- Automation & Robotics

- Pneumatic Valves & Accessories Market

Pneumatic Valves & Accessories Market Size, Share, and Growth Forecast 2026 – 2033

Pneumatic Valves & Accessories Market by Product Type (Sliding Shaft, Rotating Shaft), Application (Chemicals and Petrochemicals, Power Generation and Management, Others), and Regional Analysis for 2026-2033

Pneumatic Valves & Accessories Market Size and Trends Analysis

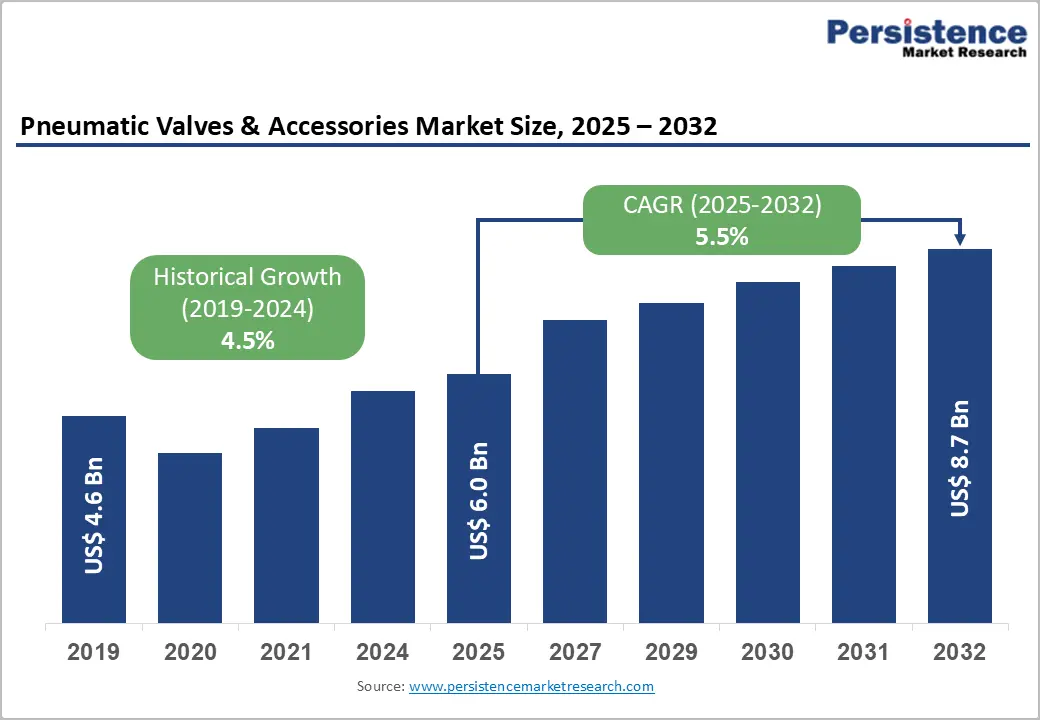

The global pneumatic valves & accessories market size is likely to be valued at US$6.0 billion in 2026 and is expected to reach US$8.7 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033, driven by the accelerating adoption of industrial automation across manufacturing and process industries, where pneumatic systems are widely used for reliable, precise, and cost-effective control of flow, pressure, and actuation.

Advances in valve design, such as modular configurations, smart monitoring, and energy-efficient operation, are improving performance and reliability. The increasing penetration of Industry 4.0, coupled with rising investments in digitalization, predictive maintenance, and sustainability initiatives, is reshaping demand patterns.

Key Industry Highlights:

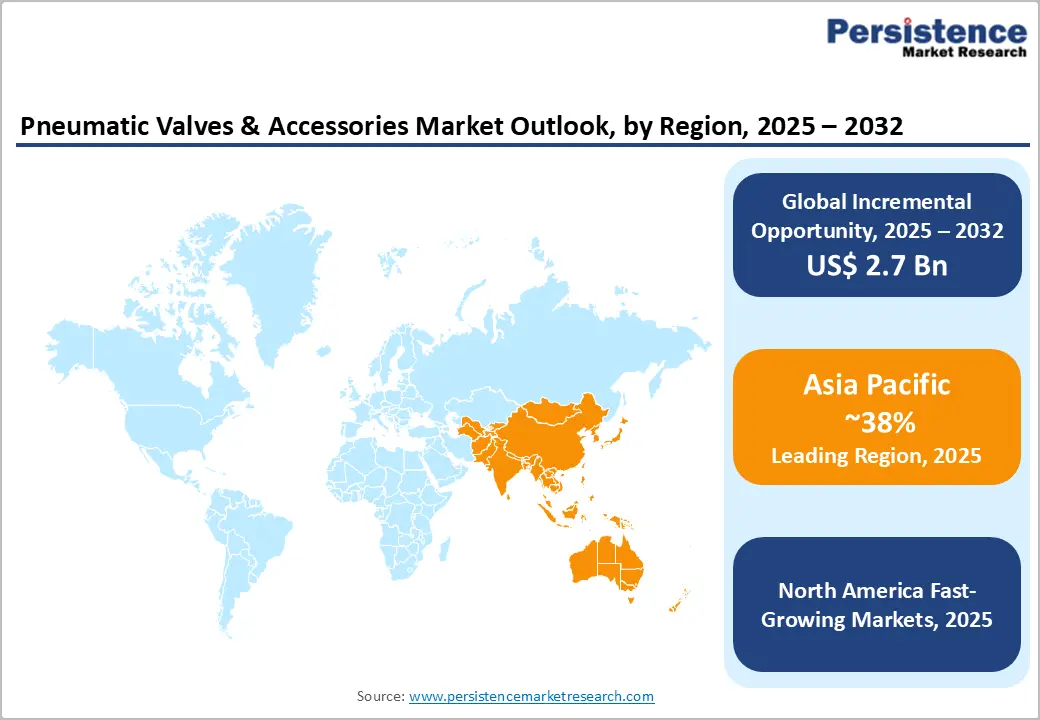

- Leading Region: Asia Pacific leads the market with around 38% share in 2025, driven by rapid industrialization, infrastructure spending, and investment in energy, electronics, and municipal services.

- Fastest-growing Region: North America is the fastest-growing region, driven by its advanced manufacturing, strong process industries, energy-efficiency regulations, active R&D, and trends toward market consolidation and next-generation pneumatic accessory adoption.

- Leading Product Type: Sliding shaft valves lead the product type segment with 55% share, due to their versatility, reliability, and ease of integration.

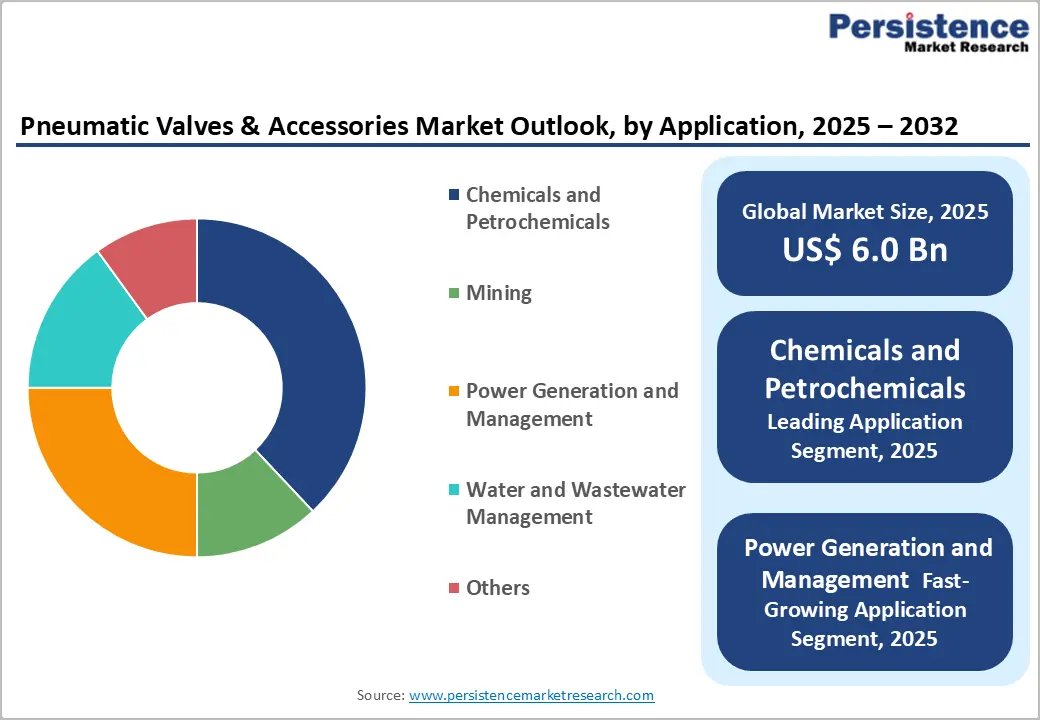

- Leading Application Type: Chemicals and petrochemicals are the leading segment in the market with about 35% share, due to heavy reliance on pneumatic flow control in continuous process operations.

| Key Insights | Details |

|---|---|

| Pneumatic Valves & Accessories Market Size (2026E) | US$6.0 Bn |

| Market Value Forecast (2033F) | US$8.7 Bn |

| Projected Growth CAGR (2026-2033) | 5.5% |

| Historical Market Growth (2020-2025) | 4.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Proliferation of Industrial Automation

Industries are increasingly adopting automated production systems to enhance efficiency, improve product quality, and reduce human intervention. Pneumatic valves are widely used in automated environments for controlling air flow, pressure, and actuation in machinery, robotics, material handling systems, and assembly lines. Their ability to deliver fast, precise, and repeatable motion makes them highly suitable for continuous and high-speed operations. Pneumatic systems are valued for their durability, safety, and ease of maintenance, which supports their widespread use across manufacturing, chemicals, power generation, food processing, and utilities.

Automation is also influencing innovation within the pneumatic valves market. Manufacturers are developing compact, modular, and retrofit-friendly valve designs that integrate seamlessly into automated production lines. The demand for smart pneumatic valves with built-in sensors, diagnostics, and connectivity is rising, enabling real-time monitoring and predictive maintenance. These features help reduce downtime, optimize energy usage, and extend equipment life. As automation investments continue to expand globally, pneumatic valves and accessories remain essential components, supporting scalable, efficient, and intelligent industrial operations.

High Capital Outlay Requirements

Advanced pneumatic systems often require significant upfront investment, including costs for high-performance valves, actuators, control units, sensors, and system integration. Installation expenses and the need for compatible automation infrastructure can also further increase the overall project cost. These financial demands can be challenging, particularly for small and medium-sized enterprises, which may operate with limited budgets and prioritize short-term cost savings over long-term efficiency gains. Customization requirements for specific industrial processes elevate procurement costs. Integration with legacy systems often requires additional engineering and calibration efforts.

The high initial investment can slow the adoption of technologically advanced pneumatic solutions, especially in cost-sensitive industries and emerging regions. While pneumatic systems offer long-term benefits such as reliability, lower maintenance, and improved operational efficiency, the return on investment may not be immediately evident to all end users. Budget constraints often lead industries to delay upgrades or opt for basic valve configurations. This limits the penetration of smart and energy-efficient pneumatic accessories.

Smart Technology Integration

Industries increasingly adopt digitalized and automated operations. Modern pneumatic valves are being equipped with embedded sensors, communication modules, and control intelligence that enable real-time monitoring of pressure, flow, temperature, and valve position. These capabilities improve process visibility and allow operators to detect performance deviations early, enhancing system reliability and operational control across industrial environments. Such smart pneumatic solutions support seamless integration with plant-wide automation and control systems. They also enable faster response times and more consistent performance in demanding industrial applications.

The integration of smart pneumatic solutions also supports predictive maintenance and energy optimization initiatives. By continuously monitoring system conditions, smart valves help identify air leaks, pressure losses, and inefficient operating cycles, reducing unplanned downtime and maintenance costs. Seamless connectivity with industrial control systems enables remote diagnostics and faster decision-making, which is particularly valuable in large-scale or distributed facilities. As industries prioritize efficiency, uptime, and sustainability, the adoption of intelligent pneumatic valves and accessories is expected to accelerate, creating strong opportunities for manufacturers offering advanced, connected solutions.

Category-wise Analysis

Product Type Insights

Sliding-shaft pneumatic valves and accessories dominate the market, accounting for approximately 55% of revenue in 2025. Their strong adoption is driven by high versatility, dependable performance, and seamless integration across a wide range of industrial systems, particularly within process industries. Modular construction and retrofit-friendly designs enable OEMs and end users to expand, upgrade, and maintain systems efficiently, making sliding-shaft solutions well-suited for both new installations and modernization projects. These valves are widely used in chemical processing for precise linear flow control and in water and wastewater treatment for regulating inlet and outlet flows. They are also extensively deployed in food and beverage production, where hygienic design, repeatable actuation, and consistent performance are critical.

Rotating-shaft pneumatic valves and accessories represent the fastest-growing product segment, supported by advances in rotary actuator technology and increasing adoption in high-duty-cycle applications. Industries such as power generation and mining are driving demand due to the segment’s superior durability, high-torque capability, and operational flexibility under demanding conditions. Rotating-shaft valves deliver accurate rotary control and are engineered to withstand cyclical stress, making them ideal for long-life applications. In power plants, they are commonly used in turbine control and fuel-handling systems, while in mining operations, they play a vital role in slurry transport and bulk material flow control in harsh operating environments.

Application Type Insights

The chemicals and petrochemicals segment leads, accounting for 35% revenue share in 2025, driven by the sector’s reliance on pneumatic flow control for safe, continuous, and precise process operations. Ongoing modernization of refineries, expansion of specialty chemical facilities, and the need for strict process safety measures have further strengthened demand. Pneumatic valves control flow, pressure, and actuation, providing reliable, efficient, and easy-to-maintain operation for high-precision processes. For example, they are extensively applied in batch processing systems and hazardous material handling units where fail-safe operation is critical. They are also preferred in corrosive and high-temperature environments due to their durability and operational stability.

The power generation and management segment represents the fastest-growing application area, supported by investments in smart grids, renewable energy integration, and the modernization of thermal and hydroelectric plants. Pneumatic valves play a vital role in the automated control of turbines, boiler feed systems, and cooling circuits. In renewable power facilities, they are used in auxiliary control systems for consistent performance. In mining, water, and wastewater management, pneumatic solutions are increasingly adopted for slurry handling, flow regulation, and treatment processes, driven by infrastructure upgrades, sustainability initiatives, and tightening regulations.

Regional Insights

North America Pneumatic Valves & Accessories Market Trends

North America is emerging as the fastest-growing region in the pneumatic valves & accessories market, driven by a combination of industrial modernization, automation adoption, and investment in smart manufacturing technologies. The U.S. leads the market, supported by a well-established industrial base, widespread adoption of automation, and a focus on energy-efficient operations. Pneumatic valves are widely used in chemicals, food and beverage, pharmaceuticals, and power generation for precise flow and pressure control. For example, Emerson Electric has expanded its portfolio of advanced pneumatic valves and automation solutions to support U.S. manufacturers seeking higher efficiency and reliability in process operations.

Innovation in smart pneumatic technology is another major trend. Valves and accessories equipped with sensors, real-time monitoring, and connectivity features are being adopted to enable predictive maintenance, reduce downtime, and optimize energy usage. The market is also witnessing increased interest in low-leakage valves and compact designs to improve operational efficiency and reduce compressed air losses. Manufacturers are focusing on digital integration and intelligent system controls, aligning pneumatic valve operations with Industry 4.0 standards.

Europe Pneumatic Valves & Accessories Market Trends

Europe remains a significant market for pneumatic valves & accessories, due to its well-established industrial base and strong focus on automation and precision manufacturing. The region, led by countries such as Germany, France, and Italy, is witnessing increased adoption of smart pneumatic systems featuring IoT-enabled valves, real-time diagnostics, and predictive maintenance capabilities. Manufacturers are favoring modular and retrofit-ready designs to upgrade existing production lines while maintaining operational efficiency and minimizing downtime. For example, Festo continues to expand its smart pneumatic solutions across European manufacturing plants, supporting flexible automation and digitally connected production environments.

Energy efficiency and regulatory compliance are also key drivers in Europe. Companies are prioritizing low-leakage valves, eco-friendly designs, and optimized air-preparation systems to reduce compressed-air losses and operational costs. Green initiatives and carbon-neutral targets are encouraging the integration of sustainable pneumatic solutions across sectors such as automotive, pharmaceuticals, food and beverage, and packaging.

Asia Pacific Pneumatic Valves & Accessories Market Trends

Asia Pacific is the leading region in the pneumatic valves & accessories market, driven by rapid industrialization, automation adoption, and strong manufacturing activity in countries such as China, India, Japan, and the ASEAN bloc. The region benefits from cost advantages, a robust OEM base, and large-scale industrial infrastructure, which support both local production and export-oriented growth. Key industries rely on pneumatic systems for precise automated control, boosting the region’s market lead. For example, SMC Corporation continues to strengthen its pneumatic valve manufacturing and automation solutions across Asia to meet rising demand from high-volume production facilities.

Smart pneumatic technologies represent a major trend in the region. Valves equipped with embedded sensors, IoT connectivity, and real-time diagnostics are being widely adopted to support predictive maintenance, minimize downtime, and improve energy efficiency. Sustainability initiatives are further shaping demand, with low-leakage valves and energy-efficient air-preparation systems gaining traction to reduce compressed-air losses and operating costs. Rapid infrastructure development in emerging economies is also driving the adoption of automated pneumatic solutions in water treatment, power generation, and mining applications.

Competitive Landscape

The global pneumatic valves & accessories market exhibits a moderately fragmented structure, driven by the presence of numerous regional and international manufacturers catering to diverse industrial applications. Companies are focused on offering innovative, high-quality, and energy-efficient pneumatic solutions to meet the growing demand for automation, smart manufacturing, and Industry?4.0 integration.

With key leaders including SMC Corporation, Festo SE & Co.?KG, Parker Hannifin Corporation, Emerson Electric Co., Bosch Rexroth, Camozzi Automation, and Norgren (IMI Precision Engineering), the market is characterized by a competitive push toward smart and energy-efficient pneumatic technologies. These players compete through continuous product innovation, development of digitalized and connected pneumatic solutions, expansion of manufacturing capacities, and enhanced after-sales service.

Key Industry Developments:

- In July 2024, Emerson launched its AVENTICS Series XV pneumatic valves, designed to enhance production efficiency with a compact, flexible, and high-performance platform. The XV03 model handles flow volumes up to 350?L/min, while the upcoming XV05 is set to deliver up to 880?L/min. Built with durable metal threads and aluminum base plates, these valves support popular fieldbus protocols, including Profinet, Ethernet/IP, and EtherCAT, enabling seamless integration and easy commissioning into existing automation systems.

- In November 2024, KI launched the Tank Bottom Ball Valve, designed for general-purpose tanks and vessels handling slurries and powders. It features an ISO?5211 mounting pad for direct actuator installation, an angle stem for insulated tanks, and a fire-resistant, anti-static design, and was showcased at Valve World 2024 in Düsseldorf, Germany.

Frequently Asked Questions

The global pneumatic valves & accessories market is valued at US$6.0 billion in 2026 and expected to reach US$8.7 billion by 2033, reflecting robust growth.

Major demand drivers include the proliferation of the industrial automation Industry, regulatory mandates for energy efficiency, and ongoing expansion in primary process industries.

In the application category of the pneumatic valves & accessories market, the chemicals and petrochemicals segment is the leading contributor, accounting for 35% of revenue in 2025, driven by its extensive use of pneumatic flow control in continuous process operations.

Asia Pacific leads the market with around 38% revenue share, driven by rapid industrialization, infrastructure spending, and investment in energy, electronics, and municipal services.

A key opportunity lies in deploying smart, IoT-ready pneumatic valves, especially in water/wastewater management and emerging markets pursuing rapid urbanization.