- Biotechnology

- Pap Smear & HPV Testing Market

Pap Smear & HPV Testing Market Size, Share, and Growth Forecast, 2025 - 2032

Pap Smear & HPV Testing Market by Test Type (Pap Testing, HPV Testing), Product & Service (Instruments & Analyzers, Consumables & Reagents, Software & AI Platforms, Testing Services), Application (Cervical Cancer Screening, Vaginal Cancer Screening, Clinical Trials & Epidemiology, Others), End-use, and Regional Analysis for 2025 - 2032

Pap Smear & HPV Testing Market Size and Trend Analysis

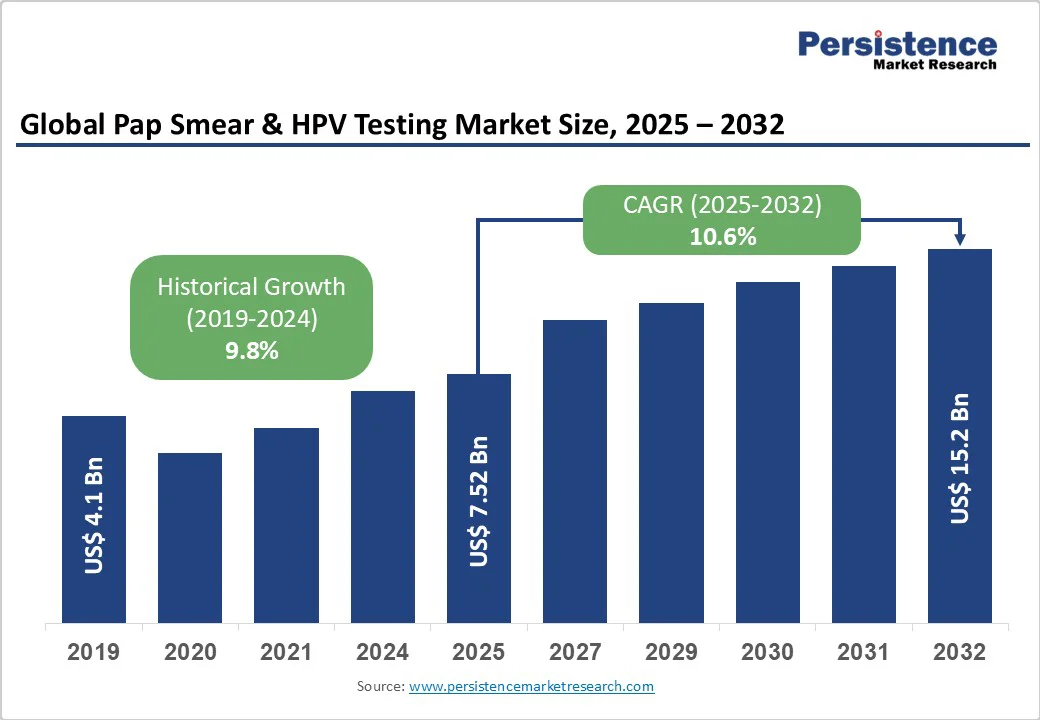

The global pap smear & hpv testing market is likely to be valued at US$7.5 Bn in 2025 and reach US$15.2 Bn by 2032, growing at a CAGR of 10.6% during the forecast period from 2025 to 2032.

The Pap Smear & HPV Testing market is experiencing robust growth driven by increasing awareness of cervical cancer screening, advancements in diagnostic technologies, and the rising prevalence of HPV-related diseases.

Key Industry Highlights:

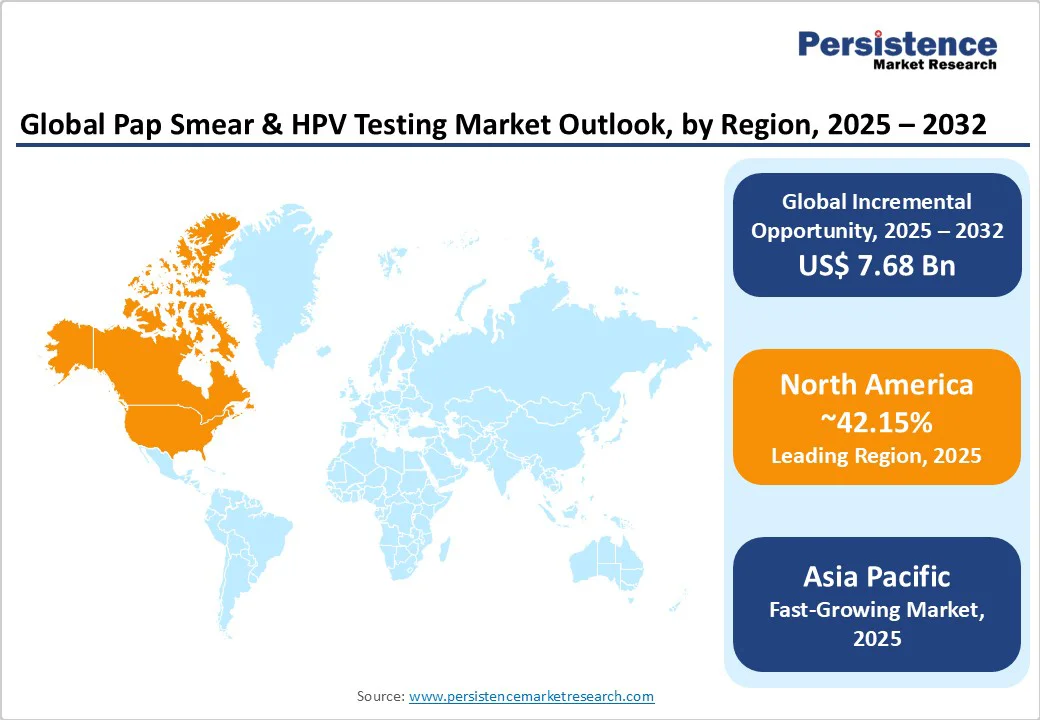

- Leading Region: North America holds a 42.1% share in 2025, driven by advanced healthcare infrastructure, high screening rates, and the strong presence of key players, including Hologic, Inc. and Quest Diagnostics.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, propelled by rising healthcare investments, growing awareness of cervical cancer screening, and large populations in countries such as China and India.

- Investment Plans: Gavi is investing over $600 million from 2022 through 2025 to revitalize its HPV vaccine program, aiming to protect 86 million girls against cervical cancer by accelerating coverage and introducing vaccination in more countries, making up for pandemic-related disruptions and advancing health equity, and boosting demand for HPV testing solutions.

- Dominant Test Type: HPV Testing accounts for nearly 58.6% of the Pap Smear & HPV Testing market share, driven by its higher sensitivity and specificity in detecting high-risk HPV strains.

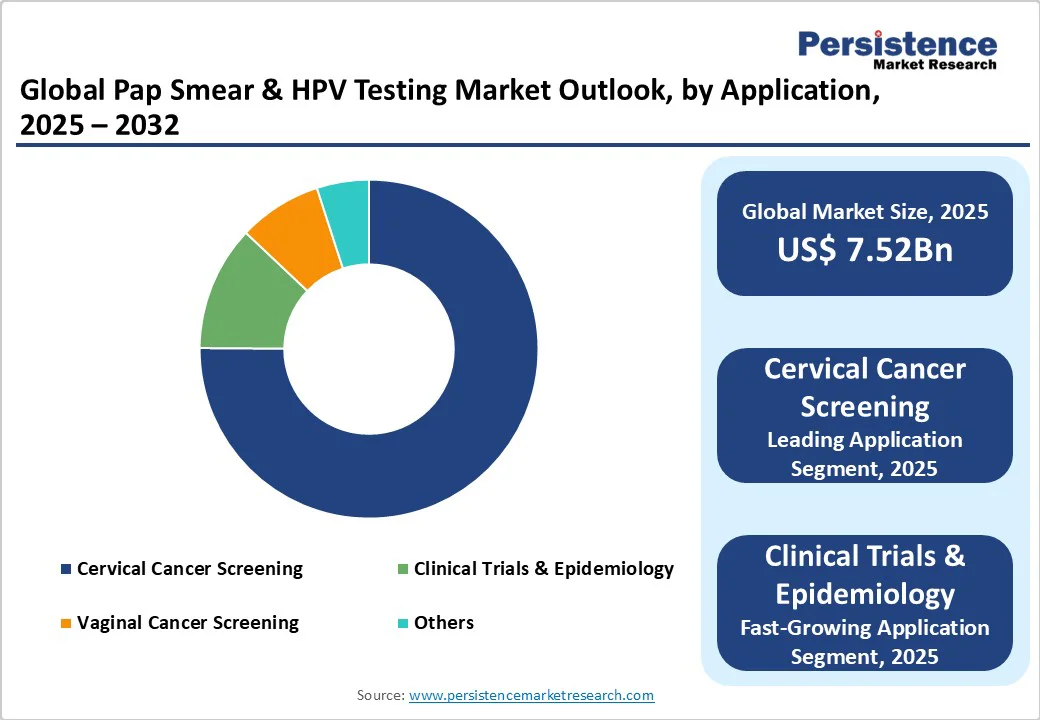

- Leading Application: Cervical Cancer Screening accounts for over 75.4% of market revenue, driven by global health campaigns and early detection initiatives.

| Key Insights | Details |

|---|---|

| Pap Smear & HPV Testing Market Size (2025E) | US$ 7.52 Bn |

| Market Value Forecast (2032F) | US$15.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 10.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 9.8% |

Market Dynamics

Driver: Rising Awareness and Government Initiatives for Cervical Cancer Screening

The Pap Smear & HPV Testing market is rapidly growing, driven by heightened global awareness of cervical cancer and expanding government screening programs. Cervical cancer remains a critical health challenge, with the World Health Organization estimating 660,000 new cases in 2024 alone. Early detection through Pap smear and HPV testing is vital for reducing mortality by identifying precancerous changes.

Governments worldwide are reinforcing screening efforts, such as the U.S. Preventive Services Task Force recommending routine HPV testing for women aged 30-65 and India’s Ayushman Bharat program, integrating cervical cancer screening into primary healthcare.

Industry leaders, such as Hologic, Inc., have reported increased sales of HPV testing kits in 2024, reflecting a rising demand. Innovations in high-sensitivity HPV tests, combined with robust public health campaigns promoting women’s health, are poised to sustain market momentum. These factors collectively ensure that the market will continue to expand steadily through 2032, thereby enhancing early detection and prevention worldwide.

Restraint: High Costs and Limited Access in Low-Income Regions

The Pap smear & HPV testing market faces notable challenges, primarily due to the high costs of advanced diagnostic technologies and limited healthcare access in low-income regions. Leading HPV testing instruments from companies such as QIAGEN and Roche require significant financial investment, which many healthcare facilities in developing countries cannot afford.

In 2024, the average cost of an HPV test ranged between $30 and $100, creating a substantial barrier in budget-constrained areas such as Sub-Saharan Africa.

Furthermore, the scarcity of trained healthcare professionals and inadequate medical infrastructure in rural and underserved regions limit the effective adoption of both Pap smear and HPV testing. These challenges are compounded by competition from low-cost alternatives such as visual inspection with acetic acid (VIA), which, although less accurate, offer a more affordable screening option. Collectively, these factors restrict market penetration and overall growth potential in cost-sensitive markets, slowing progress toward widespread cervical cancer screening.

Opportunity: Advancements in AI and Point-of-Care Testing

The integration of artificial intelligence (AI) with point-of-care (POC) testing is revolutionizing the market by enhancing diagnostic accuracy and accessibility. AI-driven platforms significantly enhance Pap smear analysis by minimizing human error and improving the detection of abnormal cells, resulting in earlier and more reliable diagnoses.

Leading companies, such as BD and Thermo Fisher Scientific, are pioneering AI-based software that automates slide analysis, thereby increasing efficiency and throughput in laboratories. Meanwhile, POC HPV testing devices from innovators such as NURX Inc. provide rapid, reliable results in remote or underserved areas, overcoming traditional accessibility barriers.

Government initiatives, including the EU’s Horizon 2020 program, are funding advancements in AI-driven diagnostics, fostering the development of cost-effective and scalable screening tools. These innovations are expected to drive market growth and improve cervical cancer screening outcomes globally through 2032, particularly in resource-limited settings.

Category-wise Insights

By Test Type

- HPV testing dominates the market, holding approximately 58.6% share in 2025, due to its superior sensitivity in detecting high-risk HPV strains linked to cervical cancer. Widely adopted in screening programs, HPV tests are favored for their ability to identify precancerous changes early. Companies such as QIAGEN and Roche lead with advanced molecular diagnostic kits, catering to demand in North America and Europe.

- Pap testing is the fastest-growing segment, driven by its widespread use in routine cervical cancer screening and increasing adoption in emerging economies. Its affordability and established infrastructure make it a preferred choice in regions such as the Asia Pacific, where companies such as Abbott are expanding their portfolios to meet growing demand.

By Product & Service

- Consumables & reagents segment leads contributing over 45.2% of revenue in 2025, driven by the recurring need for testing kits, reagents, and collection devices in Pap smear and HPV testing. High testing volumes in diagnostic laboratories and hospitals fuel demand, with key players such as Hologic, Inc., and BD offering comprehensive reagent portfolios.

- Software and AI platforms are the fastest-growing segment, propelled by advancements in automated diagnostic tools. AI-driven platforms enhance the accuracy of Pap smear analysis and streamline workflows in diagnostic labs. Companies such as Thermo Fisher Scientific are innovating with AI solutions to meet the growing demand for efficient and scalable diagnostics.

By Application

- Cervical cancer screening application dominates, accounting for over 75.4% of market revenue in 2025, driven by global health campaigns promoting early detection of cervical cancer. High screening rates in developed regions and government initiatives in emerging economies fuel demand, with players such as Quest Diagnostics supplying advanced testing solutions.

- The clinical trials & epidemiology segment is the fastest-growing, driven by increasing research on HPV-related diseases and vaccine development. Growing investments in clinical trials, particularly in North America and Europe, support demand for specialized testing services, with companies such as Seegene Inc. expanding offerings for epidemiological studies.

By End-use

- The hospitals & surgical clinics segment leads the market, contributing approximately 48.7% of revenue in 2025, due to high testing volumes and advanced diagnostic infrastructure.

- Hospitals are key centers for cervical cancer screening, with major players such as Abbott supplying instruments and reagents to meet demand.

- Home care is the fastest-growing segment, driven by the rise of self-sampling HPV testing kits. These kits improve accessibility, particularly in remote areas, with companies such as NURX Inc. and Femasys Inc. innovating to offer user-friendly, at-home testing solutions for women.

Regional Insights

North America Pap Smear & HPV Testing Market Trends

North America is projected to dominate the market, accounting for nearly 42.1% share in 2025. This leadership is fueled by the region’s advanced healthcare infrastructure, high cervical cancer screening rates, and a strong presence of key industry players, including Hologic, Inc., Quest Diagnostics, BD, and Abbott. These companies benefit from well-established distribution networks that supply hospitals, clinics, and diagnostic labs across the U.S. and Canada.

The U.S. healthcare system alone is expected to spend $5.7 trillion by 2026, according to the Centers for Medicare & Medicaid Services, supporting continued demand for screening technologies. In Canada, universal healthcare and national screening programs endorsed by organizations such as the Canadian Cancer Society promote routine Pap and HPV testing. Furthermore, growing consumer preference for high-sensitivity HPV tests, coupled with government funding for cancer prevention, bolsters the region’s dominance and drives innovation and accessibility in cervical cancer diagnostics.

Asia Pacific Pap Smear & HPV Testing Market Trends

Asia Pacific is the fastest-growing market for Pap smear and HPV testing, driven by its vast population base, rising healthcare investments, and increasing awareness of cervical cancer prevention. Countries such as China and India are spearheading regional growth through large-scale government screening initiatives.

China’s National Health Commission reported a screening coverage of 51.5% among women aged 35-64 in 2023-2024, significantly boosting demand for HPV testing kits. In India, the Ayushman Arogya Mandirs and National Health Mission (NHM) have screened over 10.18 crore (101.8 million) women aged 30-65 as of July 2025, underscoring strong public health engagement.

The region also benefits from an expanding diagnostic landscape, with local players such as Seegene Inc. and global giants like Roche and BD scaling up their operations. The growing prevalence of HPV-related diseases and robust government-led health campaigns further ensure that the Asia Pacific will remain a dominant and high-growth region in cervical cancer screening through 2032.

Europe Pap Smear & HPV Testing Market Trends

Europe stands as the second-fastest-growing region in the Pap smear and HPV testing market, driven by robust regulatory frameworks, rising awareness of cervical cancer prevention, and substantial investments in diagnostic innovation.

Countries such as Germany and the UK lead this momentum through well-established public health systems and organized screening programs. Germany’s robust diagnostic infrastructure and high adoption of molecular testing technologies support the expansion of HPV screening.

In the UK, the National Health Service (NHS) offers a nationwide cervical screening program, which encourages early detection and contributes to market growth. Leading diagnostic companies such as QIAGEN and Roche continue to innovate with advanced testing platforms and AI-driven tools.

Additionally, the EU’s Horizon 2025 program promotes cutting-edge research and development in digital and AI-enabled diagnostics, further enhancing demand for high-sensitivity and automated testing solutions. This combination of regulatory support, technological leadership, and public health initiatives positions Europe for sustained growth through 2032.

Competitive Landscape

The global Pap Smear & HPV Testing market is highly competitive, characterized by a mix of established players and innovative newcomers. Companies such as Abbott, QIAGEN, BD, and Hologic, Inc. dominate through extensive product portfolios and global distribution networks.

The Pap Smear & HPV Testing market is fragmented, with regional players such as Seegene Inc. focusing on localized offerings in the Asia Pacific. Key players are investing in AI-driven diagnostics and point-of-care testing to enhance market share, driven by demand for high-sensitivity HPV tests and automated Pap smear analysis.

Key Industry Developments:

- February 2025: Metropolis Healthcare and Roche Diagnostics India announced the launch of a self-sampling HPV DNA test for cervical cancer screening in India, aiming to improve early detection and expand access, particularly in smaller towns. This initiative seeks to address significant health challenges in India by providing women with a convenient, comfortable, and stigma-free way to undergo screening for cervical cancer.

- May 2025: Teal Health received FDA approval for its Teal Wand, the first and only at-home self-collection device for cervical cancer screening. The device, which collects vaginal samples to test for HPV, offers a more comfortable and convenient alternative to in-clinic screenings and aims to improve adherence to regular cervical cancer screening. The approval was supported by clinical trials showing high accuracy and a strong patient preference for the at-home method.

Companies Covered in Pap Smear & HPV Testing Market

- Abbott

- QIAGEN

- Becton dickinson and company

- Quest Diagnostics Incorporated

- Hologic, Inc.

- F. Hoffmann-La Roche Ltd

- Femasys Inc.

- Arbor Vita Corporation

- NURX Inc.

- Seegene Inc.

- Thermo Fisher Scientific Inc.

- BioMerieux

- Others

Frequently Asked Questions

The Pap Smear & HPV Testing market is projected to reach US$7.52 Bn in 2025.

Rising awareness, government-led screening programs, and advancements in diagnostic technologies are the key market drivers.

The Pap Smear & HPV Testing market is poised to witness a CAGR of 10.6% from 2025 to 2032.

Advancements in AI-driven diagnostics and point-of-care testing are the key market opportunities.

Abbott, QIAGEN, BD, Hologic, Inc., and F. Hoffmann-La Roche Ltd are key market players.