- Specialty & Fine Chemicals

- Chemicals for Paper Recycling Market

Chemicals for Paper Recycling Market Size, Share, and Growth Forecast, 2025 - 2032

Chemicals for Paper Recycling Market By Chemical Type (Deinking Chemicals, Bleaching Agents, Others), Application (Recycled Paper Products, Newsprint, Others), Form, End-use, and Regional Analysis for 2025 – 2032

Chemicals for Paper Recycling Market Size and Trends Analysis

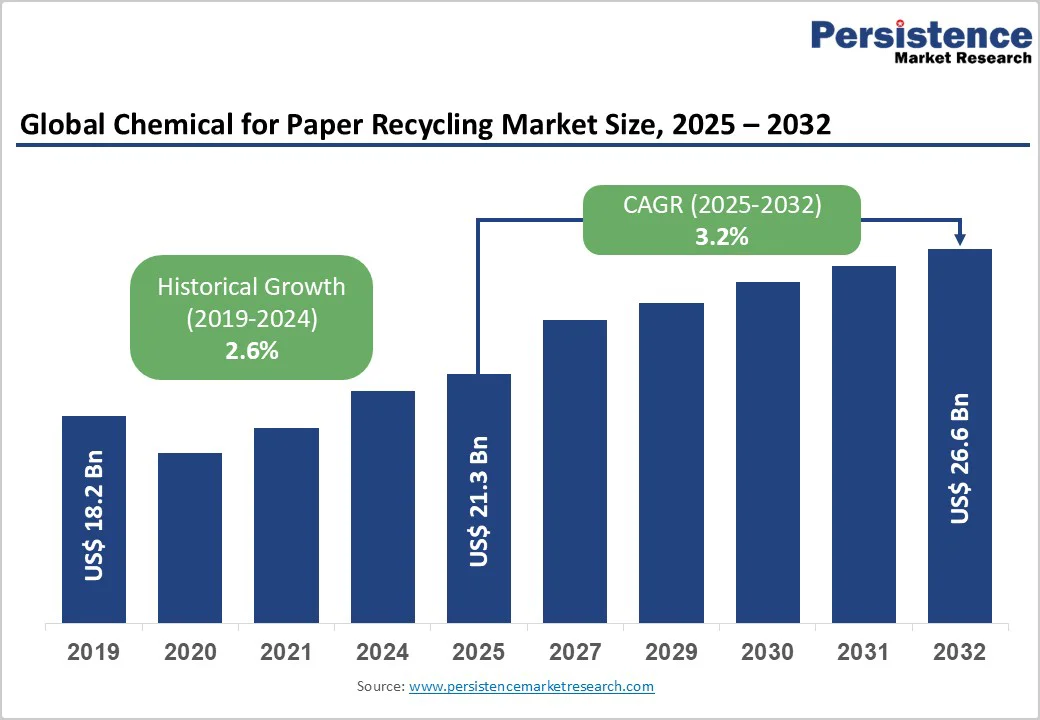

The global chemicals for paper recycling market size is likely to be valued US$21.3 Billion in 2025, estimated to US$26.6 Billion by 2032, growing at a CAGR of 3.2% during the forecast period from 2025 to 2032, driven by the increasing prevalence of sustainable practices, rising consumer preference for eco-friendly paper products, and advancements in recycling technologies. The need for efficient deinking and bleaching, particularly in packaging, has significantly boosted the adoption of chemicals for paper recycling across various demographics. The market is further propelled by innovations in bio-based and low-impact formulations, catering to consumer preferences for sustainable and effective options. The growing acceptance of chemicals for paper recycling as an alternative to virgin materials, particularly for producers seeking cost savings, is a key growth factor.

Key Industry Highlights:

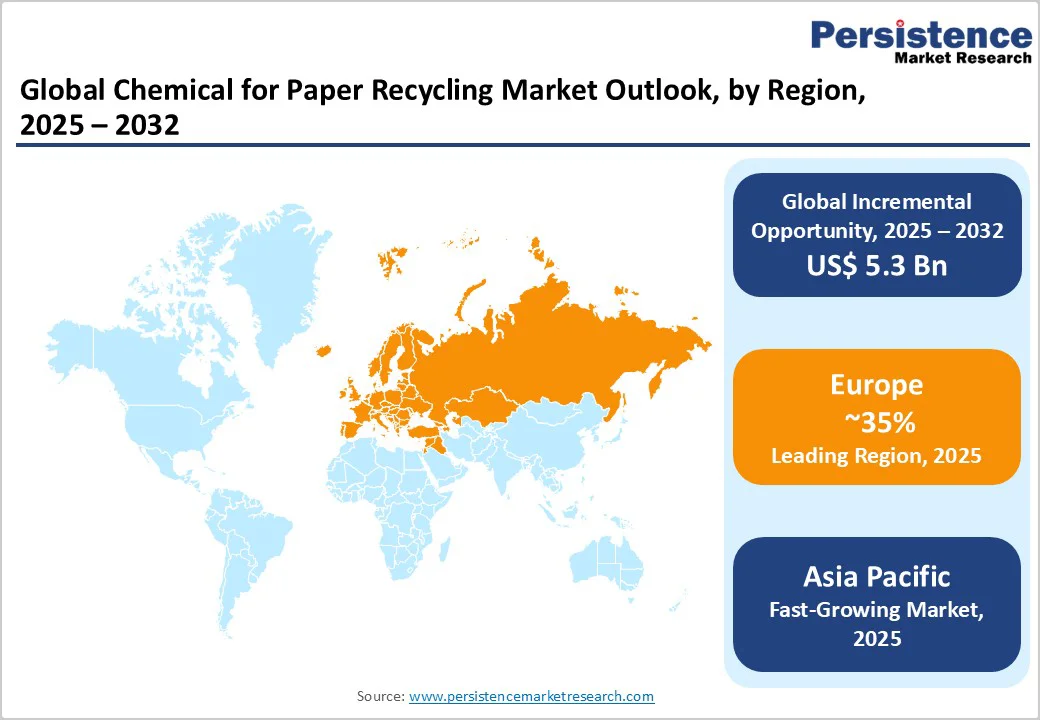

- Leading Region: Europe, commanding a 35% market share in 2025, driven by advanced recycling infrastructure, high prevalence of sustainable practices, and strong R&D activities in Germany.

- Fastest-growing Region: Asia Pacific, fueled by increasing industrialization, rising awareness of recycling, and growing investments in paper innovation in countries China and India.

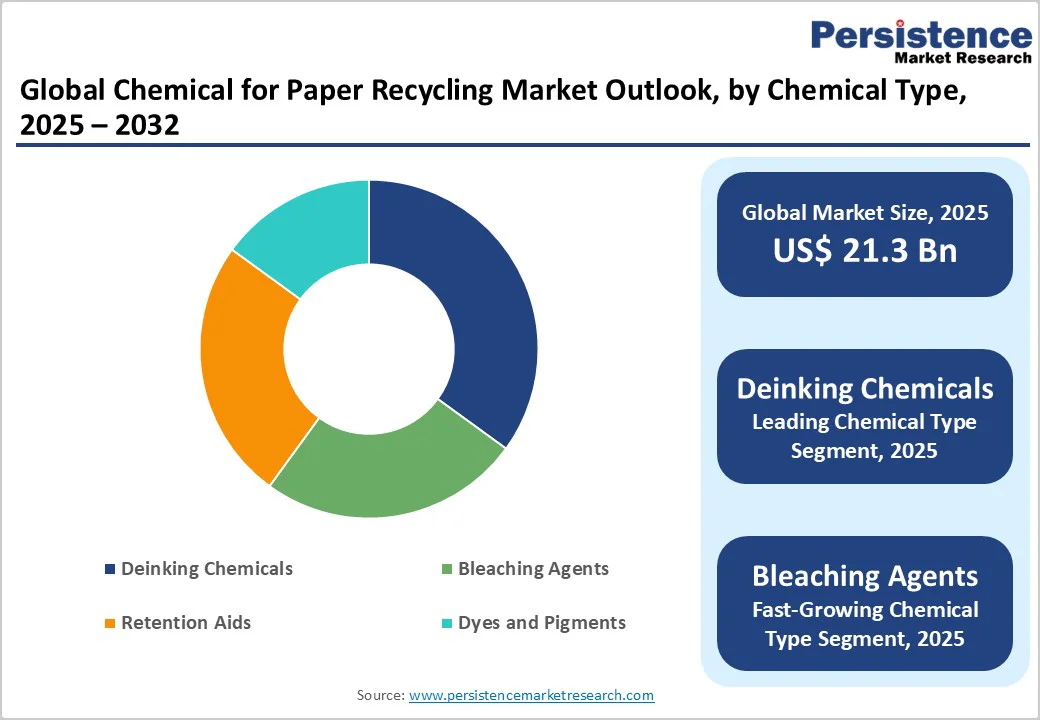

- Dominant Chemical Type: Deinking Chemicals, holding approximately 30% of the market share, due to its critical role in removing inks and contaminants.

- Leading Application: Packaging, accounting for over 40% of market revenue, driven by the need for high-quality recycled materials.

- Leading Form: Liquid, contributing nearly 50% of market revenue, due to their widespread accessibility and ease of use.

- Key Market Driver: Increasing global mandates for waste reduction and recycled content in packaging are boosting demand for chemicals that enhance fiber recovery, de-inking, and bleaching efficiency.

- Market Opportunity: Growing demand for eco-friendly de-inking and bleaching agents opens avenues for bio-based, low-toxicity chemical innovations.

| Key Insights | Details |

|---|---|

| Chemicals for Paper Recycling Market Size (2025E) | US$21.3 Bn |

| Market Value Forecast (2032F) | US$26.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Sustainable Practices and Demand for Eco-Friendly Paper Products

The increasing prevalence of sustainable practices globally is a primary driver of the chemicals for paper recycling market. Recycling efforts affect a significant portion of paper production worldwide, with a higher prevalence in developed regions. This widespread initiative creates a substantial demand for effective and efficient chemicals. Chemicals for paper recycling offer superior deinking and bleaching, typically more effective than traditional methods, making them ideal for producers seeking improved quality. This is particularly critical for industries with high demand for recycled paper.

The growing adoption of deinking chemicals, such as those marketed by companies BASF SE, has gained traction due to their proven efficacy in trials, with many users reporting improved fiber quality. Additionally, the rise in awareness and the increasing availability of eco-friendly chemicals in industrial mills have boosted access, further driving market expansion. The surge in demand for sustainable solutions, coupled with innovations in bio-based formulations, continues to propel the market forward, particularly in developed regions with advanced recycling systems.

High Development and Regulatory Costs

The high costs associated with the development and regulatory approval of chemicals for paper recycling pose a significant restraint on market growth. Developing these chemicals requires advanced technologies, rigorous testing, and specialized components to ensure efficacy and safety. These processes involve substantial financial investment, often exceeding millions of dollars, which can be a barrier for smaller companies and startups entering the market. Additionally, regulatory bodies impose stringent requirements for approval, including extensive safety and efficacy testing. Compliance with these standards, along with the need for specialized manufacturing facilities, increases overall costs and extends development timelines.

For instance, the approval process for new deinking chemicals can take several years, with costs escalating due to multiple phases of trials and post-market surveillance requirements. Smaller firms often struggle to meet these financial demands, limiting their ability to compete with established players BASF SE and Dow Inc. Furthermore, the complexity of integrating advanced features, such as bio-based elements, adds to production costs, which can deter innovation and slow market expansion, particularly in cost-sensitive regions.

Advancements in Bio-Based and Eco-Friendly Formulations

Advancements in bio-based and eco-friendly formulations present significant growth opportunities for the chemicals for paper recycling market. Bio-based chemicals reduce environmental impact, making them a preferred choice for producers concerned with sustainability. These formulations align with growing demand for greener options. Additionally, eco-friendly designs that integrate advanced features, such as improved retention, offer enhanced efficacy by targeting specific recycling needs, providing more comprehensive solutions.

For example, companies BASF SE and Dow Inc. are investing in R&D to develop bio-based chemicals that combine sustainability with advanced technology. These innovations reduce development timelines and costs by leveraging modular approaches that can be adapted for various needs. Furthermore, the integration of smart features, such as optimized dosing, is enhancing the precision and efficiency of chemicals, improving satisfaction. As the demand for sustainable and effective recycling grows, these advancements are expected to drive market expansion, particularly in regions with high environmental focus, such as Europe and North America.

Category-wise Analysis

Chemical Type Insights

Deinking chemicals dominates the market, expected to account for approximately 30% of the share in 2025. Its dominance is driven by its efficiency, effectiveness, and cost-effectiveness, making it a preferred choice for recycling processes. Deinking chemicals, such as those offered by Dow Inc., are highly effective in removing contaminants, with designs ensuring quality during use. Its ability to offer clean fibers and its compatibility with various papers make it a preferred choice for both producers and manufacturers.

Bleaching agents is the fastest-growing segment, driven by its eco-friendly properties and increasing adoption in sustainable formulations. Bleaching agents offer brightness and purity, making them appealing for high-quality paper. The growing focus on sustainability and the development of bleaching-based innovative designs are further accelerating its adoption, particularly in Europe and North America.

Application Insights

Recycled paper products leads the market, holding 40% of the share in 2025. Their dominance stems from their versatility, accessibility, and immediate use, making them suitable for a wide range of producers. Recycled paper products are widely used due to their efficiency and growing demand.

Tissue paper is the fastest-growing segment, driven by the rise of hygiene products and increasing adoption in consumer goods. The convenience of soft textures, coupled with advanced features, is driving rapid adoption.

Form Insights

Liquid leads the market, holding approximately 50% of the share in 2025. Their dominance stems from their ease, accessibility, and immediate application, making them suitable for a wide range of processes. Liquid forms are widely used due to their convenience and efficiency.

Powder is the fastest-growing segment, driven by the rise of compact storage and increasing preference for dry applications. The convenience of long shelf life, coupled with cost savings, is driving rapid adoption. The Asia Pacific region, with its growing infrastructure, is a key contributor to this segment’s growth.

End-use Insights

Packaging dominates the market, contributing nearly 40% of revenue in 2025. Their widespread accessibility, coupled with the growing availability of recycled materials, drives their dominance. Packaging offers durability and versatility, making it the preferred choice for producers seeking sustainable solutions.

Tissue Production is the fastest-growing segment, fueled by the rise of hygiene demands and increasing consumer focus on soft products. The convenience of high-quality options, coupled with innovations, is driving rapid adoption.

Regional Insights

Europe Chemicals for Paper Recycling Market Trends

Europe accounts 35% share in 2025, supported by strong regulatory frameworks and collaborative research initiatives. Leading countries such as Germany, France, and Italy are driving market growth through investments in chemical innovation and increasing awareness of recycling efficiency. The European Chemicals Agency (ECHA) supports the development of advanced formulations, with companies such as BASF SE focusing on eco-friendly bleaching agents.

The high prevalence of paper recycling, particularly in Western Europe, and the growing demand for high-quality recycled products are key drivers. Europe’s focus on circular economy and sustainable production further strengthens its market position, ensuring steady growth in the forecast period.

North America Chemicals for Paper Recycling Market Trends

North America is projected to account for nearly 25% of the global Chemicals for Paper Recycling Market in 2025, driven by high recycling rates and advanced paper mills in the U.S. The U.S. market is characterized by robust R&D activities, with companies such as Eastman Chemical Company leading innovations in deinking chemicals.

The high consumption of recycled paper, coupled with strong environmental policies, fuels demand for efficient chemicals. The rise in bio-based formulations and the availability of advanced retention aids in industrial mills further drive market growth. Additionally, the rise in sustainable packaging, supported by private investments, positions the U.S. as a leader in market innovation and adoption.

Asia Pacific Chemicals for Paper Recycling Market Trends

Asia Pacific is the fastest-growing market for chemicals for paper recycling, driven by increasing industrialization and rising paper consumption in countries China and India. China’s chemical industry is expanding rapidly, with companies such as Mitsubishi Chemical Corporation investing in cost-effective deinking solutions.

India’s growing recycling infrastructure and increasing prevalence of sustainable practices, particularly in urban areas, are boosting demand for affordable and efficient chemicals. The rise of industrial mills and government initiatives to improve recycling rates are further accelerating market growth. Additionally, the adoption of granular forms and the growing focus on tissue production are creating substantial opportunities for market expansion in the region.

Competitive Landscape

The global chemicals for paper recycling market is highly competitive, characterized by a mix of global chemical giants and specialized firms. In developed regions North America and Europe, large players such as BASF SE, Dow Inc., and Eastman Chemical Company dominate through advanced R&D capabilities and established supply chains. In the Asia Pacific, regional players such as Mitsubishi.

Chemical Corporation are gaining traction by offering cost-effective solutions tailored to local markets. Companies are focusing on product innovation, such as bio-based and eco-friendly chemicals, to gain a competitive edge. Strategic partnerships, acquisitions, and investments in sustainable technologies are further intensifying the competitive landscape.

Key Industry Developments

- In February 2024, Kemira launched biomass-balanced wet strength resins and polyamines (ISCC PLUS certified) for the paper industry, enabling a transition to more renewable-based materials in paper chemicals.

- In August 2025, Eastman Chemical Company (US) announced a partnership with a leading paper manufacturer to develop a new line of biodegradable chemicals specifically designed for paper recycling. This strategic move not only aligns with the growing demand for sustainable solutions but also positions Eastman as a frontrunner in the eco-friendly chemicals segment.

Frequently Asked Questions

The global chemicals for paper recycling market is projected to reach US$21.3 Billion in 2025.

The surge in e-commerce packaging and advancements such as enzyme-based de-inking and bio-based additives are driving the adoption of sustainable paper recycling chemicals.

The market is poised to witness a CAGR of 3.2% from 2025 to 2032.

Integration of bio-based chemicals and digital process optimization are key opportunities.

BASF SE, Dow Inc., Eastman Chemical Company, Solvay SA, and SABIC are key players.