- Marine

- Pneumatic Fender Market

Pneumatic Fender Market Size, Share, and Growth Forecast, 2026 - 2033

Pneumatic Fender Market by Product Configuration (Tire-Chain Net, Sling Type, Rib Type/Mat Net), Technology Type (Standard ISO, Smart/IoT-Enabled), Sales Channel (OEM, Aftermarket), End-user Industry, and Regional Analysis 2026 - 2033

Pneumatic Fender Market Size and Trends Analysis

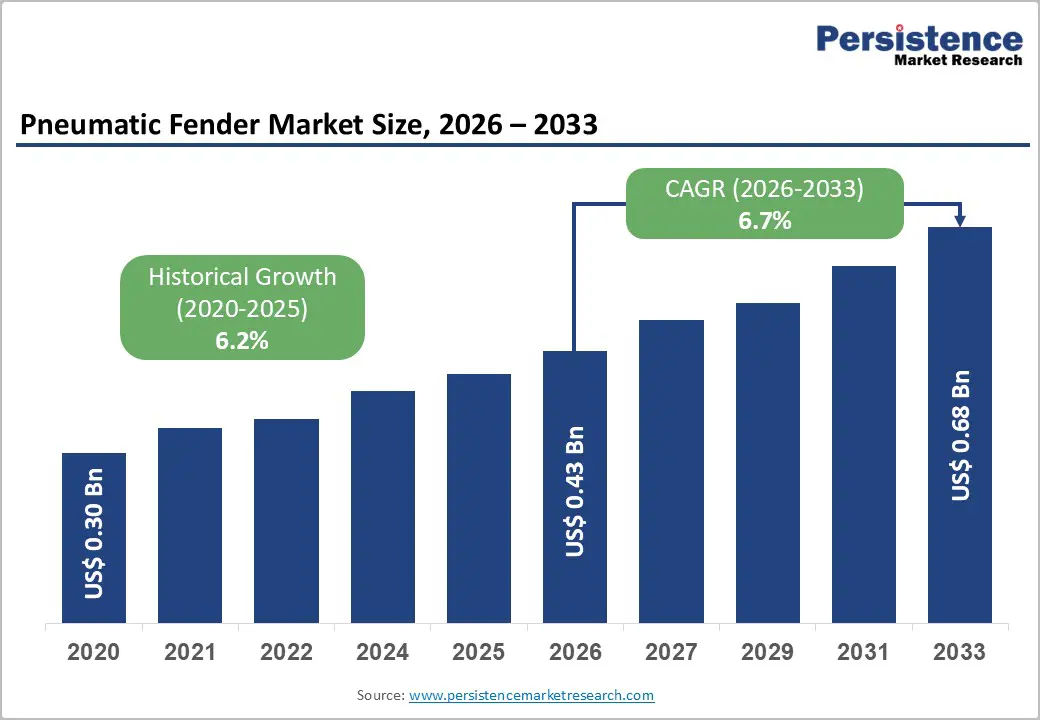

The global pneumatic fender market size is likely to be valued at US$0.43 billion in 2026 and is expected to reach US$0.68 billion by 2033, growing at a CAGR of 6.7% during the forecast period from 2026 to 2033, driven by the escalating volume of seaborne trade and the resultant expansion of deep-water port infrastructures worldwide.

The transition toward large-scale vessels, such as Ultra Large Container Vessels (ULCVs) and LNG carriers, necessitates advanced energy-absorption solutions to ensure berthing safety. The integration of IoT-enabled monitoring systems and a stringent regulatory focus on ISO standards further catalyze market modernization and replacement demand across the shipping and energy sectors.

Key Industry Highlights:

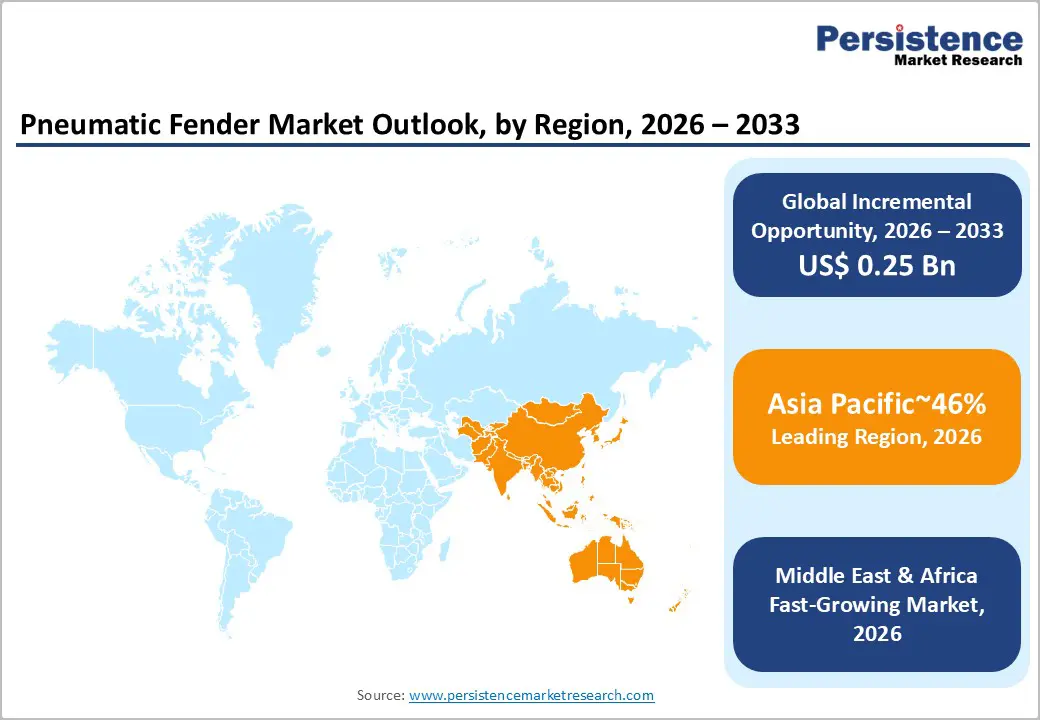

- Leading Region: Asia Pacific is projected to lead due to deep shipbuilding concentration and dense port infrastructure expansion, accounting for approximately 46% share in 2026, driven by technology adoption in sensor-enabled fenders and integrated marine supply ecosystems, which strengthen regional scale advantages.

- Fastest Growing Region: The Middle East & Africa is anticipated to grow the fastest due to accelerated port construction, logistics corridor diversification, and state-backed maritime infrastructure programs. Key countries across GCC jurisdictions are expected to drive adoption through large-scale terminal investments, energy export expansion, and automated berth infrastructure initiatives supporting ISO-compliant pneumatic systems.

- Leading Product Configuration: Tire-chain Net is expected to lead in accounting, with an estimated 64% share in 2026, driven by entrenched deployment in high-impact berthing, superior abrasion resistance, and lifecycle durability across shipping and offshore applications.

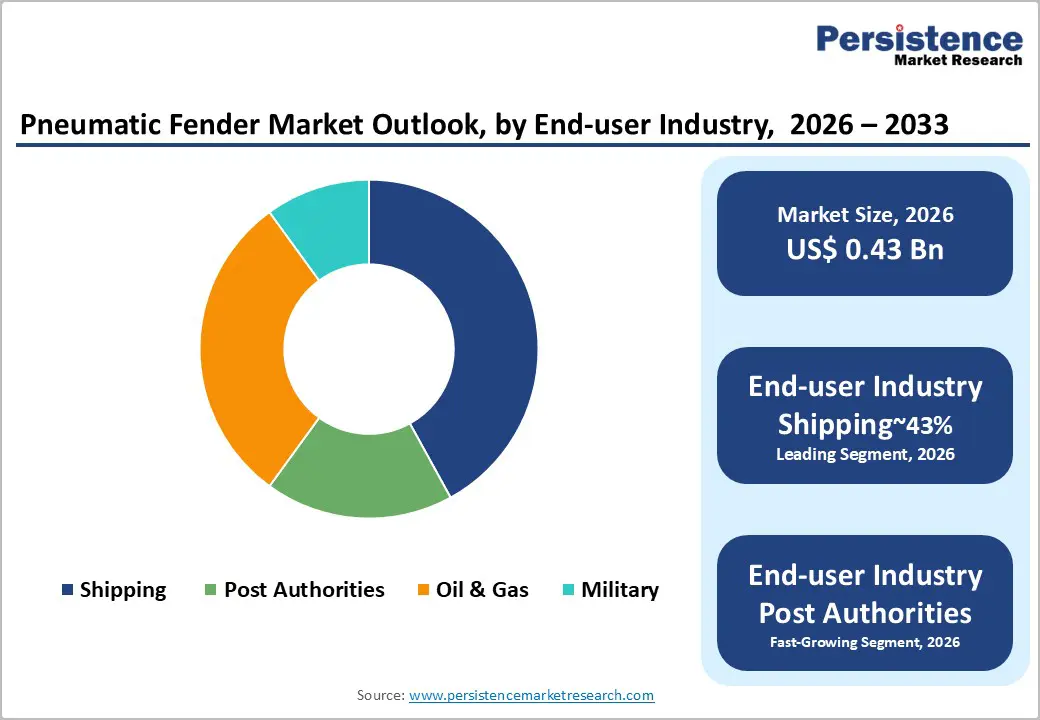

- Leading End-user Industry: The shipping industry is projected to dominate due to high berthing frequency, cost-efficiency priorities, and suitability across bulk carriers and tanker fleets, with approximately 42% share in 2026.

| Key Insights | Details |

|---|---|

|

Pneumatic Fender Market Size (2026E) |

US$0.43 Bn |

|

Market Value Forecast (2033F) |

US$0.68 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Surge in LNG and Bulk Carrier Vessel Sizes

The progressive enlargement of LNG carriers and bulk transport vessels intensifies berthing impact dynamics. Larger hull geometries displace greater mass, amplifying kinetic energy during docking maneuvers. Terminal infrastructure, therefore, confronts elevated reaction forces and structural loading thresholds. Conventional fendering systems demonstrate reduced efficacy under high-energy vessel interactions. Pneumatic fenders with superior absorption capacity mitigate concentrated hull stress concentrations. This requirement becomes critical within LNG transfer terminals operating under stringent safety regimes. Cryogenic cargo operations impose a zero-tolerance policy for structural compromise or impact-induced deformation. Consequently, demand for engineered floating systems calibrated for extreme energy dissipation strengthens.

Port authorities and energy terminals recalibrate procurement specifications to address vessel scale escalation. High-capacity pneumatic configurations capable of absorbing up to 1,000 kJ/m gain preference. Enhanced internal pressure control and reinforced rubber cord layers improve performance reliability. Compliance with maritime safety conventions further institutionalizes adoption across regulated terminals. Insurance underwriting increasingly factors berthing risk mitigation into premium calculations. Lifecycle economics favor advanced fenders that reduce maintenance frequency and dock repair expenditure. Supply chains consequently shift toward specialized elastomer compounds and precision fabrication standards. These structural dynamics collectively reinforce sustained demand within LNG and bulk logistics corridors.

Expansion of Global Seaborne Trade and Fleet Modernization

The sustained expansion of international maritime trade structurally elevates demand for high-capacity pneumatic fender systems. Seaborne logistics continues to dominate global merchandise movement, reinforcing port throughput intensity. Merchant fleets are increasingly transitioning toward larger vessel classes to capture scale efficiencies. These vessels generate elevated berthing energy, intensifying impact loads during docking operations. Conventional fixed fender systems face structural limitations under higher displacement and kinetic forces. Consequently, port operators prioritize floating pneumatic configurations with superior energy absorption characteristics. This transition reshapes procurement standards toward performance-certified systems capable of mitigating hull stress. Regulatory compliance and insurance risk frameworks further institutionalize demand for advanced berthing protection technologies.

Fleet modernization simultaneously compels infrastructure retrofitting across established and emerging maritime hubs. Accommodation of new-generation vessels necessitates engineered fender solutions with enhanced resilience. Ports handling New Panamax categories require significantly greater impact dissipation capabilities. Failure to upgrade protection systems increases asset deterioration and lifecycle maintenance expenditure. High-performance pneumatic fenders reduce reaction forces while preserving quay wall integrity. Advances in material engineering of reinforced rubber composites improve durability under cyclical loading. Capital allocation increasingly favors modular, relocatable fender assets supporting flexible berth utilization. These structural shifts collectively reinforce sustained demand across global port infrastructure ecosystems.

Barrier Analysis - Maintenance Complexity and Technical Expertise Constraints

The growing technical sophistication of pneumatic fender systems introduces specialized maintenance requirements across global ports. Advanced configurations increasingly incorporate sensor-enabled pressure monitoring and smart valve assemblies. These integrated systems demand trained personnel capable of precision inspection and component servicing. However, maritime infrastructure markets face a structural shortage of certified technical labor. Skin replacement procedures require controlled deflation protocols and reinforced bonding expertise. Improper handling risks performance degradation and compromised energy absorption efficiency. Limited availability of skilled technicians extends maintenance cycles and increases operational downtime. This skills gap constrains optimal lifecycle utilization of high-performance pneumatic fender assets.

Maintenance complexity also reshapes cost structures across the aftermarket service ecosystem. Port operators must allocate higher budgets for specialist contractors and technical training programs. Spare component logistics for smart valves and reinforced outer skins introduce supply chain coordination challenges. Regulatory safety audits intensify documentation requirements for verifying maintenance compliance. Delays in certified servicing elevate risk exposure during high-energy berthing operations. Insurance and liability frameworks increasingly scrutinize maintenance records for impact mitigation systems. Smaller ports with limited technical infrastructure experience disproportionate operational strain. These structural labor and capability gaps collectively moderate the adoption velocity of technologically advanced pneumatic fender platforms.

Environmental Compliance and End-of-Life Disposal Constraints

The production of large-scale rubber pneumatic fenders attracts increasing environmental regulatory scrutiny. Manufacturing processes involve elastomer compounding, carbon black integration, and vulcanization emissions. Environmental compliance frameworks impose tighter controls on industrial discharge and air pollutants. These requirements elevate input costs across raw material sourcing and processing stages. Carbon accountability expectations increasingly influence procurement decisions within port authorities. Lifecycle assessments now extend beyond operational performance toward embedded environmental impact. Limited recycling pathways for reinforced rubber composites complicate circularity objectives. Environmental governance pressures also reshape manufacturing and supply chain strategies.

End-of-life disposal presents structural challenges due to material complexity and scale. Pneumatic fenders incorporate multilayer cord reinforcements bonded to durable rubber skins. Separation and recovery of composite materials remain technologically constrained and economically inefficient. Inadequate recycling infrastructure across maritime regions increases reliance on landfill or incineration. Disposal liabilities introduce long-term cost considerations for port operators and asset owners. Regulatory tightening on industrial waste management further heightens compliance burdens. Sustainability reporting standards increasingly require disclosure of disposal methodologies and environmental footprint. These combined pressures moderate margin flexibility and influence procurement toward environmentally optimized alternatives.

Opportunity Analysis – Integration of Smart Sensor Technologies within Pneumatic Fender Systems

The embedding of IoT-enabled sensors in pneumatic fenders is transforming performance-monitoring frameworks. Real-time measurement of internal pressure and impact energy enhances operational visibility during berthing events. These data streams enable port authorities to detect performance deviations before structural degradation occurs. Integration with centralized monitoring platforms strengthens asset management across multi-berth terminals. Artificial intelligence analytics further interpret load patterns and cyclical stress exposure. This technological evolution shifts fender systems from passive protection devices to intelligent infrastructure components. Enhanced diagnostic capability reduces unplanned downtime and optimizes maintenance scheduling efficiency. Consequently, digital integration strengthens reliability within high-traffic maritime logistics corridors.

Predictive maintenance capabilities materially influence lifecycle cost structures and operational continuity. Early fault detection reduces the risk of catastrophic failure during high-energy docking operations. Reduction in unexpected servicing requirements improves berth availability and throughput consistency. Data-driven maintenance planning enhances budget forecasting and resource allocation discipline. Regulatory compliance documentation becomes more structured through automated performance logging systems. Integration with broader port digitalization initiatives supports coordinated infrastructure management. Specialized electronics and sensor integration introduce higher upfront capital intensity. However, operational efficiency gains and reduced exposure to downtime create a structural justification for technology adoption across advanced port ecosystems.

Adoption of Sustainable Materials Supporting Offshore and Port Infrastructure Expansion

The transition toward sustainable composite materials is reshaping pneumatic fender manufacturing strategies. Offshore oil and gas operators account for a meaningful share of end-user demand. Decarbonization agendas aligned with international energy transition frameworks reinforce material substitution priorities. Recyclable PVC and rubber hybrid formulations reduce lifecycle emissions relative to conventional compounds. These alternatives mitigate exposure to carbon border adjustment mechanisms within regulated trade corridors. Environmental compliance pressures, therefore, influence procurement specifications across energy terminals. Material innovation also supports alignment with corporate sustainability disclosure requirements. Consequently, eco-engineered fenders gain institutional acceptance within environmentally scrutinized offshore infrastructure projects.

Port authorities, representing a fast-expanding demand cluster, increasingly integrate sustainable fender systems. Smart port development frameworks prioritize environmentally compatible infrastructure components. Recyclable composite adoption supports emissions accounting and circularity reporting obligations. Premium pricing potential reflects added compliance value and differentiated environmental performance. Manufacturers adjust their supply chains toward sourcing certified low-emission raw materials. Regulatory alignment across European trade regimes strengthens demand visibility for compliant products. Integration with digital monitoring systems further enhances sustainability traceability metrics. These converging dynamics structurally expand the opportunity for eco-optimized pneumatic fender platforms.

Category–wise Analysis

Product Configuration Insights

Tire-chain net is expected to lead, accounting for approximately 64% share in 2026, underpinned by entrenched deployment across high-impact berthing and ship-to-ship transfers. Its outer lattice of tires and galvanized chains shields the fender body from abrasion and sharp hull projections, materially extending service life under repetitive loading. Ports and terminal operators prioritize durability and total ownership efficiency in heavy-frequency environments, reinforcing standardization around chain-net configurations. Yokohama Rubber Company, Trelleborg AB, Shibata Fender Team, Palfinger Marine, and IRM Offshore and Marine Engineers anchor enterprise workflows with high-spec, ISO-aligned portfolios. Proven reliability in shipping-intensive settings and balanced cost–performance characteristics sustain replacement cycles and utilization intensity.

Sling type is expected to be the fastest-growing segment, driven by mobility requirements and rapid deployment needs across offshore and temporary installations. Its simplified construction eliminates the heavy chain-tire net, reducing mass and enabling quicker handling during emergency response and short-notice operations. Offshore oil and gas and naval users value portability for dynamic positioning and variable berth geometries. Palfinger Marine, Trelleborg AB, Yokohama Rubber Company, FenderCare Marine, and Floating Fender Co. expand smooth-skin and high-pressure lines to capture early-cycle demand. Operational flexibility, lower handling complexity, and compatibility with sensitive hull coatings accelerate adoption across cruise, commercial, and specialized marine corridors.

End-user Industry Insights

The shipping industry is estimated to lead, accounting for approximately 42% share in 2026, anchored by sustained global vessel traffic and recurring berthing protection requirements. The structural dependence of bulk carriers and tankers on pneumatic systems secures predictable replacement demand across high-frequency ship-to-ship operations. Operators prioritize abrasion-resistant, ISO-aligned configurations to mitigate hull stress and docking risk. Yokohama Rubber Company and Trelleborg AB reinforce dominance through heavy-duty synthetic rubber portfolios and sensor-enabled platforms. Henger Shipping Supply, FenderCare Marine, and JIER Marine Fenders support lifecycle services and environmental design enhancements. High-volume cargo corridors and standardized fleet specifications sustain utilization intensity and cost-efficient procurement cycles.

Port authorities are expected to be the fastest-growing segment, driven by accelerating smart port integration and terminal automation initiatives. As container vessels scale in size, ports modernize fixed and floating systems with embedded monitoring capabilities. Intelligent fender platforms equipped with IoT sensors enhance predictive maintenance and asset visibility. Trelleborg Marine and Infrastructure advances SmartFender solutions aligned with automated berth management frameworks. Yokohama Rubber Company and ShibataFenderTeam expand custom-engineered installations across Asia Pacific and Europe. Henger Shipping Supply and Palfinger AG strengthen durability-focused portfolios for commercial terminals. Infrastructure digitization and automation-linked procurement accelerate adoption beyond conventional maritime protection models.

Regional Insights

Asia Pacific Pneumatic Fender Market Trends

Asia Pacific is anticipated to remain the dominant regional market, accounting for approximately 46% share in 2026, supported by deep shipbuilding concentration, dense port infrastructure expansion, and integrated marine supply ecosystems. The region is positioned to anchor both demand and production, as high vessel throughput and expanding offshore logistics corridors reinforce continuous replacement and capacity augmentation cycles. Manufacturing scale in China, South Korea, and Japan is anticipated to sustain cost-efficient fabrication of rubber composites, chain assemblies, and high-pressure fender systems. Technology adoption is likely to advance through sensor-enabled monitoring integration within major container terminals and energy transfer hubs. Regulatory alignment with international maritime safety standards is expected to reinforce specification uniformity across commercial and naval procurement frameworks. This ecosystem depth is projected to preserve Asia Pacific’s structural leadership within the global maritime protection infrastructure.

The Middle East & Africa is expected to register the fastest growth trajectory, as state-backed port expansions and logistics corridor diversification accelerate infrastructure deployment. The region is positioned to transition from hydrocarbon-export dependence toward integrated maritime trade hubs anchored in containerization and energy transfer terminals. Greenfield port development is anticipated to favor high-specification pneumatic systems compatible with automated mooring and digital monitoring architectures. Harsh climatic conditions across Gulf coastlines are likely to reinforce preference for UV-resistant, high-durability rubber composites over legacy timber or low-grade elastomer solutions. Harmonization of maritime safety standards across GCC jurisdictions is expected to elevate specification thresholds and consolidate demand toward ISO-compliant suppliers. These structural forces are set to sustain MEA’s accelerated adoption curve within the global fender ecosystem.

North America Pneumatic Fender Market Trends

North America is expected to remain a mature and structurally stable market, supported by LNG export expansion and defense-linked maritime procurement. The region is positioned to emphasize premiumization rather than volume-led capacity buildout, with demand anchored in replacement cycles and high-specification upgrades. Strong alignment between safety mandates and environmental compliance frameworks is anticipated to reinforce the adoption of ISO-certified, high-durability pneumatic systems. Investment concentration along the Gulf Coast is projected to prioritize hydro-pneumatic and high-pressure configurations tailored for liquefied gas carriers. Technology differentiation through sensor-enabled monitoring and predictive maintenance platforms is expected to elevate lifecycle performance standards. These dynamics are likely to sustain North America’s high-value positioning within the global marine protection ecosystem.

The U.S. is expected to anchor regional momentum through LNG terminal expansion and naval modernization programs concentrated along the Gulf and Atlantic corridors. Federal oversight by maritime and environmental authorities is anticipated to preserve stringent qualification pathways for berthing protection systems. Terminal operators are likely to integrate smart fender technologies within broader port digitalization initiatives to enhance operational reliability and compliance transparency. Vendor strategies are projected to emphasize advanced elastomer formulations, corrosion-resistant fittings, and embedded monitoring solutions tailored for energy export terminals. Defense procurement frameworks are expected to sustain demand for rapid-deployment and mission-specific pneumatic configurations.

Europe Pneumatic Fender Market Trends

Europe is expected to remain a mature and structurally stable market, shaped by regulatory harmonization and sustainability-led infrastructure modernization. The region is positioned to emphasize replacement-driven demand as legacy berthing systems are upgraded to align with European Green Deal objectives. Ports across Northern and Western corridors are anticipated to integrate IoT-enabled pneumatic fenders within broader digital port architectures. Environmental compliance frameworks are likely to reinforce the specification of recyclable rubber compounds and energy-efficient production standards. Engineering depth and maritime design expertise are expected to sustain Europe’s leadership in customized, high-performance fender configurations.

Germany is expected to anchor regional momentum through advanced port modernization and engineering-led system integration strategies. Major gateways are anticipated to prioritize sensor-integrated fenders compatible with automated berth management platforms. Industrial collaboration between port authorities and marine engineering firms is likely to accelerate the adoption of tailored double-chamber and high-durability variants. Regulatory alignment across European Union member states is projected to standardize procurement criteria and phase out sub-compliant legacy installations. These dynamics are positioned to reinforce Germany’s role in shaping Europe’s innovation-oriented fender ecosystem.

Competitive Landscape

The global pneumatic fender market is moderately consolidated, with leadership concentrated among global marine engineering suppliers such as Yokohama Rubber Company, Trelleborg AB, ShibataFenderTeam, Palfinger AG, and FenderCare Marine. These participants influence specification benchmarks, ISO-compliant manufacturing standards, and procurement frameworks across LNG terminals, commercial ports, and naval installations. Their functional significance extends beyond product supply toward lifecycle engineering support, testing validation, and integration with automated mooring and monitoring platforms.

Competitive positioning reflects clear vertical differentiation between high-specification engineered systems and cost-optimized standard configurations serving volume-driven corridors. Market leaders integrate elastomer science, chain fabrication, hydro-pneumatic engineering, and increasingly sensor-enabled diagnostics within unified solution portfolios, while regional manufacturers compete on localized assembly, shorter lead times, and price discipline. The industry is witnessing gradual consolidation through strategic partnerships, service-led expansion, and digital platform integration linking pressure monitoring with port management systems. Lifecycle service models, including rental fleets and maintenance contracts, are expected to strengthen recurring revenue structures and reinforce ecosystem lock-in. As smart port initiatives expand, integration capability across hardware, electronics, and compliance documentation is positioned to define competitive resilience.

Key Industry Developments:

- In November 2025, Trelleborg opened a state-of-the-art manufacturing facility in Vietnam. Located in the Phu My 3 Specialized Industrial Park, this plant significantly ramps up manufacturing capacity for marine fenders to meet growing demand in Southeast Asia.

- In October 2025, Yokohama Rubber showcased its comprehensive range of "World-First" pneumatic fenders at the World Ports Conference. The presentation focused on visual demonstrations of durability testing and the operational capabilities of pneumatic models in supporting approximately 80% of global trade volume.

Companies Covered in Pneumatic Fender Market

- Trelleborg Marine & Infrastructure

- Shibata Fender Team AG

- The Yokohama Rubber Co., Ltd.

- Bridgestone Corporation

- Sumitomo Rubber Industries, Ltd.

- Palfinger AG

- Fendercare Marine

- Qingdao Jier Engineering Rubber

- Shandong Nanhai Airbag Engineering

- Evergreen Maritime

- IRM Offshore and Marine

- Anchor Marine & Supply, Inc.

- Marine Fenders International

- Toyo Seiko

- HYC Offshore

- Industrial Pneumatic Fenders Corp.

Frequently Asked Questions

The global pneumatic fender market is projected to reach approximately US$0.68 billion by 2033, expanding from an estimated US$0.43 billion in 2026. This growth trajectory reflects a compound annual growth rate of 6.7% during the forecast period, supported by vessel upsizing, LNG infrastructure expansion, and modernization of port berthing systems.

The transition toward Ultra Large Container Vessels and LNG carriers significantly increases berthing impact energy. Larger displacement and kinetic force during docking require higher energy absorption capacity. Pneumatic fenders calibrated for elevated reaction forces are increasingly specified to protect quay walls and vessel hull integrity across high-traffic maritime corridors.

The pneumatic fender market is anticipated to grow at a CAGR of 6.7% from 2026 to 2033. Historical growth between 2020 and 2025 remained stable at approximately 6.2%, indicating sustained structural expansion driven by fleet modernization and offshore terminal upgrades.

Smart pneumatic fenders equipped with IoT sensors enable real-time monitoring of internal pressure and impact loads. Integration with port digital management platforms supports predictive maintenance, reduces unplanned downtime, and enhances compliance documentation. This transition transforms fenders from passive safety components into intelligent infrastructure assets.

Key participants include Trelleborg Marine & Infrastructure, ShibataFenderTeam AG, The Yokohama Rubber Co., Ltd., Bridgestone Corporation, and Palfinger AG, alongside other regional and international marine engineering suppliers contributing to specification standardization and lifecycle service expansion.