- Smart Packaging

- Foodservice Paper Bags Market

Foodservice Paper Bags Market Size, Share and Growth Forecast, 2026 - 2033

Foodservice Paper Bags Market by Product Type (Flat Paper Bags, Satchel Paper Bags, Others), Material Type (Kraft Paper, Others), Application (Bakery & Confectionery, Quick Service Restaurants (QSRs), Others), and Regional Analysis for 2026 - 2033

Foodservice Paper Bags Market Size and Trends Analysis

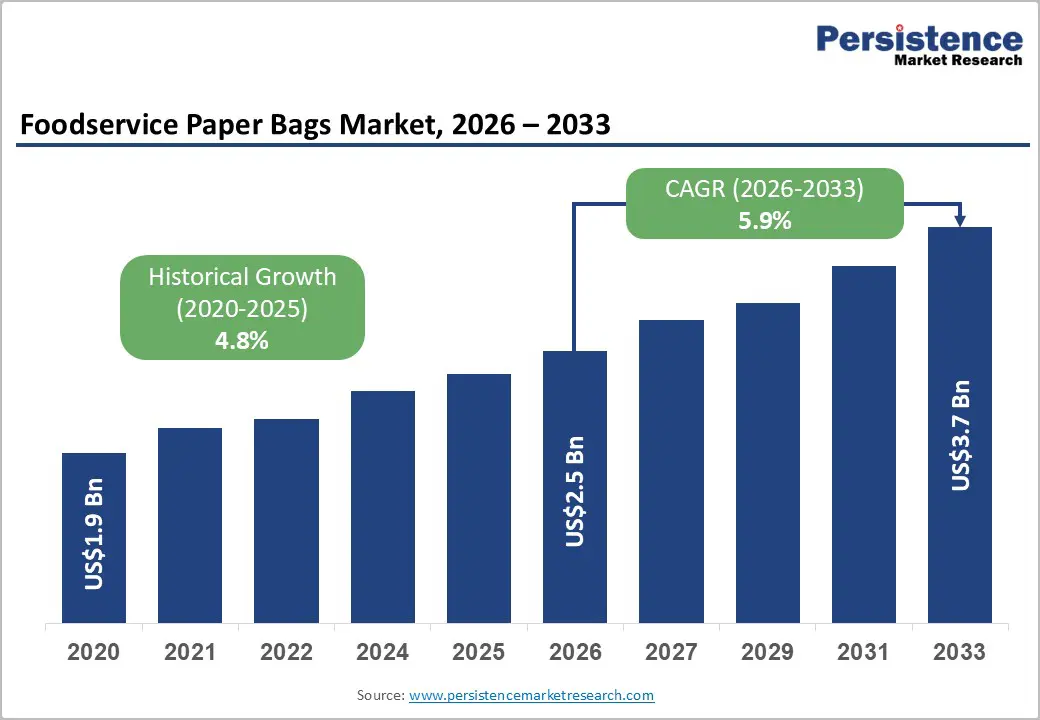

The global foodservice paper bags market size is likely to be valued at US$2.5 billion in 2026 and is expected to reach US$3.7 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033, driven by growing adoption of sustainable food packaging solutions across QSRs, bakeries, and food delivery platforms.

Regulatory measures such as the EU Single-Use Plastics Directive and plastic bans in India, Canada, and parts of the U.S. are accelerating the shift toward paper-based alternatives. In addition, rising urbanization and the growth of digital food delivery platforms like Zomato, Uber Eats, and DoorDash are boosting demand for kraft paper foodservice packaging.

Key Industry Highlights:

- Product Type Dynamics: SOS paper bags are expected to lead with around 35% market share in 2026, while twist handle bags are projected to grow the fastest at a CAGR of 6.8% by 2033, driven by rising demand from QSRs, bakeries, and food delivery services in the foodservice paper bags market.

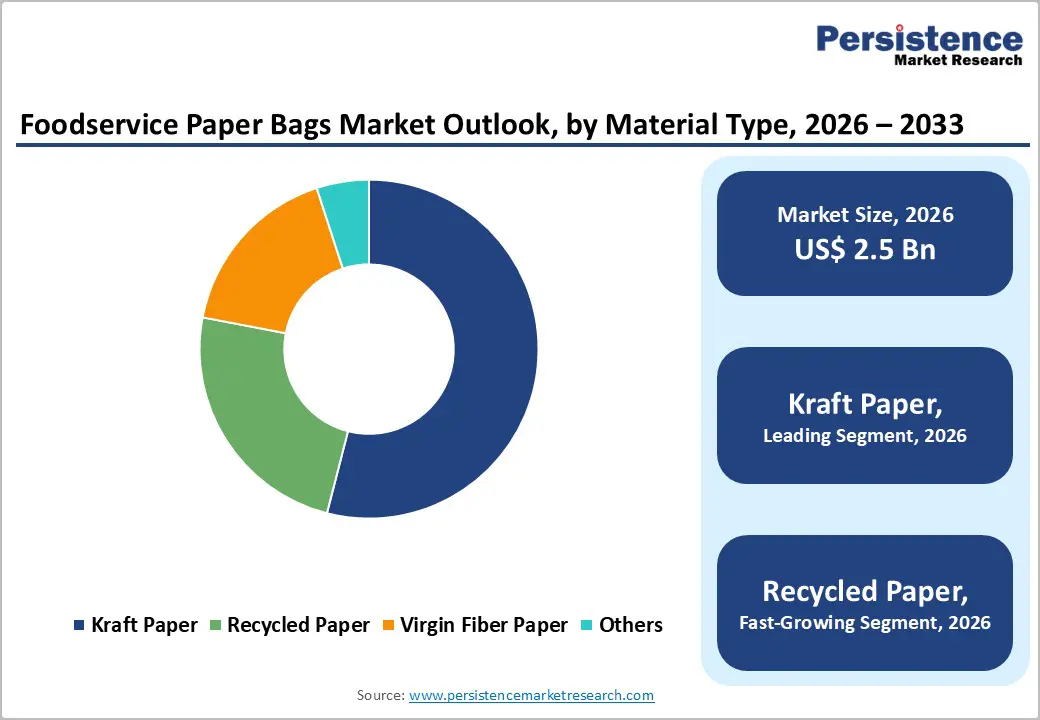

- Material Type Dynamics: Kraft paper is anticipated to dominate with approximately 52% share in 2026, while recycled paper is expected to register the fastest growth at a CAGR of 7.4% through 2033, supported by circular economy policies and rising adoption of eco-friendly food packaging solutions.

- Application Dynamics: Quick Service Restaurants (QSRs) are projected to hold the largest share at around 39% in 2026, while food delivery & takeaway services are expected to grow at the fastest rate with a CAGR of 8.1% by 2033, driven by rapid expansion of platforms like Uber Eats, Zomato, and DoorDash.

- Regional Dynamics: Asia Pacific is expected to dominate with approximately 40% market share in 2026, while also recording the fastest growth at a CAGR of 7.2% through 2033, led by China and India, supported by urbanization, QSR expansion, and strong regulatory push against plastic packaging.

- Competitive Landscape: Leading players are focusing on sustainable packaging innovation and capacity expansion strategies, with top companies collectively accounting for a significant portion of global supply in the paper food packaging market, driven by long-term contracts with QSR chains and food delivery platforms.

DRO Analysis

Driver - Global Regulatory Push toward Plastic Substitution and Sustainable Packaging Adoption

One of the strongest drivers of the foodservice paper bags market is the global regulatory shift away from single-use plastics. According to the United Nations Environment Programme (UNEP), more than 140 countries have implemented some form of plastic regulation. The European Commission’s Single-Use Plastics Directive (2019/904) mandates reduction of plastic carrier bags, accelerating adoption of paper-based alternatives.

Similarly, India’s Ministry of Environment, Forest and Climate Change (MoEFCC) implemented a nationwide ban on select plastic items in 2022. These regulations are pushing foodservice operators toward eco-friendly kraft paper bags and recycled fiber packaging, significantly expanding demand in QSRs and delivery segments. The result is a structural shift in procurement policies across global foodservice chains, increasing long-term adoption of compliant packaging formats.

Restraint - Higher Production Costs and Raw Material Price Volatility in Paper-Based Packaging

A major restraint impacting the foodservice paper bags market is the relatively higher cost of production compared to conventional plastic packaging. According to the Food and Agriculture Organization (FAO) and global pulp industry reports, wood pulp prices have shown volatility due to supply chain disruptions, energy inflation, and forestry constraints.

Kraft paper production is highly energy-intensive, increasing manufacturing costs by 20–35% compared to polyethylene alternatives in some regions. Small foodservice businesses, especially in emerging markets, face affordability challenges when transitioning to paper packaging. Additionally, dependency on forestry-based raw materials raises concerns about supply sustainability and price fluctuations, limiting adoption in cost-sensitive segments despite regulatory pressure.

Opportunity - Expansion of Online Food Delivery Ecosystems and Sustainable Packaging Integration

A significant opportunity for the foodservice paper bags market lies in the rapid expansion of online food delivery services. According to the World Bank digital economy insights and Statista digital commerce reports, global online food delivery penetration has grown at double-digit rates since 2020, particularly in Asia Pacific and North America. This creates strong demand for durable, leak-resistant, and branded paper packaging.

The opportunity is estimated to account for over US$1 billion in incremental demand by 2033, driven by QSRs, cloud kitchens, and aggregator platforms. Companies are increasingly investing in moisture-resistant coatings and reinforced self-opening square (SOS) paper bags, creating product innovation opportunities aligned with sustainability mandates and consumer preference for eco-friendly packaging.

Category-wise Analysis

Product Type Insights

Self-Opening Square (SOS) paper bags are estimated to dominate the foodservice paper bags market, accounting for around 35% share in 2026. Their leadership is expected to be supported by strong adoption across QSRs and bakery chains, where high-volume and fast-paced packaging operations are critical. These bags are widely estimated to remain the preferred format due to their structural strength, stackability, and compatibility with automated filling systems used in standardized foodservice operations globally.

Twist handle bags are estimated to be the fastest-growing product type, expanding at a CAGR of 6.8% by 2033. Growth is expected to be driven by rising demand for premium and convenience-oriented packaging in cafés and food delivery ecosystems. Increasing urban takeaway consumption and branding-focused packaging strategies are likely to further support adoption, particularly in last-mile delivery environments handling multi-item orders.

Material Type Insights

Kraft paper is estimated to lead the foodservice paper bags market with a 52% share in 2026, supported by regulatory-driven substitution of plastic packaging. Government measures such as India’s single-use plastic restrictions (2022) and the EU Directive 2019/904 are expected to continue driving adoption. Kraft paper is widely estimated to remain the preferred material due to its strength, grease resistance, and biodegradability across QSR and bakery applications.

Recycled paper is estimated to be the fastest-growing material segment, registering a CAGR of 7.4% through 2033. Growth is expected to be supported by circular economy policies and Extended Producer Responsibility (EPR) frameworks across major economies. Foodservice operators are increasingly shifting toward recycled content packaging to align with sustainability targets, while improving recycling infrastructure is expected to strengthen raw material availability.

Application Insights

Quick Service Restaurants (QSRs) are estimated to dominate the application landscape with around a 39% share in 2026, making them the largest end-use segment. Growth is expected to be supported by global expansion of fast-food chains and the need for standardized, cost-efficient packaging solutions. Paper bags are widely estimated to remain essential in QSR takeaway operations due to hygiene compliance, operational speed, and scalability.

Food delivery & takeaway services are estimated to be the fastest-growing application segment, expanding at a CAGR of 8.1% by 2033. Expansion is expected to be driven by rapid growth in digital food ordering platforms and cloud kitchen models in urban areas. Increasing usage of platforms such as Uber Eats, Zomato, and Deliveroo is expected to raise packaging intensity per order, while plastic reduction policies continue to support the shift toward eco-friendly food packaging solutions.

Regional Analysis

North America Foodservice Paper Bags Market Trends

North America is estimated to account for a 27% share of the global foodservice paper bags market in 2026, supported by high penetration of organized foodservice and mature packaging infrastructure. Regulatory momentum from the U.S. EPA’s waste reduction and sustainable materials programs, along with Canada’s federal restrictions on selected single-use plastics, is steadily accelerating the shift toward paper-based alternatives. Growth is also reinforced by rising consumer demand for recyclable and compostable packaging in urban foodservice ecosystems.

U.S. Foodservice Paper Bags Market Trends

The U.S. is estimated to represent 80–85% of the North America market, anchored by its large QSR base and advanced food delivery ecosystem. A key observable trend is the rapid transition toward high-strength kraft and grease-resistant paper bags, particularly across fast-food chains adapting to state-level packaging restrictions in California and New York. Expansion of digital platforms such as DoorDash and Uber Eats is increasing order fragmentation, which is indirectly lifting per-order packaging consumption.

Canada Foodservice Paper Bags Market Trends

Canada is estimated to contribute 10–12% share within North America, with demand strongly shaped by federal plastic reduction mandates and municipal sustainability programs. Market behavior is shifting toward fully recyclable, certification-backed paper packaging, especially in metropolitan hubs like Toronto and Vancouver. Growth is further supported by rising café culture and steady expansion of takeaway dining formats across urban retail foodservice outlets.

Europe Foodservice Paper Bags Market Trends

Europe is estimated to hold 22–24% share of the global foodservice paper bags market in 2026, shaped heavily by strict environmental governance and early adoption of circular economy principles. The EU Green Deal framework continues to drive packaging transformation across member states, with a strong push toward recyclable and compostable materials. This regulatory clarity is creating consistent demand across both retail foodservice and institutional catering channels.

Germany Foodservice Paper Bags Market Trends

Germany is estimated to account for 29% of Europe’s market in 2026, supported by its highly developed packaging manufacturing base and robust recycling systems. A noticeable trend is the increasing deployment of premium-grade kraft and compostable paper bags across organized foodservice chains, aligned with strict waste segregation norms. Strong industrial efficiency and automation in packaging production are also improving scalability for high-volume demand.

U.K. Foodservice Paper Bags Market Trends

The U.K. is estimated to hold 17% share within Europe in 2026, with growth closely tied to the expansion of food delivery platforms and urban takeaway culture. A key trend is the shift toward brand-integrated sustainable packaging, where paper bags are increasingly used as a marketing extension for foodservice operators. Growth in cloud kitchens and dark store models is further intensifying demand for lightweight yet durable packaging formats.

Asia Pacific Foodservice Paper Bags Market Trends

Asia Pacific is estimated to dominate with a 40% share of the global market in 2026, making it both the largest and most dynamic regional market. Expansion is driven by rapid urban migration, rising disposable income, and strong penetration of digital food ordering ecosystems. Regulatory actions restricting single-use plastics across India, China, and Southeast Asia are significantly reshaping packaging demand toward paper-based alternatives.

China Foodservice Paper Bags Market Trends

China is estimated to account for 40% of the Asia Pacific market in 2026, supported by large-scale manufacturing strength and high domestic consumption of packaged food. A key trend is the rapid scaling of app-based food delivery ecosystems, which has increased packaging frequency per transaction. Government-led environmental initiatives in major cities are further reinforcing adoption of recyclable and kraft-based packaging formats across both retail and foodservice sectors.

India Foodservice Paper Bags Market Trends

India is estimated to hold 20% share within Asia Pacific, driven by fast-growing QSR networks and strong digital food delivery expansion. A defining trend is the shift toward low-cost kraft paper packaging in urban delivery ecosystems, supported by regulatory restrictions on selected plastic formats. Rapid growth of cloud kitchens and increasing penetration of organized foodservice in Tier-2 and Tier-3 cities are further strengthening long-term demand visibility.

Competitive Landscape

The global foodservice paper bags market is moderately consolidated, with leading players such as International Paper, WestRock, Mondi, Smurfit Kappa, Novolex, and Huhtamaki collectively estimated to account for around 45% of global revenue share. These companies benefit from integrated pulp-to-packaging operations, strong supply agreements with global QSR chains, and large-scale manufacturing capacity that supports consistent demand across foodservice and delivery ecosystems. Their scale advantage enables efficient pricing and standardized supply across multiple regions.

Competitive positioning is increasingly driven by sustainability-focused innovation and capacity expansion, with emphasis on kraft paper upgrades, grease-resistant coatings, and recyclable barrier technologies aligned with global plastic reduction policies. The remaining market is fragmented across regional players competing on cost efficiency and customization, particularly in Asia Pacific. However, strict food-grade compliance and sustainability standards create high entry barriers, supporting gradual consolidation as larger firms expand through capacity additions and strategic partnerships.

Key Industry Developments:

- In April 2025, Novolex completed the US$6.7 billion acquisition of Pactiv Evergreen, significantly expanding its footprint in foodservice packaging, including paper bags, cups, and containers. The deal strengthens Novolex’s position across North America’s QSR supply chain and enhances its sustainable packaging portfolio through vertically integrated production capabilities.

- In January 2025, the International Paper–DS Smith transaction gained regulatory momentum, marking a major consolidation move in the paper packaging industry. The deal reflects a broader M&A cycle reshaping the sector across Europe and North America, driving competitive restructuring and accelerating consolidation in kraft paper and foodservice packaging assets.

Companies Covered in Foodservice Paper Bags Market

- International Paper Company

- WestRock Company

- Mondi Group

- Smurfit Kappa Group

- Novolex Holdings

- Huhtamaki Oyj

- Georgia-Pacific LLC

- Stora Enso

- DS Smith Plc

- Sonoco Products Company

- Genpak LLC

- Rengo Co., Ltd.

- Uflex Ltd.

- Billerud AB

- SCG Packaging

Frequently Asked Questions

The global foodservice paper bags market is projected to reach US$2.5 billion in 2026.

Rising demand for sustainable food packaging, regulatory plastic bans, and growth in food delivery services drive the market.

The foodservice paper bags market is expected to grow at a CAGR of 5.9% from 2026 to 2033.

Growth opportunities lie in online food delivery expansion, sustainable packaging innovation, and emerging urban foodservice demand.

Key players include International Paper, WestRock, Mondi Group, Smurfit Kappa, Novolex, and Huhtamaki.