- Media & Entertainment

- Photo Printers Market

Photo Printers Market Size, Share, and Growth Forecast, 2025 - 2032

Photo Printers Market By Technology (Inkjet Photo Printers, Dye-Sublimation Photo Printers, Others), Printer Format (Portable and Pocket Printers, Compact Desktop Printers, Others), End-user, and Regional Analysis for 2025 - 2032

Photo Printers Market Size and Trends Analysis

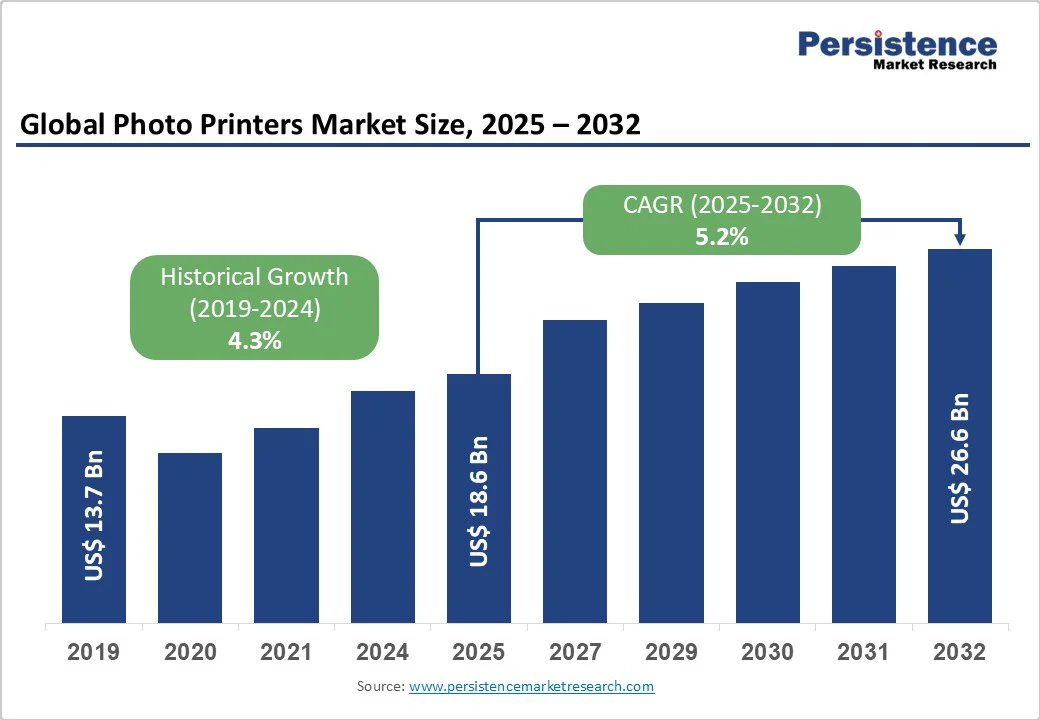

The global photo printer market is expected to reach US$18.6 billion in 2025. It is expected to reach US$26.6 billion by 2032, growing at a CAGR of 5.2% during the forecast period from 2025 to 2032, driven by rising demand for instant and portable printing solutions, greater smartphone integration, and continuous innovations in inkjet and dye-sublimation technologies.

Demand for personalized prints, event-based services, and mobile integration is reshaping the industry, while manufacturers focus on eco-friendly consumables and sustainable designs.

Key Industry Highlights

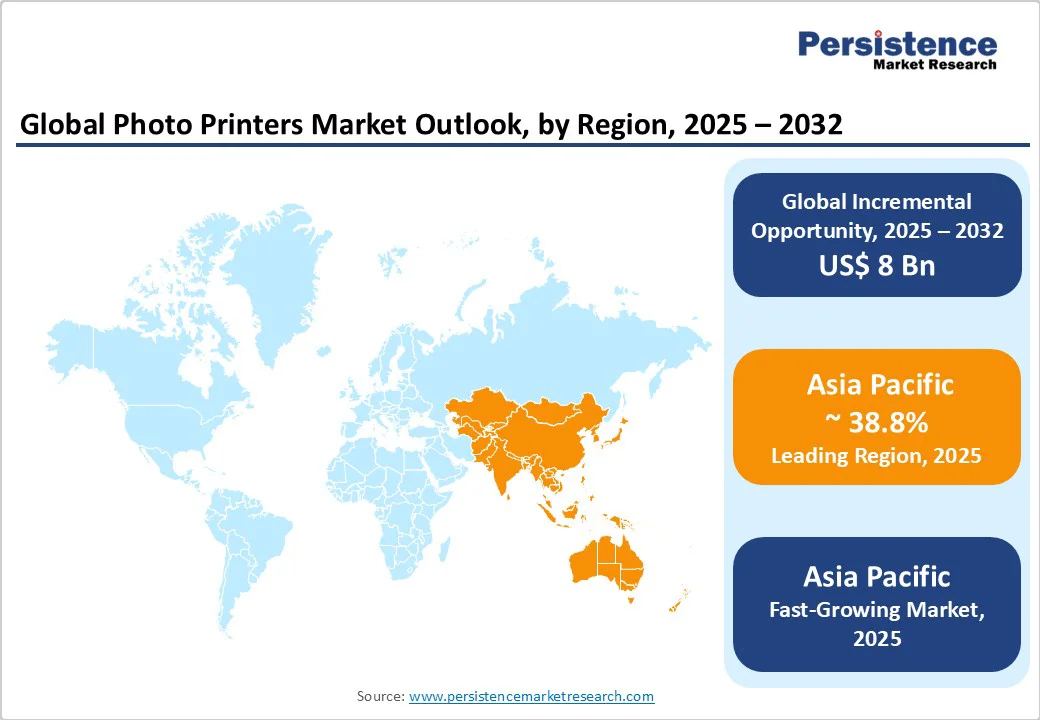

- Leading Region: Asia Pacific accounted for approximately 38.8% of the global market revenue, driven by large-scale manufacturing in China, high smartphone adoption, and strong consumer demand in Japan and India.

- Fastest-Growing Region: Asia Pacific is supported by expanding urban populations, domestic production incentives, and rapid growth in on-demand and event-based photo printing.

- Investment Plans: Major industry leaders such as Canon, Epson, and HP are investing in AI-enabled printing systems, recyclable materials, and compact dye-sublimation printers to strengthen their global portfolios and sustainability credentials.

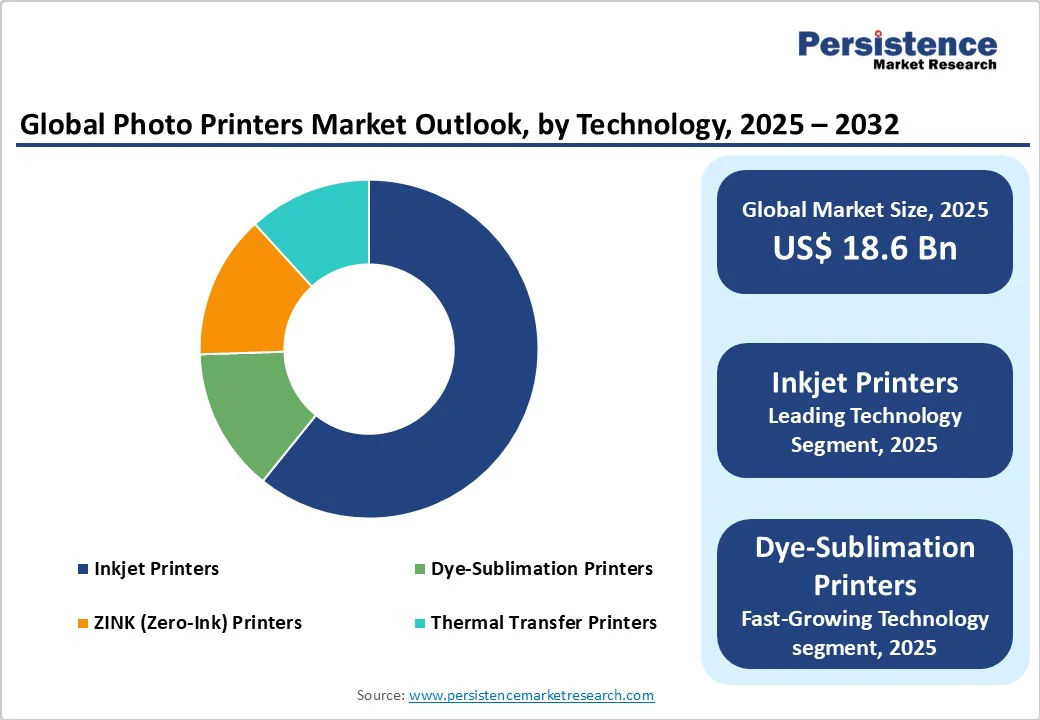

- Dominant Technology: Inkjet printers maintain a 62.3% share of the global market, attributed to affordability, multipurpose functionality, and technological improvements in printhead precision and pigment-based ink formulations.

- Leading Printing Format: Kiosk and Minilab Systems account for about 29% of market share due to widespread adoption in retail photo centers and pharmacies, offering instant printing, digital payment integration, and high-volume throughput.

| Key Insights | Details |

|---|---|

| Photo Printers Market Size (2025E) | US$18.6 Bn |

| Market Value Forecast (2032F) | US$26.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Instant and Mobile Printing

Smartphone penetration and social-media-driven lifestyles are key growth catalysts. Consumers increasingly prefer to capture and print photographs instantly for personal collections and events. The proliferation of portable printers that connect directly to smartphones has accelerated this trend.

Portable photo printers are growing at an annual rate of over 10% and have become an accessible entry point for consumers, especially millennials and Gen-Z. The adoption of compact wireless printers at social events and retail spaces enhances user engagement and drives recurring sales of consumables such as ribbons, photo paper, and film cartridges.

Advancements in Printing Technologies

Continuous innovation in dye-sublimation and precision inkjet technologies has improved print quality, color accuracy, and durability. Inkjet technology currently accounts for nearly 62% of global revenue, supported by its broad compatibility with various photo media and lower operational costs.

Dye-sublimation offers quick drying and smudge-free output, making it ideal for instant photo services and portable printers. The rapid transition to high-definition printheads, coupled with power-efficient and compact printer designs, has expanded adoption across both consumer and professional segments, leading to faster replacement cycles and higher upgrade rates.

Recurring Revenue from Consumables and Media

A fundamental growth factor for photo printer manufacturers is the razor-and-blade business model, in which affordable hardware drives long-term revenue from consumables. As users print frequently at home or during events, recurring demand for ink cartridges, ribbons, and photo paper ensures predictable revenue streams.

Subscription models for ink refills and creative print packs are being integrated into mobile applications, raising per-user spending. This model enhances vendor profitability and customer retention while stabilizing revenue even when hardware unit sales fluctuate.

Barrier Analysis - High Consumables Cost and Environmental Regulations

Despite technological progress, consumables remain relatively expensive. The total cost of ownership for photo printers, factoring in ink, ribbons, and specialty media, can exceed the initial device cost, discouraging long-term adoption among price-sensitive consumers.

Environmental regulations in the European Union and North America mandate responsible waste management and recycling, increasing compliance expenses for manufacturers. Companies with strong circular supply chains and recycling programs are better positioned to absorb these regulatory costs, while smaller manufacturers face margin pressure.

Digital Substitution and Reduced Printing Frequency

The proliferation of high-resolution smartphone displays and social-media sharing platforms has diminished the need for physical prints. Younger demographics increasingly store and share photos digitally, reducing per-capita photo printing volumes.

Online print-on-demand services also capture part of the value chain by offering affordable photo books and gifts without hardware ownership. These trends collectively limit the addressable consumer base for standalone photo printers, compelling manufacturers to focus on premium niches and high-frequency event applications.

Opportunity Analysis - Expansion of Portable and Smartphone-Connected Printers

The most promising opportunity lies in portable and smartphone-integrated printers, which are expected to record a CAGR exceeding 10% through 2030. These compact devices cater to on-the-go printing and creative expression, appealing strongly to younger users.

Manufacturers that offer app-driven customization, augmented-reality overlays, and consumable subscription services can increase user engagement and profitability. With the portable category already accounting for over one-fourth of global unit shipments, this segment will remain central to market expansion through 2032.

Event and Experiential Printing Services

Event printing is a fast-growing application, driven by weddings, exhibitions, music festivals, and brand activations. The event and entertainment segment is expanding at a high CAGR, contributing significantly to the consumables turnover.

Service providers and rental operators increasingly deploy compact dye-sublimation and wireless printers that deliver immediate outputs. OEMs partnering with event companies and retail networks can achieve higher recurring revenues through media sales and equipment leasing, transforming printers from static devices into integrated event-solution systems.

Software Ecosystem and Subscription Integration

The convergence of hardware and software platforms presents new monetization avenues. Integrating cloud storage, editing tools, and automatic refill subscriptions enables continuous engagement beyond hardware sales. Consumers benefit from creative control, while manufacturers secure predictable recurring income.

Subscription-based service models also provide valuable usage data that can inform product innovation. This digital integration has become a key differentiator among leading brands, allowing them to compete not only on print quality but on user experience and app functionality.

Category-wise Analysis

Technology Insights

Inkjet printers continue to dominate the global photo printer landscape, accounting for nearly 62.3% of total market revenue. Their popularity stems from a balance of affordability, versatility, and user familiarity. Inkjet photo printers accommodate a wide range of media formats and are widely used in home and professional settings due to their ability to print both photographs and standard documents.

Ongoing innovation in micro-piezo printhead architecture and pigment-based ink formulations has notably improved image resolution, color saturation, and fade resistance. These technological enhancements ensure that inkjet printers remain the preferred choice for consumers and professionals alike, securing their leading position through 2032.

Dye-sublimation printers represent the fastest-growing technology segment. Their ability to produce high-quality, smudge-resistant prints in seconds has made them indispensable for instant photo booths, event kiosks, and portable photo printing solutions.

Leading manufacturers such as Canon and Fujifilm have expanded their product portfolios to include advanced dye-sublimation models equipped with wireless connectivity, compact form factors, and enhanced print speeds. The ongoing surge in travel photography, experiential events, and social media-driven demand for tangible photo outputs continues to propel this segment’s rapid global expansion.

Printer Format Insights

Kiosk and minilab systems held approximately 29% of the global market share, reflecting their pivotal role in retail photo finishing and pharmacy printing services. Their reputation for high reliability, fast throughput, and consistent print quality underpins steady adoption across major retail chains worldwide.

Modern kiosks are being upgraded with touch-free upload capabilities, cloud-based photo management, and integrated digital payment systems, aligning with changing consumer behavior and hygiene preferences. This digital transformation allows brick-and-mortar photo centers to maintain relevance and customer engagement in an era dominated by mobile photography and online sharing.

Portable and pocket printers are the most dynamic category. Compact, battery-powered devices that connect seamlessly via Bluetooth or Wi-Fi have become particularly popular among smartphone users, travelers, and creative hobbyists. Their appeal lies in portability, instant photo gratification, and the fun of personal customization through mobile apps.

Many brands now offer co-branded or influencer-designed editions, positioning these devices as both functional and lifestyle accessories. The segment’s strong connection to mobile ecosystems ensures sustained growth momentum, especially within younger demographics seeking tangible, shareable memories.

Regional Insights

Asia Pacific Photo Printers Market Trends - Manufacturing Strength and Social Media-Driven Market Growth

Asia Pacific remains the largest and fastest-growing regional market, accounting for nearly 38.8% of global photo printer revenue. China leads regional production and consumption, benefiting from extensive manufacturing infrastructure and competitive component sourcing.

Japan continues to dominate the premium and professional photo printer category, leveraging its advanced imaging ecosystem and innovations in thermal dye-transfer technology. India and ASEAN countries, including Thailand, Indonesia, and Vietnam, are emerging as key growth markets, supported by urbanization, smartphone proliferation, and rising disposable incomes.

Recent developments underscore Asia Pacific’s growing industrial self-sufficiency. In March 2025, Canon Inc. inaugurated a new manufacturing line in Zhuhai, China, to produce portable dye-sublimation printers for export across Southeast Asia. Epson Singapore introduced its SureLab D1070 series in 2024, targeting event photographers and small studios seeking high-speed output.

In India, HP launched its Smart Photo Studio program (2025) in collaboration with local distributors to train small printing businesses on sustainable operations and digital workflows.

Government initiatives, including India’s “Make in India” program and Vietnam’s electronics localization schemes, continue to attract investment in regional production hubs, lowering import dependency and enhancing supply chain efficiency. The combination of social media-driven photo culture, event-based printing demand, and technological affordability positions Asia Pacific as the engine of global market growth through 2032.

North America Photo Printers Market Trends - Premium Innovation and Sustainable Printing Ecosystem

North America represents a mature yet highly profitable photo printer market, sustained by strong consumer purchasing power and a large installed base of professional and home photo printers.

The U.S. continues to lead regional demand, driven by event photography, influencer-led brand activations, and photo booth services at weddings and social gatherings. Retail leaders such as Walmart and CVS Health have invested in next-generation photo kiosks featuring touchless user interfaces and AI-based image enhancement systems, enhancing convenience and safety.

In April 2025, HP Inc. launched its Smart Tank Photo series in the U.S., emphasizing refillable ink solutions and carbon-neutral operations. Canon USA expanded its service footprint by integrating cloud-based photo management into its mini printer lineup for seamless smartphone connectivity. Canada’s market reflects a stable growth trajectory, underpinned by consumer preference for eco-certified printers and reusable photo paper.

Regulatory measures, such as Canada’s Extended Producer Responsibility (EPR) policy, are prompting manufacturers to redesign consumables using recyclable and biodegradable materials. The region’s innovation ecosystem, anchored by Epson, HP, and Canon R&D centers, continues to fuel advances in image processing and color calibration technologies, reinforcing North America’s status as a hub for printer innovation.

Europe Photo Printers Market Trends - Eco-Design Leadership and Cloud-Connected Retail Expansion

Europe displays balanced market expansion, driven by a blend of environmental consciousness, premium imaging culture, and modernized retail photo services. Germany remains the nucleus of professional-grade printing technologies, hosting advanced R&D centers for companies such as Epson Europe GmbH and Fujifilm Europe.

The U.K. and France lead in compact and portable printer adoption, fueled by high smartphone penetration and the trend toward home-based printing for instant memories. Southern markets, especially Spain and Italy, are experiencing renewed demand from tourism-related photo printing, event photography, and travel souvenir production.

The European Union’s Circular Economy Action Plan and updated Waste Electrical and Electronic Equipment (WEEE) Directive mandate strict compliance with cartridge recycling and waste reduction. These frameworks are pushing OEMs to adopt closed-loop production systems and eco-friendly, refillable printer designs. In February 2024, Fujifilm Europe unveiled its Instax Mini SE, a portable printer made with 30% recycled plastic, setting new benchmarks for sustainable design.

Epson Europe launched its EcoTank L-series printers in October 2024, integrating heat-free printing technology that reduces energy consumption by up to 80% compared to thermal rivals. Partnerships between printer brands and retail chains, such as CEWE’s collaboration with Canon Europe in 2025 to deploy cloud-connected kiosks across EU photo labs, have also improved accessibility and digital service integration across the continent.

Competitive Landscape

The global photo printers market is moderately concentrated, led by Epson, Canon, HP, Fujifilm, and Kodak, which together generate over 60% of revenue through strong brands, technological leadership, and global distribution. Mid-tier players such as DNP, Brother, and HiTi focus on niche segments such as portable and dye-sublimation printers.

Competition centers on product innovation, consumables integration, and geographic expansion. Leading companies emphasize ecosystem integration, subscription ink services, mobile apps, and sustainability, while optimizing costs and digital engagement to strengthen customer loyalty.

Key Industry Developments

- In August 2025, Xiaomi launched the Portable Photo Printer 1S in Spain, a palm-sized ZINK printer (50 × 76 mm output) with Bluetooth 5.2, multi-user connectivity, and AR editing features, positioned for mobile, travel, and youth segments.

- In January 2025, Instax (under Fujifilm Holdings Corporation) announced the launch of the Instax Wide Evo Hybrid instant camera/printer, which doubles as a smartphone-connected printer for 50 × 76 mm film prints and uses Bluetooth wireless connection for print-from-phone.

Companies Covered in Photo Printers Market

- Canon Inc.

- Seiko Epson Corporation

- HP Inc.

- Fujifilm Holdings Corporation

- Sony Corporation

- Mitsubishi Electric Corporation

- Kodak Alaris Inc.

- Ricoh Company, Ltd.

- LG Electronics Inc.

- Brother Industries, Ltd.

- Samsung Electronics Co., Ltd.

- Polaroid Corporation

- Lexmark International, Inc.

- Dell Technologies Inc.

- HiTi Digital, Inc.

- Shinko Electric Co., Ltd.

- DNP Imagingcomm America Corporation

- Xiaomi Corporation

- Zebra Technologies Corporation

- Kyocera Document Solutions Inc.

Frequently Asked Questions

The photo printers market size in 2025 is estimated at US$18.6 Billion.

By 2032, the photo printers market is projected to reach US$26.6 Billion.

Key trends include portable and smartphone-connected printers, wireless and cloud integration, eco-friendly consumables, dye-sublimation advancements, subscription ink services, and AI-driven print quality optimization.

Inkjet printers lead the market with a 62.3% share, driven by affordability, versatility, and innovations in printhead design and pigment-based inks.

The photo printers market is expected to grow at a CAGR of 5.2% from 2025 to 2032.

Major players include Canon Inc., Seiko Epson Corporation, HP Inc., Fujifilm Holdings Corporation, and Sony Corporation.