- Testing, Inspection, & Certification

- Postal Automation System Market

Postal Automation System Market Size, Share, and Growth Forecast, 2026 - 2033

Postal Automation System Market by Component Type (Hardware, Software, Services), Technology (Culler Facer Canceller, Letter Sorter, Flat Sorter, Mixed Mail Sorter, Parcel Sorter, Others), Application (Government Postal, Commercial Postal), and Regional Analysis for 2026 - 2033

Postal Automation System Market Size and Trends Analysis

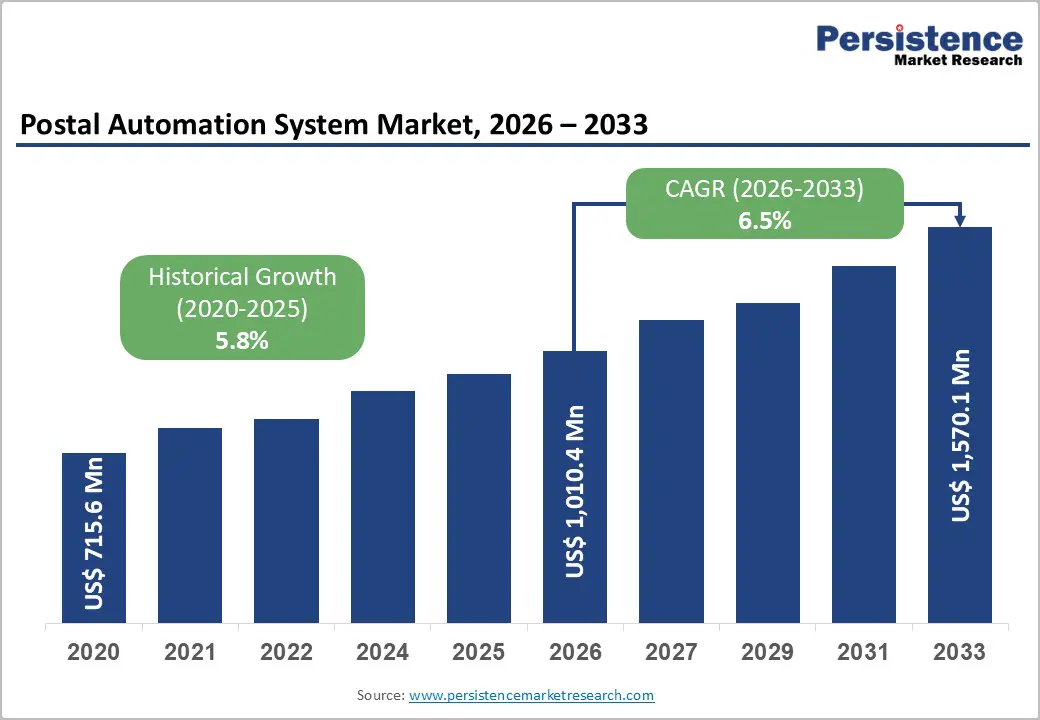

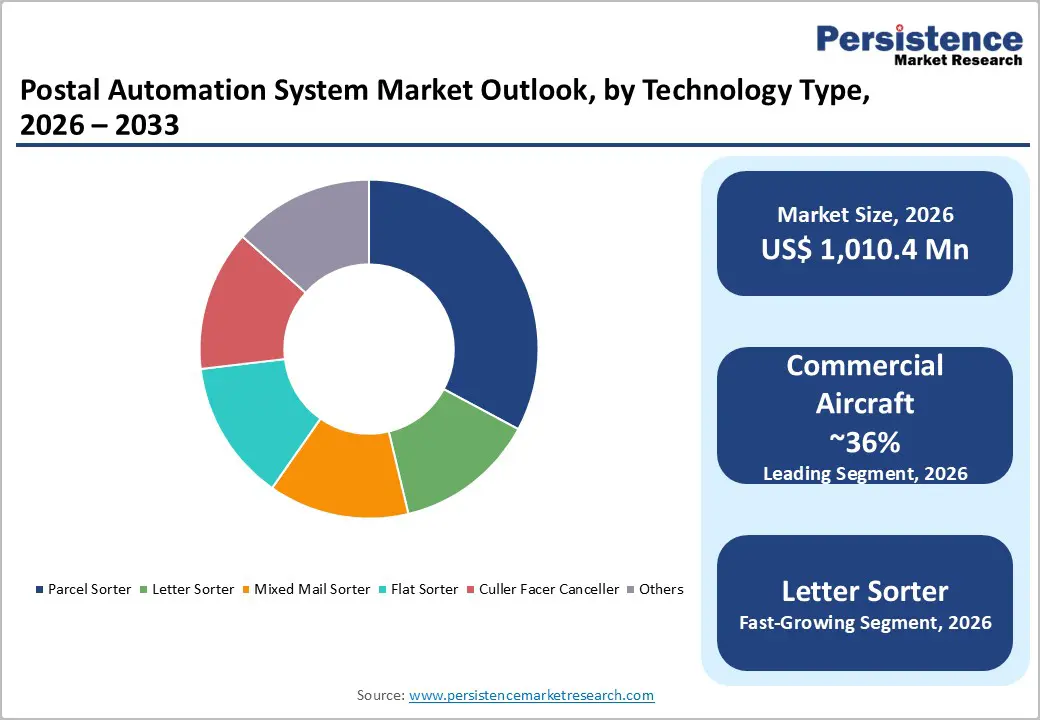

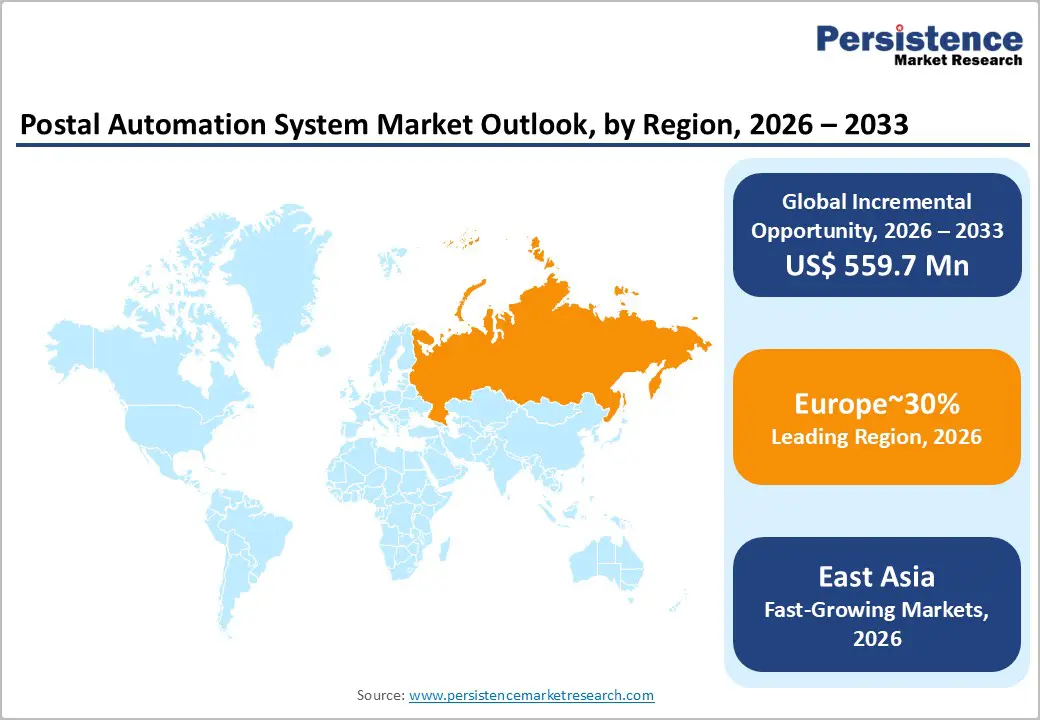

The global postal automation system market size is likely to be valued at US$ 1,010.4 million in 2026 and is projected to reach US$ 1,570.1 million by 2033, growing at a CAGR of 6.5% between 2026 and 2033. This trajectory is built from a market base of approximately US$ 715.6 million in 2020, reflecting a 5.8% historical CAGR over six years.

The market expansion is propelled by the unprecedented surge in parcel volumes driven by e-commerce expansion, with global parcel deliveries reaching 217 billion units in 2025 representing growth of approximately 5,900 parcels per second. The systematic replacement of labor-intensive manual sorting with advanced automation technologies incorporating artificial intelligence, robotics, and IoT integration is driving market traction. The consolidation of the competitive landscape, notably exemplified by Körber's €1.15 billion acquisition of Siemens Logistics' mail and parcel business in 2022, which has strengthened global capacity for large-scale, integrated automation solutions, and regional variations with North America and East Asia reflect differing maturity profiles and e-commerce penetration rates across postal ecosystems globally.

Key Industry Highlights:

- Leading Region: Europe holds the largest share at approximately 30%, driven by Germany, France, UK, and Scandinavian countries investing in postal automation and labor cost optimization.

- High-Growth Region: East Asia is the fastest-growing market, fueled by China, Japan, South Korea, and emerging Southeast Asian e-commerce infrastructure buildout and modernization programs.

- Dominant Component: Hardware dominates with 61% share, including high-speed sorting machines, conveyor systems, and barcode scanners essential for operational efficiency.

- Fastest-Growing Component: Software solutions are rapidly expanding, driven by AI-powered sorting, predictive analytics, and integration with legacy infrastructure for improved throughput and accuracy.

- Largest Technology: Parcel sorters hold 36% market share, reflecting the structural shift from letters to high-volume e-commerce packages requiring automated cross-belt and optical scanning systems.

| Key Insights | Details |

|---|---|

| Postal Automation System Market Size (2026E) | US$ 1,010.4 Mn |

| Market Value Forecast (2033F) | US$ 1,570.1Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Dynamics

Drivers - Exponential E-Commerce Volume Growth and Last-Mile Delivery Pressure

The e-commerce sector's rapid expansion has fundamentally reshaped postal infrastructure requirements. Global e-commerce sales reached approximately US$5.2 trillion and are projected to grow by 56 percent over the next four years, directly translating into unprecedented parcel processing demands on traditional postal networks.

The Postal Automation System Market must accommodate this volumetric shift while maintaining service velocity and accuracy standards that consumers increasingly expect. Automated sorting systems can process between 40,000 to 42,500 items per hour representing a tenfold improvement over manual sorting operations that handle approximately 4,000-5,000 items daily. This capacity differential is critical: operators that fail to automate face service degradation and competitive disadvantage against courier and logistics firms investing heavily in mechanization.

The market impact manifests as mandatory capital expenditure cycles for national postal organizations, evident in coordinated automation deployments across Europe, Asia-Pacific, and North America during 2023-2025.

Government Digital Transformation Mandates and Infrastructure Investment

Sovereign governments increasingly view postal system modernization as essential infrastructure development aligned with digital economy objectives. India's Department of Posts launched IT 2.0 Advanced Postal Technology representing a INR 5,800 crore approximately US$700 million investment program to upgrade 1.65 lakh (165,000) post offices nationwide with cloud-based systems, QR-code-based payments, and 10-digit DIGIPIN addressing protocols. Concurrent initiatives include India's Digital Address Code infrastructure project and partnerships integrating postal networks with e-commerce platforms, such as Amazon integration in northeastern regions.

The European Union's digital infrastructure directives have similarly mandated postal service modernization across member states, with Germany, France, and the UK deploying government-funded automation projects valued at €200 plus million annually. These policy-driven investments establish multi-year demand pipelines for the Postal Automation System Market, particularly in hardware deployment and systems integration services.

Restraint - Capital Intensity and Financing Barriers for Smaller Operators

The postal automation system market exhibits a structural accessibility problem: comprehensive automation solutions require capital investments ranging from US$20-50 million for mid-scale sorting facilities and US$80-150 million for large regional hubs. Smaller postal operators, particularly those in developing economies or rural regions, cannot amortize such investments over sufficient parcel volumes, creating a competitive bifurcation. Capital constraints are compounded by limited access to favorable financing, as financial institutions perceive postal operators as non-core lending segments. This barrier has resulted in a two-tier market structure where dominant players consolidate automated infrastructure while smaller competitors face operational efficiency disadvantages.

Opportunity - Emerging Market E-Commerce Infrastructure Buildout

Developing economies in Southeast Asia, South Asia, and Africa are experiencing early-stage e-commerce penetration coupled with minimal existing automation infrastructure. China's parcel volume reached 100+ billion units annually in 2024, yet vast regional sorting operations remain semi-automated. Indonesia, Vietnam, Thailand, and India represent greenfield opportunities for the Postal Automation System Market, where national postal operators must simultaneously build infrastructure and modernize operations. India Post's digital transformation initiatives, including partnerships with private e-commerce operators and government support for rural logistics through the Dak Ghar Niryat Kendra (DNK) program, which has onboarded 3,400 plus exporters signal demand for scalable, cost-effective automation solutions tailored to high-volume, mixed-item parcel processing.

The Indo-Thai bilateral postal agreement, formalized in August 2024, establishing cross-border tracked packet services, demonstrates how automation becomes essential infrastructure for postal service convergence. These emerging markets offer a higher CAGR potential of around 10-12% annually than mature markets, as they are installing automation systems for the first time rather than replacing legacy equipment.

AI-Driven Autonomous Sorting and Lights-Out Facility Concepts

The integration of artificial intelligence, machine learning, and advanced robotics into postal sorting creates opportunities for fundamentally different operational models. BEUMER Group's March 2025 demonstration of "lights-out" warehouse automation with AutoDrop functionality processing 10,000 pieces per hour with automated, space-optimized unloading represents a prototype for next-generation facilities requiring minimal human intervention. These systems reduce operational staffing by 50-60% compared to semi-automated facilities while maintaining throughput targets and improving accurate metrics.

The market can expand substantially by offering modular, software-driven solutions that existing operators can retrofit to legacy infrastructure. India Post's IT 2.0 platform, incorporating centralized sorting configuration and network-wide uniform parcel processing logic, demonstrates demand for intelligent software layers that overlay existing hardware. Market participants offering AI-powered address recognition, dynamic route optimization, and predictive failure analytics, addressing traditional Chinese characters as demonstrated by NEC's Hong Kong Post system upgrade address specific regional requirements while commanding premium pricing.

Category-wise Analysis

Component Type Insights

Hardware components hold the largest share around 61%, including automated sorting machines, conveyor systems, barcode scanners, and robotic handling equipment dominate the Postal Automation System Market by revenue, reflecting the capital-intensive nature of infrastructure modernization. Sorting machines designed for letter processing capable of 40,000+ items/hour, and parcel processing 8,000-15,000 items/hour command premium valuations due to their operational criticality.

The Toshiba system deployed at Chunghwa Post's major Taiwan mail centers in March 2018, processing 42,500 letters hourly and 8,000 packages hourly, exemplifies hardware's performance standards. These systems incorporate advanced character recognition and barcode reading technologies requiring significant R&D investment and integration expertise.

The hardware segment's share reflects multi-year replacement cycles for postal operators, where equipment typically operates 15-20 years before technological obsolescence or capacity constraints necessitate upgrades. This stable, predictable demand profile makes hardware a core revenue anchor for market participants, though margins face compression as competition intensifies among established vendors.

Software solutions for postal automation represent the fastest-expanding component segment, driven by operators' recognition that hardware throughput gains depend critically on intelligent control systems, integration platforms, and data analytics capabilities.

Technology Insights

Parcel sorters represent the dominant technological segment, holding a share of 36% within the Postal Automation System Market, reflecting the structural shift in postal traffic composition away from letters toward packages. Parcel sorters employ cross-belt conveyor technology, advanced optical scanning, and destination-based routing to segregate packages by delivery zones with minimal human intervention.

Processing capacities range from 8,000 to 15,000+ items per hour, depending on system sophistication, module count, and automation density. The Posten Bring facility in Jönköping, Sweden, equipped with Fives' singulator and cross-belt sorter technology, addresses a 169% surge in parcel volumes over three years by deploying a system designed to boost sorting capacity by approximately 300%. Fives' GENI-Belt cross-belt sorter deployed for ACS Courier in Athens handles over 15,000 items per hour with integrated induction lines and slide chutes for reliability and accuracy optimization. Parcel sorter dominance reflects e-commerce's persistent growth: global parcel volumes are projected to continue expanding at 8-12% annually through 2030, while letter volumes contract at 3-5% annually.

Regional Insights

North America Postal Automation Market Trends

North America commands approximately 27% of the global Postal Automation System Market, representing the largest single regional market despite recent growth moderation. The United States Postal Service (USPS) and Canada Post have implemented substantial automation modernization programs, with capital deployment averaging US$300-400 million annually across mail sorting infrastructure, parcel handling systems, and processing facility upgrades. Labor cost dynamics serve as the primary demand driver: North American postal and logistics operations face documented annual wage escalation of 15-20% combined with persistent workforce shortages, making automation investment economically justified despite capital intensity.

The North American market exhibits mature competitive dynamics dominated by established vendors such as Lockheed Martin Corporation, which supplies automated mail handling systems for USPS regional facilities; Pitney Bowes maintains a significant presence in mailroom automation serving corporate and government clients; and Vanderlande Industries provides conveyor and sortation systems.

The 2022 - 2024 period witnessed substantial regulatory and policy attention to postal service efficiency, particularly following disruptions to Canada Post operations in late 2024, intensifying focus on infrastructure modernization as a pathway to service reliability. Investment trends favor software integration and real-time tracking capabilities, reflecting customers' demand for visibility into parcel status and delivery timing requirements that hardware-only solutions no longer satisfy.

East Asia Postal Automation Market Trends

East Asia represents the highest-growth regional market within the Postal Automation System Market, driven by e-commerce expansion in China, Japan, South Korea, and emerging penetration in Southeast Asia. The Chinese postal system, operator of the world's largest parcel sorting infrastructure, drives substantial equipment demand through volume alone, though fragmentation between state and private operators creates vendor diversity.

Taiwan's postal modernization exemplifies regional trends. Toshiba's March 2018 deployment of high-speed automated letter and parcel sorting systems at Chunghwa Post's major mail centers represented a significant capability enhancement, with integrated systems featuring advanced character recognition and barcode reading technologies enabling processing of 42,500 letters and 8,000 packages hourly.

The project's turnkey delivery and long-term maintenance support model strengthened Toshiba's regional positioning, demonstrating the integration services dimension of the Postal Automation System Market. Hong Kong's postal automation modernization continued through 2024, with NEC's February 2017 system upgrade introducing traditional Chinese character recognition and sorting for automated processing of 564,000 items hourly across 15 Central Mail Centre operational systems, reflecting regional requirement specificity.

Europe Postal Automation Market Trends

Europe maintains the largest regional market share at approximately 30% of global postal automation value, with demand concentrated in Germany, France, United Kingdom, and Scandinavian countries.

Germany leads European automation adoption through Deutsche Post DHL Group's continuous infrastructure modernization, with facility automation spanning letter processing, parcel sorting, and delivery logistics. The country's labor cost structure averages approximately €45,000-55,000 annually, and combined with workforce availability constraints, has driven sustained automation investment. Sweden's Posten Bring demonstrates regional modernization trends through the October 2023 deployment of Fives' advanced sorting systems at the flagship Jönköping facility, addressing 169% parcel volume growth over three years through a system architecture designed to deliver approximately 300 percent capacity enhancement. The system's design incorporates singulator and cross-belt sorter technology, enabling flexible reconfiguration for evolving parcel size and weight distributions essential capability in markets experiencing rapid e-commerce category expansion.

Competitive Landscape

The global Postal Automation System market is consolidated, dominated by a few major players due to high technological complexity and capital-intensive infrastructure. Leading companies such as Körber AG, NEC Philippines, SOLYSTIC, Pitney Bowes Inc., Vanderlande Industries B.V., and BEUMER Group offer comprehensive solutions across hardware, software, and services for letter, flat, mixed mail, and parcel sorting systems. These players focus on innovations like AI-enabled sorting, robotics, and smart conveyors to improve efficiency and reduce manual handling. Smaller companies provide niche or regional solutions, creating limited market fragmentation. Strategic partnerships, mergers, and government and commercial postal contracts further strengthen the positions of the top players. The market’s consolidated nature enables these key players to set industry standards while addressing growing e-commerce and logistics demands.

Key Developments:

- In March 2025, BEUMER Group showcased its latest innovations in postal and logistics automation at PROMAT 2025, Chicago, emphasizing fully automated “lights-out” warehouse solutions. The company introduced the AutoDrop function for its BG Pouch System, enabling automated, space- and weight-optimized unloading of conveyed goods, processing up to 10,000 pieces per line per hour, reducing manual handling, and improving order throughput.

- Additionally, BEUMER demonstrated Dynamic Bulk Pick, an AI-driven robot-assisted system for automated loading of loop and line sorters, enhancing efficiency in parcel and postal operations. These technologies reinforce BEUMER’s position as a pioneer in postal automation systems and end-to-end intralogistics automation.

Companies Covered in Postal Automation System Market

- Toshiba Infrastructure Systems & Solutions Corporation

- Körber AG

- NEC Philippines, INC.

- SOLYSTIC

- Pitney Bowes Inc.

- Vanderlande Industries B.V.

- Fives Group

- Leonardo S.p.A.

- Lockheed Martin Corporation

- BEUMER GROUP

- Interroll Group

- Dematic

- Eurosort

- Fluence Automation LLC.

Frequently Asked Questions

The Global Postal Automation System Market is projected to be valued at US$ 1,010.4 Mn in 2026.

The Parcel Sorter segment is expected to account for approximately 36% of the Global Postal Automation System Market by Technology Type in 2026.

The market is expected to witness a CAGR of 6.5% from 2026 to 2033.

Exponential e-commerce volume growth, last-mile delivery pressure, and government-driven digital transformation mandates are driving Postal Automation System Market growth.

Greenfield e-commerce infrastructure built out in emerging markets and adoption of AI-driven autonomous sorting and lights-out facilities present key growth opportunities in the Postal Automation System Market.

Key players in the Postal Automation System Market include Körber AG, NEC Philippines, SOLYSTIC, Pitney Bowes Inc., Vanderlande Industries B.V., and BEUMER Group.