- Transportation & Logistics

- North America Postal Services Market

North America Postal Services Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

North America Postal Services Market By Service Type (Standard Postal Services, Express Postal Services / Courier / CEP), Item Type (Letters & Documents, Parcels & Packages), Destination (Domestic Postal Services, International Postal Services), Industry (E-commerce & Retail, Government & Public Sector, BFSI, Healthcare & Pharmaceuticals, Manufacturing & Industrial) and Country Analysis for 2026 - 2033

North America Postal Services Market Trends & Analysis

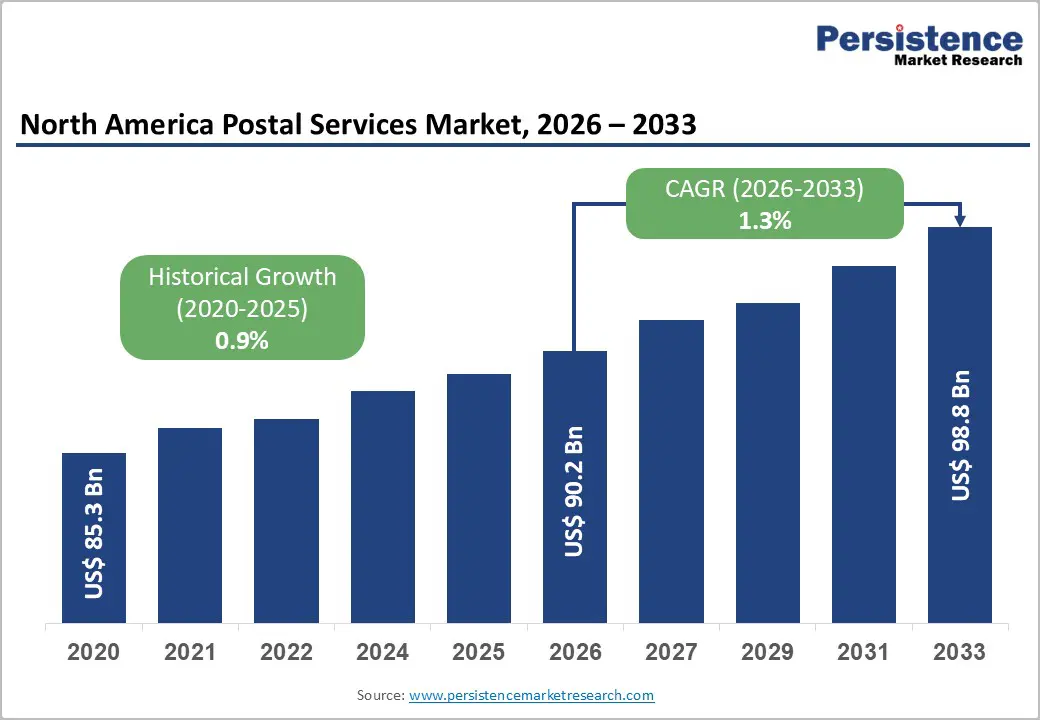

The North America postal services market size is anticipated at US$ 90.2 billion in 2026 and is projected to reach US$ 98.8 billion by 2033, growing at a CAGR of 1.3% between 2026 and 2033.

The market's steady expansion is anchored by surging e-commerce parcel volumes, digital transformation of delivery networks, and sustained last-mile infrastructure investment. The shift from traditional letter mail to parcel delivery, now accounting for 58.1% of item volume, continues to redefine service portfolios for both legacy postal operators and private couriers.

Technological convergence across route optimization, real-time tracking, and automated sorting is driving operational efficiency gains. Simultaneously, regulatory mandates supporting universal service obligations and cross-border trade facilitation under USMCA are reinforcing network investment across the U.S. and Canada.

Key Industry Highlights:

- Leading Service Type: Standard postal services lead with 62.9% share in 2026; Express postal /CEP is the fastest-growing at 3.3% CAGR, driven by e-commerce same/next-day delivery demand.

- Top Item Segment: Parcels & packages commands 58.1% share; Letters & documents are declining at –1.5% CAGR amid accelerating digital substitution across BFSI and government sectors.

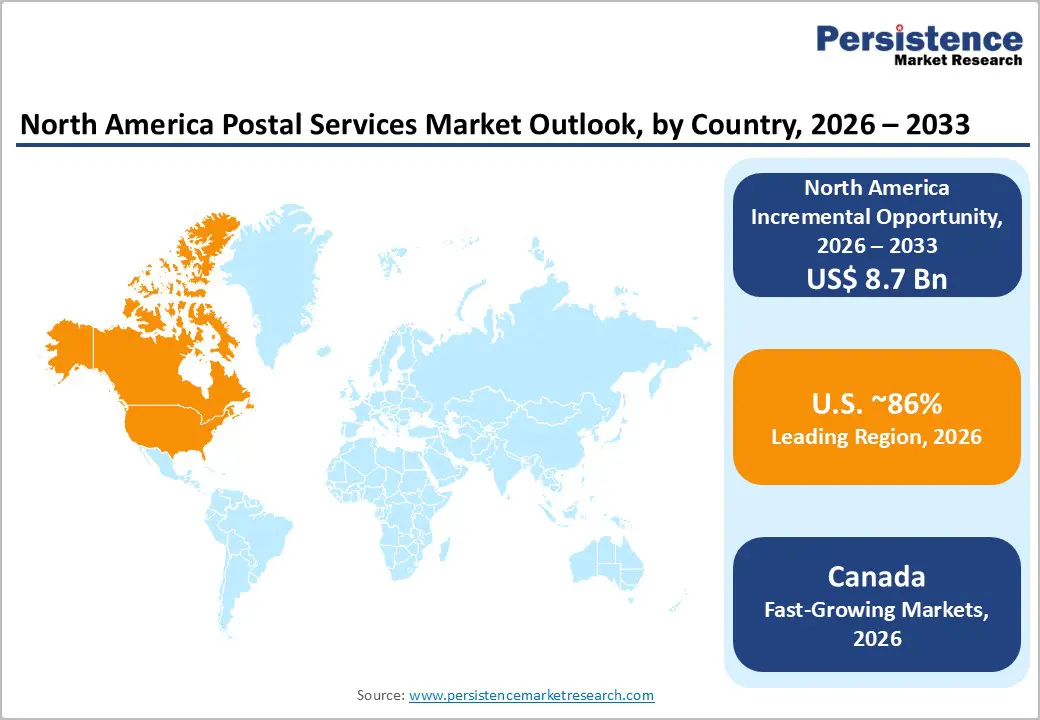

- Country Leader: The U.S. holds 86% of the regional market share, with the Southern U.S. representing ~USD 28.5 Bn; Canada is likely to reach a 1.1% CAGR, with Ontario anchoring ~USD 5.3 Bn in sub-national revenue.

- Emerging Vertical: Healthcare & pharmaceuticals is the fast-growing vertical at 3.0% CAGR, creating high-margin cold-chain delivery opportunities for certified postal and courier operators.

- Competitive Shift: Amazon overtook USPS as the top delivery provider by volume in 2026; UPS leads revenue-based share at 29.8%, signaling a structural market reorganization.

Market Dynamics Analysis

Drivers - E-commerce-Led Parcel Volume Surge

The exponential growth of online retail in North America is the primary driver of demand for postal services. The U.S. e-commerce parcel delivery market was valued at approximately USD 68.86 billion in 2024, projected to grow at a CAGR of 9.8% through 2034, directly feeding last-mile delivery volumes for both private carriers and USPS. Amazon, Walmart, and Shopify collectively drove over 60% of consumer parcel growth in 2024. The South U.S. region alone captured 32.2% of e-commerce logistics share in 2025, supported by port proximity and nearshoring infrastructure along the Gulf Coast.

Consumer expectations for same-day and next-day delivery have compelled postal operators to expand sorting automation, fulfillment density, and carrier partnerships. According to supply chain data, next-day services led U.S. delivery revenue with a 41.8% share in 2025, signaling premium service demand as the core revenue growth lever. This dynamic is pushing postal service providers toward higher-value express-parcel tiers, accelerating market monetization beyond traditional letter revenue streams.

Technological Modernization and Automation Investment

Automation, artificial intelligence, and real-time logistics platforms are fundamentally restructuring the economics of postal service delivery across North America. AI-powered predictive analytics, now deployed across route planning, inventory management, and dynamic pricing, are compressing operational costs while improving delivery accuracy and customer satisfaction metrics. The integration of machine learning in sortation facilities has reduced per-parcel handling costs and enabled scalable capacity during peak seasons for both USPS and private operators.

The deployment of drone delivery pilots, autonomous last-mile vehicles, and digital dispatch platforms is accelerating carrier differentiation. UPS's "Better Not Bigger" strategic pivot explicitly targets technology investment in AI and robotics as a long-term profitability driver, alongside targeted acquisitions in healthcare logistics. These investments reflect a broader industry consensus that technology modernization, not volume expansion alone, will determine competitive positioning and margin quality by 2033.

Restraints - Decline in Letter Mail and Flat Revenue Mix

The secular decline of first-class letter mail remains a persistent structural challenge for North American postal operators. USPS letter and document volumes have contracted at approximately –1.5% CAGR, reflecting accelerating digital substitution driven by e-billing, e-government services, and electronic communication platforms. This deterioration in revenue mix disproportionately affects universal service obligation (USO) carriers, which must maintain infrastructure for declining-volume segments, creating operational inefficiencies and profitability pressures that private carriers are not subject to.

Intensifying Low-Cost Competitive Pressure from Gig Economy Platforms

The emergence of gig-economy delivery platforms, operating with variable-cost driver networks and minimal fixed infrastructure, is disrupting traditional postal service pricing in the high-frequency, low-value parcel tier. As USPS Postmaster General Steiner acknowledged in March 2026, "low-cost delivery providers using gig drivers are creating a dramatic change in how that market is being served." Amazon's reported intent to reduce USPS-bound volume by at least two-thirds by October 2026 further concentrates this competitive threat, risking volume loss from one of USPS's largest commercial clients and applying downward pressure on pricing across the sector.

Opportunities - Healthcare & Pharmaceutical Cold Chain Logistics

The healthcare and pharmaceuticals vertical represents a lucrative growth opportunity, as well as a fast-growing industry. The expansion of specialty drug distribution, direct-to-patient pharmaceutical delivery, and temperature-controlled medical supply chains requires certified, compliant, and trackable postal infrastructure. Regulatory mandates from the FDA and Health Canada governing controlled substances and biologic product delivery are creating captive demand for postal operators with validated cold-chain capabilities.

UPS Healthcare's strategic acquisitions and dedicated medical logistics infrastructure signal the scale of this opportunity. The addressable market for pharmaceutical courier services in North America is estimated in excess of USD 12 billion by 2027, with temperature-sensitive parcel shipments growing at high single-digit annual rates. Postal operators with CGMP-compliant infrastructure and last-mile cold-chain integration are positioned to capture significant incremental revenue from this clinically regulated demand.

Smart City & Government Digital Infrastructure and Cross-Border E-commerce

Government modernization agendas across North America are driving procurement demand for secure, trackable postal services that support digital identity, census operations, and public health communications. Federal and state government agencies remain a foundational revenue base, with opportunities expanding into secure document exchange, election mail management, and last-mile connectivity for underserved rural communities where private carriers lack economic incentive to operate.

International postal services, currently accounting for 19.3% of destination-based market volume, represent a high-growth opportunity anchored in USMCA cross-border trade flows. International postal services are poised to grow at a leading CAGR, driven by SME cross-border e-commerce between the U.S., Canada, and global trade partners. Simplified customs clearance procedures, real-time duty-calculation platforms, and harmonized postal tariffs under bilateral agreements are reducing friction in cross-border shipments.

Category-wise Analysis

Service Type Insights

Standard postal services leads the North America postal services market with a 62.9% revenue share in 2026, underpinned by the sheer scale of USPS universal service operations and established commercial contract mail volumes across government, BFSI, and healthcare verticals. Compared to Express Postal Services, Standard services benefit from a broader addressable base, including non-time-sensitive e-commerce returns, utility bills, and regulated communications, segments that remain largely insulated from platform substitution. A shift in dominance toward Express/CEP is plausible over 2028–2030 as premium parcel demand scales.

Express Postal Services (Courier/CEP) is a fast-growing service with a 3.3% CAGR, driven by same-day and next-day consumer delivery demand, B2B time-sensitive shipments, and pharmaceutical cold-chain logistics. Rising consumer willingness to pay for speed and certainty underpins sustained premium pricing power.

Item Type Insights

Parcels & Packages commands a 58.1% share in 2026, reflecting the structural pivot of postal networks from communication-era letter handling to commerce-era parcel fulfillment. This dominance is supported by the compounding growth of e-commerce, marketplace returns logistics, and subscription box distribution across the U.S. and Canada. While letters & documents retain a residual base in regulated industries, the gap between the two segments is widening, and Parcels are expected to consolidate further toward a 65%+ share by 2033.

Parcels and packages are the item types driving growth, while letters and documents are declining at a -1.5% CAGR, reflecting irreversible digital substitution in billing, legal, and communications sectors. Parcel volume growth is fuelled by elevated return rates, cross-border e-commerce, and B2B industrial shipments.

Destination Insights

Domestic Postal Services holds an 80.7% market share, reflecting the depth and density of intra-national commerce, universal service obligations, and established last-mile infrastructure across U.S. suburban and rural geographies. The domestic segment benefits from predictable regulatory frameworks, established carrier networks, and the concentrated e-commerce demand base within North America. While structurally dominant, the domestic share is expected to gradually moderate as cross-border trade facilitation matures and international volumes scale.

International Postal Services is the fastest-growing destination segment, with a 3.6% CAGR, driven by expanding USMCA e-commerce corridors, growing SME cross-border trade, and increasing outbound shipments of pharmaceutical and technology products from North American manufacturing hubs.

Industry Insights

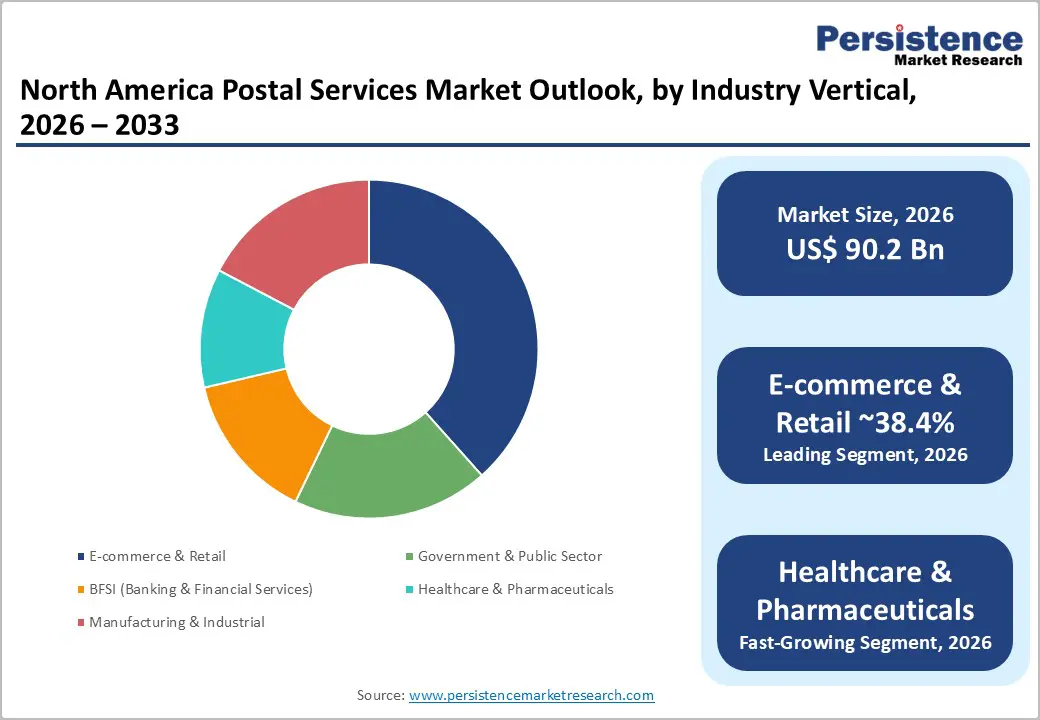

E-commerce & Retail leads all verticals with a 38.4% share in 2026, and this dominance reflects the industry's profound structural dependency on postal and parcel networks for fulfillment, returns, and last-mile delivery. No other vertical approaches this scale or growth intensity. Amazon, Walmart, and direct-to-consumer brands collectively generate over one-third of all postal service revenue, and this concentration is only deepening as online retail penetration expands. A dominance shift is unlikely before 2033, given e-commerce penetration still has significant headroom.

Country Insights

U.S. Postal Services Market Trends

The U.S. holds an 86% share of the North America postal services market, representing approximately USD 77.6 billion in 2026, anchored by USPS's constitutionally mandated universal service network and the scale of private courier operations by UPS, FedEx, and Amazon Logistics. The regulatory environment, governed by the Postal Regulatory Commission (PRC) and the Postal Accountability and Enhancement Act, establishes rate-setting, service standard enforcement, and competitive access rules that define the operating parameters for all carriers.

Southern U.S. Postal Services Market

The Southern U.S. market accounts for approximately USD 28.5 billion, driven by population density, manufacturing nearshoring corridors, Gulf Coast port activity, and the concentration of distribution infrastructure along Interstate 35 and I-10 trade corridors. Texas, Florida, and Georgia anchor Southern market leadership through high e-commerce fulfillment density and cross-border USMCA freight flows.

The Northeast and Midwest follow as the second- and third-most prominent sub-markets, supported by high-density urban delivery networks in New York, Chicago, and Boston, along with significant BFSI and healthcare postal demand from financial and pharmaceutical sector headquarters concentrated in these regions.

Canada Postal Services Market

Canada contributes approximately 14% of the North American postal services market, with a stable growth trajectory at 1.1% CAGR driven by e-commerce adoption, multicultural urban population growth, and cross-border trade facilitation. Canada Post Corporation operates the universal service network under the Canada Post Corporation Act, while FedEx Canada and UPS Canada compete in the express and premium parcel segments.

Ontario Postal Services Market Trends

Ontario accounts for approximately USD 5.3 billion in postal services revenue, reflecting its status as Canada's most populous province and primary e-commerce fulfillment hub, housing the Greater Toronto Area's dense consumer base, major logistics parks, and financial sector concentration. Canada Post's ongoing Smart Delivery and parcel locker expansion initiatives are concentrated in Ontario's urban-suburban corridors, supported by regulatory harmonization under the CRTC and Canada Post review framework.

Quebec and British Columbia represent the second- and third-most prominent Canadian sub-markets, with Quebec's bilingual regulatory environment and BC's Pacific Gateway positioning supporting distinct postal service demand profiles and cross-border parcel activity via Vancouver's international freight corridors.

Competitive Landscape

The North America postal services market exhibits a moderately consolidated structure, where a small number of dominant operators, USPS, UPS, FedEx, and Amazon Logistics, collectively account for the substantial majority of revenue. Key differentiators include network density, last-mile delivery speed, technology investment in tracking and AI-routing, and vertical specialisation in healthcare or B2B logistics. Platform-based gig-economy entrants are fragmenting the low-value parcel tier, intensifying competition at the margin.

Innovation, network expansion, and cost leadership define the three dominant strategic themes. UPS's "Better Not Bigger" pivot targets premium healthcare and SMB verticals; FedEx's DRIVE programme pursues USD 2.2 billion in structural cost savings by FY2025; and Amazon Logistics has overtaken USPS as the top delivery provider by volume in early 2026, signalling a paradigm shift in competitive dynamics.

Strategic Developments

- In September 2024, UPS officially assumed role as USPS's primary air cargo provider, replacing FedEx after a 20-year contract. The USD multi-billion agreement covers Priority Mail Express and Priority Mail, reinforcing UPS's integrated ground-air network strategy and expanding domestic air sortation capacity.

- In March 2024, FedEx announced USD 1.8 billion in cost savings for FY2024 and USD 2.2 billion targeted for FY2025 through the DRIVE restructuring initiative, consolidating express and ground networks and renegotiating vendor contracts to improve margin quality post USPS contract loss.

- In April 2025, FedEx and UPS collectively invested USD 20 million in federal lobbying in 2025 to influence postal regulatory reform as USPS faced financial restructuring. Both companies sought to shape PRC rate-setting rules and expand private carrier access to USPS infrastructure.

North America Postal Services Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 85.3 Bn |

|

Current Market Value (2026) |

US$ 90.2 Bn |

|

Projected Market Value (2033) |

US$ 98.8 Bn |

|

CAGR (2026–2033) |

1.3% |

|

Leading Country |

United States |

|

Dominant Service Type |

Standard Postal Services, 62.9% |

|

Top-ranking Product |

Parcels & Packages, 58.1% |

|

Incremental Opportunity |

US$ 8.7 Bn |

Companies Covered in North America Postal Services Market

- United States Postal Service

- United Parcel Service

- FedEx

- Amazon Logistics

- DHL Express

- Canada Post

- OnTrac

- LaserShip

- Purolator

- XPO Logistics

- GEODIS

- Pitney Bowes

- Stamps.com

- GLS Canada

- Intelcom Express

Frequently Asked Questions

E-commerce parcel volume growth, technological automation, and cross-border trade facilitation under USMCA are the primary demand drivers, with the U.S. e-commerce parcel market alone growing prominently in the forecast period.

The North America postal services market is projected to grow at a CAGR of 1.3% from 2026 to 2033, with Express Postal / CEP services expanding at the faster sub-segment rate of 3.3% CAGR.

Healthcare cold-chain logistics (3.0% CAGR), international cross-border e-commerce (3.6% CAGR), and government digital infrastructure postal mandates represent the three highest-value actionable opportunities by 2033.

USPS, UPS, FedEx, Amazon Logistics, DHL Express, and Canada Post are the dominant operators, with Amazon having overtaken USPS as the highest-volume delivery provider in North America as of early 2026.