- Hardware & Software IT Services

- Retail Analytics Market

Retail Analytics Market Size, Share, and Growth Forecast 2026 - 2033

Retail Analytics Market by Solution (Software: Data Management & Integration, Reporting & Visualization Tools, Predictive Analytics & AI Engines, Customer Analytics Platforms; Services: Training & Consulting, Integration & Deployment, Managed Services), Deployment Mode (On-Premise, Cloud-Based), Retail Format (Supermarkets & Hypermarkets, Department Stores, Specialty Stores, Convenience Stores, E-commerce & Online Retailers, Omnichannel Retailers), Function, Industry, and Regional Analysis, 2026 - 2033

Retail Analytics Market Size and Trend Analysis

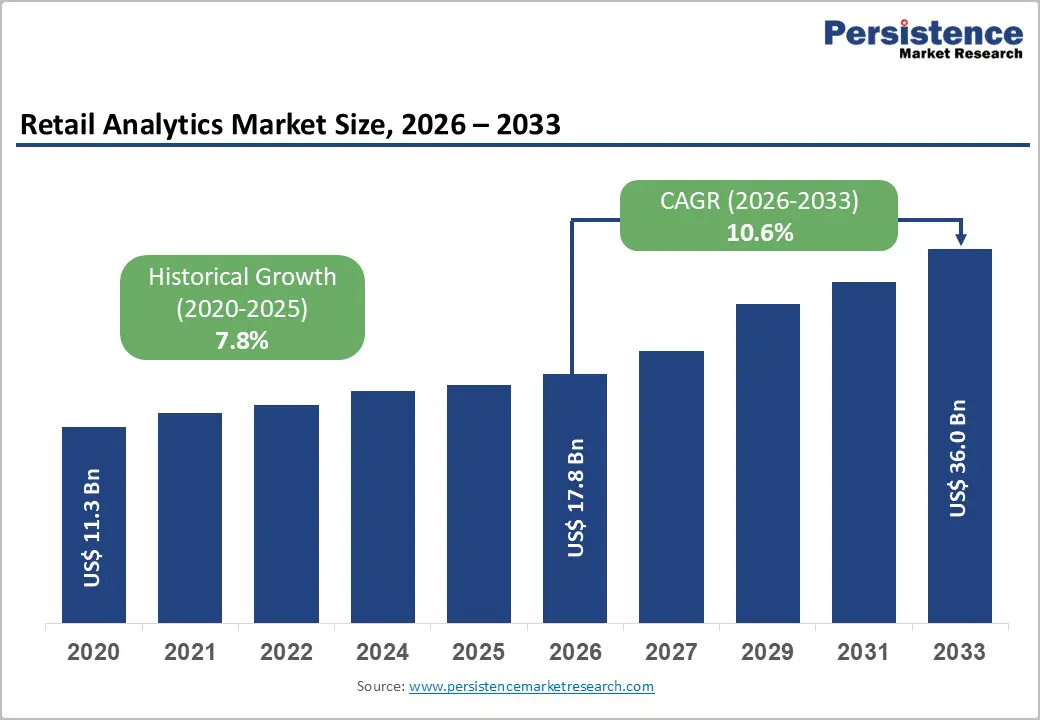

The global Retail Analytics market size is expected to be valued at US$ 17.8 billion in 2026 and projected to reach US$ 36.0 billion by 2033, growing at a CAGR of 10.6% between 2026 and 2033.

This exceptional growth trajectory is primarily driven by the retail sector’s accelerating adoption of data-driven decision-making frameworks amid intensifying competitive pressures, evolving consumer expectations, and the rapid proliferation of omnichannel commerce. Retailers are investing heavily in advanced analytics platforms, incorporating artificial intelligence, machine learning, and real-time data integration, to optimize inventory management, personalize customer experiences, and improve supply chain efficiency. The exponential growth in retail data volumes generated through point-of-sale systems, loyalty programs, e-commerce platforms, and in-store sensors is creating an urgent need for sophisticated analytical solutions capable of converting raw data into actionable commercial intelligence.

Key Industry Highlights

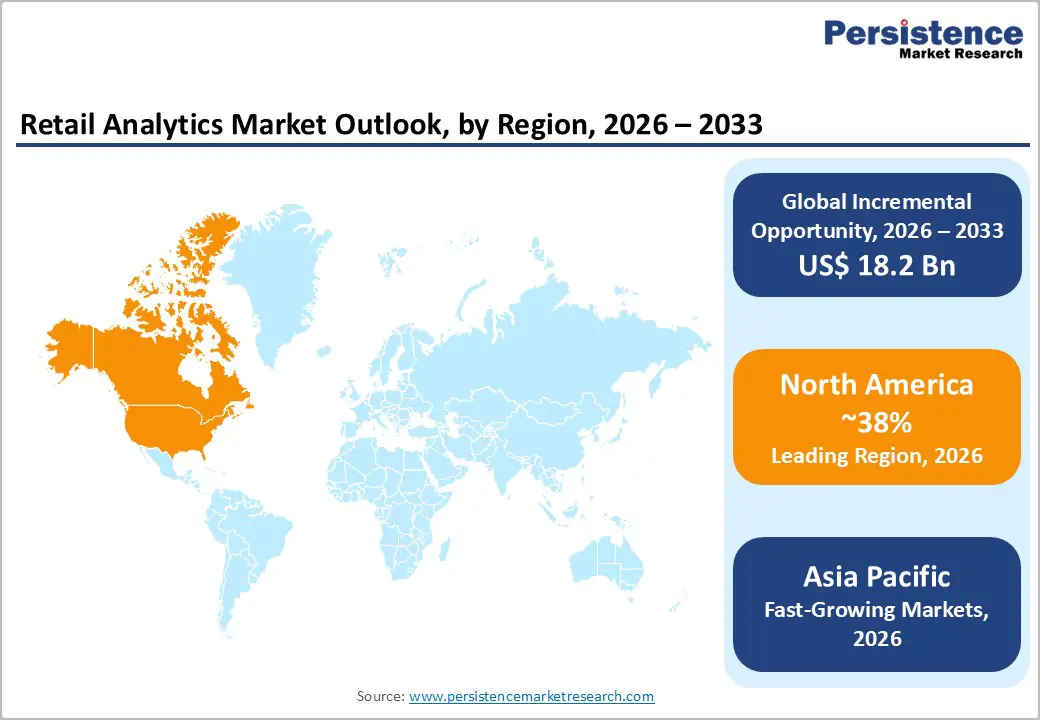

- Leading Region: North America leads the global Retail Analytics market with approximately 38% share in 2025, anchored by the United States’ concentration of technology innovation, large-scale retail enterprises, and early adoption of AI-driven analytics platforms including those from Microsoft and Salesforce.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market through 2033, driven by China’s AI-native e-commerce ecosystem, India’s rapid retail digitalization under the Digital India initiative, and ASEAN market expansion creating strong demand for cloud-based retail intelligence platforms.

- Dominant Solutions Segment: Software solutions dominate the Solution category with approximately 65% share in 2025, reflecting widespread adoption of cloud-delivered SaaS analytics platforms for predictive analytics, customer intelligence, and AI-driven merchandising optimization across global retail enterprises.

- Fastest Growing Segment: Cloud-based deployment is the fastest-growing segment within Deployment Mode through 2033, accelerated by retailers’ preference for scalable, low-capital-expenditure analytics infrastructure that enables real-time data processing and seamless integration across omnichannel commerce operations.

- Key Opportunity: The integration of generative AI into retail analytics platforms represents the most transformative near-term market opportunity, enabling natural language querying, automated insight generation, and accessible analytics for non-technical retail users, creating significant differentiation potential for platform vendors.

| Key Insights | Details |

|---|---|

|

Retail Analytics Market Size (2026E) |

US$ 17.8 Billion |

|

Market Value Forecast (2033F) |

US$ 36.0 Billion |

|

Projected Growth CAGR (2026–2033) |

10.6% |

|

Historical Market Growth (2020–2025) |

7.8% |

Market Dynamics

Drivers - Exponential Growth in Retail Data and Demand for AI-Driven Insights

The volume of data generated across retail touchpoints, including point-of-sale terminals, mobile commerce applications, loyalty programs, social media interactions, and connected in-store devices, has grown at an unprecedented pace, compelling retailers to invest in scalable analytics infrastructure. According to the International Data Corporation (IDC), the global datasphere is expected to reach 175 zettabytes by 2025, with retail among the top data-generating verticals. Artificial intelligence and machine learning embedded within analytics platforms are enabling retailers to move beyond descriptive reporting toward predictive and prescriptive capabilities, forecasting demand patterns, identifying at-risk customers, and dynamically optimizing pricing strategies in real time. Companies such as Microsoft Corporation and IBM Corporation have deepened their retail analytics offerings through AI-native cloud platforms, reflecting the sector-wide recognition that advanced analytics is now a foundational competitive capability rather than a supplementary tool.

Omnichannel Retail Expansion Accelerating Analytics Platform Adoption

The structural shift from single-channel retailing toward integrated omnichannel commerce is a fundamental demand catalyst for the retail analytics market. According to the National Retail Federation (NRF), over 73% of consumers use multiple channels during their shopping journey, creating complex, cross-touchpoint datasets that require unified analytics platforms to interpret effectively. Retailers are deploying analytics solutions that consolidate data streams from physical stores, e-commerce platforms, mobile applications, and social commerce channels into cohesive customer intelligence frameworks. This need for unified data visibility is driving investment across solutions spanning customer journey mapping, attribution modeling, and inventory synchronization analytics. Salesforce Inc. and SAP SE have both significantly expanded their retail-focused analytics suites in response to this trend, embedding omnichannel intelligence capabilities directly into their enterprise commerce platforms to serve both mid-market and large-format retail customers.

Restraints - Data Privacy Regulations and Compliance Complexity

The global expansion of data privacy legislation, including the European Union’s General Data Protection Regulation (GDPR), the California Consumer Privacy Act (CCPA), and analogous frameworks emerging across India, Brazil, and Southeast Asia, is creating significant compliance complexity for retail analytics deployments. Retailers collecting granular behavioral, transactional, and demographic data must navigate increasingly stringent consent requirements, data minimization mandates, and cross-border data transfer restrictions. A 2023 PwC consumer survey found that 85% of consumers regard data privacy as a purchasing consideration, underscoring reputational risks associated with non-compliance. These regulatory dynamics increase implementation costs, constrain the scope of permissible data collection, and introduce legal uncertainty that can delay analytics investment decisions, particularly among small and mid-sized retail operators with limited compliance infrastructure.

High Implementation Cost and Integration Challenges for Legacy Systems

A persistent barrier to retail analytics adoption, especially among traditional brick-and-mortar retailers, is the substantial upfront investment required to integrate modern analytics platforms with legacy point-of-sale, enterprise resource planning (ERP), and inventory management systems. Many established retailers operate on decades-old technological infrastructure that lacks the APIs and data architecture required for seamless analytics integration. According to a Gartner survey, over 60% of large-scale data and analytics projects experience cost overruns or timeline delays, with system integration complexity cited as the leading contributing factor. These friction points are particularly acute for independent and regional retailers, who may lack the technical resources and IT personnel required to manage complex multi-system deployments, effectively narrowing near-term addressable market potential despite strong underlying demand.

Opportunity - Generative AI Integration Creating Next-Generation Retail Intelligence Platforms

The emergence of generative artificial intelligence as a practical commercial technology is opening transformative opportunities for retail analytics platform providers. Generative AI capabilities, including natural language querying, automated insight generation, and conversational analytics interfaces, are dramatically lowering the barrier to analytics adoption among non-technical retail users, enabling store managers, merchandising teams, and marketing executives to extract data-driven insights without specialist data science expertise. Microsoft Corporation’s integration of generative AI through Copilot across its Azure retail analytics ecosystem exemplifies how leading technology vendors are embedding these capabilities at scale. According to McKinsey & Company, generative AI could add US$ 400 billion to US$ 660 billion annually in value to the retail sector globally, with productivity gains concentrated in merchandising, marketing, and customer service functions directly served by analytics platforms. Vendors that successfully embed generative AI into intuitive, accessible analytics workflows will command significant differentiation and accelerated adoption across the forecast period.

Rising Demand for Real-Time Analytics in E-commerce and Quick Commerce

The rapid growth of e-commerce and quick commerce, encompassing same-day delivery, on-demand grocery platforms, and direct-to-consumer models, is creating acute demand for real-time retail analytics capabilities. Unlike traditional retail formats where data analysis cycles of days or weeks were acceptable, e-commerce and quick commerce operations require sub-second inventory visibility, dynamic pricing engines, and real-time demand sensing to remain operationally competitive. The U.S. Census Bureau reports that e-commerce sales as a share of total U.S. retail sales have grown consistently, and global e-commerce is projected to account for over 24% of all retail sales by 2026 according to eMarketer. This structural shift is driving investment in streaming analytics architectures, real-time recommendation engines, and live supply chain intelligence platforms. Amazon Web Services and Oracle Corporation are particularly well-positioned to capture this opportunity, given their combination of cloud-native analytics infrastructure and deep integration with commerce operations platforms.

Category-wise Analysis

Solution Insights

Software solutions constitute the dominant segment within the Solution category of the Retail Analytics market, capturing approximately 65% of total market share in 2025. This leadership reflects the foundational role of software platforms, including predictive analytics and AI engines, customer analytics platforms, and reporting and visualization tools, in enabling retailers to derive actionable intelligence from their data assets. The proliferation of SaaS-based retail analytics software has significantly lowered adoption barriers, enabling retailers of varying scales to access enterprise-grade analytics capabilities through subscription models. SAP SE, SAS Institute Inc., and QlikTech International AB maintain strong software portfolio positions across the retail vertical. The rapid embedding of machine learning and AI capabilities into commercial software platforms, enabling automated anomaly detection, demand forecasting, and customer segmentation, continues to expand the functional value of software solutions and reinforce segment dominance through the forecast horizon.

Deployment Mode Insights

Cloud-based deployment is the leading segment within the Deployment Mode category, commanding approximately 62% of market share in 2025. Cloud-native retail analytics platforms offer retailers scalability, lower upfront capital expenditure, and rapid deployment timelines compared to on-premise alternatives, critical advantages in a sector characterized by seasonal demand volatility and fast-evolving technology requirements. The COVID-19 pandemic served as a major inflection point for cloud adoption in retail, as organizations required rapid digital infrastructure scaling to support sudden shifts to online commerce and remote operations. Microsoft Azure, Amazon Web Services, and Google Cloud have each established dedicated retail industry solutions that leverage cloud-native analytics capabilities, reinforcing the platform ecosystem around cloud deployment. As 5G connectivity expands and edge computing matures, cloud-based analytics architectures are further strengthening their position by enabling real-time data processing closer to store-level touchpoints.

Retail Format Analysis

E-commerce and Online Retailers represent the dominant segment within the Retail Format category, holding approximately 30% of market share in 2025. The inherently data-rich nature of digital retail, where every customer interaction, page view, search query, and abandoned cart generates analyzable data, makes e-commerce uniquely suited to advanced analytics applications. Online retailers have built analytics into their core operating models, deploying real-time recommendation engines, dynamic pricing algorithms, and customer lifetime value models that generate direct, measurable commercial returns. Amazon.com and Alibaba Group represent benchmark examples of analytics-native retail organizations that have defined industry best practices for data-driven commerce. The rapid growth of cross-border e-commerce, facilitated by platforms such as Shopify and marketplace aggregators, is further expanding the addressable analytics market within this format, as merchants seek tools to optimize product listings, customer acquisition costs, and fulfillment performance across global channels.

Function Insights

Merchandising and Pricing is the leading segment within the Function category, accounting for approximately 28% of market share in 2025. Pricing and assortment decisions are among the highest-value levers available to retail operators, with even marginal improvements in pricing accuracy or product mix optimization delivering material impact on gross margins. Advanced analytics platforms enabling dynamic pricing, markdown optimization, competitive price monitoring, and assortment planning have seen strong adoption across grocery, apparel, and electronics retail formats. The National Retail Federation (NRF) has noted that data-driven merchandising decisions are among the top strategic investment priorities for retail executives. Blue Yonder Inc. and Teradata Corporation have established strong positions within this functional segment, offering specialized platforms that combine historical sales analytics with AI-driven demand forecasting to support automated and semi-automated merchandising decisions at scale.

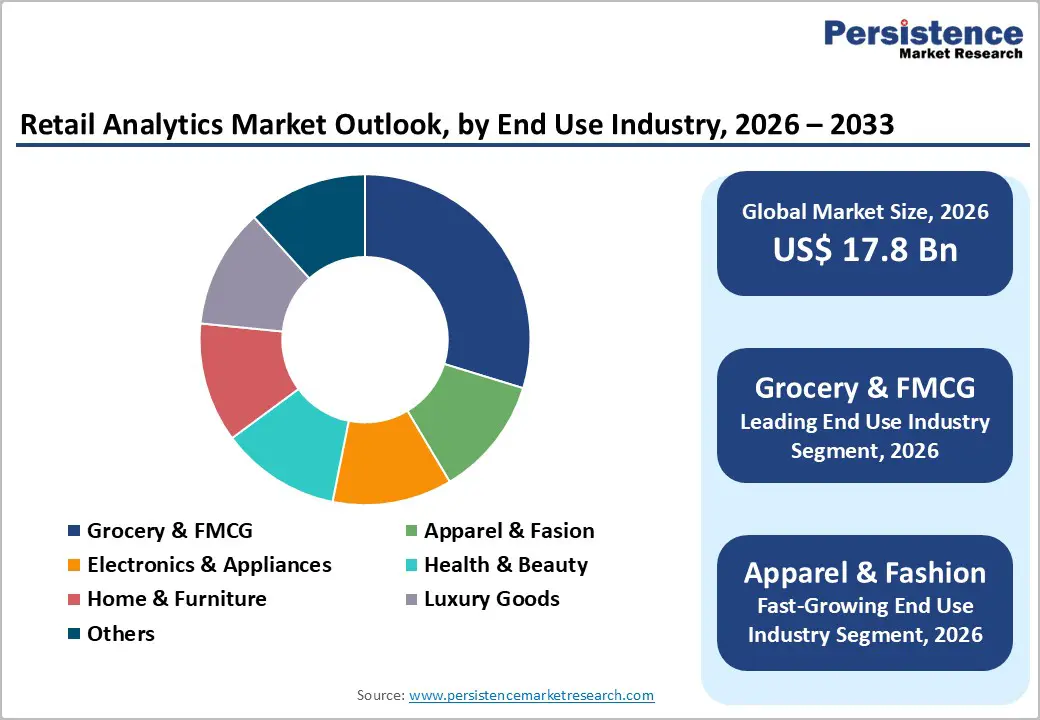

Industry Insights

Grocery and FMCG (Fast-Moving Consumer Goods) is the dominant segment within the Industry category, representing approximately 27% of market share in 2025. Grocery retail’s combination of extremely high transaction volumes, complex perishable inventory management requirements, razor-thin operating margins, and intensely price-sensitive consumer behavior creates a particularly compelling use case for advanced analytics. Retailers operating in this segment must continuously optimize promotional effectiveness, markdown timing, category layouts, supplier performance, and demand forecasting accuracy to remain operationally viable. The Food Marketing Institute (FMI) has documented that data analytics capabilities are among the top operational investment priorities for grocery retailers globally. SAP SE and Blue Yonder Inc. are prominent analytics solution providers with deep grocery and FMCG customer bases, offering integrated platforms spanning demand sensing, promotional planning, and supply chain analytics tailored to the sector’s unique operational demands.

Regional Insights

North America Retail Analytics Market Trends and Insights

North America maintains its position as the leading region in the global Retail Analytics market, accounting for approximately 38% of total market share in 2025. The United States serves as the epicenter of retail analytics innovation, home to a dense ecosystem of technology vendors, analytics startups, and early-adopting retail enterprises operating at global scale. Regulatory developments, including the California Consumer Privacy Act (CCPA) and evolving Federal Trade Commission (FTC) guidance on data practices, are shaping how analytics platforms are architected, driving investment in privacy-preserving analytics and consent management infrastructure. The U.S. retail sector, valued at over US$ 7 trillion annually according to the U.S. Census Bureau, provides an enormous and commercially sophisticated addressable base for analytics solution providers.

Leading technology corporations headquartered in North America, including Microsoft Corporation, Amazon Web Services, Salesforce Inc., Oracle Corporation, and Teradata Corporation, maintain dominant positions within the retail analytics technology stack, benefiting from deep integration with enterprise IT environments and established retail customer relationships. The region’s mature venture capital ecosystem continues to fund specialized retail analytics startups, maintaining a strong pipeline of innovation across functions including computer vision-based in-store analytics, AI-driven pricing optimization, and real-time supply chain intelligence.

Europe Retail Analytics Market Trends and Insights

Europe represents a well-established and growing market for retail analytics solutions, characterized by strong regulatory maturity and increasing cross-sector technology investment. Germany, the United Kingdom, France, and the Netherlands are the primary markets within the region, collectively hosting major retail conglomerates and sophisticated omnichannel operators that have made significant analytics investments. The European Union’s GDPR framework has been a defining structural force in the region’s analytics landscape, compelling solution providers to build privacy-by-design architectures and giving European retailers a globally recognized compliance template that is increasingly influencing analytics platform design worldwide.

The U.K. retail sector, one of Europe’s most digitally advanced, has seen strong adoption of customer analytics and loyalty analytics platforms, with retailers such as Tesco and Sainsbury’s building industry-benchmark data strategies. SAP SE, headquartered in Walldorf, Germany, is a particularly dominant vendor in the European enterprise retail analytics space. The European Commission’s Digital Decade targets and the EU Data Act, which came into force in 2024, are creating new frameworks for data sharing and interoperability that are expected to further enable analytics-driven retail innovation across member states through the forecast period.

Asia Pacific Retail Analytics Market Trends and Insights

Asia Pacific is the fastest-growing region in the global Retail Analytics market, projected to register the highest CAGR during the 2026–2033 forecast period, driven by the region’s extraordinary retail expansion, rapid digital commerce penetration, and government-supported digitalization initiatives. China represents the region’s largest and most analytically sophisticated retail market, where technology-native commerce platforms such as Alibaba Group and JD.com have established global benchmarks for real-time, AI-driven retail analytics at massive scale. China’s retail digitalization is further supported by the country’s 14th Five-Year Plan, which explicitly prioritizes digital economy development and data infrastructure investment.

India and ASEAN nations are emerging as high-velocity growth markets within the region. India’s retail sector is undergoing a structural transformation driven by the Digital India initiative, rapid smartphone penetration, and the explosive growth of platforms such as Flipkart and Reliance Retail, creating strong demand for customer analytics, supply chain intelligence, and pricing optimization tools. Japan and South Korea maintain technologically sophisticated retail analytics ecosystems, with leading retailers deploying advanced in-store sensing, loyalty analytics, and AI-driven demand forecasting. HCLTech, with significant operations across Asia Pacific, is well-positioned to serve the region’s growing analytics services demand through integrated consulting, deployment, and managed services offerings.

Competitive Landscape

The global Retail Analytics market demonstrates a moderately consolidated structure, characterized by the presence of large enterprise technology platforms, specialized analytics vendors, and emerging AI-native startups. Established platform providers leverage integrated cloud ecosystems, extensive retail customer bases, and sustained R&D investments to retain competitive advantage, while niche players differentiate through domain specialization and agile innovation cycles.

Key business strategies center on deep integration of AI and generative AI capabilities, development of cloud-native and scalable architectures, and deployment of pre-configured retail data models tailored to merchandising, supply chain, and customer intelligence functions. Vendors are increasingly adopting subscription-based and analytics-as-a-service models, alongside outcome-driven pricing frameworks tied to measurable performance improvements. Competitive intensity is further rising as cloud providers accelerate retail verticalization, embed analytics directly within commerce and ERP platforms, and enhance interoperability to support unified, omnichannel decision-making across complex retail environments.

Key Developments

- February, 2026: Enverus launched its Minerals Marketplace platform for buying and selling mineral and non-operated interests, offering direct buyer-seller engagement, secure transactions, and data-backed valuation tools to streamline mineral deals without transaction fees.

- February, 2026: Amazon unveiled new AI-powered tools to help sellers launch and manage products more effectively, offering AI-driven demand insights, faster product launches, and enhanced review and marketing capabilities to support seller growth and reduce risk.

Companies Covered in Retail Analytics Market

- Microsoft Corporation

- IBM Corporation

- Amazon Web Services

- Oracle Corporation

- Salesforce Inc.

- QlikTech International AB

- HCLTech

- Zoho Corporation

- RetailNext Inc.

- SAS Institute Inc.

- SAP SE

- Teradata Corporation

- Alteryx, Inc.

- EDITED

- Blue Yonder Inc.

- Google LLC (Google Cloud Retail)

- Tableau Software (Salesforce)

- Dunnhumby Ltd.

- 1010data (Advance Auto Parts subsidiary)

- Aptos, LLC

Frequently Asked Questions

The global Retail Analytics market is estimated at US$ 17.8 billion in 2026, growing at a 7.8% CAGR between 2020 and 2025.

Growth is driven by rising retail data volumes, omnichannel commerce expansion, and increasing adoption of AI-powered analytics platforms.

North America leads the market with approximately 38% share in 2025, supported by advanced technology adoption and major analytics vendors.

The main opportunity lies in integrating generative AI, enabling automated insights, conversational analytics, and broader accessibility for retail users.

Key players include Microsoft, SAP, IBM, Oracle, Salesforce, SAS, AWS, Qlik, Blue Yonder, Teradata, HCLTech, RetailNext, Alteryx, EDITED, and Zoho.