- Consumer Goods

- Paper Frames Market

Paper Frames Market Size, Share, and Growth Forecast, 2026- 2033

Paper Frames Market by Product Type (Single-Photo Paper Frames, Multi-Photo / Collage Paper Frames, Decorative & Designer Paper Frames, and Customized / Personalized Paper Frames), By Application (Home Decor, Commercial & Office Display, Events & Gifting, Educational & Institutional Use, and Advertising & Promotional Displays), By Distribution Channel, Offline Retail Stores, Online Platforms, Wholesale / Bulk Supply), and Regional Analysis for 2026 – 2033.

Paper Frames Market Size and Trends Analysis

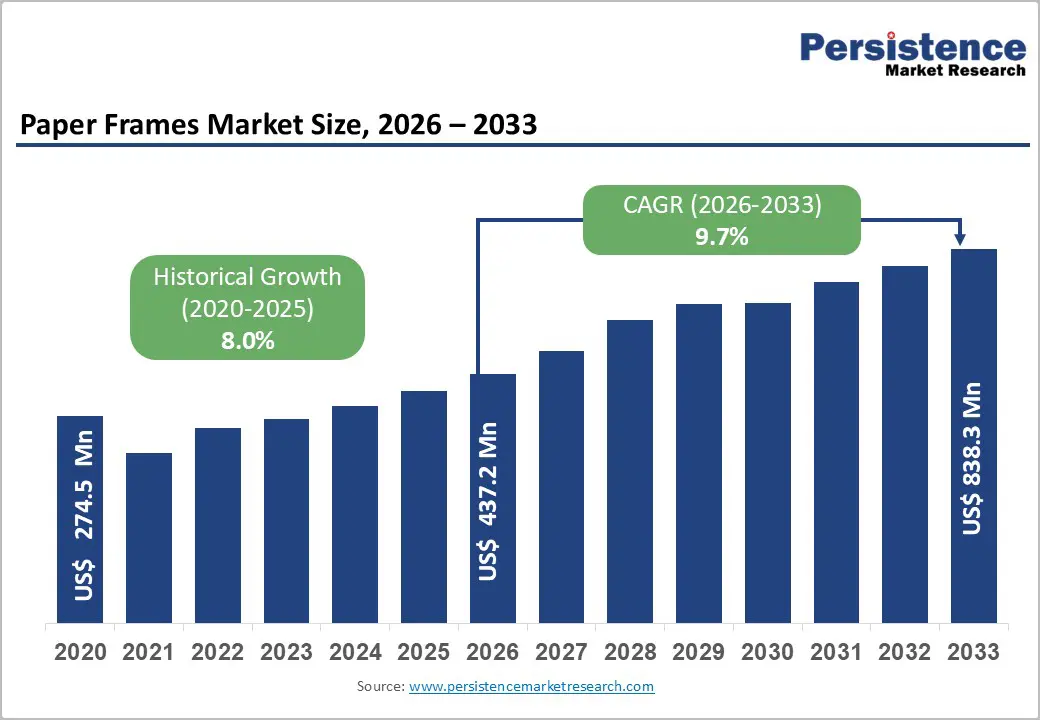

The global paper frames market size was valued at US$ 274.5 Million in 2020 and is projected to reach US$ 437.2 Million by 2026 and US$ 838.3 Million by 2033, growing at a CAGR of 9.7% between 2026 and 2033. This robust growth trajectory reflects accelerating consumer demand for decorative and functional framing solutions across residential, commercial, and institutional applications.

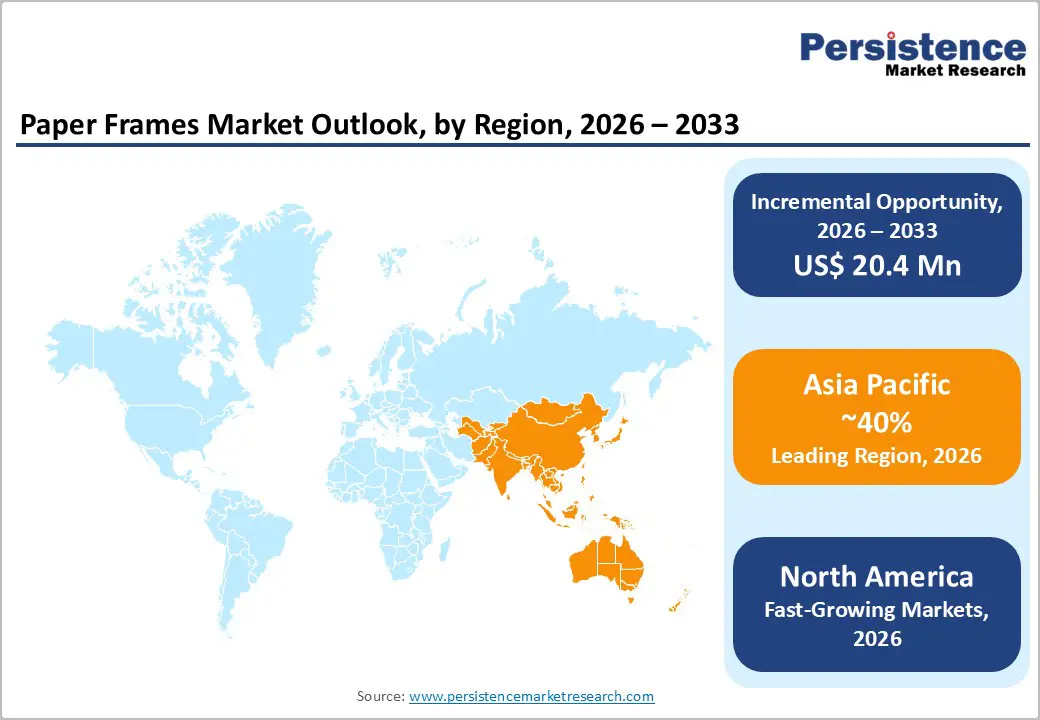

The market's expansion is underpinned by three primary drivers: rising disposable incomes driving home aesthetic investments, digital commerce acceleration expanding market accessibility, and growing consumer appetite for personalized and customizable products. North America and Asia-Pacific represent the critical growth engines, with Asia-Pacific commanding above 40% revenue share while North America demonstrates the highest growth velocity at 10.5% CAGR. The market exhibits structural maturation with clear segment leadership while simultaneously generating high-growth niches in customized solutions and commercial display applications.

Key Industry Highlights:

- Segment Leadership and Growth: Single-photo paper frames dominate with 45%+ revenue share, while multi-photo and collage frames represent the fastest-growing category at 10.8% CAGR; home decor applications command 45%+ share while commercial and office display applications are the fastest-growing segment at 10.9% CAGR, indicating market shift toward professional and specialized applications.

- Distribution Channel Transformation: Offline retail stores retain 55%+ market share as the dominant channel, while online platforms are the fastest-growing distribution channel at 10.6% CAGR, reflecting structural shift toward e-commerce and digital customization services particularly pronounced in Asia-Pacific and North America.

- Regional Growth Dynamics: Asia-Pacific dominates with 40%+ global revenue share, while North America demonstrates the highest growth rate at 10.5% CAGR, driven by rising disposable incomes, accelerating digital commerce, and consumer preference for personalized and customizable decorative solutions across both regions.

- Market Drivers and Opportunities: Rising home décor investment, e-commerce proliferation, personalization trends, and sustainability regulatory mandates are primary growth catalysts; multi-photo frames (10.8% CAGR), commercial applications (10.9% CAGR), and emerging market penetration represent highest-potential growth opportunities.

- Competitive Positioning: The market is moderately fragmented with Larson-Juhl and Nielsen Bainbridge leading the premium segment, regional manufacturers dominating Asia-Pacific, and digital specialists capturing growing e-commerce share; differentiation increasingly driven by sustainability certifications, customization capabilities, and digital consumer experiences rather than traditional product features.

| Key Insights | Details |

|---|---|

| Paper Frames Market Size (2026E) | US$ 437.2 Mn |

| Market Value Forecast (2033F) | US$ 838.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 9.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.0% |

Market Dynamics

Key Growth Drivers

Escalating Consumer Spending on Home Aesthetics and Personalization

Rising disposable incomes and elevated consumer focus on home environment enhancement constitute the primary market catalyst. Data from Fortune Business Insights indicates the global home decor market reached US$ 747.75 billion in 2024 and is projected to expand at a 4.58% CAGR through 2032, creating significant spillover demand for complementary products including picture and paper frames. This trend gained particular momentum post-pandemic, as consumers reallocated expenditure toward home improvement and interior customization rather than travel and entertainment. The personalized gifts market, which encompasses photo frames and customized home décor, is projected to grow from US$ 29.85 billion in 2024 to US$ 57.19 billion by 2033 at a 9.7% CAGR, directly aligning with paper frame market growth trajectories. Photo frames and home décor articles comprise the fastest-growing subsegment within personalized gifts, expanding at 7.97% CAGR, demonstrating that consumers increasingly view framed displays as essential components of curated personal spaces. This behavioral shift is particularly pronounced in urban demographics across North America and Asia-Pacific, where cultural emphasis on aesthetic expression and social media-driven home presentation norms drive disproportionate spending on decorative solutions.

Market Restraining Factors

Raw Material Cost Volatility and Supply Chain Constraints

The paper frames industry faces structural exposure to pulp and recovered fiber price fluctuations. Recent market analysis indicates that pulp and recovered paper exhibit greater price volatility than finished paperboard, with pulp prices declining 10.8% in recent periods while recovered paper increased 4.5%, creating unpredictable cost structures for manufacturers. Furthermore, paper board prices in key regions reached US$ 0.23/kg in Northeast Asia, US$ 0.25/kg in Europe, and US$ 0.26/kg in India as of December 2025, with prices rising 2.6% during 2025 following two years of decline. Energy costs, particularly in European and Asian manufacturing hubs, remain elevated relative to pre-pandemic baselines. These cost pressures disproportionately impact smaller manufacturers and artisanal producers with limited pricing power, constraining margins and reducing product diversification capability. Supply chain fragmentation—particularly post-pandemic logistics disruptions—further elevates working capital requirements for inventory management.

Paper Frames Market Trends and Opportunities

Commercial and Institutional Display Applications

The commercial display market reached US$ 54.45 billion in 2024 and is projected to expand at 7.3% CAGR through 2032, with retail, office, and hospitality sectors accounting for the majority of growth. Within this macro-market, commercial and office display applications represent the fastest-growing paper frames segment at 10.9% CAGR. Corporate branding, employee recognition programs, heritage displays, and event memorabilia create substantial bulk ordering opportunities. Museums, galleries, and educational institutions require archival-quality framing solutions with growing emphasis on sustainable materials. The estimated addressable opportunity for paper frames in commercial segments reaches approximately US$ 100-150 million globally, with North America and Western Europe commanding 65% share. Professional framing services that integrate paper frames with premium positioning and customization capabilities are expanding market penetration in this segment

Paper Frames Market Insights and Trends

Product Type Insights

Single-photo dominance meets rapid growth of multi-photo paper frames globally

The global paper photo frames market shows a clear contrast between a mature, high-volume core segment and a fast-expanding premium niche. Single-photo paper frames remain the dominant product type, accounting for over 45% of total revenue. Their leadership is driven by enduring consumer preference for classic framing formats used in homes, offices, and professional settings. Standard sizes such as 4×6, 5×7, and 8×10 inches enable large-scale, cost-efficient manufacturing and streamlined distribution. Affordable pricing, typically ranging from US$3–15, supports widespread adoption across income groups. However, this segment reflects structural maturity, with steady but modest growth of around 5–6% CAGR. Intense competition among branded retailers and mass manufacturers limits margin expansion, pushing players toward geographic expansion and channel diversification rather than product-led growth.

In contrast, multi-photo and collage paper frames represent the fastest-growing segment, expanding at a robust 10.8% CAGR. Growth is fueled by social media-driven personalization, gifting culture, and modern interior design trends such as gallery walls. Higher design complexity enables premium pricing and attractive gross margins of 45–60%. Digital customization tools and e-commerce visualization features further accelerate demand by transforming frames from functional products into creative, experience-driven purchases. Asia-Pacific and North America, particularly urban markets, are key growth engines for this segment.

Application Insights

Home decor dominance with accelerating commercial demand reshaping framing applications

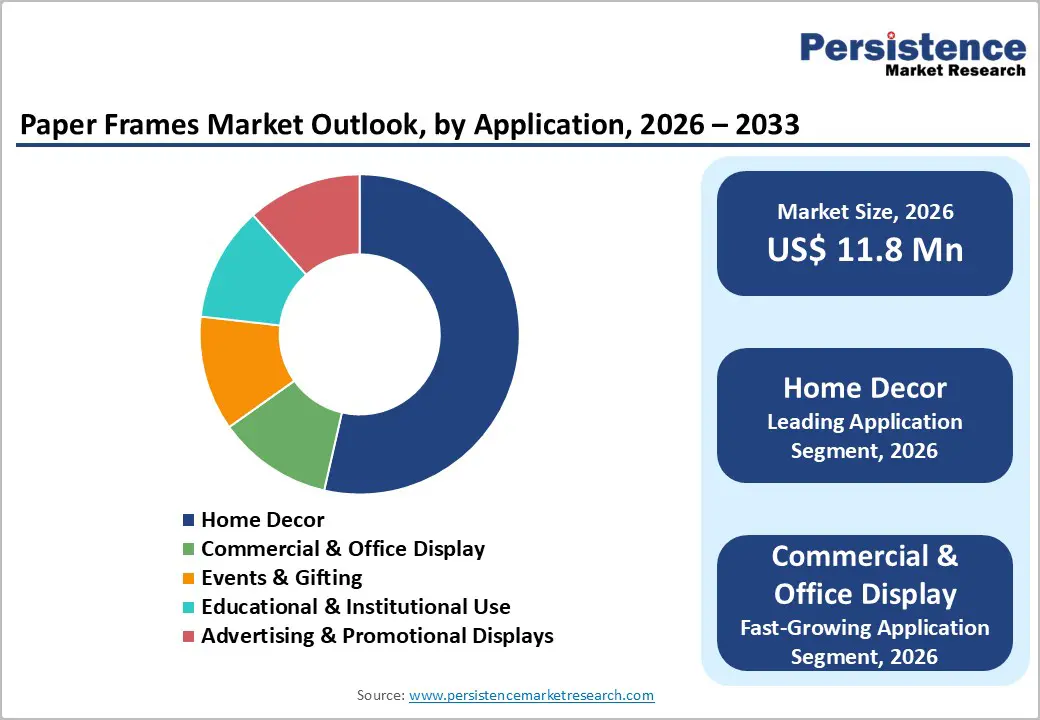

Home décor remains the cornerstone application, accounting for over 45% of total revenue and providing consistent, volume-driven demand across regions and consumer segments. This segment spans residential wall art, shelf accents, bedroom and living room displays, and aspirational interior personalization. Growth in the global home décor market, projected to reach US$1.098 trillion by 2032, creates strong structural tailwinds for frame-based products. Frames function as flexible décor elements that complement furniture, textiles, and lighting, allowing consumers to refresh interiors every three to five years at relatively low cost. Demand is supported by stable pricing, predictable seasonal cycles such as holidays and home refresh periods, and efficient distribution through mass retailers, specialty stores, and e-commerce platforms. Product innovation emphasizes design versatility, sustainability, and alignment with evolving trends including minimalism, maximalism, and cultural fusion aesthetics.

In contrast, commercial and office display applications represent the fastest-growing segment, expanding at a 10.9% CAGR. Growth is driven by corporate branding, employee recognition, workplace aesthetics, and event memorabilia. Organizations increasingly view enhanced office environments as tools for talent attraction and retention, particularly in professional services sectors. This segment benefits from bulk procurement, recurring contracts, and customization-led differentiation, supporting pricing premiums of 20–40% over consumer products. With penetration still limited among SMEs and emerging markets, commercial applications offer a substantial long-term growth runway.

Regional Insights and Trends

Asia-Pacific leads global paper frames market with scale and speed

Asia-Pacific dominates the global paper frames market, accounting for over 40% of total revenue and exhibiting the fastest growth momentum worldwide. The regional market is currently valued at approximately US$ 170–220 million and is projected to surpass US$ 400 million by 2033, supported by strong domestic consumption and export-oriented manufacturing. China serves as the region’s primary production and export hub, leveraging its well-established paper manufacturing infrastructure, cost-efficient labor base, and deeply integrated supply chains. These advantages enable large-scale output while maintaining competitive pricing in global markets.

India represents the fastest-growing consumer market within the region, driven by rapid urbanization, expanding middle-class disposable incomes, and accelerating adoption of e-commerce. The personalized gifting segment in India is growing at a CAGR of 26.28%, significantly boosting demand for customized paper frames. Japan, in contrast, reflects stable and mature demand, with consumers favoring premium-quality, minimalist, and aesthetically refined frame designs aligned with local cultural preferences. Southeast Asian countries such as Thailand, Vietnam, and Indonesia contribute incremental growth through rising digital retail penetration and increasing gifting culture.

Key growth drivers include rapid urban development, rising purchasing power, and the faster growth of online retail compared to traditional stores, particularly in China and India. Online customization platforms are steadily gaining share by offering convenience and design flexibility. While tightening sustainability regulations across the region increase compliance costs, they are also accelerating innovation in eco-friendly materials and processes, strengthening long-term market competitiveness.

North America leads global paper frames market through personalization demand

The North American paper frames market represents a US$120–150 million opportunity and demonstrates the highest regional growth momentum, expanding at an estimated CAGR of 10.5%. The United States accounts for the majority of demand, supported by a robust home décor market projected to reach US$305.51 billion by 2032, which significantly boosts downstream demand for framing and wall display solutions. A strong cultural preference for personalization and visual storytelling underpins market growth, with wall art and decorative framing accounting for nearly 75% of the U.S. wall décor segment.

The personalized gifts market in North America is growing at 8–10% CAGR, with photo frames emerging as the fastest-growing subcategory due to emotional value, customization options, and social media–driven gifting trends. A highly developed distribution ecosystem further strengthens market performance, combining large craft retailers such as Michaels and Hobby Lobby, premium framing specialists like Larson-Juhl and Nielsen Bainbridge, and powerful e-commerce platforms including Shutterfly, Etsy, Zazzle, and Vistaprint.

Sustainability regulations, including Extended Producer Responsibility initiatives, are accelerating adoption of recyclable materials and eco-friendly manufacturing. Additionally, commercial demand from hospitality, healthcare, and corporate offices is expanding. Overall, investment opportunities are strongest in premium customization, sustainable paper-based materials, and B2B framing solutions tailored to mid-market enterprises.

Paper Frames Market Competitive Landscape

The paper frames market is moderately fragmented, with no single player commanding dominant global share. Larson-Juhl and Nielsen Bainbridge lead the premium market segment, with Larson-Juhl reporting revenue exceeding US$ 300 million annually, though these figures encompass broader framing and art materials beyond paper frames specifically. Huahong Holding Group, Intco Framing, Dunelm, and Pottery Barn represent significant mid-tier competitors with established distribution networks and brand recognition. The competitive structure reflects regional variation: North America is relatively consolidated with Larson-Juhl, Nielsen Bainbridge, and Michaels commanding substantial share; Europe supports multiple heritage manufacturers and artisanal producers; Asia-Pacific exhibits high fragmentation with local manufacturers dominating regional markets and specialized exporters serving global channels.

Entry barriers are moderate, characterized by capital requirements for manufacturing equipment and working capital, regulatory compliance costs (particularly sustainability certifications), and distribution channel access. Brand recognition provides pricing power in premium segments, but differentiation is primarily design-driven and easily replicated. Online retail accessibility reduces distribution barriers, enabling new entrants to reach consumers through e-commerce without traditional retail relationships. The market exhibits high price sensitivity in mid-market segments, limiting differentiation and compressing margins for undifferentiated products. Consolidation activity remains limited; the most notable strategic transaction involved Crescent Cardboard Company acquiring Nielsen Bainbridge's US operations, reflecting consolidation within premium professional framing segments rather than mass-market commoditization

Key Industry Developments

In October 2025, Aura Launches $499 Cordless E-Paper Photo Frame With 3-Month Battery Life

Companies Covered in Paper Frames Market

- Bluecat Paper LLP

- Nazeer Handmade Paper

- Ashrafi International

- Essence Ecocrafts

- Otto International

- Pineapple Homes Pvt. Ltd.

- Spiritual Soul

- Camelon Exports

- Himalayan Paper Works

- Shenzhen Xinsichuang Arts & Crafts Co., Ltd.

- Other Market Players

Frequently Asked Questions

The Paper Frames market is estimated to be valued at US$ 437.2 Mn in 2026.

The principal factor driving demand for picture/photo frames (including paper or eco-friendly variants) is consumers’ increasing interest in home personalization, interior decoration, and displaying memories or artwork.

In 2026, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global Paper Frames market.

Among applications, home decor has the highest preference, capturing beyond 45% of the market revenue share in 2026, surpassing other applications.

Bluecat Paper LLP,Nazeer Handmade Paper, Ashrafi International, Essence Ecocrafts Otto International, and Pineapple Homes Pvt. Ltd. There are a few leading players in the Paper Frames market.