- Beauty & Personal Care

- Personal Care Ingredients Market

Personal Care Ingredients Market Size, Share, Trends, Growth, Forecast 2026 - 2033

Personal Care Ingredients Market By Ingredients (Surfactants, Emollients, Conditioning Polymers, Rheology Modifiers, Antimicrobials, UV Protection, Color Cosmetic Ingredients, Emulsifiers, Others), Source (Natural, Synthetic), Application (Skin Care, Hair Care, Oral Care, Color Cosmetics, Antiperspirants & Deodorants (AP/Deo), Toiletries, Nail Care, Others), by Regional Analysis, 2026 - 2033

Personal Care Ingredients Market Share and Trends Analysis

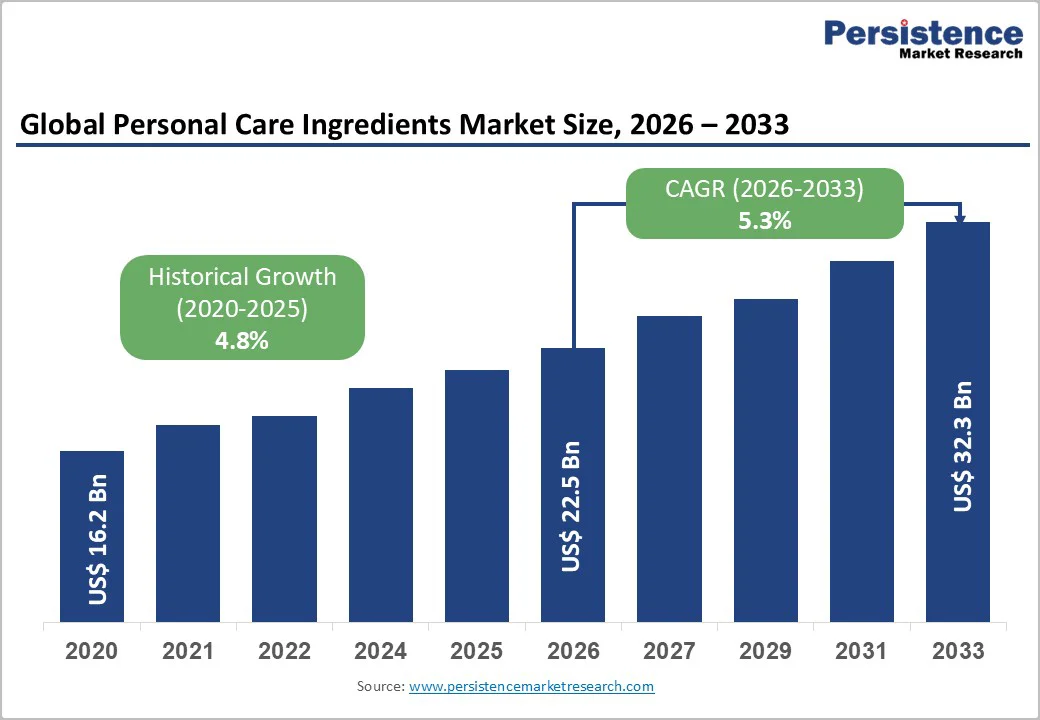

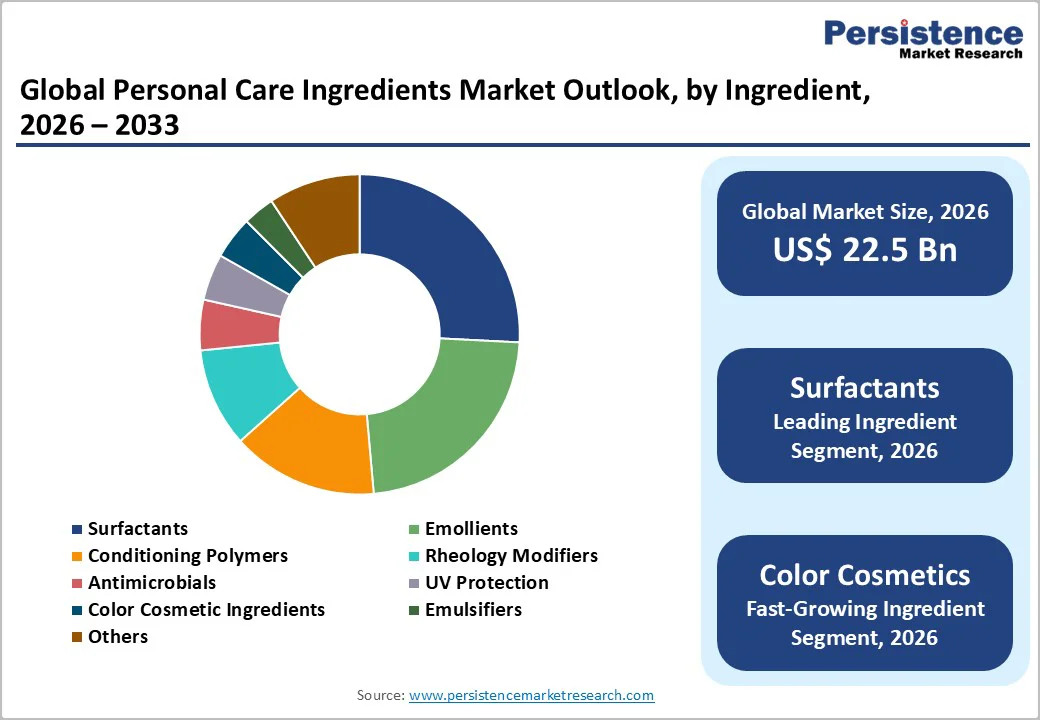

The global personal care ingredients market size is valued at US$22.5 billion in 2026 and is projected to reach US$32.3 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. Shifts in consumer preference toward natural and sustainable formulations, rising disposable incomes in emerging economies, and increased awareness of skin health and personal hygiene post-pandemic are among the crucial drivers of market growth.

The personal care ingredients industry has been indicating consistent upward momentum as beauty and wellness segments integrate advanced biotechnology-derived actives and clean-label ingredients to meet evolving consumer demands for efficacy, transparency, and environmental responsibility.

Global Personal Care Ingredients Market: Key Takeaways

- Natural Ingredients Dominance: Natural ingredients command 50% market share in 2026 while simultaneously representing the fastest-growing segment, with the organic cosmetics market to exceed US$50 billion by 2033, reflecting the clean beauty transformation

- Segmentation Leadership: Surfactants dominate with 25% share, while color cosmetic ingredients emerge as the fastest-growing segment

- Leading Application Segment: Skin care applications lead with 45% share, followed by hair care and color cosmetics

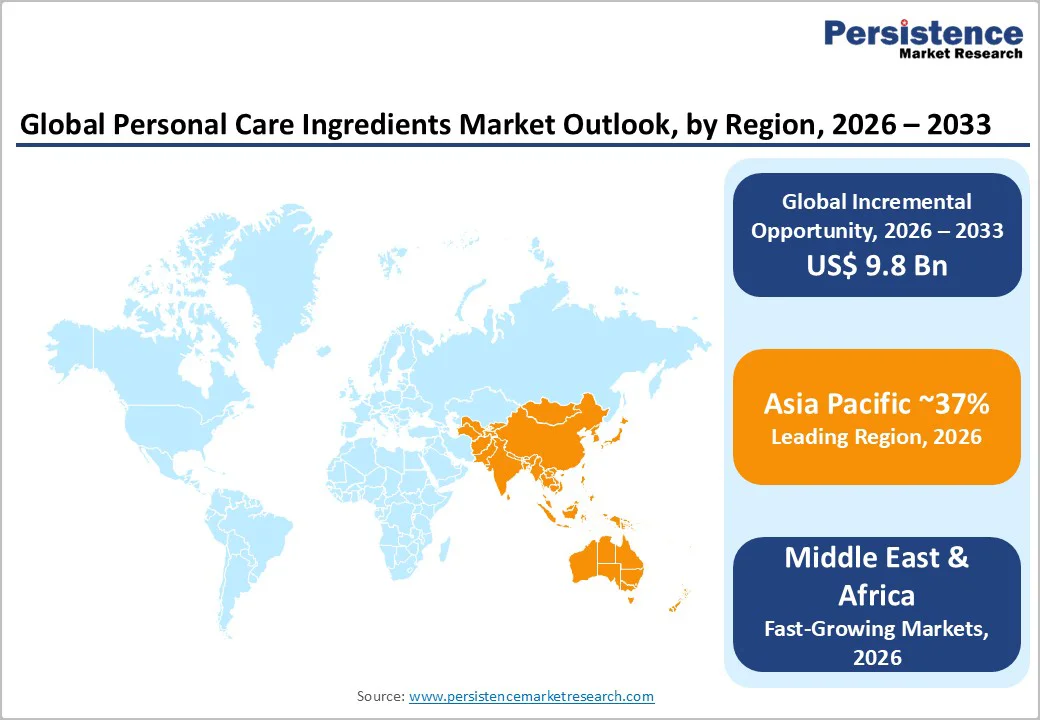

- Regional Dynamics: Asia Pacific leads with over 35% global share, Europe second largest; Africa is the fastest-growing region with double-digit growth projected

- Strategic M&A Activity: Clariant acquired Lucas Meyer Cosmetics (US$810 million); Evonik acquired Novachem, DSM merger with Firmenich

- Regulatory Evolution: European Commission issued four major cosmetic ingredient amendments in 2024 including UV-filter restrictions, nanomaterial prohibitions, and 64 CMR substance bans effective 2025-2026, driving reformulation investments and sustainable alternative development

| Key Insights | Details |

|---|---|

|

Personal Care Ingredients Market Size (2026) |

US$22.5 billion |

|

Projected Market Value (2032F) |

US$32.3 billion |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.3% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

4.8% |

Market Dynamics Analysis

Drivers - Rising Consumer Preference for Natural and Organic Ingredients

The personal care ingredients market is experiencing a fundamental shift toward natural and sustainable formulations, with the natural ingredients segment dominating the market. According to the Chemical Abstracts Service (CAS), over 40% of global consumers now prioritize natural components in their beauty and personal care products, reflecting heightened health consciousness and concerns regarding synthetic chemicals and their potential long-term effects. This behavioral transformation has been reinforced by post-pandemic hygiene routines, with the U.S. Centers for Disease Control and Prevention (CDC) reporting that over 50% of U.S. adults adopted improved personal hygiene practices during COVID-19, many of whom continue to prioritize non-toxic, dermatologist-tested formulations.

The natural cosmetics ingredients market is projected to expand significantly, demonstrating the accelerating momentum of bio-derived, biodegradable, and upcycled ingredients in premium formulations. Major ingredient suppliers are responding by launching natural-based product lines and acquiring biotech-active capabilities to capture premiums associated with a performance-plus-ecolabeling positioning.

Expansion of Skincare and Anti-Aging Product Segments

Skincare applications command the leading market position, accounting for over 45% of market share in 2025, driven by increasing global focus on skin health, anti-aging benefits, and cosmeceutical efficacy. The growth of the global skincare ingredients market is driven by sophisticated consumer demand for active ingredients that deliver measurable outcomes, including peptides, botanicals, microbiome-friendly actives, and encapsulated delivery systems.

Demographic shifts further reinforce this trend, particularly in Europe, where aging populations are driving demand for anti-aging formulations backed by clinical evidence. According to a survey, 70% of Indian consumers prefer skincare products formulated with organic and plant-derived ingredients, while North American markets demonstrate high per capita spending on dermatological products.

The conditioning polymers segment, which is expected to grow with a CAGR of 3.5% between 2026 and 2033, is valued for enhancing texture, moisturization, and manageability across hair and skincare applications. This convergence of efficacy-driven innovation and demographic tailwinds positions skincare ingredients as the cornerstone of market growth through 2032.

Technological Advancement and Biotechnology Integration

Ingredient innovation through biotechnology, precision fermentation, and AI-driven formulation platforms is fundamentally transforming product development cycles and ingredient sophistication. The biotech-derived skincare actives segment is exhibiting double-digit growth, projected to exceed US$10 billion by 2033, as brands pivot toward lab-grown peptides, growth factors, and probiotic ferments offering targeted benefits including anti-aging, brightening, and microbiome support.

Leading ingredient manufacturers, including BASF, Evonik Industries, and Croda International, launched multiple biotechnology-enabled actives in 2024, such as Evonik's Vecollage® Fortify L (vegan collagen polypeptide through precision fermentation) and NeoPlanta® Withania (COSMOS-certified adaptogenic skincare solution). Digital diagnostics and AI-driven personalization platforms are enabling ingredient customization based on DNA, skin microbiome, and real-time diagnostics—a segment expected to grow at 15% CAGR through 2033. This technological convergence enables faster time-to-market, ingredient transparency, and claim substantiation through clinical and analytical data, driving average selling price increases and repeat-purchase revenue for suppliers demonstrating measurable efficacy.

Restraints - Stringent Regulatory Frameworks and Compliance Complexity

The personal care ingredients market faces significant operational challenges due to increasingly stringent regulatory standards enforced by authorities, including the European Commission Cosmetics Directive (ECCD), U.S. Food and Drug Administration (FDA), and regional regulatory bodies.

In 2024, the European Commission issued four major regulatory amendments affecting cosmetic ingredients, including Regulation (EU) 2024/996, which prohibited the UV-filter 4-Methylbenzylidene Camphor (4-MBC) effective May 2025, and Regulation (EU) 2024/858, which added multiple nanomaterials to the prohibited substances lists. Additionally, Regulation (EU) 2024/2462 introduced restrictions on perfluorohexanoic acid (PFHxA) and related substances effective October 2026.

The UK's Cosmetic Products Regulations 2024 imposed restrictions on 64 CMR (Carcinogenic, Mutagenic, or Reprotoxic) substances and limited kojic acid use to facial and hand products at maximum 1% concentration.

These evolving compliance requirements necessitate continuous reformulation investments, extensive safety assessments, and robust documentation systems, creating substantial barriers to entry for smaller manufacturers and increasing time-to-market cycles. Multinational ingredient suppliers must navigate divergent regulatory landscapes across regions, complicating global product standardization and supply chain management.

Raw Material Price Volatility and Supply Chain Constraints

The market experiences persistent headwinds from fluctuating raw material prices and supply chain disruptions, particularly affecting petrochemical-derived ingredients and specialty botanical extracts. Oleochemical feedstock costs, essential for surfactants and emollients production, exhibit volatility correlated with crude oil prices and agricultural commodity markets.

Natural ingredient sourcing faces additional challenges, including seasonal availability, climate-dependent crop yields, and sustainability certification requirements that elevate procurement costs. The shift toward natural and organic formulations intensifies competition for limited supplies of certified organic botanicals, creating upward price pressure that compresses manufacturer margins.

Furthermore, geopolitical tensions, trade restrictions, and logistics bottlenecks continue to affect ingredient availability and lead times, particularly for specialty actives and biotechnology-derived ingredients that require cold-chain logistics. These structural cost pressures necessitate strategic supplier diversification, vertical integration investments, and development of bio-derived alternatives to mitigate dependency on traditional raw material sources.

Opportunities - Sustainable and Circular Economy Business Models

The accelerating transition toward sustainability-driven ingredient sourcing and circular economy principles presents transformative revenue opportunities for forward-thinking manufacturers. The carbon-neutral skincare ingredients market is growing substantially, reflecting consumer willingness to pay premiums for formulations aligned with environmental pledges.

Major ingredient corporations, including BASF, Lubrizol, and Clariant, are implementing Product Carbon Footprint (PCF) transparency initiatives, upcycled-byproduct extraction programs, and renewable-feedstock substitution to meet brand-owner sustainability targets.

The 2022 Lubrizol-Suzano partnership exemplifies this trend, focusing on eucalyptus-based biodegradable ingredients combining natural-based performance with renewable sourcing. Regulatory incentives, corporate ESG commitments, and consumer activism supporting eco-labeled products are creating structural demand shifts favoring suppliers with verified sustainability credentials, circular ingredient loops, and biodegradable formulation chemistries.

First-movers establishing green chemistry capabilities, bio-fermentation platforms, and waste-stream valorization technologies will capture disproportionate value in premium segments where sustainability premiums offset higher production costs.

Expansion of Multifunctional and Active Ingredient Segments

The market is witnessing robust demand growth for multifunctional ingredients that deliver multiple benefits, including cleansing, conditioning, preservation, and sensory enhancement within a single component, reducing formulation complexity and cost-per-product for brand owners.

Active ingredients, including peptides, botanicals, probiotics, and microbiome-friendly actives, are experiencing mid-to-high single-digit CAGR growth as consumers seek claim-driven, efficacy-backed products substantiated by clinical data. Conditioning polymers, rheology modifiers, and preservative-booster technologies enable brands to differentiate through enhanced texture, stability, and shelf life while maintaining a clean-label positioning. The antimicrobial cosmetic preserving market is driven by regulatory scrutiny, consumer safety awareness, and demand for natural-aligned preservation systems.

Broad-spectrum preservation technologies and blended delivery systems are expected to dominate in 2025, supporting longer shelf life without compromising product performance or regulatory compliance. Ingredient suppliers developing synergistic preservative systems, polymeric delivery platforms, and multifunctional actives addressing cost-in-use and regulatory efficiency will capture expanding market share across mass-market and premium segments.

Category-wise Analysis

Ingredients Insights

Surfactants dominate the ingredient category, accounting for 25% of market share in 2026, driven by their essential role in cleansing, foaming, emulsification, and solubilization across personal care formulations, including shampoos, body washes, and facial cleansers. Surfactants, including anionic (sodium lauryl sulfate), nonionic, and amphoteric formulations, reduce surface tension and enhance the user experience by producing abundant foam and effectively removing oil.

The clean beauty movement is driving substitution from petrochemical-derived surfactants toward natural alternatives such as sugar-based surfactants and amino acid derivatives, which offer milder skin profiles while maintaining functional performance. Natural surfactants are widely used in organic cosmetics for their diverse properties, including conditioning and special effects, and manufacturers are investing in biodegradable, renewable feedstock-based surfactant platforms.

Emollients represent the second-largest ingredient segment, holding over 20% market share in 2026, providing critical skin-conditioning benefits including moisturization, barrier protection, and sensory enhancement. The transition from traditional petrochemical-derived emollients toward bio-based alternatives, including plant oils, butters (shea, cocoa), and renewable esters, reflects consumer preferences for environmentally sustainable formulations without compromising efficacy or skin feel.

Color cosmetic ingredients are the fastest-growing segment, propelled by expanding color cosmetics applications, including foundations, lipsticks, eyeshadows, and mascara, driven by social media influence, beauty tutorial proliferation, and the inclusive beauty movement emphasizing diverse shade ranges. The segment benefits from ingredient innovation in pigments, film-formers, and multifunctional actives, enabling long-wear, transfer-resistant, and skin-beneficial cosmetic formulations that blur the line between makeup and skincare.

Source Insights

Natural ingredients dominate the market, with a 50% share in 2026, and are the fastest-growing segment, driven by the accelerating consumer shift toward clean beauty, sustainability, and ingredient transparency. The natural and organic cosmetics market is projected to surpass US$50 billion by 2033, far outpacing the growth of synthetic alternatives.

The remarkable expansion reflects rising health consciousness, concerns about synthetic chemical effects, and cultural affinity for plant-based remedies, particularly in India (Ayurvedic ingredients such as turmeric, neem, and aloe vera) and East Asia (K-beauty botanical formulations).

Natural ingredients command price premiums justified by clean-label appeal, sustainability certifications (COSMOS, Ecocert), and perceived safety advantages, with manufacturers willing to absorb higher sourcing costs to access rapidly growing consumer segments prioritizing environmental and health considerations.

Application Insights

Skin Care dominates application segments, accounting for over 45% of market share in 2026, positioned as the primary growth driver supported by the global skincare boom, anti-aging demographic trends, and cosmeceutical integration. The skincare ingredients market is expected to grow, driven primarily by younger consumer cohorts seeking clean-label formulations enriched with active ingredients that deliver hydration, barrier repair, and anti-aging benefits. Ingredient innovation targeting specific skin concerns, including acne treatment (salicylic acid, benzoyl peroxide), anti-aging (peptides, retinoids, antioxidants), and moisturization (hyaluronic acid, ceramides, glycerin), enables claim-driven product differentiation and premium pricing strategies.

Color cosmetics emerge as the fastest-growing application segment, experiencing accelerated adoption driven by social media beauty influence, makeup tutorial proliferation, inclusive beauty movement, and hybrid products combining cosmetic coverage with skincare benefits.

The segment drives demand for sophisticated pigments, long-wear polymers, film-formers, and skin-beneficial actives, enabling "skinification" of makeup through hybrid formulations that offer both aesthetic and functional skin benefits. Brands increasingly position color cosmetics as skincare delivery vehicles, incorporating anti-aging peptides, hydrating actives, and sun protection into foundation and concealer formulations, thereby expanding addressable markets and justifying premium pricing.

Regional Market Insights

North America Personal Care Ingredients Market: Share Analysis & Growth

North America represents a mature market characterized by high per capita spending, sophisticated distribution infrastructure, and innovation leadership. The U.S. personal care ingredients market is valued at US$4.5 billion in 2026 and projected to grow at a 4.5% CAGR through 2033. The region holds a strong position in the global skincare ingredients market, supported by robust consumer purchasing power, established cosmeceutical channels, and a healthy innovation pipeline.

The U.S. market demonstrates strength in dermatologically tested, clinically backed formulations addressing skin conditions and anti-aging concerns, with consumers exhibiting sophisticated ingredient literacy and a willingness to pay premiums for proven efficacy.

Key growth drivers include the clean beauty movement and the transformation from niche to mainstream positioning, with major retailers such as Sephora, Ulta Beauty, and Target dedicating significant shelf space to natural and sustainable brands. The antimicrobial-preserving market in the U.S. is driven by regulatory compliance requirements and consumer-led demand for safer formulations featuring high-purity actives in the dermocosmetic and premium categories. However, market maturity creates headwinds, including category saturation, intense competitive dynamics, and consumer price sensitivity during economic uncertainty. Regulatory frameworks, while providing consumer protection, impose compliance costs and reformulation requirements following FDA guidance updates and state-level restrictions (California Proposition 65).

Europe Personal Care Ingredients Market: Trend Insights & Opportunities

Europe is the second-largest market for personal care ingredients globally, expected to surpass US$5.5 billion by 2033, characterized by stringent regulatory harmonization, sophisticated sustainability expectations, and aging demographics driving anti-aging product demand. Germany leads the demand for personal care ingredients in Europe, accounting for over 1/5th of the regional demand in 2026, followed by France and the U.K.

In 2024 alone, four major regulatory amendments affected the permissibility of ingredients, underscoring ongoing vigilance for consumer safety and environmental protection. The inclusive beauty trend is gaining momentum across Europe, driving demand for broader shade ranges, diverse hair-type formulations, and culturally specific beauty solutions that address pan-European demographic diversity.

Demographic aging across Western Europe creates structural growth for anti-aging actives, with consumers aged 50+ representing high-value customer segments willing to invest significantly in evidence-based anti-aging treatments. Japan-style anti-aging sophistication is emerging, with European consumers demanding multi-benefit formulations supported by clinical efficacy data.

Regulatory environment impacts include accelerated removal of problematic chemistries (parabens, certain UV filters, microplastics) and mandated substitution with bio-derived, biodegradable alternatives, creating opportunities for sustainable ingredient suppliers.

Investment trends favor biotechnology platforms, upcycled ingredient technologies, and circular economy business models aligned with EU Green Deal objectives and corporate sustainability commitments.

Asia Pacific Personal Care Ingredients Market: Leadership & Regional Growth

Asia Pacific dominates as the leading region, accounting for over 35% of global market share in 2026, driven by a vast population base, rapid economic development, an expanding middle class, and rising beauty consciousness across diverse cultures.

The region serves as both the largest consumption market and dominant manufacturing hub, with competitive labor costs, robust chemical industry infrastructure, and integration into global supply chains, positioning countries including China, India, South Korea, and Japan as preferred sourcing locations for ingredient production and finished product manufacturing.

China's personal care ingredients market is valued at US$4.28 billion in 2026, representing the largest single-country opportunity within Asia Pacific. The market benefits from unprecedented growth in skincare consumption, driven by K-beauty influence, the emergence of C-beauty brands, and sophisticated consumer demand for efficacy-driven formulations featuring cutting-edge actives.

India emerges as the fastest-growing country in Asia Pacific, expected to achieve 8-10% growth between 2026 and 2033, driven by rising disposable incomes, accelerating urbanization, and a deep cultural affinity for Ayurvedic and herbal formulations. The Indian personal care ingredients market is likely to exceed US$2.5 billion by 2033. Key growth drivers include the expanding middle class demanding quality branded products, government support through the Ministry of AYUSH promoting herbal formulations, and successful domestic brands, demonstrating consumer acceptance of indigenous botanical ingredients.

Japan represents a mature, sophisticated market characterized by advanced adoption of anti-aging products, stringent formulation standards, and consumer preference for functional cosmetics that deliver measurable benefits.

Southeast Asia exhibits robust growth potential driven by young demographics, rising beauty consciousness influenced by social media and K-beauty trends, and increasing accessibility of international brands through e-commerce and modern retail expansion. Price sensitivity requires differentiated approaches combining aspirational branding with accessible pricing, creating opportunities for regional manufacturing leveraging local botanical ingredients and cost-efficient production platforms.

However, price sensitivity remains pronounced across tier-2 and tier-3 cities and Southeast Asian markets, necessitating value-oriented formulations and accessible price points.

Latin America Personal Care Ingredients Market: Vibrant and Dynamic

Latin America demonstrates a promising growth trajectory anchored by Brazil as the regional leader, with Brazil's personal care ingredients market expected to exceed US$2.5 billion by 2033.

The region benefits from rich biodiversity, providing access to unique botanical ingredients, including Amazonian extracts, Brazilian butters and oils (açaí, cupuaçu, babassu), and traditional formulation knowledge increasingly incorporated into modern personal care products.

Brazilian consumers exhibit sophisticated beauty consciousness and high per capita consumption of personal care products, creating substantial domestic demand supporting local ingredient production and formulation capabilities.

Key growth drivers include expanding middle class across Brazil, Mexico, Colombia, and Argentina, rising beauty awareness driven by social media influence and aspirational brand positioning, and increasing preference for natural formulations featuring regional botanical ingredients.

E-commerce penetration accelerates market access for independent brands and international players, overcoming traditional distribution challenges posed by geographic dispersion and a fragmented retail infrastructure. Regulatory harmonization efforts through Mercosur facilitate intra-regional trade and reduce compliance complexity for ingredient suppliers serving multiple countries.

Middle East & Africa Personal Care Ingredients Market: Fast-Growing Region

The Middle East & Africa region represents an emerging opportunity, with Africa identified as the fastest-growing territory, exhibiting double-digit growth projected over the next 5-10 years.

Growth drivers include rapid urbanization, an expanding young population with rising beauty consciousness, increasing disposable incomes in key markets such as Nigeria, South Africa, Kenya, and Ghana, and greater accessibility to international and regional beauty brands through modern retail and e-commerce channels.

Africa's emerging markets demonstrate nascent yet rapidly accelerating personal care adoption, driven by youth demographics (median age below 20 in many countries), smartphone penetration that enables social media beauty influence, and a rising middle class in urban centers. Textured hair care represents a significant opportunity, given the demographic predominance of textured and coily hair types that are underserved by global mass-market formulations.

Challenges include infrastructure limitations, fragmented distribution requiring localized approaches, economic disparities limiting access to premium products, and regulatory frameworks that vary significantly by country. Investment priorities emphasize distribution infrastructure, local manufacturing, reducing import dependency, sustainability partnerships with agricultural communities, and culturally relevant product development addressing specific hair and skin types prevalent in African populations.

The Middle East markets, particularly the UAE, Saudi Arabia, and Qatar, demonstrate high per capita spending on premium personal care products, driven by affluent consumer segments, tourism infrastructure, and cultural emphasis on personal grooming and fragrance.

Demand skews toward luxury positioning, halal-certified formulations, and products addressing specific regional needs, including extreme climate conditions, modest beauty preferences, and cultural fragrance traditions. Ingredient opportunities include halal certification becoming essential for market access, formulations addressing hot-climate challenges (high humidity, sun exposure, air-conditioning effects), and fragrance-forward products reflecting regional preferences for strong, long-lasting scents.

Competitive Landscape

The personal care ingredients market exhibits moderate to high concentration, with leading multinational chemical corporations commanding significant market shares through diversified product portfolios, global distribution networks, technological leadership, and long-standing customer relationships.

Top-tier suppliers, including BASF SE, Croda International, Evonik Industries, Dow, Ashland Inc., Clariant AG, LANXESS AG, and Solvay, collectively represent approximately 35-40% of global market value, benefiting from vertical integration, R&D scale advantages, and comprehensive ingredient portfolios spanning surfactants, emollients, active ingredients, and functional additives.

The competitive landscape is evolving toward consolidation through strategic M&A, capability-building in biotechnology and sustainable ingredients, and vertical integration to secure raw material supplies and downstream formulation expertise.

Strategic Developments

- In 2025, Dow, a leader in specialty chemicals, is introducing four new personal care ingredients and the “Beauty in Harmony” concept collection at in-cosmetics Asia 2025, showcasing its commitment to science-driven solutions for beauty brands and consumers in the Asia Pacific region.

- In 2024, Clariant AG acquired Lucas Meyer Cosmetics, a leading supplier of high-value cosmetics and personal care ingredients, from IFF for US$810 million. The acquisition will support Clariant's growth in high-margin specialty chemicals and consumer markets driven by increasing demand for natural and sustainable products.

- In 2024, Symrise formed a joint venture with Virchow Group in India to produce personal care ingredients. This partnership aims to enhance Symrise's position as a top supplier of high-quality personal care solutions, including multifunctional protection ingredients and advanced UV filters.

Companies Covered in Personal Care Ingredients Market

- BASF SE

- LANXESS AG

- Clariant AG

- Croda International Plc

- Dow Chemicals

- Stephan

- Solvay S.A.

- DSM-Firmenich

- Momentive Performance Chemicals

- Wacker AG

- IFF

- Ashaland Inc.

- ADEKA Corporation

- Syensqo

- Evonik Industries

Frequently Asked Questions

The global personal care ingredients market was valued at US$22.5 billion in 2026 and is projected to reach US$32.3 billion by 2033, growing at a CAGR of 5.3%. This growth is driven by rising demand for natural ingredients, skincare sophistication, and biotechnology-enabled formulations.

Surfactants lead with 25% market share, followed by emollients at 23%, while color cosmetic ingredients represent the fastest-growing segment. Growth drivers include multifunctional formulations, social media influence, and the clean beauty movement, expanding color cosmetics applications.

Natural ingredients account for 50% market share in 2026 and represent the fastest-growing segment due to consumer preference for clean beauty, environmental sustainability concerns, and regulatory support.

Asia Pacific dominates with over 35% global share, particularly China and India. Africa is identified as the fastest-growing region with double-digit growth projected over the next 5-10 years, while North America and Europe remain mature, established markets.

BASF SE, Croda International, Dow, LANXESS AG, Evonik Industries, Ashland Inc., and Clariant AG are market leaders, supported by companies including Solvay, Lonza Group, and Symrise AG. These firms compete through R&D innovation, sustainability credentials, and strategic acquisitions, strengthening specialty ingredient portfolios.