- Smart Packaging

- Rolling Papers Market

Rolling Papers Market Size, Share, and Growth Forecast, 2026 - 2033

Rolling Papers Market by Material (Hemp, Rice Straw, Others), Basis Weight (Mid-Weight, Thick, Others), Application, and Regional Analysis for 2026 - 2033

Rolling Papers Market Size and Trends Analysis

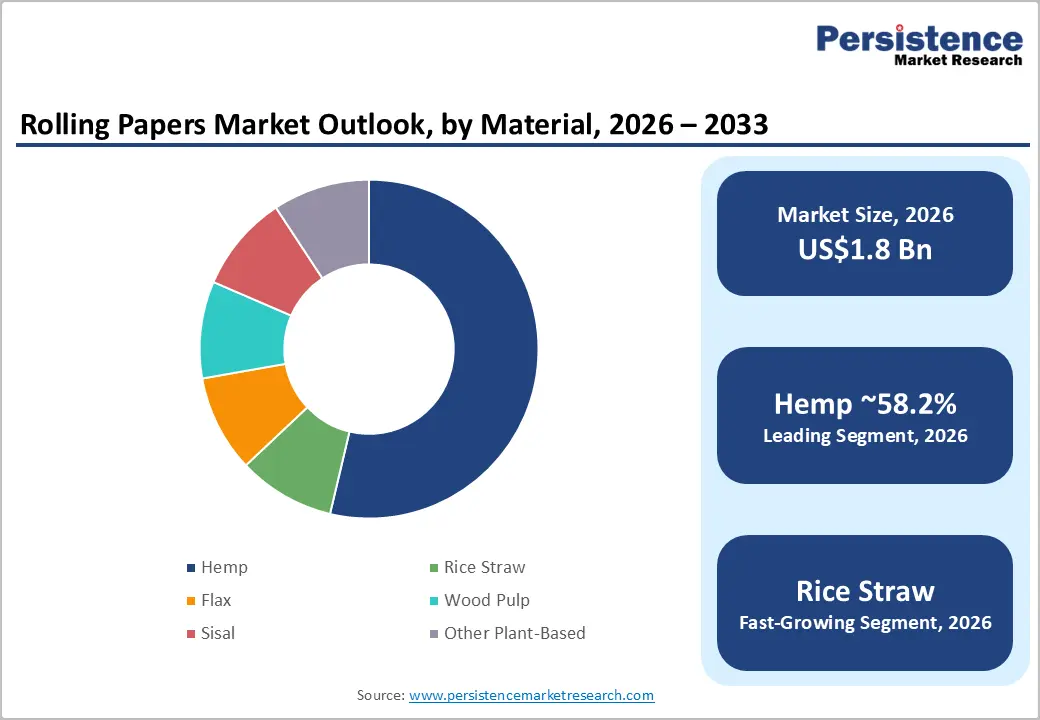

The global rolling papers market size is likely to be valued at US$1.8 billion in 2026 and is expected to reach US$2.5 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033.

Market expansion is primarily driven by rising cannabis legalization and pre-roll consumption in regulated markets, steady roll-your-own tobacco demand in mature regions, and ongoing material innovation, particularly in hemp- and rice-based papers that command premium pricing. Evolving regulatory frameworks and stricter youth protection policies continue to pose structural challenges for manufacturers and distributors.

Key Industry Highlights

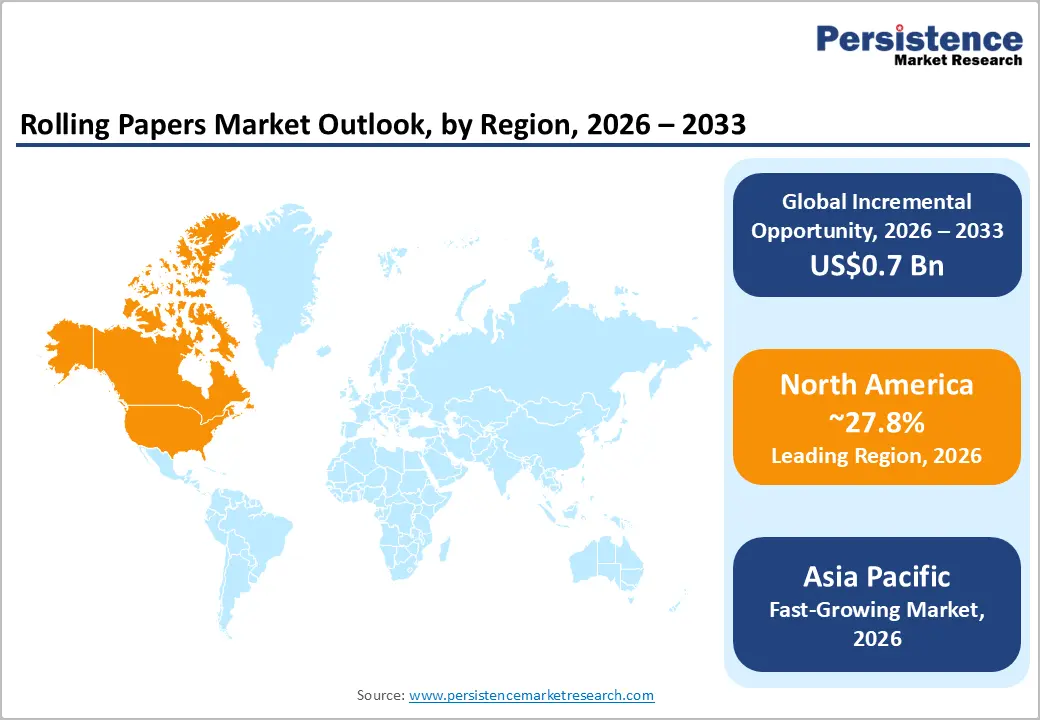

- Leading Region: North America is projected to hold 27.8% share, driven by the U.S. with high pre-roll adoption, premium hemp uptake, and a robust dispensary ecosystem.

- Fastest-growing Region: Asia Pacific, fueled by cost-effective manufacturing, expanding roll-your-own traditions, and rising premium rolling-paper demand in urban centers.

- Investment Plans: Focus on automation, expansion of hemp/rice processing capacity, and B2B pre-roll supply chains, targeting both domestic and export markets.

- Dominant Material: Hemp is expected to hold a 58.2% share in 2026, leading by value due to sustainability, alignment with cannabis culture, and premium positioning.

- Leading Application: Tobacco rolling is estimated to hold a 63.4% share and continues to dominate overall volume due to its large global user base and consistent demand across both mature and emerging markets, despite faster growth in cannabis/herb applications.

| Key Insights | Details |

|---|---|

| Rolling Papers Market Size (2026E) | US$1.8 Bn |

| Market Value Forecast (2033F) | US$2.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8 % |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Legalization and Pre-Roll Surge Driving Cannabis Application Growth

Legalization and retail maturation across North America and select European markets have significantly accelerated the adoption of pre-rolls and infused pre-rolls. These formats are increasingly preferred for convenience, dosage consistency, and retail merchandising efficiency. As pre-rolls gain a larger share of cannabis retail sales, demand for single-use rolling papers and pre-formed cones continues to rise. This trend supports both higher unit volumes and increased average selling prices, particularly for premium, ultra-thin, and specialty papers. The cascading impact follows a clear pattern: dispensary expansion increases pre-roll penetration, which, in turn, drives higher repeat purchases of rolling papers through both B2B manufacturing channels and consumer retail outlets.

Material Shift toward Hemp and Sustainable Fibers Enabling Premiumization

Consumers and retailers are increasingly prioritizing hemp-based and other plant-derived rolling papers due to sustainability concerns, perceived purity, and alignment with natural consumption trends. Hemp papers currently account for the largest share of the material mix, representing approximately 58.2% of market consumption by value. Brands are actively repositioning their portfolios toward certified organic, low-ash, and additive-free paper variants, reinforcing premium positioning. This material transition supports margin expansion and stimulates frequent new product launches, including rice-hemp blends and unbleached options. As a result, the overall market value continues to grow even in regions where unit consumption remains relatively stable.

Innovation in Formats and Value Chain Integration

Advancements in rolling paper formats and upstream manufacturing technologies are reshaping demand dynamics. The proliferation of pre-rolled cones, improved adhesive formulations, and high-speed pre-roll machines has created new demand from commercial cannabis manufacturers and dispensary chains. Basis-weight diversification, ranging from mid-weight to thicker papers optimized for machine stuffing, allows suppliers to serve both artisanal consumers and industrial B2B clients. These innovations increase average order sizes and enable cross-selling of complementary products such as filters and tips, driving revenue growth beyond traditional unit-based expansion.

Barrier Analysis - Regulatory Tightening and Fragmented Jurisdictional Policies

Rolling papers operate at the intersection of tobacco and cannabis regulations, exposing the market to frequent and unpredictable policy changes. Sudden regulatory actions, including sales bans, advertising restrictions, and enhanced age-verification requirements, can significantly disrupt retail availability and distribution strategies. In certain jurisdictions, restrictions on flavored papers or pre-rolled cones have directly reduced product visibility and consumer access. This regulatory fragmentation increases compliance costs, heightens inventory risk, and complicates cross-border expansion strategies for global brands.

Illicit Market Competition and Sustained Price Pressure

In markets where legal cannabis products face high taxation or supply chain inefficiencies, illicit channels continue to undercut regulated offerings. Lower illicit pricing exerts downward pressure on retail margins, which in turn cascades upstream to rolling paper suppliers. In mature tobacco markets, declining cigarette consumption and aggressive public health campaigns further limit long-term volume growth. These factors collectively compress margins in commoditized paper segments and accelerate consolidation among manufacturers seeking scale efficiencies.

Opportunity Analysis - Premium Hemp and Specialty Paper Expansion

Shifting consumer preferences toward natural, organic, and low-contaminant products present a significant premiumization opportunity. Certified hemp papers and ultra-thin rice blends are increasingly viewed as high-quality alternatives, supporting price premiums of 25-40% over conventional papers. If premium hemp products capture even 10-15% of total market volume, incremental revenue potential could reach approximately US$ 150-250 million over the forecast period within the existing global market base. Manufacturers capable of securing traceable raw material supply and scaling certified production are best positioned to capture this value.

B2B Pre-Roll Manufacturing and Automation Supply Chains

As dispensaries and branded cannabis operators increasingly outsource pre-roll production to co-packers and automated facilities, demand is rising for machine-grade rolling papers, pre-formed cones, and controlled-burn formulations. Suppliers that align product specifications with high-speed pre-roll equipment can establish stable, high-volume B2B revenue streams. Capturing even 5-8% of upstream pre-roll supply requirements in leading legalized markets can generate substantial recurring revenues and strengthen long-term commercial partnerships.

Category-wise Analysis

Material Insights

Hemp is expected to be the dominant material in the rolling papers market, accounting for approximately 58.2% of the total market value. Sustainability advantages, cultural alignment with cannabis consumption, and favorable regulatory treatment as an industrial agricultural product drive its leadership. Hemp papers are marketed as clean-burning, additive-free, and environmentally responsible, enabling consistent premium pricing. Most major brands now position hemp variants as core offerings rather than niche alternatives, reinforcing customer loyalty and providing manufacturers with stable, high-margin revenue streams.

Rice-based rolling papers represent the fastest-growing material segment, supported by demand for ultra-thin, neutral-flavor papers. Leveraging established rice-paper processing infrastructure, manufacturers have successfully adapted food-grade production methods to rolling paper specifications. Rice papers are particularly attractive to flavor-conscious consumers and premium pre-roll producers seeking low-ash combustion and consistent burn characteristics. Growth rates in this segment exceed the overall market average, driven by premium pricing and sustained product innovation.

Application Insights

Tobacco rolling is expected to be the largest application segment in the rolling papers market, with an anticipated share of approximately 63.4% in 2026. This segment is particularly strong in Europe (Germany, Spain, and France) and parts of Asia (Japan, India), where traditional roll-your-own (RYO) habits are deeply embedded. Consumers in this segment generally prefer mid-weight, natural, and unbleached papers, purchased in frequent, low-cost transactions, which provides a stable, recurring demand base. Leading manufacturers, such as Smoking, Rizla, and OCB, maintain extensive distribution networks and production scales to meet this ongoing demand.

The segment’s established infrastructure also facilitates the gradual introduction of newer, premium products targeting the evolving trends, including organic and flavored tobacco papers. This steady consumption ensures long-term revenue predictability and reinforces supply chain resilience, particularly in mature markets where RYO remains culturally significant.

The cannabis and herb rolling segment is likely to be the fastest-growing application category, fueled by the legalization of recreational and medical cannabis in North America (U.S., Canada) and select European markets (Netherlands, Switzerland). This segment is anticipated to grow as regulated retail channels expand and pre-rolled products, infused papers, and flavored variants gain popularity. Premium rolling papers designed for cannabis, such as hemp-based, ultra-thin, or rice papers, are increasingly adopted by consumers willing to pay higher per-unit prices.

For example, brands such as RAW, Juicy Jay’s, and Elements have successfully leveraged innovation in rolling paper formats to capture a growing share of this market. The combination of evolving legal frameworks, product sophistication, and retail proliferation makes this segment a key growth driver for rolling paper manufacturers, particularly in North America and emerging European cannabis markets, where consumer education and product experimentation are accelerating adoption.

Regional Insights

North America Rolling Papers Market Trends - Cannabis Legalization Driving Premium Hemp Paper Adoption

North America is expected to lead the global rolling papers market with approximately 27.8% share in 2026, supported by a well-established culture of both tobacco and cannabis consumption. The U.S. accounts for the majority of regional demand, propelled by widespread legalization of recreational and medical cannabis in multiple states, including California, Colorado, and Illinois, which has expanded the consumer base for premium hemp and specialty rolling papers. North America’s high disposable income and mature retail infrastructure have accelerated the adoption of premium unbleached and hemp-based papers, which are often preferred for both tobacco and cannabis use.

For example, brands such as RAW (Phoenix, Arizona) and Juicy Jay’s (Chicago-based flavored rolling papers) have strong brand recognition and distribution across smoke shops, dispensaries, and online platforms. RAW’s unbleached hemp papers are widely associated with cannabis rolling, contributing to their status as one of the region’s most visible brands.

In Canada, progressive cannabis regulation has created a complementary growth vector, with e-commerce channels capturing a growing share of specialty rolling paper sales and small local brands (boutique hemp paper producers) increasing presence in cannabis accessory portfolios. Despite broad legalization, regulatory variability across states and provinces creates uneven growth patterns: taxation levels, packaging regulations, and age restrictions can suppress demand in certain jurisdictions, whereas others experience robust expansion in dispensary-linked retail.

Investment activity remains strong in production automation, material innovation (eco-friendly and biodegradable papers), and scalable supply chains, as manufacturers seek to align with sustainability preferences and evolving consumer segments. North America functions both as a major consumption hub and a launchpad for brands expanding into European and Asia Pacific markets, with cross-border distribution agreements and digital retail partnerships enhancing global reach.

Europe Rolling Papers Market Trends - RYO Tobacco Heritage with Sustainability-Led Premiumization

Europe remains a mature and strategically important rolling papers market, supported by a deeply rooted roll-your-own (RYO) tobacco tradition and a diverse retail ecosystem. Countries such as Germany, the U.K., France, and Spain collectively account for the bulk of European demand, with consumers historically preferring ultra-thin papers that emphasize smoothness and burn quality in roll-your-own cigarettes. own cigarettes. For example, Spain’s cultural affinity for hand-rolled tobacco has sustained high unit volumes, whereas northern European markets, such as Germany, exhibit increasing premiumization driven by eco-certified and FSC-sourced pulp papers.

European brands and manufacturers also shape market dynamics. Legacy players such as Zig-Zag (France) and OCB (France) command significant shelf presence and benefit from strong heritage branding, which supports high-end product adoption and export to other regions.

Recent industry developments include product innovation focused on sustainable materials and compostable packaging, such as OCB’s “Eco Hemp” line introduced in late 2024, which appeals to environmentally conscious consumers and aligns with EU sustainability directives. Regulatory harmonization across the European Union, including constraints on flavored tobacco and tightening controls under the Tobacco Products Directive, continues to influence product development and marketing strategies.

While tobacco control policies restrict certain flavor variants and packaging formats, selective cannabis policy liberalization (e.g., limited adult-use cannabis markets in countries such as Germany) is creating incremental opportunities for premium and specialty herb rolling papers. European distributors are responding with curated selections across specialty tobacconists, vape shops, and online channels that balance compliance with consumer demand for diverse paper formats.

Asia Pacific Rolling Papers Market Trends - High-Volume Growth from Traditional Tobacco Use and Cost-Efficient Manufacturing

Asia-Pacific is projected to be the fastest-growing regional market, driven by demographic trends, rising disposable incomes, and cultural acceptance of hand-rolled smoking products in countries such as China, India, Japan, and Southeast Asia. The region’s large population base and established tobacco-use traditions make it a significant contributor in volume, with China and India leading in unit consumption due to widespread hand-rolling. rolled cigarette preferences and cost-sensitive markets that favor local and imported rolling paper brands.

In China, demand for rolling paper is expanding as urbanization and exposure to premium products increase, while manufacturers introduce new hemp-based products. based and specialty papers tailored for both domestic consumption and export. Japan’s market also sees innovation, with Japanese manufacturers launching more than two dozen new hemp paper variants in recent years, reflecting growing interest in natural and premium formulations. Southeast Asian nations, including Indonesia and Vietnam, show double-digit growth rates where local tobacco cultures and affordable pricing encourage rising penetration of rolling papers.

Investment trends in the region focus on capacity expansion, cost-efficient manufacturing, and integration into global supply chains, thereby enabling Asia-Pacific producers to serve both regional and international markets effectively. Export-oriented strategies benefit from lower manufacturing costs and established cellulose and rice-processing infrastructure, which supports competitive pricing and diverse product offerings. While stringent regulatory environments in some countries, particularly those with strict tobacco control, present obstacles, premium imports and targeted licensing frameworks are enabling gradual market expansion. E-commerce channels also play an expanding role, connecting manufacturers and specialty brands with consumers across urban and rural markets.

Competitive Landscape

The global rolling papers market is semi-consolidated, with a small group of globally recognized brands holding strong distribution positions alongside numerous regional and private-label manufacturers. Leading players typically control mid-teen market shares, while the remaining market is fragmented across smaller producers. Competitive success is increasingly tied to brand equity, certified material sourcing, product breadth, and channel partnerships.

Leading companies emphasize premiumization, vertical integration into B2B pre-roll supply, cost-efficient manufacturing partnerships, and brand collaborations. Differentiation is achieved through certified materials, broad SKU portfolios, and strong retail and dispensary relationships, while smaller players compete through pricing and niche product innovation.

Key Industry Development

- In March 2025, Rizla launched ultra-thin flavored rolling papers in the U.K. and Germany, aiming to attract younger demographics and enhance its product appeal across key European markets.

- In March 2025, RAW announced a strategic partnership with Zig Zag France to co-distribute sustainable rolling papers and accessories across key European markets, aiming to expand both brands’ presence and growth in premium segments.

Companies Covered in Rolling Papers Market

- OCB

- RAW

- Rizla

- Zig-Zag

- Juicy Jay’s

- Elements

- Blazy Susan

- Randy’s

- Republic Technologies

- Smoking Rolling Papers

- Job Ultra Thin

- Pure Hemp

- Bambu

- Carbon Rolling Papers

- King Palm

- Shine Papers

- Top Leaf

- Cyclones

Frequently Asked Questions

The global market size is likely to be valued at US$1.8 billion in 2026.

By 2033, the market is expected to reach US$2.5 billion, reflecting steady growth over the forecast horizon.

Key trends include increasing pre-roll and cannabis consumption in legalized markets and a shift toward sustainable and premium materials such as hemp and rice blends.

By material, hemp is the leading segment, accounting for approximately 58.2% of the market share.

The rolling papers market is projected to grow at a CAGR of 4.8% between 2026 and 2033.

Key players include OCB, RAW (HBI), Rizla, Zig-Zag, and Republic Technologies.