- Medical Devices

- Pneumatic Compression Therapy Market

Pneumatic Compression Therapy Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Pneumatic Compression Therapy market by Product Type (Pneumatic Compression Sleeves, Segmented Pneumatic Compression Pumps, Programmable Pneumatic Compression Pumps, Non-Programmable Pneumatic Compression Pumps, Non-Segmented Pneumatic Compression Pumps), Distribution Channel, Regional Analysis, from 2026 - 2033

Pneumatic Compression Therapy Market Share and Trends Analysis

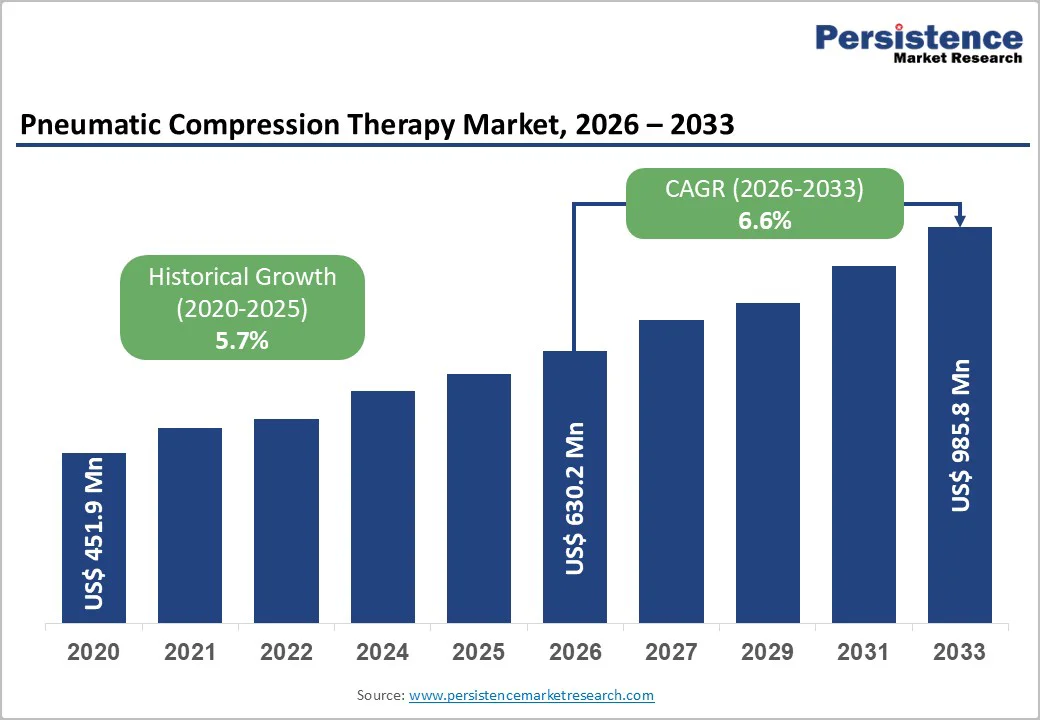

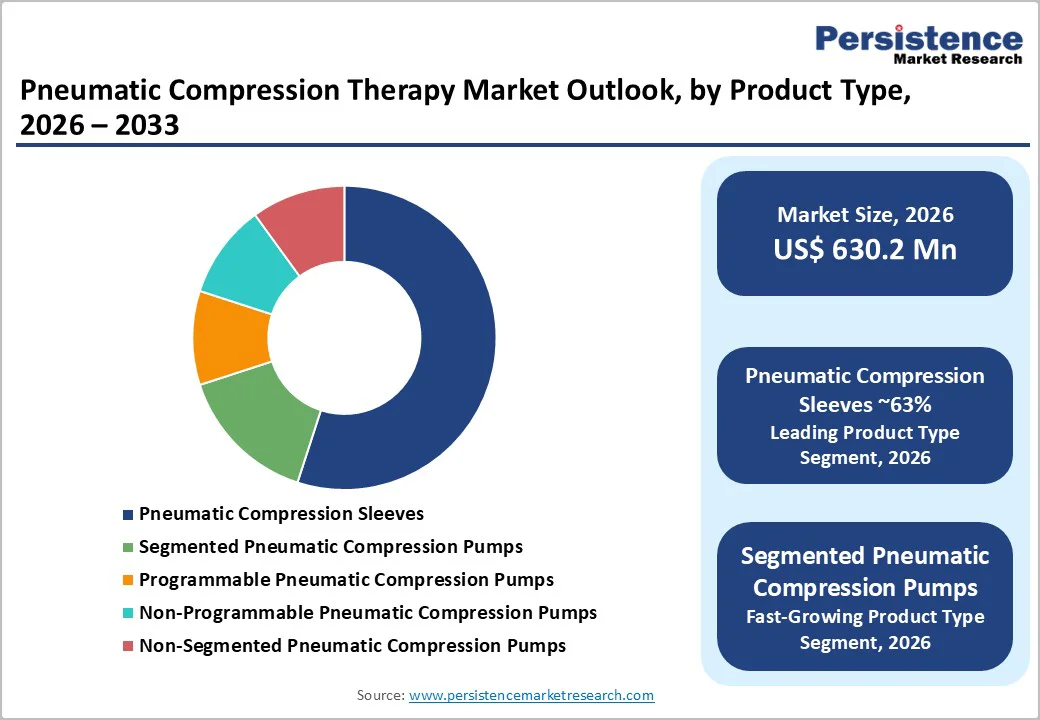

The global pneumatic compression therapy market size is estimated to be valued from US$ 630.2 million in 2026 to US$ 985.8 million by 2033, growing at a CAGR of 6.6% during the forecast period from 2026 to 2033. The global market is expanding due to the growing prevalence of lymphedema, chronic venous insufficiency, and deep vein thrombosis, as well as the rising acceptance of non-invasive therapeutic systems in hospitals and home care settings.

Increasing clinical evidence supporting intermittent pneumatic compression to improve lymphatic flow and wound healing has enhanced access to reimbursement in key regions. Additionally, aging demographics, obesity, and patients’ preference for portable home-use devices are accelerating demand for programmable and segmented pumps. These technologically advanced systems improve treatment adherence, reduce complications, and support preventive care, thereby positioning pneumatic compression therapy as a critical modality in vascular and lymphatic management.

Key Industry Highlights:

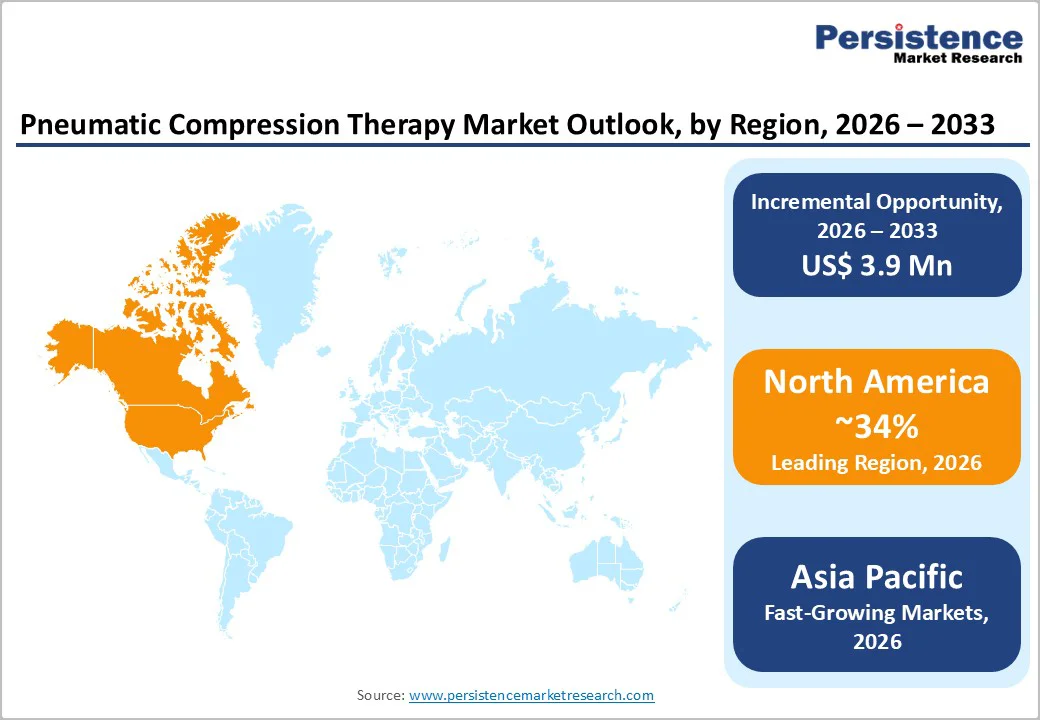

- Leading Region: North America is expected to lead the market in 2025, supported by well-established healthcare infrastructure, high awareness of venous and lymphatic disorders, and strong reimbursement frameworks.

- Fastest Growing Region: Asia Pacific is projected to be the fastest-growing market, driven by increasing prevalence of lymphedema and DVT, rising geriatric population, and expanding adoption of home-based healthcare solutions.

- Dominant Segment: Pneumatic compression sleeves are the leading segment, accounting for the largest market share due to versatility, ease of use, and clinical effectiveness in lymphedema, chronic venous insufficiency, and post-operative DVT management.

- Key Distribution Channel: Hospitals remain the primary channel, contributing the largest share, while outpatient clinics and e-commerce platforms are gaining importance for home-based therapy and follow-up care.

| Key Insights | Details |

|---|---|

|

Pneumatic Compression Therapy Market Size (2026E) |

US$ 630.2 Mn |

|

Market Value Forecast (2033F) |

US$ 985.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.7% |

Market Dynamics

Driver - Rising Technological Innovation, Portability Demand, and Online Accessibility Drive Pneumatic Compression Therapy Market Growth

The global pneumatic compression therapy market is strongly driven by rising adoption of advanced medical textiles, growing emphasis on post-operative recovery, and the increasing prevalence of venous disorders and lymphedema. The integration of innovative textile technologies, supported by developments in nanotechnology, has enabled manufacturers to design durable, ergonomic, and more efficient compression sleeves and cuffs. Military and sports applications have played an important role in experimental development, enabling rapid progress in textile engineering towards lighter, more flexible, and higher-performance materials. With increasing demand for products that offer enhanced functionality, durability, and comfort, pneumatic compression systems are evolving into portable, patient-friendly formats, thereby supporting greater adoption of home-based therapy and reducing healthcare costs. These innovations enable patients to independently manage edema and post-surgical swelling, reducing hospital visits and improving treatment adherence.

Additionally, advancements in electronics and device miniaturization have significantly contributed to innovation. Manufacturers are introducing compact products with better usability and patient compliance. For example, portable systems such as Venapro and Venowave support post-operative DVT prevention while enabling mobility during recovery. Another key driver is the accelerating shift toward online distribution channels. Online platforms provide wider product availability and competitive pricing, making pneumatic compression devices more accessible to patients and caregivers. The resulting convenience has strengthened end-user purchasing power and expanded market penetration across emerging regions.

Restraints - High Device Cost and Reimbursement Variability

The high cost of advanced segmented and programmable compression devices constrains the growth of the global pneumatic compression therapy market. These systems, while clinically effective, require significant upfront investment, making them less accessible in resource-limited regions. Even in developed markets, reimbursement coverage can be restrictive, often necessitating proof of prior conservative treatment failure or advanced disease stages. Such requirements delay patient access and reduce early adoption of these devices. In emerging economies, low insurance penetration and predominantly out-of-pocket payment models further limit affordability, forcing patients to rely on lower-cost static compression solutions.

Despite the proven efficacy of pneumatic compression in improving venous return, managing lymphedema, and preventing post-operative DVT, these economic barriers contribute to underutilization. Consequently, market expansion is tempered, as manufacturers must balance the development of technologically advanced devices with pricing strategies that consider both affordability and regional reimbursement policies.

Opportunity - Opportunity from Lightweight, Wearable, and Programmable Pneumatic Compression Devices

The development of lightweight, wearable, and programmable pneumatic compression devices represents a significant growth opportunity for the global market. Traditional compression systems were often bulky, restricting patient mobility and limiting usage primarily to clinical settings. Innovations in material science, electronics, and textile engineering have enabled manufacturers to design devices that are compact, flexible, and ergonomically optimized for long-term wear. These improvements make it easier for patients to use devices consistently, increasing adherence to prescribed therapy schedules, which is critical for effective management of conditions such as lymphedema, chronic venous insufficiency, and postoperative DVT.

Programmable systems allow personalized therapy by adjusting pressure, duration, and sequential compression patterns according to individual patient needs. This feature not only improves treatment outcomes but also enhances patient comfort and convenience, encouraging wider adoption. Additionally, wearable devices support home-based care, reducing the need for frequent hospital visits and lowering overall healthcare costs. With the global trend toward preventive care and self-management of chronic conditions, these advanced, patient-centric devices address both clinical and lifestyle requirements. As a result, the market has the opportunity to expand rapidly, especially in regions with aging populations, rising chronic disease prevalence, and increasing awareness of non-invasive therapeutic options.

Category-wise Analysis

By Product Type Insights

Pneumatic compression sleeves are projected to dominate the global market, accounting for approximately 53% of the market share in 2025. Their widespread use is attributed to their versatility across clinical conditions, including lymphedema, chronic venous insufficiency, and DVT prevention. Sleeves serve as the primary interface for both basic and advanced programmable pumps, providing coverage of the lower and upper limbs and, occasionally, the trunk. Their standardized sizing, ease of application, and relatively low replacement cost make them appealing for hospitals, outpatient clinics, and home-care settings. Clinical studies support their effectiveness in enhancing venous return and promoting lymphatic drainage when used alongside exercise or compression garments. The combination of clinical reliability, patient comfort, and adaptability across treatment areas ensures that pneumatic compression sleeves remain the preferred choice for healthcare providers, driving continued market growth and adoption in both institutional and home-based care.

By Drug Class Insights

Hospitals are expected to account for the highest share of the global pneumatic compression therapy market in 2025, reflecting their central role in acute care and peri-operative management. Intermittent pneumatic compression systems are routinely employed in surgical wards, intensive care units, and oncology departments to prevent thromboembolic events and manage post-operative edema. Hospitals benefit from established clinical protocols and guideline recommendations, making them the primary decision-makers for device procurement and brand preference, which, in turn, influences adoption in clinics and home settings.

The expansion of enhanced recovery after surgery (ERAS) programs and stricter venous thromboembolism (VTE) prevention protocols further solidifies hospitals as the dominant distribution channel. While outpatient clinics and e-commerce platforms are growing in importance for follow-up care and home-based therapy, hospitals remain the key driver of market penetration and early-stage adoption of pneumatic compression therapy systems.

Region-wise Insights

North America Pneumatic Compression Therapy Market Trends

North America, led by the U.S., represents the largest regional market, accounting for an estimated 34% share of global pneumatic compression therapy revenues in 2025. The region benefits from high awareness of venous thromboembolism and lymphedema, substantial healthcare expenditure, and strong presence of leading companies such as Tactile Medical, Medtronic, DJO Global, Inc., and Bio Compression Systems, Inc. Robust clinical evidence and detailed coverage policies from private payers, VA healthcare, and commercial insurers define clear criteria for prescribing pneumatic compression devices for lymphedema and venous leg ulcers, supporting consistent utilization in both hospital and home settings.

The innovation ecosystem in the U.S. further accelerates market development through advanced programmable and connected devices, exemplified by clinical studies on systems such as Flexitouch that demonstrate improved quality of life, high adherence, and significant limb girth reduction in veterans with lower extremity lymphedema. Growing emphasis on outpatient care, telehealth, and remote patient monitoring aligns well with data-enabled pneumatic compression solutions. At the same time, Canada’s and the U.S.’s aging populations and high obesity prevalence ensure a sustained pool of patients requiring long-term vascular and lymphatic management.

Asia Pacific Pneumatic Compression Therapy Market Trends

Asia Pacific is emerging as the fastest-growing market for pneumatic compression therapy, driven by demographic shifts, rising chronic disease prevalence, and ongoing healthcare infrastructure expansion in China, Japan, India, and ASEAN countries. The increasing incidence of cancer-related lymphedema, diabetes-related vascular complications, and venous insufficiency is creating a larger patient base that can benefit from non-invasive compression therapies. Governments and private providers are investing in specialty vascular and oncology centers, which in turn increases access to advanced compression modalities, including segmented and programmable pumps.

From a manufacturing standpoint, Asia Pacific enjoys significant cost advantages, with companies such as XIAMEN SENYANG CO., LTD and regional OEMs supplying pneumatic compression sleeves and pumps globally. Local production capabilities help reduce device prices and support broader penetration into public hospitals and private clinics, especially in India and Southeast Asia. At the same time, growing e-commerce penetration allows manufacturers to reach home-care users directly, which aligns with rising household incomes and expanding middle-class populations seeking convenient, non-invasive vascular care and recovery solutions.

Competitive Landscape

The global pneumatic compression therapy market is moderately fragmented, with a mix of multinational medical device manufacturers and specialized compression therapy companies competing across regions. Leading players such as Medtronic, Tactile Medical, ArjoHuntleigh (Getinge AB), Medline Industries, Inc., DJO Global, Inc., and Bio Compression Systems, Inc. focus on portfolio innovation, including programmable multi-chamber pumps, ergonomic sleeves, and home-care kits, while expanding geographically through distributor partnerships and direct sales networks. Key differentiators include clinical evidence, device programmability, ease of use, connectivity, service support, and payer engagement strategies, with some companies experimenting with rental, subscription, and telehealth-enabled business models to enhance affordability and adherence.

Key Industry Developments:

- In September 2024, Tactile Medical reported favorable clinical trial outcomes for lymphedema patients treated with their advanced pneumatic compression device.

Companies Covered in Pneumatic Compression Therapy Market

- Medtronic

- Tactile Medical

- ArjoHuntleigh (Getinge AB)

- Mego Afek ltd.

- Medline Industries, Inc.

- DJO Global, Inc.

- Bio Compression Systems, Inc.

- Talley Group Limited

- XIAMEN SENYANG CO., LTD

- Devon Medical Products

- EUREDUC

- Bösl Medizintechnik

- Others

Frequently Asked Questions

The global pneumatic compression therapy market is projected to be valued at US$ 630.2 Mn in 2026.

Rising lymphedema prevalence, post-surgical edema management, home-based compression devices adoption, and emphasis on venous disorder treatment.

The global market is poised to witness a CAGR of 6.6% between 2026 and 2033.

Untapped emerging markets, technology-enhanced wearable systems, post-cancer rehabilitation adoption, and expanding reimbursement support.

Major players include Medtronic, Tactile Medical, ArjoHuntleigh (Getinge AB), Mego Afek Ltd., Medline Industries, Inc., DJO Global, Inc., and Bio Compression Systems, Inc.