- Industrial Machinery

- Paper Slitting Machine Market

Paper Slitting Machine Market Size, Share, and Growth Forecast 2026 - 2033

Paper Slitting Machine Market by Blade Type (Razor Blade, Shear Blade, Air Score Blade), Technology (Manual, Semi-Automatic, Fully Automatic), and Regional Analysis for 2026 - 2033

Paper Slitting Machine Market Size and Trend Analysis

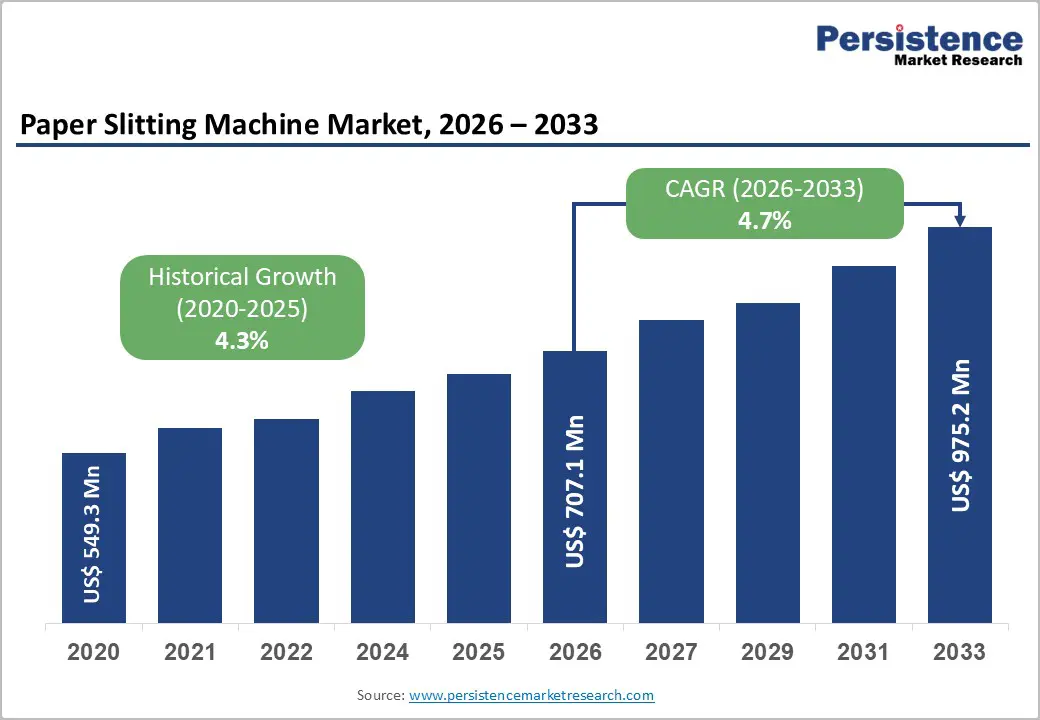

The global Paper Slitting Machine market size is supposed to be valued at US$ 707.1 million in 2026 and is projected to reach US$ 975.2 million by 2033, growing at a CAGR of 4.7% between 2026 and 2033. The market's consistent and sustained growth is driven by the global packaging industry's accelerating expansion, the revival of paper and paperboard consumption across e-commerce fulfillment and sustainable packaging applications, and the manufacturing sector's growing investment in precision converting and automation technologies.

Key Industry Highlights:

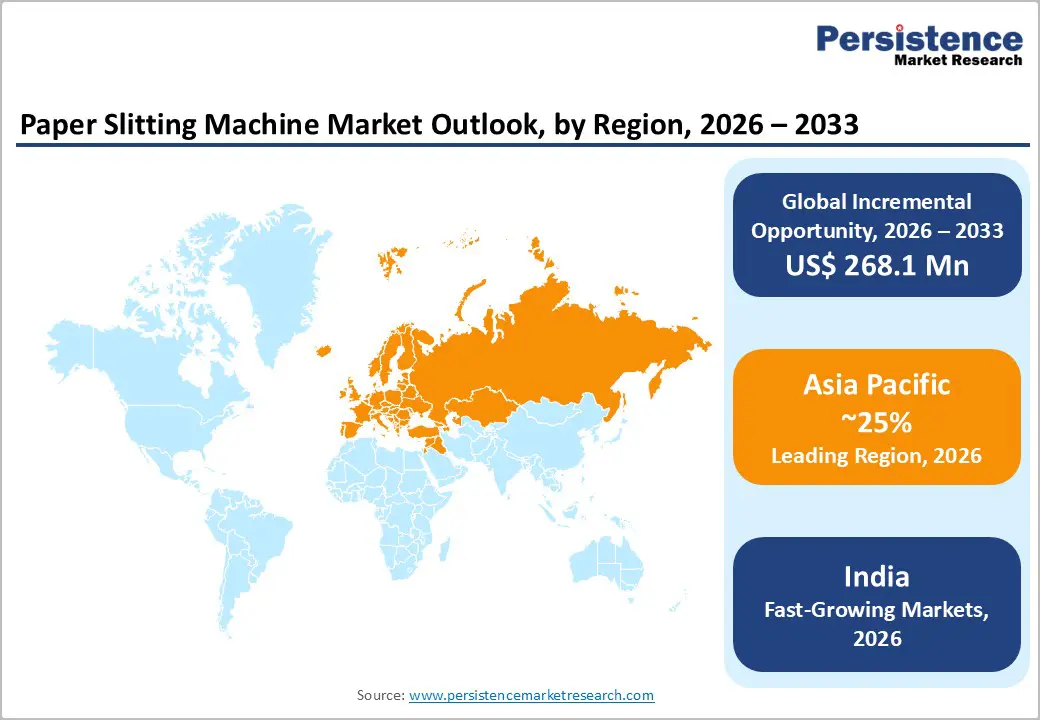

- Dominant Region: Asia Pacific leads the global Paper Slitting Machine market with China accounting for approximately 25% of world paper and paperboard output per the FAO, and India's expanding paper packaging sector, driven by BIS paper packaging mandates, generating the region's highest incremental slitting machine procurement volumes across new mill installations and converting capacity expansion programs.

- Growing Region: India is identified as the highest-growth national market driven by BIS-mandated paper packaging adoption, the PLI Scheme for allied sectors, and rapid tissue and specialty paper manufacturing capacity expansion, sustaining accelerating paper slitting machine procurement demand.

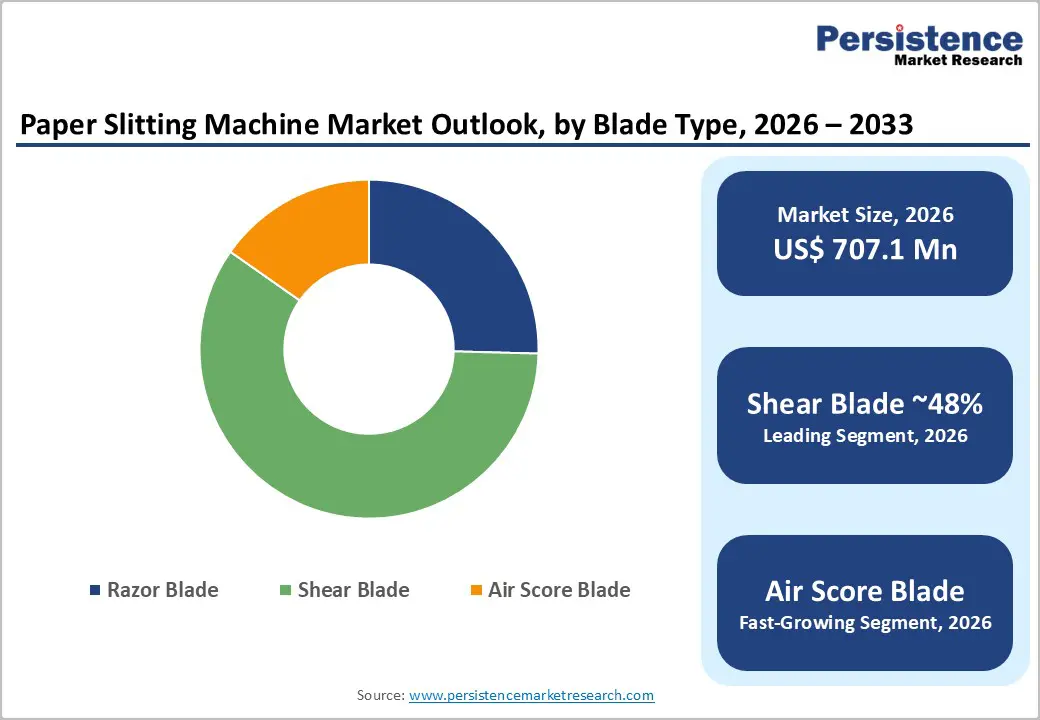

- Dominant Blade Type: Shear Blade systems dominate the Blade Type segment with approximately 48% market share in 2026, driven by their unmatched slit-edge quality, widest basis weight handling range (12–500+ gsm), and mandatory specification in pharmaceutical, food-grade, and electronics-grade paper converting applications governed by TAPPI technical guidelines.

- Dominant Technology: Fully Automatic technology is the dominant and fastest-growing segment with approximately 55% revenue share, validated by the IFR's confirmation of sustained double-digit packaging automation investment growth, with Industry 4.0 connectivity, servo tension control, and OPC-UA integration driving preference for automated over manual and semi-automatic slitting systems across premium converters globally.

- Market Opportunity: Specialty paper applications, including battery separator papers, release liners, and medical packaging grades, represent the key high-value market opportunity, requiring ±0.1 mm width tolerance precision only achievable with advanced shear and razor blade slitting systems, commanding significant machine price premiums and generating disproportionate revenue contribution for technically capable European machine manufacturers.

| Key Insights | Details |

|---|---|

|

Paper Slitting Machine Market Size (2026E) |

US$ 707.1 Million |

|

Market Value Forecast (2033F) |

US$ 975.2 Million |

|

Projected Growth CAGR (2026–2033) |

4.7% |

|

Historical Market Growth (2020–2025) |

4.3% |

Market Dynamics

Drivers - Global E-Commerce Boom and Sustainable Packaging Transition Expanding Paper Slitting Equipment Demand

The structural and permanent expansion of global e-commerce, generating an unprecedented surge in demand for corrugated boxes, kraft paper tape, paper cushioning, and flexible paper packaging materials, is directly amplifying procurement demand for high-throughput paper slitting machines across paper mills, converting plants, and packaging manufacturers worldwide. The International Post Corporation (IPC) documented that global parcel volumes in the cross-border e-commerce sector grew by approximately 11% in 2023, a trend that directly translates into higher paper and paperboard consumption requiring precision slitting before downstream converting and packaging operations.

The European Union's Single-Use Plastics Directive and growing corporate sustainability mandates are accelerating the global substitution of plastic films with paper-based packaging alternatives, expanding the addressable material volumes flowing through paper slitting operations across Europe and beyond. The Confederation of European Paper Industries (CEPI) reported that European paper and packaging production continues to grow steadily, sustaining investment in paper slitting capacity upgrades to serve premium food, pharmaceutical, and consumer goods packaging customers demanding tighter width tolerances and superior slit-edge quality.

Industry 4.0 Integration and Productivity Optimization Driving Upgrade Cycles for Automated Slitting Systems

The global manufacturing sector's accelerating adoption of Industry 4.0 automation, real-time machine performance monitoring, and predictive maintenance capabilities is generating a powerful investment cycle in technologically advanced paper slitting machines that replace legacy manual and semi-automatic equipment with fully servo-controlled, digitally networked slitting rewinder systems. Modern fully automatic paper slitting machines from manufacturers including Kampf Schneid- und Wickeltechnik GmbH & Co. KG and GOEBEL Schneid und Wickelsysteme GmbH incorporate real-time tension profiling, automatic knife positioning, OPC-UA protocol integration for MES/ERP connectivity, and automatic roll labeling systems, delivering documented productivity improvements of 20–35% compared to earlier-generation equipment while reducing operator dependency and waste.

The International Federation of Robotics (IFR) has confirmed sustained growth in industrial automation investment across Asia Pacific and Europe, the two largest paper slitting machine markets, with packaging sector automation investment representing a major component of overall manufacturing automation spending, sustaining capital equipment upgrade demand throughout the forecast period.

Restraints - High Capital Cost of Fully Automatic Systems Creating Investment Barriers for Small and Medium Converters

Fully automatic high-speed paper slitting rewinder systems with integrated servo tension control, vision inspection, and digital network connectivity represent substantial capital investments, with premium European-manufactured systems ranging from €250,000 to over €1 million per unit depending on web width, speed, and automation specification level. For small and medium-sized converting enterprises, which represent the majority of paper converting operations in Asia, Latin America, and Africa, these capital requirements create prohibitive procurement barriers, particularly during periods of elevated interest rates and constrained industrial credit access.

The European Central Bank (ECB) and U.S. Federal Reserve maintained elevated benchmark interest rates through 2024–2025, meaningfully increasing the cost of equipment financing and extending capital expenditure decision timelines for mid-market converting operations, dampening near-term demand for premium-specification slitting systems in these economically sensitive customer segments.

Environmental Regulations on Paper Industry Waste and Energy Consumption Increasing Compliance Overhead

Paper slitting and converting operations generate measurable quantities of edge trim waste, rejected slit rolls, and process energy consumption that are increasingly subject to regulatory scrutiny under evolving ISO 14001 environmental management frameworks and national industrial waste reduction mandates. The European Environment Agency (EEA) has been progressively tightening solid industrial waste landfill restrictions, compelling converters to invest in trim recycling and waste management infrastructure that adds overhead costs to slitting operations.

The European Union's Energy Efficiency Directive mandates energy auditing and efficiency improvement programs for industrial facilities, including paper converting plants, requiring investment in energy-efficient slitting machine drives, regenerative braking systems, and compressed air optimization on air-score slitting lines. These compliance requirements divert capital from new equipment procurement, moderating the upgrade investment pace among environmentally regulated converters in premium markets.

Opportunities - Flexible Packaging Boom and Specialty Paper Applications Creating High-Value Slitting Machine Demand

The global flexible packaging industry's rapid expansion, driven by the food and beverage sector's adoption of lightweight, hermetically sealed packaging formats, is creating growing demand for high-precision paper slitting machines capable of handling a broader range of specialty substrates including coated papers, multi-layer laminates, tissue, release liners, and thin-gauge specialty papers. The Flexible Packaging Association (FPA) reported that the U.S. flexible packaging market generates over US$ 34 billion in annual shipments, with paper-based flexible packaging, including kraft paper pouches, paper-based laminates for snack food packaging, and recyclable paper wrapping for household goods, representing the fastest-growing flexible packaging sub-segment.

Specialty paper slitting applications, including self-adhesive label stocks, thermal paper for point-of-sale printing, medical packaging papers, and battery separator papers for lithium-ion cells, require extremely tight width tolerances (±0.1 mm) and slit-edge quality specifications that only technically advanced razor blade and shear blade slitting systems can achieve, commanding premium machine prices and reinforcing the high-value specialty segment's revenue growth contribution throughout the forecast period.

Fully Automatic Slitting Machine Adoption in Emerging Market Paper Mill Expansions Generating New Procurement Cycles

Rapid paper and paperboard production capacity expansion across emerging economies, particularly in India, Vietnam, Indonesia, and Brazil, is generating substantial new procurement demand for paper slitting machines as newly commissioned paper mills invest in matched converting and finishing equipment. The Paper and Board Manufacturers Association of India (PBMAI) has documented significant capacity expansion announcements by major Indian paper manufacturers targeting both domestic consumption growth and export opportunities, with new integrated paper mill projects in Andhra Pradesh, Odisha, and Maharashtra including dedicated slitting and rewinding departments requiring full equipment fit-outs.

The Ministry of Commerce and Industry of India's Production Linked Incentive (PLI) Scheme for Advanced Chemistry Cell batteries and food processing equipment, both sectors driving specialty paper demand, is amplifying downstream paper consumption growth that incentivizes upstream converting capacity investment. European slitting machine manufacturers with established presence in emerging market distribution networks, including ATLAS CONVERTING EQUIPMENT LTD. and Parkinson Technologies, Inc., are strategically positioned to capitalize on these greenfield and capacity-expansion procurement opportunities, competing against lower-cost Asian equipment suppliers through superior automation capability, after-sales service support, and compliance with international machinery safety standards, including CE marking and OSHA requirements.

Category-wise Insights

By Blade Type

The shear blade slitting system leads the global market by blade type, accounting for approximately 48% of total blade type segment revenue in 2026. Shear blade slitting, which uses a pair of upper and lower circular knives operating in a scissor-like action against the web substrate, delivers the highest slit-edge quality, cleanest cut finish, and best dimensional accuracy of all slitting methods, making it the dominant specification for premium paper grades, coated paperboards, laminates, specialty papers, and multi-layer packaging substrates.

The Technical Association of the Pulp and Paper Industry (TAPPI) has published technical guidelines confirming shear blade slitting as the preferred method for premium packaging papers requiring low dust generation and precision width control, characteristics critical for pharmaceutical packaging, food-grade paper, and electronics-grade specialty paper converting applications. Shear blade systems also accommodate the widest range of paper basis weights, from ultra-thin tissue grades at 12 gsm to heavyweight industrial boards at 500+ gsm, providing maximum operational flexibility for commercial converting operations serving diverse customer specifications. Razor blade systems hold approximately 32% share, favored for high-speed thin-film and lightweight paper applications.

By Technology

The fully automatic technology segment leads the global Paper Slitting Machine market by technology, commanding approximately 55% of total technology segment revenue in 2026, a position that reflects the converting industry's progressive investment in high-throughput, low-operator-dependency production systems. Fully automatic paper slitting machines integrate motorized knife positioning systems, automatic tension control with closed-loop feedback, automatic roll diameter management, programmable slitting sequence recipe storage, and fully integrated SCADA/MES data connectivity, delivering throughput speeds of 1,000–2,000 meters per minute on advanced systems from manufacturers including Kampf Schneid- und Wickeltechnik and SOMA.

The International Federation of Robotics (IFR) confirms that industrial automation investment in the packaging machinery and converting equipment segments has sustained consistent double-digit growth rates across Asia Pacific and Europe in recent years, directly correlating with the fully automatic slitting machine segment's dominant revenue share. Semi-Automatic systems retain approximately 32% market share, serving mid-tier converting operations balancing automation investment against throughput requirements. Manual systems are declining in share, limited to very small-scale and bespoke converting applications in price-sensitive markets.

Regional Insights

North America Paper Slitting Machine Trends

North America is a mature and technically advanced market for paper slitting machines, anchored by the United States' position as the world's second-largest paper and paperboard producer and the dominant North American converting industry, encompassing flexible packaging, label converting, tissue manufacturing, and specialty paper processing. The American Forest and Paper Association (AF&PA) reported that U.S. paper and paperboard shipments exceeded 80 million short tons in recent years, sustaining continuous demand for slitting and converting equipment across a large and diverse base of manufacturing facilities. The growing U.S. flexible packaging industry, led by the Flexible Packaging Association (FPA), is a primary end-market driver for precision slitting machine investments, as converters upgrade to higher-speed, fully automatic systems to meet tight lead times and demanding quality specifications from major food, pharmaceutical, and consumer goods brand owners.

Parkinson Technologies, Inc., headquartered in Woonsocket, Rhode Island, and Universal Converting Equipment maintain established North American market positions through local technical support, rapid spare parts availability, and deep application engineering expertise tailored to North American converting industry standards including OSHA machinery safety compliance and NFPA electrical equipment requirements. The U.S. Environmental Protection Agency (EPA)'s industrial solid waste regulations and voluntary sustainability programs, such as the Sustainable Packaging Coalition's How2Recycle standard, are incentivizing North American converters to invest in low-waste, high-yield slitting systems that minimize trim waste and reduce material input costs, further driving capital equipment upgrade demand across the region's converting industry.

Europe Paper Slitting Machine Trends

Europe is the global technology leadership hub for paper slitting machines, with Germany hosting the headquarters of the world's most technically sophisticated slitting machine manufacturers, Kampf Schneid- und Wickeltechnik GmbH & Co. KG and GOEBEL Schneid und Wickelsysteme GmbH, and an advanced paper and converting industry ecosystem that demands the highest-specification slitting equipment available globally. The Confederation of European Paper Industries (CEPI) reported that European paper and board production exceeded 90 million tonnes annually across its member companies, with the packaging segment representing the largest and fastest-growing end-use category, directly sustaining investment in precision slitting equipment across European converting operations. Germany's domestic paper and packaging converting sector, encompassing hundreds of established converting SMEs and large multinational packaging groups, consistently drives procurement of next-generation fully automatic slitting systems equipped with Industry 4.0 machine connectivity and digital performance monitoring.

The United Kingdom's converting and flexible packaging industry, served by specialist distributor ASHE Converting Equipment, maintains consistent demand for technically advanced slitting solutions, while France's pharmaceutical and food-grade paper converting sectors create demand for precision high-cleanliness slitting systems meeting EU GMP and FDA 21 CFR Part 11 audit trail compliance. Spain's growing flexible packaging manufacturing sector, with major converting operations concentrated in the Basque Country and Catalonia industrial zones, is an important growth market for both new machine procurement and retrofit automation upgrades. The EU Machinery Directive 2006/42/EC, governing machinery safety standards including slitting machines, and its upcoming revised EU Machinery Regulation are compelling machine builders to continuously upgrade safety systems, driving product development investment among European manufacturers. Euromac S.r.l. in Italy serves the Southern European market effectively through its broad product range of slitting and rewinding solutions.

Asia Pacific Paper Slitting Machine Trends

Asia Pacific is the largest and fastest-growing regional market for paper slitting machines globally, driven by the region's dominant position in global paper production, with China alone accounting for approximately 25% of world paper and paperboard output according to the FAO, and the rapid capacity expansion of paper mills and converting operations across India, Vietnam, Indonesia, and South Korea. China's massive paper and packaging industry, comprising thousands of paper mills, carton converters, label printers, and flexible packaging manufacturers, represents the world's single largest market for paper slitting machines by volume, with domestic manufacturers and imported European systems both competing for procurement across this vast installed base. China's national paper industry consolidation policies, directed by the China Paper Association (CPA), are driving smaller mills toward higher-specification equipment investments as minimum quality and efficiency benchmarks are enforced, accelerating the transition toward semi-automatic and fully automatic slitting systems.

India is Asia Pacific's fastest-growing paper slitting machine market, supported by the country's expanding paper packaging sector, driven by the Bureau of Indian Standards (BIS) notification mandating paper-based packaging for several FMCG categories, and the growing tissue paper and specialty paper manufacturing base. The SOMA company and ATLAS CONVERTING EQUIPMENT LTD. have both identified India as a strategic high-growth market for premium slitting machine expansion, consistent with the country's overall manufacturing capacity investment trajectory. Japan's technically sophisticated converting industry, centered around precision specialty paper, electronics-grade separators, and pharmaceutical packaging substrates, sustains demand for ultra-high-precision slitting machines with the tightest width and edge-quality tolerances available, positioning Japan as a premium-revenue market despite its more moderate volume growth profile compared to China and India.

Competitive Landscape

The global paper slitting machine market is moderately fragmented, with a clear tier-one of German and European precision engineering leaders, Kampf Schneid- und Wickeltechnik GmbH & Co. KG, GOEBEL Schneid und Wickelsysteme GmbH, SOMA, and ATLAS CONVERTING EQUIPMENT LTD., competing on technical sophistication, automation integration, and global service capability. These premium manufacturers differentiate through proprietary tension control algorithms, patented knife positioning systems, and comprehensive lifecycle support programs, including remote diagnostics via IIoT connectivity.

Emerging business model trends include pay-per-performance service contracts, machine-as-a-service leasing models for mid-market converters, and digital retrofit programs that upgrade legacy slitting machines with modern servo controls and Industry 4.0 connectivity without full machine replacement. Asian manufacturers compete vigorously on price in volume segments, while European specialists command premium margins in specialty and high-precision applications.

Key Developments:

- In March 2025, Kampf Schneid- und Wickeltechnik GmbH & Co. KG unveiled its next-generation COMPACTA 6 slitting rewinder system at drupa 2024, featuring enhanced IIoT-ready digital architecture, automated knife positioning with vision-guided alignment, and a compact machine footprint designed for high-output specialty paper and flexible packaging converting operations.

- In 2024, SOMA introduced advanced fully automatic slitting rewinder systems incorporating integrated Industry 4.0 machine data integration, real-time OEE monitoring dashboards, and high-speed automatic core placement, targeting premium label stock, flexible packaging, and specialty paper converting customers across European and Asian markets.

- In 2023, ATLAS CONVERTING EQUIPMENT LTD. expanded its global dealer and service network across Southeast Asia and India, establishing technical support centers to serve the region's rapidly growing paper and flexible packaging converting industry as part of a strategic commercial expansion program.

Companies Covered in Paper Slitting Machine Market

- Parkland Machines Ltd.

- ASHE Converting Equipment

- SOMA

- ATLAS CONVERTING EQUIPMENT LTD.

- GOEBEL Schneid und Wickelsysteme GmbH

- Kampf Schneid- und Wickeltechnik GmbH & Co. KG

- Euromac S.r.l.

- Parkinson Technologies, Inc.

- Pasquato Cutting Machines

- Universal Converting Equipment

- Catbridge Machinery LLC

- Laem System S.r.l.

- Wenzhou Kingsun Machinery Co., Ltd.

- Deacro Industries Ltd.

- Jennerjahn Machine Inc.

Frequently Asked Questions

The global Paper Slitting Machine market is estimated to be valued at US$ 707.1 Million in 2026 and is projected to reach US$ 975.2 Million by 2033, registering a forecast CAGR of 4.7% over the period 2026 to 2033. The market recorded a historical growth rate of 4.3% CAGR between 2020 and 2025, supported by growing paper packaging demand and converting industry automation investment globally.

The key growth drivers are the global e-commerce-led paper packaging boom, with the IPC documenting 11% cross-border parcel volume growth in 2023 driving paper and paperboard demand exceeding 400 million metric tonnes annually per the FAO, and the converting industry's Industry 4.0 automation transition toward fully automatic slitting systems that deliver 20–35% documented productivity improvements over legacy equipment, compelling upgrade investment cycles across major converting markets.

Shear Blade slitting systems lead the Blade Type category with approximately 48% revenue share in 2026. Their leadership is grounded in superior slit-edge quality, widest substrate compatibility range (12–500+ gsm), and mandatory specification in pharmaceutical, food-grade, and electronics-grade converting applications, as confirmed by TAPPI technical guidelines that designate shear blade slitting as the preferred method for premium paper and packaging substrate processing.

Asia Pacific leads the global Paper Slitting Machine market, with China contributing approximately 25% of world paper and board production per the FAO and India representing the fastest-growing national market driven by BIS-mandated paper packaging adoption, PLI Scheme industrial incentives, and rapid specialty paper capacity expansion. The region's concentration of both paper mill installations and downstream converting operations drives the world's highest aggregate demand for paper slitting equipment.

The most significant opportunity lies in specialty and technical paper slitting applications, including battery separator papers for lithium-ion cells, medical packaging grades, release liners, and thermal papers, requiring ±0.1 mm width tolerance precision achievable only with premium shear blade and razor blade systems. These high-specification applications command significant equipment price premiums and benefit from structural demand growth in electric vehicle battery manufacturing and pharmaceutical packaging sectors globally.