating them into online and quick-commerce platforms to meet growing demand.

BigBasket expanded its frozen food offerings to capture the rising demand for convenient, ready?to?cook products. In 2024, the company launched a dedicated frozen foods brand called Precia in partnership with celebrity chef Sanjeev Kapoor, broadening its range beyond basic items such as peas and corn to include momos, mithai, and other frozen products sold through its platform.

Distribution Channel Insights

Supermarkets & hypermarkets are expected to dominate the market, contributing nearly 55% of revenue in 2026, fueled by their ability to offer a wide assortment of products under one roof. These large-format stores provide consumers with convenience, competitive pricing, and access to fresh, packaged, and specialty food items.

Advanced store layouts, loyalty programs, and integrated digital solutions enhance the shopping experience, encouraging repeat visits. Walmart Inc. Walmart is the world’s largest supermarket and hypermarket retailer, generating massive food and grocery sales reportedly over US$611 billion in total company revenue, with grocery forming a major share, far exceeding most competitors’ revenues and accounting for a significant share of the global grocery retail market.

The online channel represents the fastest-growing distribution channel, propelled by convenience, accessibility, and the ability to shop anytime. Consumers increasingly prefer e-commerce platforms and mobile apps for grocery and fresh food purchases, benefiting from home delivery, quick-checkout options, and personalized recommendations. The growth is fueled by urban lifestyles, rising smartphone penetration, and digital payment adoption. Retailers are enhancing online offerings with broader assortments, subscription services, and real-time inventory visibility.

Amazon has rapidly expanded its online grocery business through Amazon?Fresh. The service now operates in over 130 cities in India, delivering groceries, fresh produce, and everyday essentials directly to customers’ homes, often with same-day or two-hour delivery options.

Regional Insights

North America Food & Grocery Retail Market Trends

Market growth in North America is characterized by a combination of mature infrastructure, high consumer expectations, and rapid technological adoption. Supermarkets and hypermarkets remain the dominant retail formats, offering extensive product assortments, fresh and packaged foods, and ready-to-eat options. Consumers increasingly prioritize quality, convenience, and sustainability, driving retailers to expand organic, locally-sourced, and private-label offerings. Cold chain logistics, efficient supply management, and advanced inventory systems enable stores to maintain freshness and reduce waste, meeting high standards for perishable items.

Online grocery penetration is a significant trend in the region, fueled by e-commerce platforms, mobile apps, and quick-commerce delivery models. Major players offer same-day delivery, subscription services, and click-and-collect options, integrating digital and physical touchpoints to enhance convenience. Loyalty programs, personalized promotions, and AI-driven recommendations are used to strengthen customer engagement and retention. Retailers are also leveraging technology to optimize operations, including demand forecasting, predictive analytics, and automated warehouses, addressing challenges such as labor shortages and supply chain volatility.

Sustainability initiatives, such as reducing plastic packaging, food waste management, and energy-efficient store designs, are gaining importance.

Europe Food & Grocery Retail Market Trends

Market growth in Europe is evolving under the influence of changing consumer preferences, technological adoption, and regulatory pressures. Supermarkets and hypermarkets remain central to the retail landscape, offering a broad range of fresh produce, packaged foods, and specialty items. Consumers increasingly demand healthy, organic, and locally sourced products, pushing retailers to expand private-label fresh food offerings and sustainable sourcing initiatives. Convenience formats, such as neighborhood stores and express outlets, are gaining popularity, particularly in urban areas where time-constrained shoppers seek quick access to essentials.

Digital transformation is reshaping the market, with online grocery shopping and click-and-collect services becoming more widespread. Retailers are integrating mobile apps, personalized promotions, and loyalty programs to enhance engagement, while advanced inventory and supply chain management systems ensure product availability and freshness. Quick-commerce models, supported by micro-fulfillment centers and local delivery networks, are helping retailers meet growing demand for fast delivery of groceries and fresh food.

Asia Pacific Food & Grocery Retail Market Trends

Asia Pacific is expected to dominate and is likely to be the fastest growing, capturing 42% revenue in 2026, propelled by urbanization, rising disposable incomes, and changing consumer lifestyles. Organized retail formats, such as supermarkets, hypermarkets, and convenience stores, are expanding quickly in major urban centers, offering a wide assortment of fresh produce, packaged foods, and ready-to-eat meals. Consumers increasingly value quality, freshness, and convenience, prompting retailers to introduce private-label fresh products and locally sourced offerings that cater to regional tastes.

Digital adoption is accelerating online grocery growth across the region. E-commerce platforms, mobile apps, and quick-commerce services enable same-day or even sub-hour deliveries, meeting the demand for convenience among busy urban consumers. Integration of online and offline channels through click-and-collect services and mobile ordering enhances accessibility, while AI-driven recommendations and personalized promotions improve customer engagement.

Supply chain efficiency is a key focus, with investments in cold chain logistics, warehouse automation, and real-time inventory management helping retailers maintain freshness and reduce wastage. Smaller-format stores and neighborhood outlets are also emerging to serve last-mile delivery needs in high-density areas.

Competitive Landscape

The global food & grocery retail market is shaped by intense competition between traditional big-box retailers and digitally native or quick-commerce players. In North America and Europe, companies such as Walmart, Costco, and Kroger dominate through extensive store networks, strong private-label offerings, and omnichannel capabilities that combine physical stores with online platforms. Their focus on fresh food, loyalty programs, and personalized promotions helps attract and retain customers while driving repeat purchases.

In the Asia Pacific region, both local leaders and international entrants are rapidly expanding, leveraging digital integration and e-commerce platforms to enhance accessibility and convenience for urban consumers. Fresh food delivery services further increase engagement by boosting store traffic, reducing substitution risks, and enabling seamless integration across multiple shopping channels. Retailers are also investing strategically in private-label ranges, quick-commerce acquisitions, and sustainability initiatives, including cold chain optimization and waste reduction.

Key Industry Developments:

- In November 2025, The Kroger Co. announced updates to its eCommerce plan, delivering a simplified and differentiated customer experience. The company attracted new households to shop at Kroger and achieved immediate improvements in e-commerce profitability. By implementing these changes, Kroger enhanced online convenience, optimized digital operations, and strengthened its position in the competitive grocery eCommerce market.

- In May 2023, Auchan Retail partnered with Trigo, the Israel-based computer vision company, to launch an autonomous grocery store for the French retail group’s head office employees. The store implemented frictionless checkout technology and advanced retail analytics, allowing employees to shop without traditional payment counters.

Companies Covered in Food & Grocery Retail Market

- Walmart

- Costco Wholesale Corporation

- 7-ELEVEN, Inc.

- Amazon.com Inc

- The Kroger Co.

- Target Brands, Inc.

- ALDI

- AEON Co Ltd

- Carrefour CA

- Schwarz Gruppe

Frequently Asked Questions

The global food & grocery retail market is projected to reach US$11.9 trillion in 2026

Fresh food consumption and the expansion of modern retail formats are the primary drivers of the food and grocery retail market.

The food & grocery retail market is poised to witness a CAGR of 3.5% from 2026 to 2033.

Key market opportunities include the growth of private-label fresh offerings, the rise of quick-commerce models, expansion across the Asia Pacific region, and the integration of online-to-offline retail channels.

Walmart, Costco, Kroger, Amazon, and ALDI are the key players.