- Medical Devices

- Orthopedic Power Tools Market

Orthopedic Power Tools Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Orthopedic Power Tools Market by Product Type (Large Bone Power Tools, High-speed Power Tools, Small Bone Power Tools), End-user (Hospitals, Outpatient Facilities), and Regional Analysis, from 2026 to 2033

Orthopedic Power Tools Market Share and Trends Analysis

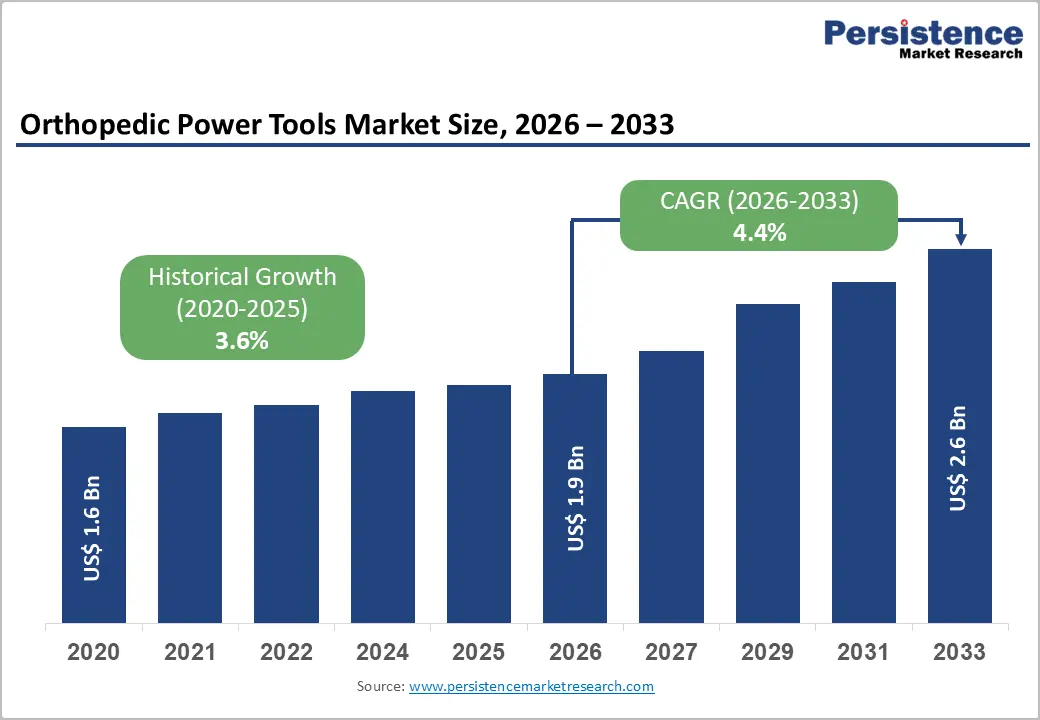

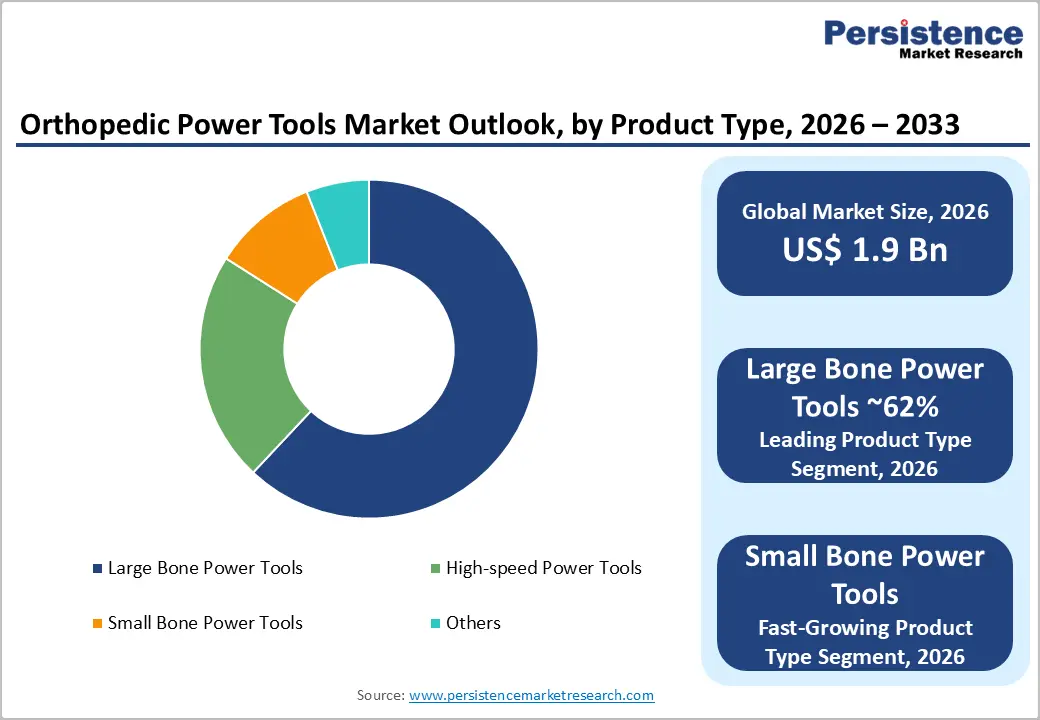

The global orthopedic power tools market size is expected to be valued at US$ 1.9 billion in 2026 and projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033.

Orthopedic power tools are specialized surgical instruments designed to assist orthopedic surgeons in performing various procedures, including bone cutting, drilling, and fixation. These tools typically operate on electrical or pneumatic power, enhancing precision and efficiency during surgery. Common examples include saws, drills, and reamers. The sector is experiencing significant growth, driven by technological advancements, an aging population, and increased orthopedic surgery volumes. One notable trend is the transition towards minimally invasive surgical techniques, which demand more sophisticated power tools that can operate in constrained environments while maintaining efficacy.

Among other trends in the orthopedic power tools market, the integration of robotics and artificial intelligence into orthopedic surgical procedures is revolutionizing the landscape. It enhances precision and reduces human error. Another key trend is the growing emphasis on patient safety and comfort, which has led to the development of ergonomic tools to reduce surgeon fatigue and improve the overall surgical experience. Furthermore, the rise of outpatient surgeries is boosting demand for lightweight and portable power tools, making them easy to handle and transport.

Key Industry Highlights

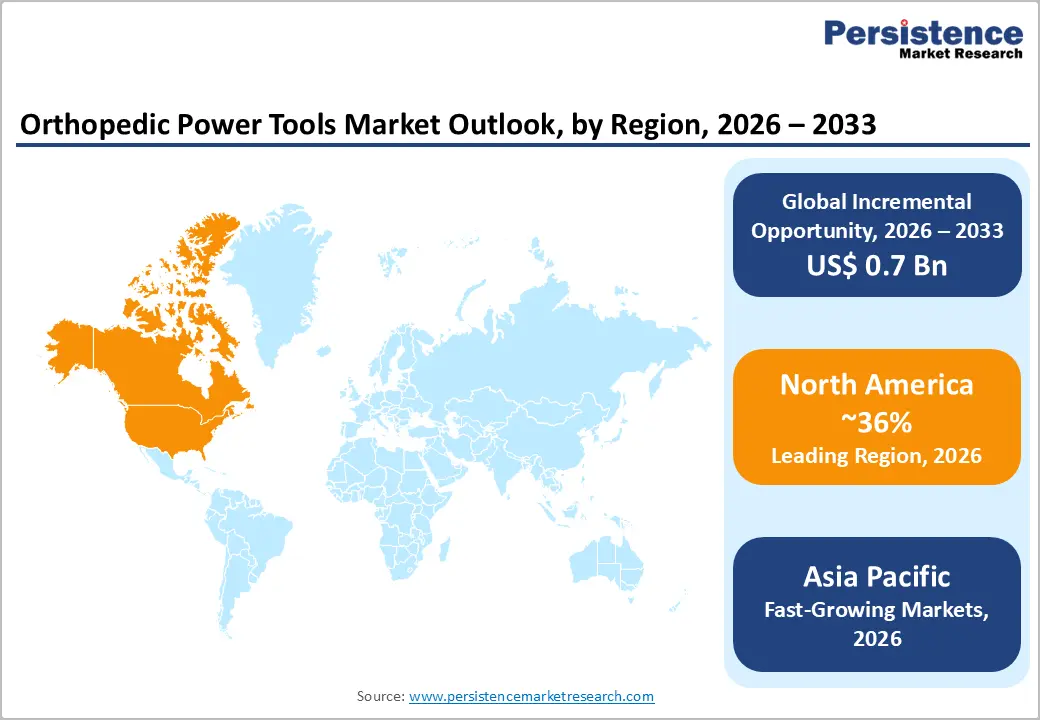

- Leading Region: North America leads due to advanced healthcare infrastructure, high orthopedic surgery volumes, strong reimbursement policies, and early adoption of minimally invasive surgical technologies.

- Fastest Growing Region: Asia Pacific grows fastest, driven by rising orthopedic disorder prevalence, expanding surgical facilities, government healthcare investments, and increasing patient awareness.

- Dominant Segment: Large bone power tools dominate, supported by high incidence of fractures, sports-related injuries, and rising demand for joint replacement and complex orthopedic procedures.

- Fastest Growing Segment: Small bone power tools grow fastest, aided by innovations in precision surgical instruments, ergonomic designs, minimally invasive procedure adoption, and increasing outpatient surgical centers.

| Key Insights | Details |

|---|---|

| Orthopedic Power Tools Market Size (2026E) | US$ 1.9 Bn |

| Market Value Forecast (2033F) | US$ 2.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.4% |

| Historical Market Growth (CAGR 2020 to 2024) | 3.6% |

Market Dynamics

Driver - Increasing Prevalence of Orthopedic Conditions

The global burden of orthopedic conditions continues to rise due to aging populations, sedentary lifestyles, and increasing participation in sports and physical activities. Disorders such as osteoarthritis, osteoporosis, spinal degeneration, and traumatic fractures are becoming more common across both developed and developing regions. According to international health organizations, age-related musculoskeletal disorders are among the leading causes of disability worldwide. As life expectancy increases, a larger share of the population requires joint replacement, fracture fixation, and corrective orthopedic procedures. This growing surgical volume directly increases demand for reliable and high-performance orthopedic power tools that support accuracy and efficiency during complex procedures.

Additionally, improved diagnosis and awareness of early treatment are encouraging timely surgical interventions. Hospitals and orthopedic centers are therefore upgrading their surgical toolsets to manage higher caseloads while maintaining clinical precision and patient safety.

Advancements in Surgical Technology

Rapid technological progress in orthopedic surgery is a critical driver of demand for advanced power tools. Innovations such as computer-assisted navigation, robotic-assisted surgery, and improved imaging technologies have significantly enhanced surgical accuracy and consistency. These advancements require compatible power tools that can deliver precise control, stable torque, and consistent performance during procedures. Battery-powered systems, improved motor efficiency, and reduced-vibration designs are further enhancing surgeon comfort and procedural outcomes. In parallel, the integration of digital platforms enables improved preoperative planning and intraoperative guidance, raising expectations for tool precision. As healthcare facilities modernize operating rooms to align with evolving surgical standards, investment in technologically advanced orthopedic power tools continues to grow. Manufacturers are responding by focusing on innovation, durability, and compatibility with next-generation surgical systems, supporting long-term market expansion.

Restraints - High Costs of Advanced Technologies

The orthopedic power tools market is constrained by the high costs associated with advanced surgical technologies. Modern power tools that incorporate features such as robotic assistance, smart sensors, and enhanced battery systems require significant investments in research, engineering, and manufacturing. These elevated costs are reflected in the final product pricing, making advanced tools less accessible for small and mid-sized hospitals, ambulatory surgical centers, and clinics, particularly in cost-sensitive regions. Budget constraints often compel healthcare providers to rely on conventional or refurbished equipment rather than upgrading to newer systems. Additionally, ongoing expenses related to maintenance, training, and consumables further increase the total cost of ownership. As a result, high technology costs can slow adoption rates and restrict market penetration across emerging and underserved healthcare settings.

Stringent Regulatory Requirements

Stringent regulatory frameworks present a significant challenge for the orthopedic power tools market. Medical device authorities enforce rigorous safety, performance, and quality standards to ensure patient protection, but compliance can be complex and time-consuming. Manufacturers must undergo extensive clinical evaluations, documentation, and audits before obtaining product approvals, thereby substantially delaying market entry. These regulatory processes often require high financial and technical resources, increasing overall development costs. Smaller manufacturers may struggle to meet these requirements, limiting their ability to compete with established players. Frequent updates to regulatory guidelines also add compliance uncertainty and operational risk. Consequently, prolonged approval timelines and regulatory burdens can slow innovation cycles, reduce product availability, and restrain overall market growth.

Opportunity - Rise of Outpatient Surgery Centers

The rapid expansion of outpatient surgery centers is creating strong growth opportunities for the orthopedic power tools market. These facilities focus on shorter procedures, faster patient turnover, and lower operational costs, and drive demand for compact, reliable, and easy-to-handle surgical tools. Unlike large hospitals, outpatient centers prefer portable systems with quick setup, minimal maintenance, and high procedural efficiency. This shift encourages manufacturers to design ergonomic, battery-powered, and multifunctional orthopedic tools suited for same-day surgeries. As outpatient orthopedic procedures increase, suppliers that align product design with space efficiency, mobility, and cost control can significantly strengthen adoption and long-term partnerships within this evolving care model.

Integration of Smart Technologies

The incorporation of smart technologies, such as IoT and AI, into orthopedic power tools presents a promising opportunity for market players. Manufacturers can significantly improve surgical outcomes and patient safety by developing connected devices that provide real-time data analytics, surgical performance tracking, and enhanced precision.

This innovation can also facilitate remote monitoring and training, enabling surgeons to adopt new techniques and technologies more easily. As healthcare undergoes digital transformation, the demand for smart orthopedic power tools is expected to increase, thereby driving market growth.

Category-wise Analysis

By Product Type Insights

The large-bone power tools segment is expected to remain the dominant product type in the orthopedic power tools market, accounting for approximately 62% of the market in 2025. This leadership is primarily driven by the increasing prevalence of orthopedic conditions, high-impact accidents, and sports-related injuries that often require complex surgical interventions involving large bones. For instance, in the U.S., over 3.5 million sports-related injuries are reported annually among youth, highlighting the critical need for robust surgical solutions. These procedures require precise, high-torque instruments capable of efficiently handling dense bone structures.

Additionally, the increasing adoption of joint replacement surgeries and spinal fixation procedures further increases demand for large-bone power tools. Hospitals and orthopedic centers are investing in advanced, reliable devices to enhance surgical accuracy, reduce operative times, and improve patient recovery outcomes, reinforcing the segment’s market leadership.

By End-user Insights

The hospital segment is the leading end user in the orthopedic power tools market, accounting for the largest share of revenue and projected to grow at a CAGR of 4.1% over the forecast period. Hospitals are the primary sites for orthopedic surgeries, including joint replacements, fracture fixation, and spinal procedures, which require advanced power tools for precise and efficient operations. The increasing number of orthopedic procedures performed daily in hospitals drives consistent demand for high-quality instruments.

Moreover, hospitals are increasingly adopting technologically advanced surgical tools, such as high-speed drills, battery-powered saws, and ergonomic handpieces, to enhance procedural accuracy and reduce patient recovery time. Dedicated orthopedic centers and specialty hospitals prioritize upgrading their surgical equipment to meet rising patient volumes and complex case requirements. This ongoing investment in advanced power tools continues to strengthen hospitals’ dominance as the key end user in the market.

Region-wise Insights

North America Orthopedic Power Tools Market Trends

The North American orthopedic power tools market is witnessing robust growth, driven by the increasing adoption of minimally invasive surgical techniques across hospitals and specialty centers. These procedures reduce patient recovery time, minimize tissue damage, and enhance surgical precision, prompting healthcare providers to invest in advanced power tools. Key market players such as Stryker, DePuy Synthes, and Medtronic are actively introducing innovative devices, including high-torque drills, battery-operated saws, and ergonomically designed handpieces, tailored to meet the evolving needs of surgeons. In December 2021, DePuy Synthes launched the UNIUM System power drill, offering enhanced control, customizable speed settings, and improved intraoperative efficiency.

The region also benefits from a well-established healthcare infrastructure, stringent regulatory standards that ensure device safety, and high reimbursement coverage for orthopedic surgeries, which further support market expansion. Moreover, increasing awareness of orthopedic conditions, a rising geriatric population, and significant investment in the research and development of smart surgical tools contribute to North America’s leadership in the global orthopedic power tools market, thereby consolidating its position as the most influential regional market.

Asia Pacific Orthopedic Power Tools Market Trends

The Asia Pacific orthopedic power tools market is experiencing rapid growth due to rising orthopedic surgical volumes, expanding healthcare infrastructure, and increasing medical tourism in countries such as India, China, and Japan. The prevalence of degenerative bone diseases, fractures from road traffic accidents, and sports injuries is driving demand for advanced surgical interventions, prompting hospitals to adopt innovative power tools. Countries such as China have experienced a sharp rise in joint replacement surgeries, with total knee arthroplasty procedures increasing significantly in recent years, underscoring the growing need for efficient orthopedic instruments.

Local manufacturers, including Shanghai Bojin Medical Instrument Co., Ltd., are enhancing production capacity and developing cost-effective solutions to serve the growing patient population. Furthermore, government initiatives that promote healthcare accessibility, such as India’s National Health Mission, are facilitating hospital expansions and upgrades, thereby increasing the adoption of advanced orthopedic devices.

The region’s advantage in manufacturing, combined with increasing investments in minimally invasive technologies and growing awareness of orthopedic health, positions the Asia Pacific as the fastest-growing market, with strong potential for further penetration by international and regional orthopedic power tool providers.

Competitive Landscape

The orthopedic power tools market is moderately fragmented, with leading players like Stryker, DePuy Synthes (Johnson & Johnson), Medtronic, Zimmer Biomet, and B. Braun SE dominating key segments. Companies are focusing on product innovation, R&D investments, and strategic partnerships to enhance their market presence and technological capabilities. Emerging players, particularly in Asia Pacific, are leveraging cost-effective manufacturing and localized solutions to capture market share. Key differentiators include ergonomic designs, battery-powered tools, high-torque drills, and integration with minimally invasive or smart surgical systems. Additionally, companies are adopting training programs and digital platforms to support surgeons and improve surgical outcomes, strengthening brand loyalty and competitiveness.

Key Industry Developments:

- September 2024, Arthrex, a global leader in minimally invasive surgical technology and medical education, launched OrthoPedia Patient. This interactive digital platform offers patients easy-to-understand videos on a range of orthopedic conditions and treatments. The platform encourages a self-directed educational journey through anatomy, treatment options, surgical animations, and demonstrations of cutting-edge techniques.

- March 2024, Surgical Holdings has expanded its portfolio by introducing a range of single-patient-use products, including diathermy plates, ultrasound gels, ECG electrodes, and defibrillation electrodes, in collaboration with Telic. The company aims to ensure consistent and reliable access to these vital items, focusing on quality and sustainability. The new division will include a new sales team and state-of-the-art warehouse facilities, enhancing distribution capabilities.

Companies Covered in Orthopedic Power Tools Market

- Stryker

- CONMED Corporation

- Medtronic

- DepuySynthes (Johnson & Johnson MedTech)

- B. Braun SE

- Zimmer Biomet

- NSK / Nakanishi inc.

- Shanghai Bojin Medical Instrument Co.,Ltd

- Richard Wolf GmbH

- Arthrex, Inc.

- Kaiser Medical Technology Ltd

- Others

Frequently Asked Questions

The global orthopedic power tools market is projected to be valued at US$ 1.9 Bn in 2026.

Rising orthopedic surgeries, aging population, sports injuries, demand for minimally invasive procedures, and continuous technological advancements in surgical instruments.

The global orthopedic power tools market is expected to witness a CAGR of 4.4% between 2026 and 2033.

Expansion of outpatient surgical centers, growing emerging markets, adoption of battery-powered tools, and innovation in ergonomic, precision-enhancing orthopedic devices.

North America is the leading region in the global orthopedic power tools market.