- Smart Packaging

- Paper Printing Market

Paper Printing Market Size, Share, and Growth Forecast, 2025 - 2032

Paper Printing Market By Paper Type (Coated Papers, Uncoated Papers), Application (Packaging Printing, Label Printing), End-user Industry, and Regional Analysis for 2025 - 2032

Paper Printing Market Size and Trends Analysis

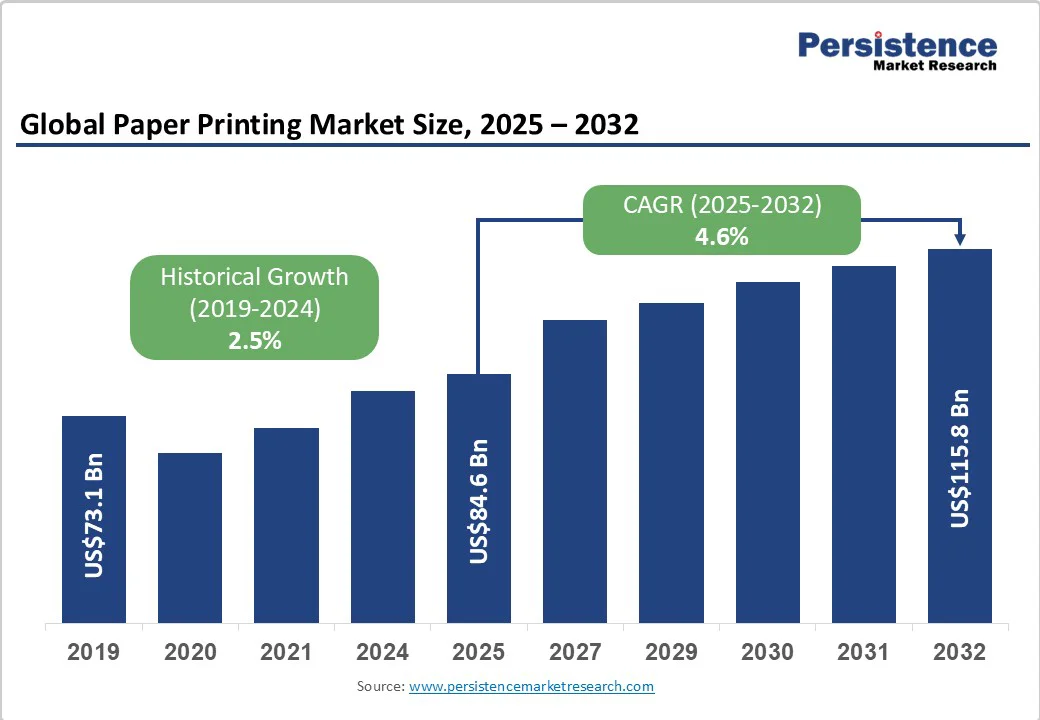

The global paper printing market size is expected to reach US$84.6 billion by 2025. It is expected to reach US$115.8 billion by 2032, growing at a CAGR of 4.6% during the forecast period from 2025 to 2032, driven by the surge in packaging and labeling applications, the substitution of plastics with fiber-based materials under sustainability regulations, and advancements in digital press technologies that enable efficient short-run and customized print jobs.

While traditional publishing segments are contracting, packaging and specialty papers are absorbing this shift, leading to a healthier and more diversified market structure. Firms integrating recycling and digital printing capabilities are expected to capture the strongest margins over the forecast period.

Key Industry Highlights

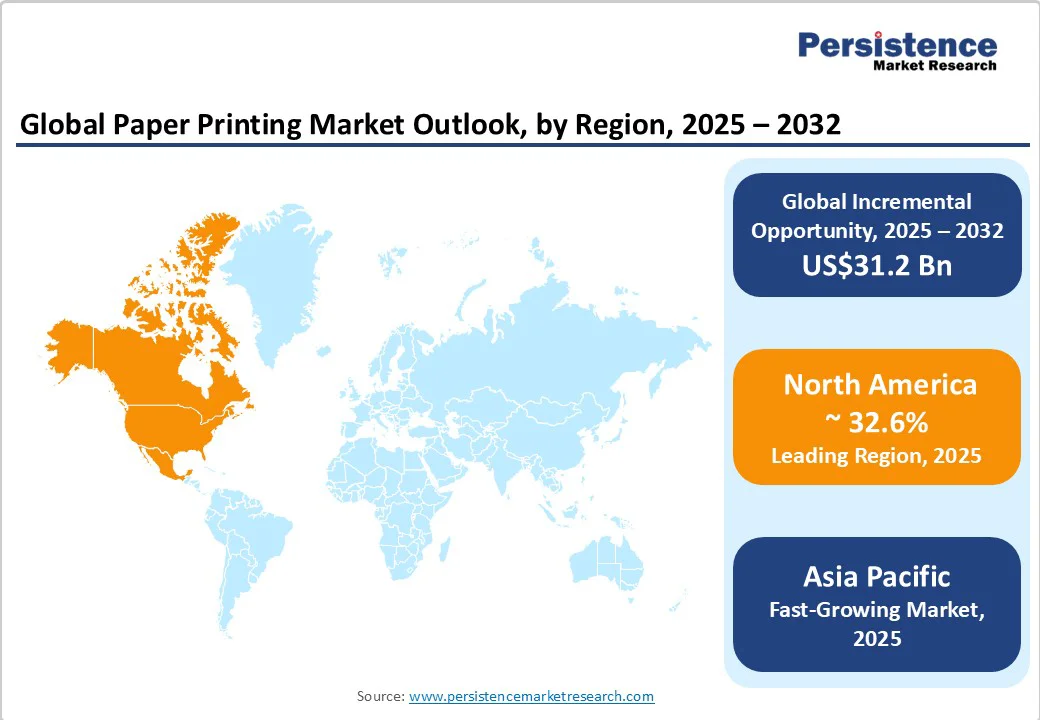

- Leading Region: North America accounts for approximately 32.6% of global market revenue, driven by large-scale packaging, FMCG demand, and digital printing adoption.

- Fastest-growing Region: Asia Pacific projected CAGR 6.2% from 2025 to 2032, led by China, India, and ASEAN nations due to e-commerce growth and industrial packaging expansion.

- Investment Plans: Capacity expansions for recycled fiber, digital press installations, and vertical integration in packaging solutions across North America, Europe, and Asia Pacific.

- Dominant Category 1: Packaging Printing represents 57% of the total market revenue, driven by retail, e-commerce, and food & beverage industries.

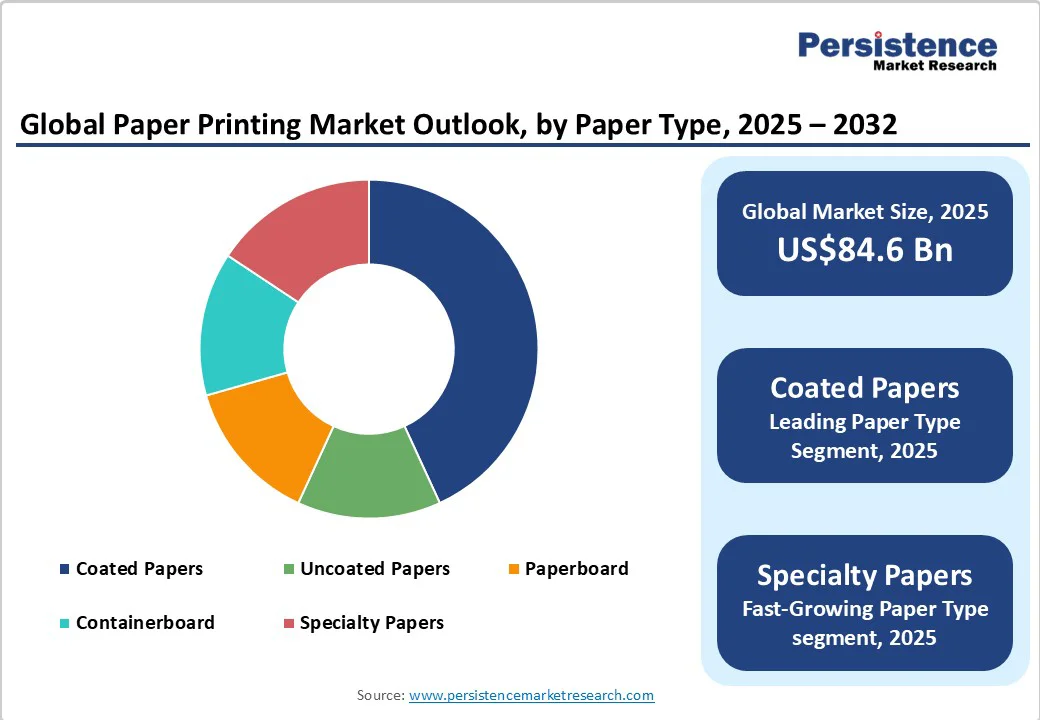

- Leading Category 2: Coated papers, approximately 44% market share in 2025, due to superior print quality and use in premium packaging and commercial print applications.

| Key Insights | Details |

|---|---|

| Paper Printing Market Size (2025E) | US$84.6 Bn |

| Market Value Forecast (2032F) | US$115.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Packaging and E-Commerce Applications

Packaging printing has become the most significant demand driver in the paper printing industry. The rapid expansion of e-commerce and fast-moving consumer goods (FMCG) sectors has increased the need for printed corrugated boxes, folding cartons, and high-quality labels.

Packaging applications account for over half of the total market revenue, as companies prioritize branding, sustainability, and product differentiation. The shift toward heavier grades and premium finishes generates higher margins for converters and papermakers. Integrated players that provide both paper substrate and printed packaging services benefit most from this volume and value synergy.

Regulatory Support for Fiber-Based Packaging

Government regulations worldwide are increasingly promoting recyclable, fiber-based packaging solutions. The European Union’s Packaging and Packaging Waste Regulation (PPWR) and Extended Producer Responsibility (EPR) frameworks have accelerated the move toward recyclable and compostable materials.

These policies are compelling brand owners to transition from plastic packaging to paper-based alternatives. In addition, mandates on a minimum recycled content levels create steady demand for recycled fiber. As a result, papermakers that can deliver certified recycled content and verifiable sustainability credentials enjoy growing customer loyalty and premium pricing advantages.

Advancements in Digital Printing Technologies

The adoption of digital and inkjet printing technologies has transformed the operational efficiency of paper printing. Digital presses allow for on-demand production, reduced waste, and mass customization. Print providers can now execute short runs profitably, catering to promotional, event-based, or personalized packaging.

Automation, improved color calibration, and integration with e-commerce platforms enhance overall print quality and delivery speed. This technological shift is expanding the customer base beyond traditional publishing, fueling growth in sectors such as direct-to-consumer packaging and on-demand printing services.

Barrier Analysis - Declining Demand for Graphic and Publishing Papers

The continued digitization of media and communication has led to a secular decline in graphic and writing paper consumption, particularly in developed economies. The shift to digital advertising, online news, and electronic documentation reduces demand for traditional printing papers.

This structural contraction has caused underutilization of certain paper mills and pricing pressure in the commercial print segment. As publishers and print advertisers migrate online, the offset printing segment experiences margin compression and lower order volumes.

Volatility in Raw Materials and Energy Costs

Paper production is highly sensitive to fluctuations in pulp, energy, and freight costs. Sharp increases in pulp prices or global shipping rates can significantly erode profit margins for both paper manufacturers and printing companies.

Smaller converters and print houses often face liquidity challenges during periods of volatility, which limit their ability to modernize equipment or adopt sustainable processes. Persistent cost fluctuations also complicate long-term pricing strategies and contract negotiations with downstream customers.

Opportunity Analysis - Premiumization of Packaging and Brand Differentiation

As brands compete for consumer attention, high-quality, visually distinctive packaging is emerging as a key marketing tool. The growing popularity of luxury, eco-friendly, and limited-edition packaging provides new revenue opportunities for papermakers and converters.

Premium packaging papers, embossed finishes, metallic inks, and hybrid printing techniques command higher margins. The segment for high-end packaging is estimated to grow at a CAGR of over 6%, representing a multi-billion-dollar opportunity by 2032. Firms that invest in advanced finishing capabilities and design collaboration platforms are expected to benefit the most.

Circular Economy and Recycled Fiber Integration

The transition toward a circular economy creates opportunities across the paper value chain. Recycled paper collection, fiber reprocessing, and traceable material certification are becoming lucrative service lines.

Manufacturers that establish closed-loop recycling systems and invest in de-inking and fiber-purification technologies gain long-term supply security. Global demand for certified recycled paper is projected to rise steadily through 2032, particularly in Europe and North America, where regulations are increasingly mandating higher recycled content thresholds.

Growth in Emerging Markets

Emerging economies in Asia, Latin America, and Africa offer strong growth prospects as literacy rates, consumer goods consumption, and demand for retail packaging rise. Rapid urbanization and the expansion of middle-class populations are driving investments in packaging, education, and commercial printing infrastructure.

Local governments are supporting domestic pulp and paper production to reduce reliance on imports. These factors collectively make emerging markets a strategic frontier for global paper printing companies to expand into.

Category-wise Analysis

Paper Type Insights

Coated papers continue to dominate, accounting for approximately 44% of the market share in 2025, due to their superior print clarity, smoothness, and durability. These papers are ideal for applications requiring high-quality graphics and precise color reproduction, such as magazines, luxury catalogues, premium brochures, and packaging for cosmetics or electronics.

Coated papers provide a higher price per ton compared to uncoated grades, as brands and advertisers are willing to pay for enhanced visual appeal and finish. For example, high-end cosmetic brands such asL’Oréal and Estée Lauder frequently use coated paper for printed inserts, promotional materials, and packaging sleeves.

Specialty papers, including barrier papers, label stock, security papers, and anti-counterfeit papers, are witnessing the fastest growth. This expansion is driven by rising demand for food-safe packaging, pharmaceutical labeling, and secure documentation. For instance, barrier papers with grease- or moisture-resistant coatings are increasingly used for takeaway food packaging by chains such as McDonald’s and Starbucks, replacing conventional plastic wraps.

Security papers are used for passports, certificates, and legal documents, while eco-friendly label papers are becoming integral in sustainable beverage packaging, such as beer and juice bottles. The segment is projected to grow at a CAGR of over 6% through 2032, supported by regulatory compliance and sustainability trends.

Application Insights

Packaging is the largest application segment, accounting for roughly 57% of total revenue. Paper-based packaging is increasingly replacing plastics due to environmental regulations, consumer preference, and cost-effectiveness. The growth is particularly strong in retail, FMCG, and e-commerce industries, where printed cartons, boxes, and wraps serve both functional and branding purposes.

Examples include Amazon’s paper shipping boxes, Unilever’s folded paper cartons for personal care products, and Nestlé’s eco-friendly food packaging. These applications require papers that can be printed in high resolution, withstand handling, and integrate with automated packing lines, making packaging the market’s most significant revenue contributor.

Label and flexible packaging are expanding rapidly due to food safety regulations, traceability requirements, and the rise of e-commerce. QR-coded labels, tamper-evident packaging, and customizable printed inserts are now standard across sectors such as pharmaceuticals, beverages, and logistics.

For instance, Heineken uses paper-based, peelable labels for promotions and limited editions, while FedEx and UPS rely on printed shipping labels for tracking and compliance. The shift toward sustainable, recyclable films and hybrid paper-laminates further accelerates this segment’s growth, with a projected CAGR exceeding 6.5% through 2032.

Regional Insights

North America Paper Printing Market Trends - Sustainable Graowth in Packaging and Digital Printing

North America remains one of the most mature yet profitable regions, accounting for approximately 32.6% of global market revenue. The U.S. dominates regional demand owing to its well-established packaging, publishing, and promotional printing industries.

The market benefits from robust consumer spending, high advertising budgets, and widespread adoption of sustainable materials. Extended Producer Responsibility (EPR) laws emerging in states such as California and Oregon are reinforcing recycled content adoption. Investments in digital printing infrastructure and automation are enabling shorter production runs and faster turnaround times.

Recent developments include International Paper’s April 2025 expansion of its recycled containerboard facility in Georgia, which enhances its sustainable packaging output, and Smurfit Kappa WestRock’s 2024 launch of a digital printing line for corrugated boxes in Ohio, aimed at personalized e-commerce packaging.

Key companies, such as International Paper, Smurfit Kappa, and Graphic Packaging, are focusing on vertical integration and sustainability certifications. The market outlook remains positive, with steady revenue growth projected at around 4-5% annually through 2032.

Europe Paper Printing Market Trends - Eco-Driven Innovation and Packaging Consolidation

Europe is a global leader in sustainable paper printing solutions, supported by stringent environmental regulations and innovative packaging design practices. Countries, including Germany, the U.K., France, and Spain, collectively account for a substantial share of the market. Germany leads in industrial and retail packaging, while the U.K. and France excel in luxury and creative packaging applications.

The European Union’s PPWR legislation is accelerating the transition from plastic to paper packaging and driving investment in recyclable mono-materials. Industry consolidation is evident, with players such as Mondi, DS Smith, and Stora Enso expanding their production capacities for specialty papers.

Recent developments include DS Smith’s March 2025 acquisition of a Spanish folding carton facility, aimed at increasing recycled paper usage, and Mondi’s April 2025 launch of mono-material paper pouches in Germany, enhancing sustainable flexible packaging offerings.

Asia Pacific Paper Printing Market Trends - Rapid Expansion Fueled by E-Commerce and Sustainability

Asia Pacific is the fastest-growing regional market, supported by large-scale manufacturing, strong domestic consumption, and favorable government initiatives. China remains the global production hub, accounting for a significant portion of global paper output.

Japan excels in specialty and technological innovation, while India and ASEAN countries are emerging as high-potential markets due to booming e-commerce and demand for food packaging. Rising income levels, rapid industrialization, and urbanization are encouraging the establishment of new printing and packaging facilities.

Recent developments include Nine Dragons Paper Holdings’ 2024 commissioning of a recycled fiber production line in Guangdong, China, and Oji Holdings’ 2025 launch of high-quality digital printing services in Tokyo for specialty packaging.

The introduction of plastic-ban policies across several Asian economies has accelerated the shift toward paper-based solutions. The region’s market is projected to grow at a CAGR exceeding 6%, with foreign investments focused on recycled fiber facilities, digital press technologies, and sustainable packaging innovations.

Competitive Landscape

The global paper printing market is moderately consolidated, with leading producers controlling a large portion of overall capacity. Major players such as Smurfit WestRock, International Paper, Mondi, and UPM hold substantial influence due to vertical integration across pulp, paper, and packaging operations.

The mid-tier segment remains fragmented, comprising numerous regional converters and specialty printers serving niche applications. Continuous consolidation through mergers and acquisitions is reshaping competitive positioning and increasing pricing power for integrated firms.

Leading companies focus on vertical integration, sustainability leadership, and technological innovation. Strategies include securing recycled fiber sources, investing in advanced digital printing, and expanding into emerging markets. Competitive differentiation is increasingly based on offering complete solutions from raw fiber to finished printed packaging.

Key Industry Developments

- In April 2025, International Paper announced the expansion of its Recycled Containerboard Line in Georgia, aiming to increase sustainable packaging capacity for North America’s FMCG and e-commerce sectors.

- In March 2025, DS Smith acquired a folding carton facility in Spain, enhancing its production of recycled paperboard cartons for food and consumer goods packaging.

- In April 2025, Mondi launched EcoFlex Mono-Material Pouches in Germany, designed for recyclable flexible packaging in food and beverage applications.

Companies Covered in Paper Printing Market

- International Paper

- Smurfit WestRock

- Mondi plc

- Stora Enso

- DS Smith

- UPM-Kymmene

- Oji Holdings

- Sappi Limited

- Nine Dragons Paper Holdings

- Nippon Paper Group

- Georgia-Pacific

- Graphic Packaging Holding Company

- Klabin S.A.

- Asia Pulp & Paper (APP)

- Huhtamaki Oyj

- WestRock Company

- Clearwater Paper Corporation

- Burgo Group

- Mitsubishi Paper Mills

- Rengo Co., Ltd.

Frequently Asked Questions

The paper printing market size in 2025 is estimated at US$84.6 Billion.

The paper printing market is projected to reach US$115.8 Billion by 2032, reflecting steady growth across packaging, commercial, and specialty printing applications.

Key trends are the shift from traditional publishing to packaging-driven growth and the rising adoption of digital and on-demand printing technologies.

By paper type, coated papers hold 44% market share in 2025. By application packaging printing, accounting for 57% of the total revenue.

The paper printing market is expected to grow at a CAGR of 4.6% between 2025 and 2032, driven primarily by packaging, digital printing adoption, and sustainable material trends.

Key players include International Paper, Smurfit WestRock, Mondi plc, and Stora Enso Oyj.