- Home Appliances

- Inkjet Printers Market

Inkjet Printers Market Size, Share, and Growth Forecast, 2025 - 2032

Inkjet Printers Market By Product Type (Consumer & Home Printers, Office & SMB Printers, Others), Technology (Piezoelectric Drop-on-Demand (DOD), Thermal Inkjet, Others), Ink Type, End-user, and Regional Analysis for 2025 - 2032

Inkjet Printers Market Size and Trends Analysis

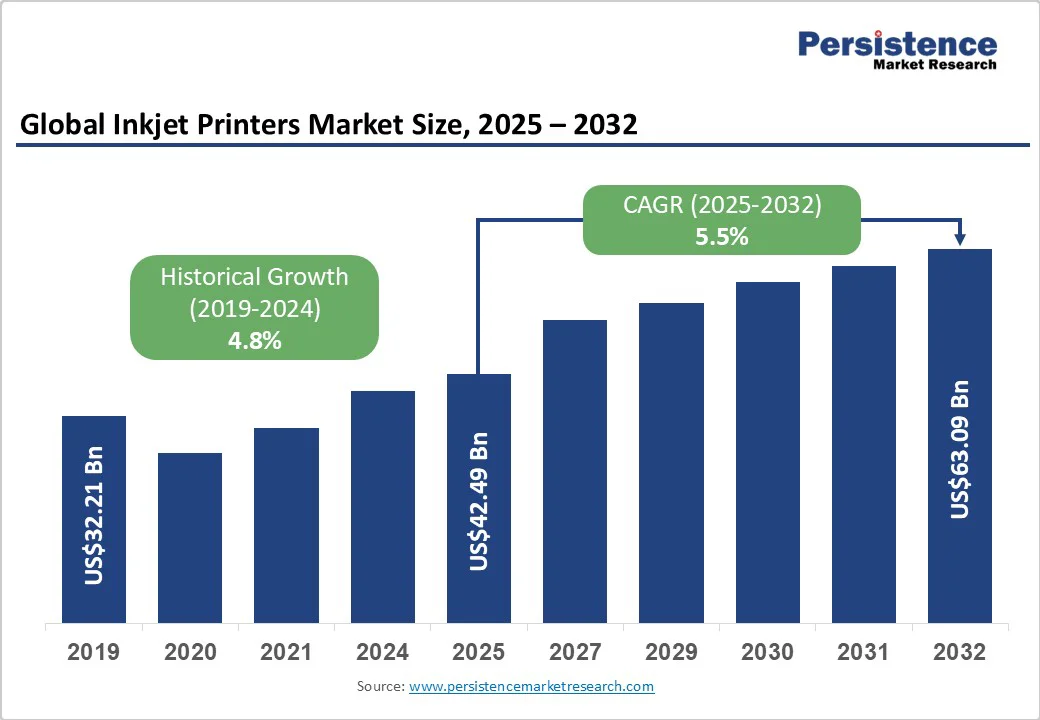

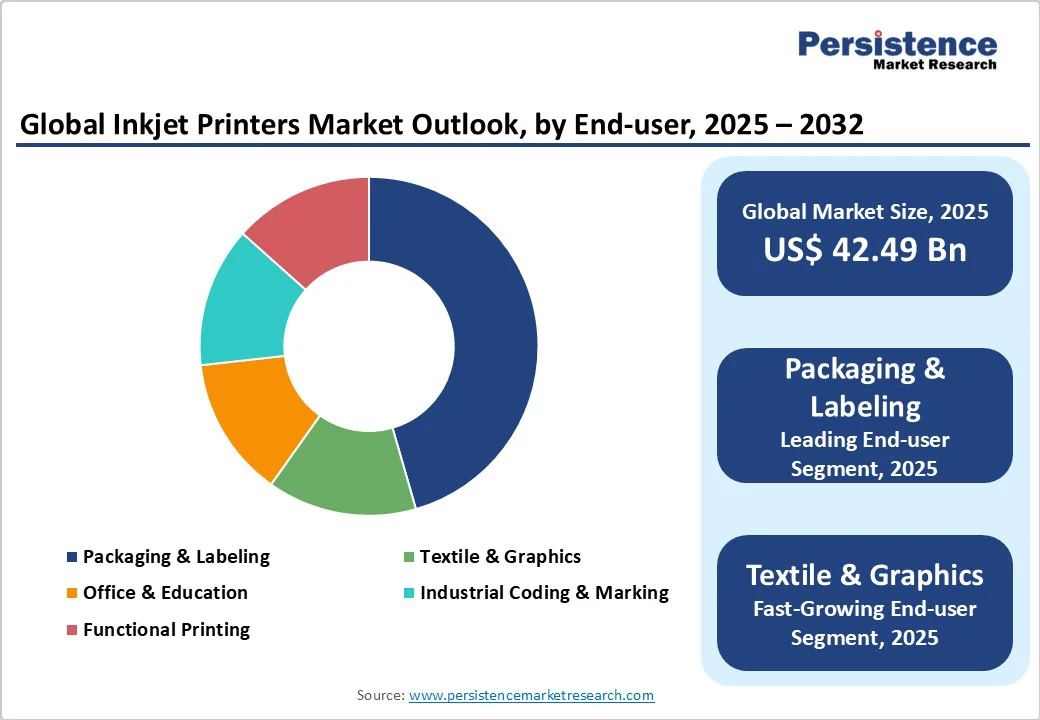

The global inkjet printers market size is likely to be valued at US$42.49 Billion in 2025. It is expected to reach US$63.09 billion by 2032, growing at a CAGR of 5.5% during the forecast period from 2025 to 2032, driven by rising demand for digital printing in packaging and textile applications, cost-effective high-resolution printing technologies, and the adoption of refillable ink systems among consumers and small businesses.

Continuous technological advancements in AI-assisted image correction, high-speed printheads, and sustainable ink formulations are further supporting this expansion.

Key Industry Highlights

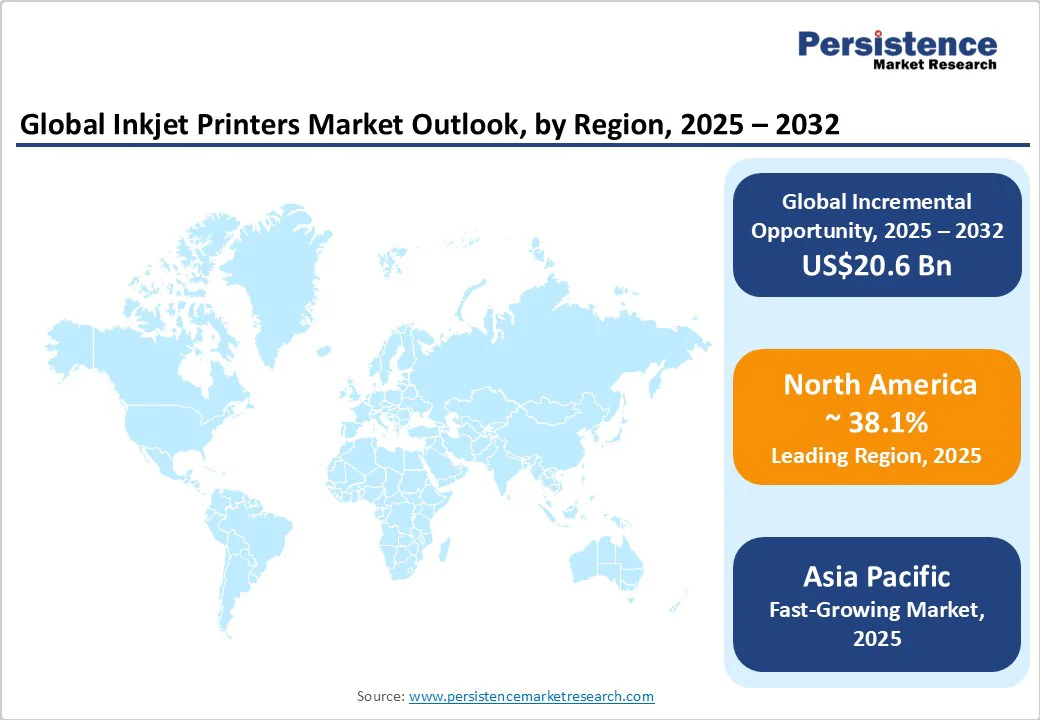

- Leading Region: North America, accounting for approximately 38.1% of the global market revenue in 2025, driven by high adoption of production inkjet in packaging and commercial printing.

- Fastest-Growing Region: Asia Pacific, fueled by industrial expansion, textile printing demand, and low-cost manufacturing advantages.

- Investment Plans: Major OEMs (HP, Canon, Epson) are expanding production inkjet capacity, AI-enabled workflow systems, and local manufacturing in Asia Pacific and North America, representing an estimated US$3-4 billion in capex over 2025 - 2032.

- Dominant Product Type: Consumer & SMB printers lead in unit shipments, capturing approximately 51.6% of total market share in 2025, due to affordability and multifunction adoption.

- Leading End-user: Packaging & Labeling segment commands the highest revenue share at 46.2%, driven by the increasing demand for short-run, customized packaging and variable data printing.

| Key Insights | Details |

|---|---|

| Inkjet Printers Market Size (2025E) | US$42.49 Bn |

| Market Value Forecast (2032F) | US$63.09 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Commercialization of high-speed production inkjet and packaging adoption

The ongoing industrial shift toward high-speed, production-grade inkjet presses has become a major catalyst for market expansion. Packaging converters and commercial printers are increasingly opting for digital inkjet systems due to their ability to deliver variable data printing, reduced setup times, and shorter production cycles.

Vendors such as HP, Canon, and Epson have launched production presses with enhanced throughput and improved ink efficiency. This adoption reduces waste, minimizes downtime, and meets brand owners’ needs for short-run, customizable packaging, accelerating the displacement of traditional offset and flexographic printing in commercial environments.

Lower total cost of ownership through refillable and tank-based ink systems

The introduction of refillable ink-tank systems, notably Epson’s EcoTank, Canon’s MegaTank, and HP’s Smart Tank, has redefined printer economics for small and medium-sized users. By replacing costly cartridges with bulk refillable tanks, operating costs drop by as much as 70-80% over the device’s lifetime.

This cost-efficiency, combined with longer maintenance intervals and reduced plastic waste, has attracted price-sensitive home users and emerging-market SMEs. The resulting shift in consumer preference supports both unit-volume growth and recurring ink-sales revenue for OEMs, ensuring stable long-term market expansion.

Integration of AI and cloud-based printing workflows

Inkjet printers are evolving into intelligent, connected systems through AI-driven image optimization, predictive maintenance, and cloud printing services. This integration enables real-time performance monitoring and remote workflow management, enhancing uptime for enterprise customers.

The automation of color calibration and print error correction reduces operator dependence while maintaining professional output standards. As industries adopt hybrid working models and on-demand printing, these smart workflow solutions provide improved reliability and scalability, turning inkjet systems into data-enabled assets within digital production ecosystems.

Barrier Analysis - Erosion of consumable margins and aftermarket competition

Inkjet OEMs face increasing margin pressure from the proliferation of third-party ink refills and non-genuine cartridges. These alternatives undercut OEM ink pricing, affecting recurring revenue streams that historically sustained hardware sales.

The growth of refill stations and online suppliers, especially in emerging markets, has intensified competition. While manufacturers implement firmware updates and subscription models to protect margins, the structural shift toward lower-priced consumables continues to challenge profitability.

Supply-chain bottlenecks for specialized components and inks

Advanced printheads, semiconductor components, and specialty inks rely on complex global supply chains. Periodic shortages of piezoelectric materials, photoinitiators, and precision nozzles have constrained production capacities and lengthened delivery cycles.

For new entrants, stringent chemical compliance standards for inks, particularly in food packaging and medical labeling, raise production costs and delay market entry. These constraints slow capacity expansion and increase dependence on established OEM suppliers.

Opportunity Analysis - Growth in on-demand packaging and variable data printing

The surge in e-commerce and customized packaging has created substantial opportunities for digital inkjet presses in short-run and personalized production. Inkjet’s capability to print barcodes, QR codes, and individualized labels at high speed makes it ideal for agile packaging lines.

The market for digitally printed packaging is expected to expand rapidly as brands seek to localize their marketing and differentiate products. Manufacturers offering scalable, cloud-connected packaging solutions stand to capture this emerging value pool.

Expansion in industrial and functional printing applications

Inkjet technology is advancing beyond graphics into functional and industrial printing, including printed electronics, textiles, biomedical devices, and direct-to-object applications. These uses demand precise material deposition and specialized inks such as conductive, UV-curable, or bio-compatible formulations. With R&D investments increasing in these sectors, inkjet vendors have the chance to establish early dominance in high-margin industrial niches where competition is limited and technical barriers are high.

Category-wise Analysis

Product Type Insights

Consumer and small-office printers are the largest segment, representing 51.6% of market share, supported by affordability, compact size, and multifunction features. The popularity of wireless all-in-one inkjet devices has made them essential household tools for both professional and educational purposes. Their extensive installed base ensures steady consumables demand and provides a platform for OEMs to introduce subscription-based ink delivery services.

Commercial and production inkjet systems are experiencing the strongest revenue growth due to rising investment from packaging converters, print shops, and textile manufacturers. These devices deliver industrial-scale throughput, wider color gamut, and digital workflow compatibility, enabling rapid job turnover. With increasing emphasis on short-run flexibility and sustainability, production-grade inkjet systems are expected to outperform other categories during the forecast period.

End-user Insights

The packaging and labeling industry accounts for the largest revenue share, at 46.2%, driven by consumer demand for customized and sustainable packaging solutions. Inkjet systems enable efficient short runs and just-in-time production, reducing inventory waste for converters. The adoption of water-based and UV-curable inks that meet food-safety regulations further solidifies inkjet’s position in this sector.

Textile and large-format graphics printing are expected to register the highest CAGR. The rise of on-demand fashion, custom décor, and soft-signage applications has made digital inkjet printing an attractive alternative to screen printing. Eco-friendly pigment inks and direct-to-fabric printing technologies lower water and energy use, aligning with global sustainability initiatives and boosting adoption among small textile producers.

Regional Insights

North America Inkjet Printers Market Trends - Leadership in Production Inkjet and Smart Printing Infrastructure

North America represents the largest regional market, capturing around 38.1% of the global revenue in 2025. The U.S. dominates the region due to early adoption of production inkjet technologies, a robust commercial printing network, and strong demand from sectors such as healthcare, logistics, and e-commerce for labeling and document printing.

The presence of major OEMs such as HP Inc., Xerox Holdings, and Canon Inc. ensures high service reliability and advanced technical support.

The region’s regulatory environment, emphasizing energy efficiency and electronic waste recycling, has pushed manufacturers toward developing eco-compliant printers and sustainable ink solutions.

Recent developments underscore this trend, in April 2025, HP introduced its PageWide Advantage 2200 press, enhancing high-speed production capabilities for packaging applications, while Xerox expanded its AI-driven print analytics platform to support managed print services.

Continued investments in AI-enabled workflow automation, cloud-based fleet management, and predictive maintenance tools are reinforcing North America’s position as a technology leader in the global inkjet printers market.

Europe Inkjet Printers Market Trends - Growth Driven by Eco-Friendly Printing and Regulatory Compliance

Europe stands as the second-largest market for inkjet printers, led by Germany, the U.K., and France. Germany’s industrial prowess and advanced packaging sector anchor demand for industrial-grade and wide-format inkjet applications, while the U.K. and France continue to expand their digital print production capabilities.

The region’s regulatory framework, shaped by REACH and WEEE directives, enforces stringent controls on ink formulation and electronic waste disposal, which favors established OEMs with proven compliance records such as Canon, Ricoh, and Epson.

Europe is also witnessing a pronounced shift toward eco-friendly and water-based ink technologies, as well as increasing adoption of digital textile printing in response to sustainability mandates. For instance, in February 2025, Epson Europe launched the Monna Lisa ML-64000, a textile printer aimed at sustainable, high-speed printing for the fashion sector.

Canon introduced its Arizona 2300 FLXflow system in 2024, targeting wide-format commercial applications. The region’s trend toward localized manufacturing, shorter supply chains, and reduced carbon footprints continues to accelerate the transition from conventional offset printing to digital inkjet alternatives.

Asia Pacific Inkjet Printers Market Trends - Fastest-Growing Hub for Digital and Industrial Inkjet Expansion

Asia Pacific remains the fastest-growing regional market. The region’s momentum is driven by rapid industrialization, rising consumer demand, and strong manufacturing competitiveness.

China and Japan lead global production of printheads, inks, and printer assemblies, while India and ASEAN nations contribute significantly to consumer and SMB printer shipments. Low labor costs, expanding small-business ecosystems, and government-backed initiatives such as “Make in India” and “Made in China 2025” are attracting sustained OEM investments.

The region’s inkjet growth is also amplified by the booming textile and packaging industries, which are increasingly adopting digital inkjet systems for short-run, customized, and sustainable production. Notably, in March 2025, Seiko Epson announced the expansion of its production facility in the Philippines to increase output of PrecisionCore printheads, and Canon established a new R&D center in Shenzhen, China, to advance ink formulation and printhead efficiency.

Competitive Landscape

The global inkjet-printers market is moderately consolidated. Global leaders, HP, Canon, and Epson, collectively hold over half of the total revenue. Other notable participants, such as Ricoh, Fujifilm, and Konica Minolta, compete strongly in production printing, while regional players address niche applications such as coding and textile printing. Competition is increasingly defined by intellectual property in printhead design, ink chemistry, and workflow software, rather than hardware differentiation alone.

Market leaders are focusing on innovation-driven cost leadership, expanding service portfolios, and developing subscription-based ink programs to stabilize recurring revenues. Partnerships with cloud-platform providers, ink-chemistry specialists, and logistics firms support vertically integrated solutions. New entrants are pursuing niche growth in industrial and functional printing, where customization and technical expertise deliver defensible margins.

Key Industry Developments

- In May 2025, Epson introduced three new PrecisionCore printheads designed for high-speed commercial printing, enabling broader adoption in textile and signage applications.

- In February 2025, Canon Inc. launched new imagePROGRAF PRO and MegaTank G-Series printers to address the prosumer and SME market segments, improving efficiency and printhead longevity.

Companies Covered in Inkjet Printers Market

- HP Inc.

- Canon Inc.

- Seiko Epson Corporation

- Ricoh Company, Ltd.

- Konica Minolta, Inc.

- Xerox Holdings Corporation

- Fujifilm Holdings Corporation

- Brother Industries, Ltd.

- Eastman Kodak Company

- Mimaki Engineering Co., Ltd.

- Mutoh Industries Ltd.

- Markem-Imaje (Dover Corporation)

- Videojet Technologies (Danaher Corporation)

- Kyocera Corporation

- Panasonic Holdings Corporation

- Roland DG Corporation

- Lexmark International, Inc.

- Sharp Corporation

- Toshiba Tec Corporation

- OKI Data Corporation

Frequently Asked Questions

The market size is estimated at US$42.49 Billion in 2025.

The inkjet printers market is projected to reach US$63.09 Billion by 2032.

Key trends are the adoption of refillable and tank-based ink systems in consumer and SMB segments, and production-grade inkjet printers gaining traction in packaging and textile applications.

The consumer & SMB printer segment leads in unit shipments with around 51.6% share, driven by affordability, multifunction features, and strong adoption in households and small offices.

The inkjet printers market is expected to grow at a CAGR of 5.5% between 2025 and 2032.

The key market players include HP Inc., Canon Inc., Seiko Epson Corporation, Ricoh Company, Ltd., and Konica Minolta, Inc.