- Retail

- Battery Separator Paper Market

Battery Separator Paper Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Battery Separator Paper Market by Material Type (Polypropylene, Polyethylene, Others), End-user (Automotive, Industrial, Consumer Electronics, Others), and Regional Analysis for 2026 - 2033

Battery Separator Paper Market Size and Trends Analysis

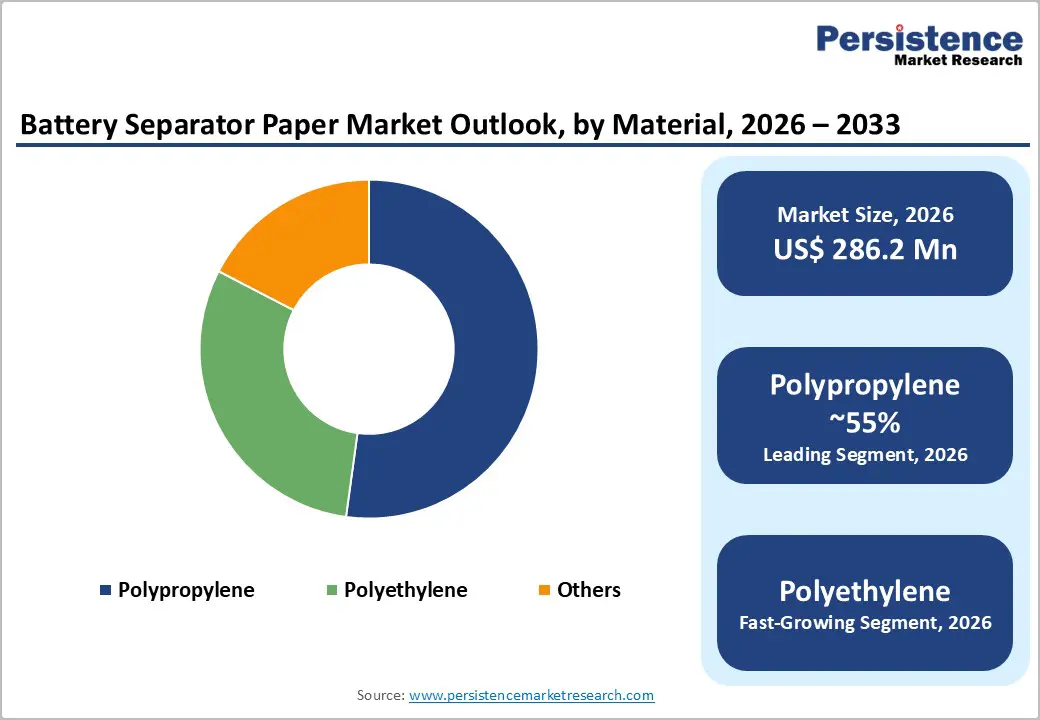

The global Battery Separator Paper market size is estimated to be valued at US$ 286.2 Mn in 2026 and is projected to reach US$ 384.3 Mn by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

The steady market expansion is primarily fueled by accelerating global demand for electric vehicles and energy storage systems, both of which rely critically on high-performance battery separator materials. According to the International Energy Agency (IEA), global electric car sales surpassed 17 million units in 2024, reflecting a year-on-year growth of over 25%. This electrification wave intensifies the need for polypropylene and polyethylene-based separator papers that ensure ionic conductivity and thermal safety within battery cells. Additionally, rising consumer electronics adoption and growing industrial energy storage deployments continue to reinforce demand across end-user segments, supporting consistent and long-term market growth.

Key Industry Highlights:

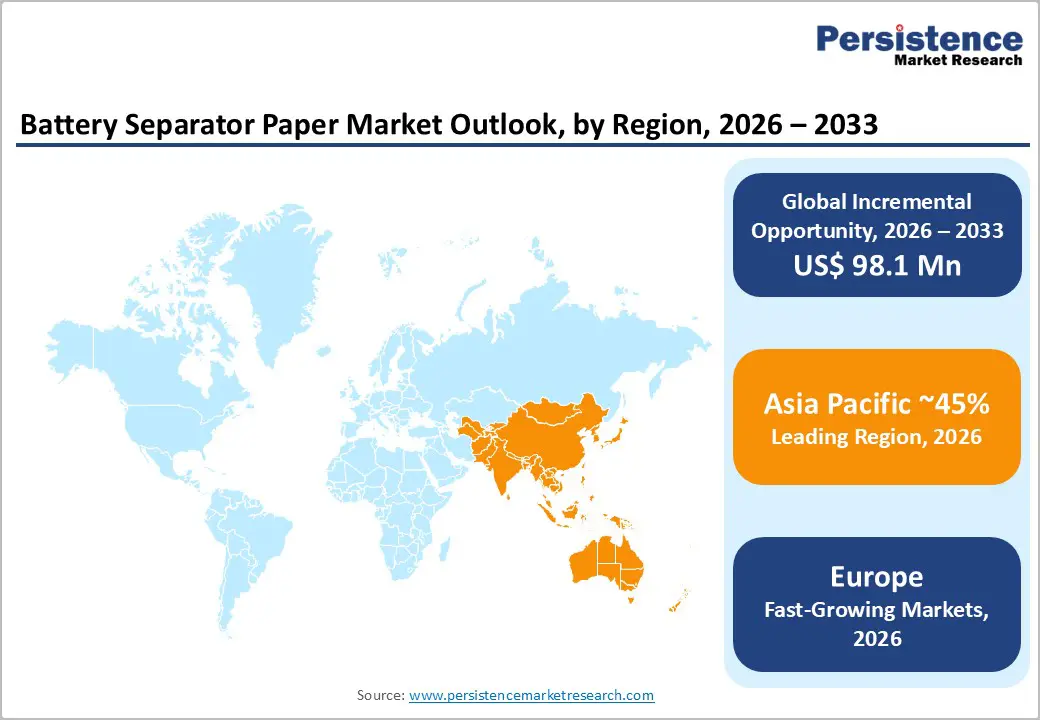

- Leading Region: Asia Pacific: Asia Pacific dominates the global battery separator paper market, led by China's commanding EV production base exceeding 11 million units in 2024 and Japan's advanced separator manufacturing ecosystem anchored by players such as Asahi Kasei Corporation and Toray Industries, Inc.

- Fastest Growing Region: North America: North America is the fastest growing regional market, driven by the U.S. Inflation Reduction Act, DOE-backed investments (e.g., ENTEK's US$ 1.2 Bn Indiana facility), and Asahi Kasei's CAD$ 1.7 Bn Canadian plant, collectively onshoring the EV battery separator supply chain.

- Dominant Material Segment: Polypropylene (Material Type): Polypropylene holds approximately 55% share in the material type category, driven by its superior thermal shutdown properties, chemical stability, cost competitiveness, and compatibility across diverse lithium-ion and lead-acid battery chemistries.

- Fastest Growing Segment: Polyethylene (Material Type): Polyethylene is the fastest growing material segment, gaining traction in advanced lithium-ion batteries due to its high ionic conductivity, thin-film flexibility, and suitability for next-generation high-energy-density EV applications and ceramic-coated composite separators.

- Key Market Opportunity: Advanced Separators and Policy-Backed Local Manufacturing: The convergence of EV supply chain localization policies (U.S. IRA, Canada ITC, EU Battery Regulation) and demand for ceramic-coated, high-performance separators in premium EVs offers a significant revenue opportunity for technically capable separator manufacturers to secure long-term offtake agreements.

| Key Insights | Details |

|---|---|

|

Battery Separator Paper Market Size (2026E) |

US$ 286.2 Mn |

|

Market Value Forecast (2033F) |

US$ 384.3 Mn |

|

Projected Growth CAGR (2026–2033) |

4.3% |

|

Historical Market Growth (2020–2025) |

3.6% |

Market Dynamics

Drivers - Rising Electric Vehicle Production Driving Separator Demand

The global transition towards electric mobility stands as the most powerful growth engine for the battery separator paper market. As highlighted by the International Energy Agency (IEA) in its Global EV Outlook 2025, electric car sales reached 17 million units in 2024, with a year-on-year increase exceeding 25%. Furthermore, total EV battery demand crossed the milestone of 1 TWh in 2024, representing a 25% increase over 2023.

Each lithium-ion and lead-acid battery cell incorporated in an electric vehicle mandates the use of at least one microporous separator paper a critical component that physically separates the anode and cathode while enabling ion transport. With projections pointing toward EV battery demand exceeding 3 TWh by 2030 (IEA), the battery separator paper market will benefit from compounding volumes across automotive applications globally.

Expanding Energy Storage Systems and Consumer Electronics Sector

The rapid deployment of grid-scale and residential energy storage systems presents a major secondary growth driver for battery separator papers. Renewable energy integration, particularly from solar and wind sources, requires reliable energy storage infrastructure, where lithium-ion batteries with high-performance separators serve as foundational components. Simultaneously, global consumer electronics adoption remains robust, with smartphones, laptops, tablets, and wearables each depending on safe and efficient battery cells.

According to the IEA Global EV Outlook 2025, battery storage demand encompassing both EV and stationary storage applications crossed 1 TWh in 2024, a historic milestone. Additionally, over 20 major car manufacturers representing more than 90% of global car sales in 2023 have committed to electrification targets, with combined projections estimating over 40 million electric cars sold by 2030. These structural demand trends across automotive, industrial, and consumer end-user segments create sustained upstream pull for battery separator paper manufacturers.

Restraint - Volatility in Raw Material Prices

One of the most persistent challenges facing the battery separator paper market is the inherent price volatility of key raw materials, particularly polypropylene (PP) and polyethylene (PE). Both polymers are downstream derivatives of petroleum feedstocks and, therefore, closely linked to crude oil price fluctuations. Any disruption in petrochemical supply chains, whether from geopolitical tensions, refinery outages, or regulatory constraints, can significantly escalate production costs for separator manufacturers.

For smaller and mid-tier producers, passing on these cost increases to customers, primarily battery cell manufacturers operating on thin margins, proves challenging. This price sensitivity can affect profitability, discourage capacity expansions, and create planning uncertainty, ultimately constraining market growth, particularly in cost-sensitive emerging economies.

Competitive Threat from Alternative Battery Technologies

Emerging next-generation battery technologies present a structural risk to the conventional battery separator paper market. Solid-state batteries, which replace liquid electrolytes with solid alternatives, have the potential to eliminate the need for traditional porous polymer separators altogether. Several leading automotive and technology players, including Toyota Motor Corporation, QuantumScape Corporation, and Samsung SDI Co., Ltd., are actively investing in solid-state battery development, with commercialization timelines targeting the late 2020s to early 2030s.

As solid-state batteries approach pilot and commercial production stages, demand for conventional polyolefin-based separators especially in the premium EV segment could face gradual substitution, posing a medium-to-long-term restraint on market expansion for existing battery separator paper manufacturers.

Opportunity - Ceramic-Coated and Advanced Functional Separators for EV Applications

The accelerating premium electric vehicle segment offers a significant opportunity for manufacturers capable of offering advanced ceramic-coated and functionalized battery separator papers. Ceramic-coated separators deliver superior thermal stability, enhanced electrolyte compatibility, and reduced shrinkage at elevated temperatures all critical for ensuring battery safety in high-performance EV applications. Leading players such as Asahi Kasei Corporation (through its Hipore™ technology) and ENTEK International, LLC already offer high-performance coated separators.

ENTEK received a conditional commitment in July 2024 and a direct loan of up to US$ 1.2 billion from the U.S. Department of Energy's (DOE) Loan Programs Office to construct a new PE-based battery separator manufacturing facility in Terre Haute, Indiana, with a planned annual capacity of 1.72 billion square meters. As EV manufacturers push toward higher energy density and safer battery architectures, demand for premium-tier separator products represents a fast-growing, value-accretive opportunity for market participants willing to invest in innovation and scale.

Government Policy Support and Localization of Battery Supply Chains

Strong government policy frameworks in key economies are creating unprecedented opportunities for battery separator paper manufacturers to establish or expand local production capacities. In North America, the U.S. Inflation Reduction Act (IRA) and Canada's Clean Technology Manufacturing Investment Tax Credit are incentivizing domestic battery supply chain build-out.

The U.S. Department of Energy (DOE) estimates that by 2030, the North American lithium-ion EV battery industry will require annual separator production of 7 to 10 billion square meters. In Europe, the European Battery Alliance envisions total battery production capacity reaching 773 GWh by 2030, up from 69 GWh in 2022, fueling enormous demand for separator materials. These policy signals translate into long-term, government-backed procurement pipelines for battery separator paper producers who can align capacity additions with regional demand centers.

Category-wise Analysis

Material Type Insights

Polypropylene (PP) commands the leading position in the battery separator paper market by material type, accounting for approximately 55% of total market share. Its dominance is underpinned by a compelling combination of superior chemical stability, high melting point, and well-established wet and dry-process manufacturing compatibility. PP separators exhibit excellent thermal shutdown properties a critical safety mechanism that causes pore closure at elevated temperatures to prevent thermal runaway in battery cells, making them a preferred choice in automotive and industrial applications.

The material's proven compatibility with both lithium-ion and lead-acid battery chemistries further broadens its addressable market. Additionally, polypropylene's cost-effectiveness relative to alternative advanced materials enables high-volume manufacturing at competitive price points, supporting widespread adoption across OEM battery supply chains. Polyethylene (PE), while currently holding a secondary market position, is the fastest-growing segment due to its high ionic conductivity, mechanical flexibility in thin-film formats, and suitability for next-generation battery architectures including solid-state hybrids and high-energy-density EV cells.

End-user Insights

The automotive segment dominates the battery separator paper market by end-user category, representing approximately 49% of total market share. This leadership is directly attributable to the rapid global electrification of passenger and commercial vehicles. As documented by the International Energy Agency (IEA), global EV battery demand reached over 950 GWh in 2024 a 25% increase over 2023 translating into enormous procurement volumes for automotive-grade battery separators.

High-performance requirements in this segment including thermal stability, mechanical strength, and precise pore size distribution drive demand for premium separator materials and coatings, creating both volume and value leadership. Battery separators in EVs must maintain structural integrity across wide temperature ranges and hundreds of charge-discharge cycles. The Industrial segment, encompassing grid-scale energy storage, UPS systems, and backup power applications, represents the second-largest end-user category and is projected to grow at an above-average pace through 2033, driven by renewable energy integration mandates globally.

Regional Insights and Trends

North America Strengthening Domestic Battery Separator Manufacturing Ecosystem

North America is one of the most strategically active regions in the battery separator paper market, underpinned by robust policy incentives and accelerating domestic battery supply chain investment. The U.S. Inflation Reduction Act (IRA), signed into law in 2022, provides substantial tax credits for domestic battery component manufacturing, incentivizing localized production of separator materials. The U.S. Department of Energy (DOE) has issued direct loans totaling up to US$ 1.2 billion to ENTEK International, LLC for its new PE-based separator plant in Terre Haute, Indiana, highlighting government's commitment to domestic separator supply security. Furthermore, ENTEK's facility, expected to produce up to 1.72 billion square meters of separator annually, positions the U.S. as a self-sustaining separator manufacturing hub.

In Canada, Asahi Kasei broke ground in November 2024 on a CAD$ 1.7 billion integrated separator manufacturing facility in Port Colborne, Ontario, in a joint venture with Honda Motor Co., Ltd.. This facility, supported by Canada's Clean Technology Manufacturing Investment Tax Credit and the Development Bank of Japan (DBJ), is expected to produce approximately 700 million square meters of coated lithium-ion battery separator annually by 2027. Collectively, these developments underscore North America's transformation into a major separator production and consumption hub.

EU Regulations and Gigafactories Driving Separator Demand

Europe's battery separator paper market is experiencing structural shifts driven by aggressive gigafactory development programs and stringent European Union (EU) regulatory mandates on zero-emission vehicles. The European Battery Alliance (EBA) projects total battery production capacity in Europe to reach 773 GWh by 2030, up significantly from 69 GWh in 2022, creating enormous upstream demand for separator materials. The EU CO2 emission standards for cars require automakers to progressively increase zero-emission vehicle sales, making EV battery supply chain localization an industrial and regulatory imperative.

Key markets including Germany, France, and Spain are seeing growing EV assembly and battery cell manufacturing investments, translating into rising domestic separator procurement. However, the European market also faces near-term headwinds: EV sales in Europe stagnated in 2024 as government subsidies were phased out in several major markets, including Germany (where EV subsidies ended in late 2023) and France. Despite this, the longer-term policy trajectory including the EU's 2035 ban on new internal combustion engine vehicle sales ensures continued separator demand growth over the forecast period, creating a stable, policy-backed demand environment for market players.

Asia Pacific Leads Global Battery Separator Paper Demand

Asia Pacific dominates the global battery separator paper market and is expected to maintain its leadership throughout the forecast period. China is the world's largest EV market, with electric car sales exceeding 11 million units in 2024 alone more than total global EV sales just two years prior driven by competitive pricing, government incentives including a trade-in subsidy scheme, and a well-integrated domestic battery supply chain. China accounts for approximately 85% of global battery cell manufacturing capacity, creating massive domestic demand for separator papers. Leading local and international manufacturers including Sinoma Lithium Film Co., Ltd. and SK Innovation Co., Ltd. are prominent in serving China's battery supply chain.

In Japan, established players such as Asahi Kasei Corporation, Toray Battery Separator Film Korea Limited, and Mitsubishi Paper Mills, Ltd. continue to invest in separator technology, with a focus on premium wet-process and ceramic-coated products. India's battery separator demand is accelerating, fueled by the government's Production Linked Incentive (PLI) scheme for advanced chemistry cell batteries and rising EV sales registrations grew 70% year-on-year in 2023 according to IEA. ASEAN markets including Thailand, where EV sales share reached 13% in 2024, and Indonesia are emerging as additional demand centers, reinforcing Asia Pacific's role as the global epicenter of battery separator paper production and consumption.

Competitive Landscape

The global battery separator paper market exhibits a moderately consolidated competitive structure, with a handful of technologically advanced players primarily headquartered in Japan, South Korea, and the United States accounting for a significant share of global output. Key differentiators among market leaders include proprietary wet-process and dry-process manufacturing capabilities, ceramic coating technologies, and long-term supply agreements with major battery cell manufacturers and automotive OEMs.

Companies are pursuing capacity expansions, joint ventures, and technology licensing as primary growth strategies. Vertically integrated players enjoy supply chain advantages, while specialist producers compete on the basis of product quality, customization, and customer intimacy. Emerging business models increasingly feature long-term offtake agreements directly with EV battery manufacturers, ensuring demand visibility. R&D investment in ultra-thin, high-porosity, and multi-layer separator technologies is intensifying across the competitive field.

Key Developments:

- In November 2024, Asahi Kasei Corporation broke ground on a CAD$ 1.7 billion lithium-ion battery separator manufacturing facility in Port Colborne, Ontario, Canada, in a joint venture with Honda Motor Co., Ltd., with a planned capacity of 700 million square meters annually commencing in 2027.

- In November 2024, ENTEK International, LLC received a direct loan of up to US$ 1.2 billion from the U.S. Department of Energy's Loan Programs Office to finance a new PE-based lithium-ion battery separator plant in Terre Haute, Indiana, designed for primary use in EV batteries.

- In January 2024, Toray Industries, Inc. announced the development of a new battery separator film using ultra-high molecular weight polyethylene (UHMWPE), offering mechanical strength comparable to stainless steel, aimed at enhancing safety in next-generation EV and energy storage batteries.

Companies Covered in Battery Separator Paper Market

- Ahlstrom

- Asahi Kasei Corporation

- Bernard Dumas

- Dow, Inc.

- Eaton Corporation plc

- ENTEK International, LLC

- Freudenberg Performance Materials

- Mitsubishi Paper Mills, Ltd.

- Sinoma Lithium Film Co., Ltd.

- SK Innovation Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Teijin Limited

- Toray Battery Separator Film Korea Limited

- UBE Corporation

- W-Scope Corporation

- Other Market Players

Frequently Asked Questions

The global Battery Separator Paper market is estimated to be valued at US$ 286.2 Mn in 2026 and is projected to reach US$ 384.3 Mn by 2033, expanding at a CAGR of 4.3% over the 2026–2033 forecast period. The market was valued at US$ 231.5 Mn in 2020, having grown at a historical CAGR of 3.6% from 2020 to 2025.

The primary demand drivers are the rapid global adoption of electric vehicles (EVs), with IEA reporting over 17 million EV sales in 2024, and the accelerating deployment of stationary energy storage systems. Growing consumer electronics production and industrial backup power applications also contribute meaningfully to sustained demand for battery separator papers across polypropylene and polyethylene material segments.

Polypropylene (PP) is the leading material segment in the battery separator paper market, accounting for approximately 55% of market share. Its dominance is attributed to superior thermal shutdown functionality, chemical stability, cost-effectiveness, and compatibility with diverse battery chemistries, including lithium-ion and lead-acid systems used in automotive and industrial applications.

Asia Pacific is the leading region in the global battery separator paper market. China with EV sales exceeding 11 million units in 2024 and commanding over 85% of global battery cell manufacturing capacity, drives the region's dominance. Japan, South Korea, and India are additional significant contributors, supported by advanced manufacturing ecosystems and growing EV adoption underpinned by national policy incentives.

The most significant growth opportunity lies in policy-backed localization of battery separator production, particularly in North America (driven by the U.S. IRA and Canada's Clean Technology ITC) and Europe (backed by the EU Battery Alliance's 773 GWh capacity target by 2030). Concurrently, rising demand for ceramic-coated and advanced functional separator papers in premium EV and energy storage applications offers a high-value product opportunity for technologically advanced manufacturers.