- Smart Packaging

- Decor Paper Market

Decor Paper Market Size, Share, and Growth Forecast, 2026 - 2033

Decor Paper Market by Product Type (Print Base Paper, Absorbent Kraft Paper, Others), Application (High-Pressure Laminates, Low-Pressure Laminates, Others), End-user, and Regional Analysis for 2026 - 2033

Decor Paper Market Size and Trends Analysis

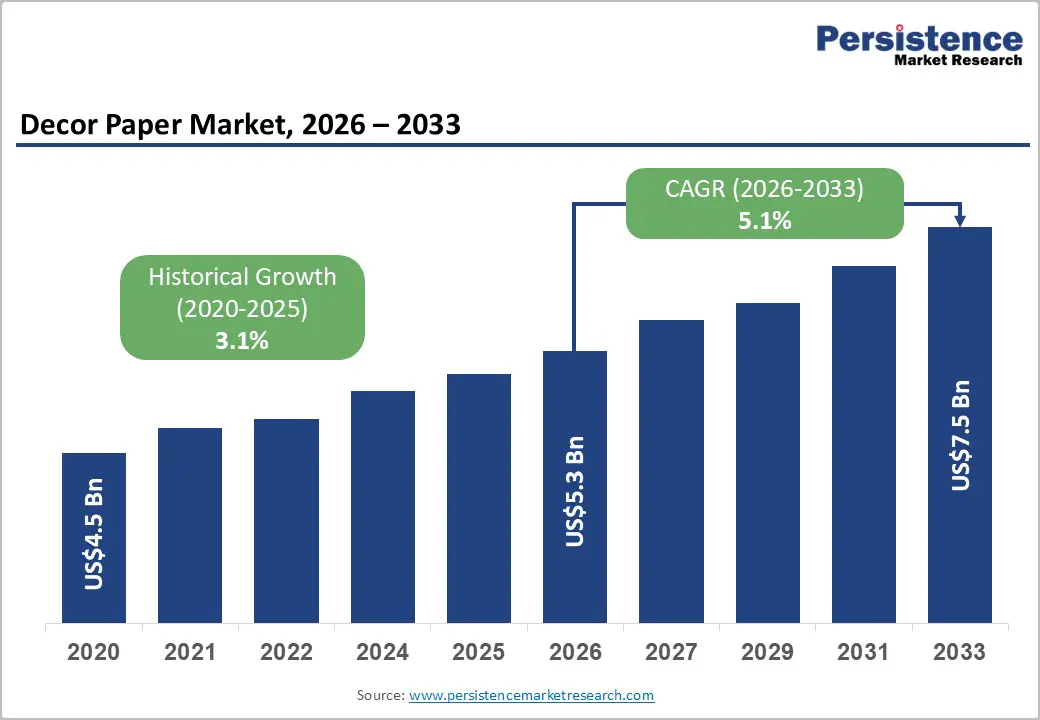

The global decor paper market size is projected to be valued at US$5.3 billion in 2026 and is expected to reach US$7.5 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033, driven by rising adoption of decor papers across furniture, laminates, flooring, and interior decorative applications, supported by urbanization and increasing disposable incomes in key economies.

Growth is further bolstered by renovation trends and the shift toward digital printing technologies, which enhance design versatility. Consumption is particularly strong in Asia Pacific, fueled by residential and commercial construction demand. Industry challenges include raw material price volatility and competition from emerging eco-friendly surface alternatives.

Key Industry Highlights

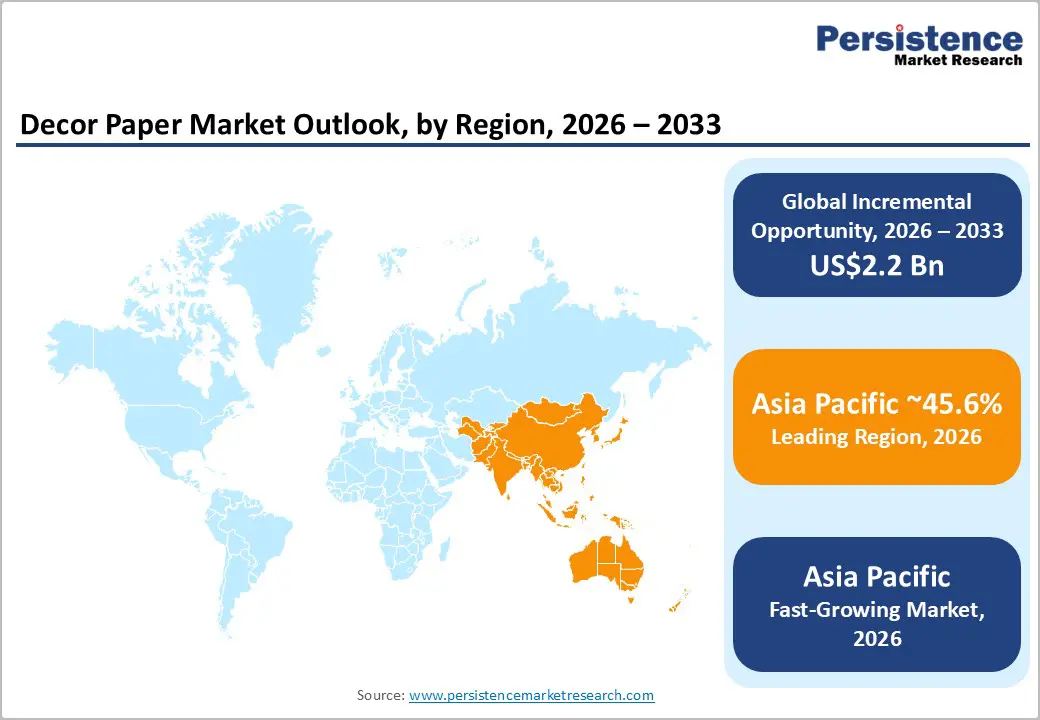

- Leading Region: Asia Pacific is projected to account for over 45.6% of market share, driven by rapid urbanization, large-scale residential and commercial construction, and strong furniture manufacturing bases in China, India, and ASEAN countries.

- Fastest-growing Region: Asia Pacific, supported by rising disposable incomes, expanding modular furniture adoption, and increasing investment in digital printing and decorative surface technologies.

- Investment Plans: Major manufacturers are expanding high-resolution digital printing capacities and localized production facilities, particularly in China, India, and the U.S., with a strong focus on sustainable raw materials and low-VOC decor paper solutions to meet regulatory and design requirements.

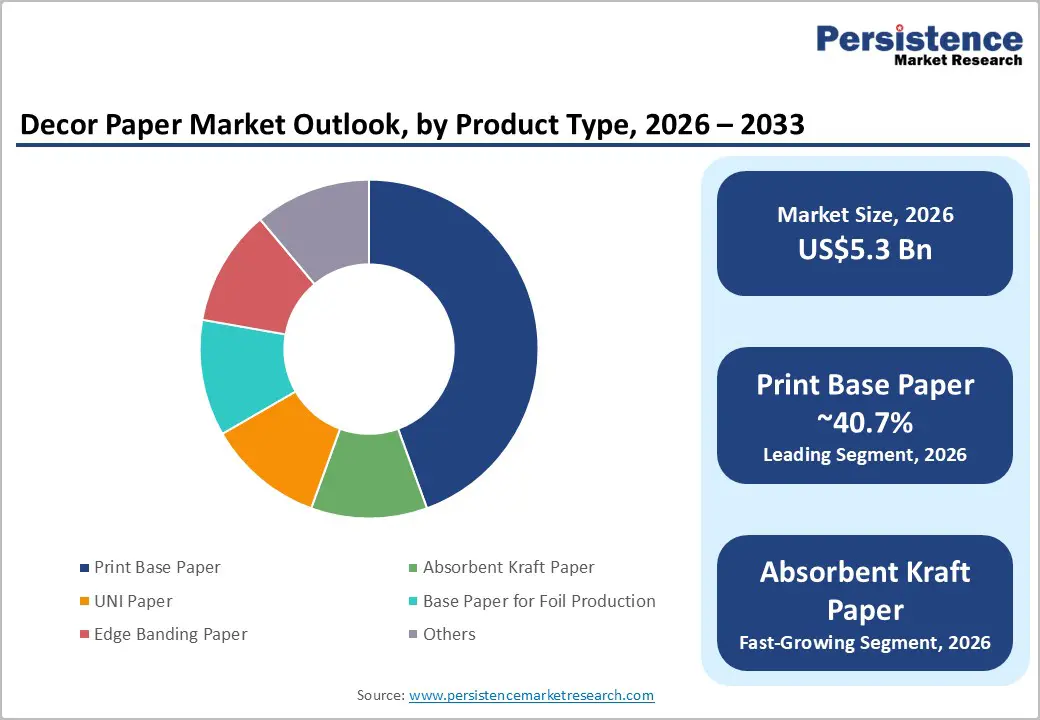

- Dominant Product Types: Print base paper, anticipated to hold over 40.7% of market share in 2026, owing to its superior print quality, compatibility with high-pressure and continuous pressure laminates, and extensive use in furniture and cabinetry applications.

- Leading End-user: Furniture and cabinets, expected to account for approximately 43.2% market share in 2026, driven by high-volume residential and office furniture production and growing preference for cost-effective, aesthetically versatile surface materials.

| Key Insights | Details |

|---|---|

| Decor Paper Market Size (2026E) | US$5.3 Bn |

| Market Value Forecast (2033F) | US$7.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Global Furniture Manufacturing and Interior Demand

The decor paper industry closely aligns with the furniture and interior décor sectors. Global wood-based panel output continues to indicate strong demand for decorative surfaces, with decor paper providing a cost-efficient solution for particle board, plywood, and MDF, particularly in high-volume furniture production. Growth in modular and ready-to-assemble furniture in markets such as China and India sustains recurring demand for high-quality printed and surface-treated papers. Renovation and remodeling activities further amplify demand. Commercial construction in Southeast Asia, including Vietnam and Thailand, increasingly specifies decor paper laminates for office, hospitality, and retail interiors due to durability and aesthetic appeal, reinforcing structural market growth.

Technological Innovation and Customization Capabilities

Advances in digital printing and surface treatment have broadened product applicability, enabling high-resolution, small-batch decor paper production. Digital printing allows complex designs while reducing inventory risk. Enhanced coatings and nanotechnology-enabled surfaces, such as antimicrobial or self-cleaning finishes, expand applications into healthcare and premium commercial spaces. Decor paper usage in high-pressure and continuous pressure laminates is increasing, and technological improvements in printing and resin compatibility further enhance aesthetic and functional performance.

Rising Renovation Activity and E-Commerce Expansion

Consumer spending on home and office renovation is increasing as e-commerce platforms provide broader access to decorative materials, including decor papers. Retail e-commerce growth facilitates direct market access for designers and DIY consumers. Home improvement retailers now stock a wide variety of decor paper products catering to both classic and modern design trends, supporting incremental market growth.

Barrier Analysis - Raw Material Price Volatility and Supply Chain Disruptions

Decor paper production is highly sensitive to fluctuations in raw material prices, particularly wood pulp, resins, specialty coatings, and printing chemicals. Wood pulp prices fluctuated by more than 30%, directly increasing input costs and creating margin pressure for manufacturers, especially those operating under long-term supply contracts. Price instability complicates procurement planning and reduces cost predictability across the value chain. Supply chain disruptions further intensify these challenges. Resins, pigments, and printing inks are often sourced from concentrated geographic regions, making manufacturers vulnerable to geopolitical tensions, trade restrictions, and production shutdowns. Logistics cost escalation has also weighed heavily on profitability; for instance, container freight rates from Asia to Europe increased sharply compared to pre-pandemic levels, affecting both raw material imports and finished product exports.

Competition from Sustainable Alternatives

The growing emphasis on sustainability poses competitive pressure for traditional decor paper products. Alternative surface materials, including reclaimed wood, bamboo-based panels, recycled composites, and engineered veneers, are gaining traction due to their perceived lower environmental impact and natural aesthetic appeal. These materials increasingly feature in eco-conscious residential and commercial projects, limiting decor paper penetration in certain applications. End users and designers are showing stronger preference for authentic natural textures and materials, particularly in premium interior segments. This shift places pressure on decor paper manufacturers to innovate and differentiate through sustainable sourcing, recyclable formulations, and certified low-emission products.

Opportunity Analysis - Premium Decor Papers with Enhanced Functional Capabilities

There is strong growth potential in premium decor papers engineered with advanced functional properties such as abrasion resistance, moisture protection, UV stability, and chemical resistance. These performance-enhanced papers are increasingly specified in high-traffic commercial spaces, institutional buildings, and hospitality environments. The integration of antimicrobial and self-cleaning surface technologies further supports adoption in healthcare and education facilities, where hygiene standards are critical. Digital printing technologies also enable short-run, high-resolution customization, allowing architects, interior designers, and furniture manufacturers to offer differentiated designs without large inventory commitments.

Growth in Emerging Economies

Emerging markets across South Asia and the Pacific present substantial growth opportunities due to rapid urbanization, expanding middle-class populations, and increasing residential and commercial real estate development. Rising demand for modular furniture, laminate flooring, and cost-effective decorative surfaces supports sustained decor paper consumption. Investment in local manufacturing and regional supply chains can unlock significant advantages, including reduced import dependence, lower transportation costs, and improved responsiveness to local design preferences. Manufacturers that establish production and design capabilities closer to high-growth markets are better positioned to capture long-term demand and enhance regional competitiveness.

Integration into Sustainable Building Standards

The increasing adoption of green building certifications and sustainability standards worldwide creates new avenues for decor paper growth. Products that meet low VOC emission requirements, formaldehyde limits, and environmental certifications are increasingly specified in premium commercial and residential developments. Manufacturers developing bio-based resin-compatible decor papers, along with products incorporating post-consumer recycled content, are well positioned to benefit from this shift. Aligning decor paper solutions with sustainable construction frameworks enhances acceptance among architects, developers, and institutional buyers, supporting long-term demand in environmentally driven market segments.

Category-wise Analysis

Product Types Insights

Print base paper is anticipated to account for over 40.7% of market revenue, maintaining its leadership due to superior versatility and strong compatibility with decorative laminate systems. It delivers excellent ink absorption, smooth surface finish, and high-definition graphic reproduction, which are essential for woodgrain, stone, and abstract designs used in furniture panels, kitchen cabinetry, wardrobes, and laminate flooring. These performance characteristics make print base paper the preferred substrate in both high-pressure laminates (HPL) and continuous pressure laminates (CPL), where visual consistency and color fidelity are critical.

Manufacturers continue to invest in advanced coating technologies, improved base paper uniformity, and enhanced substrate adhesion to meet increasingly complex design and durability requirements. For example, digitally printed print base papers are widely used in modular furniture and ready-to-assemble products, enabling manufacturers to offer design variety without maintaining large inventories. This combination of aesthetic performance, scalability, and cost efficiency reinforces print base paper’s dominant market position across residential and commercial interior applications.

Absorbent kraft paper represents the fastest-growing product segment. Its high mechanical strength, controlled porosity, and superior resin permeability make it well-suited for high-pressure laminate applications, where structural integrity during pressing is critical. Absorbent kraft papers are commonly used in laminate core layers, edge banding, and specialty decorative panels that require enhanced durability and dimensional stability. Growth is further supported by sustainability considerations and production scalability.

Kraft paper’s fibrous structure allows efficient resin impregnation with lower material waste, aligning with manufacturing efficiency and environmental goals. In both mature and emerging markets, manufacturers are optimizing kraft paper formulations to improve porosity control, resin uptake, and environmental performance, accelerating adoption in industrial furniture, commercial interiors, and high-traffic surface applications.

End-user Insights

Furniture and cabinets are anticipated to account for approximately 43.2% of market demand, making this the largest end-use segment. Decor paper is widely used in residential wardrobes, kitchen cabinets, office desks, shelving systems, and storage furniture due to its ability to deliver diverse finishes at a lower cost than solid wood or engineered veneers. The segment benefits from large-scale furniture manufacturing hubs in China, India, and Europe, where decor papers support high-volume production while maintaining consistent visual quality.

Advancements in surface treatments, including wear resistance, scratch protection, and moisture barriers, further enhance decor paper suitability for furniture exposed to frequent use. For example, decor paper-based laminates are extensively used in modular kitchens and office furniture, where durability and design flexibility are equally important. These factors sustain long-term demand and reinforce the segment’s leadership position.

Flooring is the fastest-growing end-use segment, driven by rising adoption of decor papers in laminate and engineered flooring products. Decor papers enable realistic replication of wood, stone, and ceramic visuals while offering performance advantages such as scratch resistance, dimensional stability, and ease of maintenance. This makes them particularly attractive for residential apartments, commercial offices, retail spaces, and hospitality environments.

Growth is supported by urbanization and renovation activity, especially in Asia Pacific and emerging urban centers, where consumers prioritize cost-effective yet visually appealing flooring solutions. Innovations in high-resolution printing and protective overlay layers have expanded decor paper usage in high-traffic flooring applications, reinforcing its role as a preferred decorative surface material in both new construction and refurbishment projects.

Regional Insights

North America Decor Paper Market Trends - Renovation-Led Demand with Premium, Low-Emission Focus

North America represents a significant share of global decor paper demand, supported by a mature furniture manufacturing base, strong interior design culture, and sustained renovation activity. The U.S. leads regional consumption, driven by residential remodeling, commercial interior upgrades, and demand for premium decorative surfaces. A primary growth driver in the region is home renovation and remodeling, particularly in kitchens, closets, and office interiors, where decor paper-based laminates are widely used for cabinetry, wall panels, and furniture finishes.

Large home improvement retailers such as Home Depot and Lowe’s continue to expand decorative surface assortments, indirectly strengthening downstream demand for decor paper substrates. At the same time, commercial sectors such as healthcare, education, and hospitality increasingly specify decor paper laminates for durability, hygiene, and design consistency. Technological innovation plays a critical role in North American market dynamics.

Decor paper manufacturers and laminate producers are investing in digital printing and advanced coating technologies to serve niche and customized design requirements. For example, collaborations between decor paper producers and printing technology providers have enabled higher-resolution woodgrain and stone patterns, supporting premium furniture and flooring segments. These capabilities are particularly valuable for modular furniture brands and contract furniture manufacturers seeking design differentiation without excessive inventory.

From a regulatory perspective, the market benefits from a strong push toward low-emission interior materials. EPA guidelines and state-level indoor air quality regulations, including those governing formaldehyde emissions, encourage the adoption of low-VOC and eco-certified decor paper products. As a result, manufacturers supplying resin-impregnated decor papers compatible with emission-compliant laminates gain a competitive advantage.

Investment activity reflects these trends. Several U.S.-based producers have expanded domestic decor paper and base paper capacities to reduce reliance on imports and improve supply chain resilience. Strategic partnerships with furniture OEMs and laminate manufacturers allow closer alignment between design development and production, accelerating time-to-market for new decorative collections. These investments position North America as a key hub for premium, compliant, and design-driven decor paper consumption.

Europe Decor Paper Market Trends - Sustainability-Driven Innovation and High-Design Surfaces

Europe remains a core market for decor paper, underpinned by a strong furniture manufacturing ecosystem, established interior design traditions, and an active renovation sector. Germany, France, the U.K., Italy, and Spain collectively account for the majority of regional demand, with Germany acting as a central hub for decorative surface innovation and laminate production. A defining growth driver in Europe is the regulatory emphasis on sustainability and material safety.

EU-wide regulations on formaldehyde emissions, recyclability, and chemical usage have accelerated demand for greener decor paper solutions. Manufacturers supplying papers compatible with low-emission resins and recyclable laminate systems are increasingly favored by furniture producers and project specifiers. This regulatory environment has encouraged continuous investment in cleaner production processes and sustainable raw material sourcing.

Demand for premium aesthetics and design sophistication also distinguishes the European market. European furniture and interior brands prioritize detailed surface textures, synchronized embossing, and high-fidelity prints, driving the adoption of advanced decor paper technologies. To support this demand, several producers have established dedicated design and pattern development centers, particularly in Germany, allowing faster response to evolving interior trends and closer collaboration with furniture and flooring manufacturers. Renovation activity across Western Europe further sustains decor paper consumption. Residential refurbishment, commercial retrofitting, and hospitality upgrades rely heavily on decor paper-based laminates for wall cladding, cabinetry, and furniture surfaces due to their balance of durability, appearance, and cost efficiency.

Recent developments highlight this focus on innovation and sustainability. European producers have expanded recyclable decor paper lines and strengthened partnerships aimed at bio-based resin compatibility, aligning with circular economy objectives. These initiatives directly influence purchasing decisions by furniture OEMs and construction specifiers, reinforcing Europe’s position as a leader in environmentally responsible decor paper applications.

Asia Pacific Decor Paper Market Trends - High-Volume Growth Fueled by Urbanization and Furniture Manufacturing

Asia Pacific is projected to be the largest and fastest-growing regional market, accounting for over 45.6 % of global decor paper volume. Growth is driven by rapid urbanization, large-scale construction activity, and strong furniture manufacturing bases in China, India, and ASEAN economies such as Vietnam, Thailand, and Indonesia. China dominates regional demand due to its extensive furniture manufacturing ecosystem and high output of wood-based panels. Decor paper consumption is closely tied to both domestic construction and export-oriented furniture production, where printed laminates offer cost-effective aesthetic enhancement.

Several manufacturers in China have expanded high-resolution decor paper production lines, targeting premium applications in cabinetry, flooring, and commercial interiors. India represents one of the fastest-growing markets in the region, supported by urban housing development, rising disposable incomes, and increasing adoption of modular furniture and laminate flooring. Growth is reinforced by domestic investments in decor paper manufacturing, which reduces import dependence and improves cost competitiveness. Local producers increasingly adopt digital printing technologies to meet the rising demand for contemporary designs.

ASEAN countries contribute through export-focused furniture manufacturing, supplying global markets with competitively priced products finished using decor paper laminates. Vietnam and Indonesia, in particular, benefit from shifting global supply chains and growing foreign investment in furniture and panel manufacturing facilities. Regulatory and investment trends also shape the market. Sustainability and emissions regulations in China and India encourage cleaner production practices and the use of compliant raw materials.

Foreign direct investment and regional expansions, including new sales offices and technical support centers, improve market penetration and customer responsiveness. These developments collectively strengthen Asia Pacific’s role as the primary growth engine of the global decor paper market.

Competitive Landscape

The global decor paper market is moderately concentrated, with leading players holding approximately 45-60% of the global share. The remaining share is distributed among regional and niche manufacturers. Competitive differentiation is driven by innovation, sustainable materials, printing technology, and supply chain efficiencies. Market leaders focus on digital printing innovation, surface technology advancement, scale efficiencies, sustainable product lines, and strategic expansion into emerging economies.

Key Industry Developments

- In June 2025, Stora Enso launched its EcoDecor Pro decorative paper line, featuring enhanced recycled-content options targeting sustainable interior laminates and wall panels.

- In February 2024, Lamigraf established a new design hub in Mönchengladbach, Germany, aimed at expanding decorative pattern development capabilities to respond to evolving European interior design trends.

Companies Covered in Decor Paper Market

- Ahlstrom

- WestRock

- SCHATTDECOR

- Lamigraf

- Neodecortech

- Felix Schoeller Group

- Kastamonu Entegre

- Surteco Group

- Sappi

- BMK GmbH

- Munich Paper

- Kronospan

- Interprint

- Pfleiderer

- ARAUCO

- Hangzhou Huawang New Material

- Shandong Qifeng New Material

- Zhejiang Dilong Culture Development

Frequently Asked Questions

The global decor paper market is estimated to be valued at US$5.3 billion in 2026.

By 2033, the decor paper market is expected to reach approximately US$7.5 billion.

Key trends include increasing adoption of digital printing for high-resolution designs, growing demand for low-VOC and sustainable decor papers, expansion of modular and ready-to-assemble furniture, and rising use of decor papers in laminate flooring and commercial interiors.

Print base paper is the leading product segment, anticipated to account for over 40.7% of market revenue, owing to its superior print quality, compatibility with decorative laminates, and extensive use in furniture and cabinetry applications.

The decor paper market is projected to grow at a CAGR of 5.1 % between 2026 and 2033.

Major players include Ahlstrom, WestRock, SCHATTDECOR, Lamigraf, and Neodecortech.