- Medical Devices

- Orthopedic Digit Implants Market

Orthopedic Digit Implants Market Size, Share, and Growth Forecast, 2026 - 2033

Orthopedic Digit Implants Market by Product Type (Metatarsal Joint Implants, Metacarpal Joint Implants, Hemi-Phalangeal Implants, Others), Material (Titanium, Nitinol, Silicon Pyrocarbon, Stainless Steel, Advanced Composites), and Regional Analysis for 2026 - 2033

Orthopedic Digit Implants Market Size and Trends Analysis

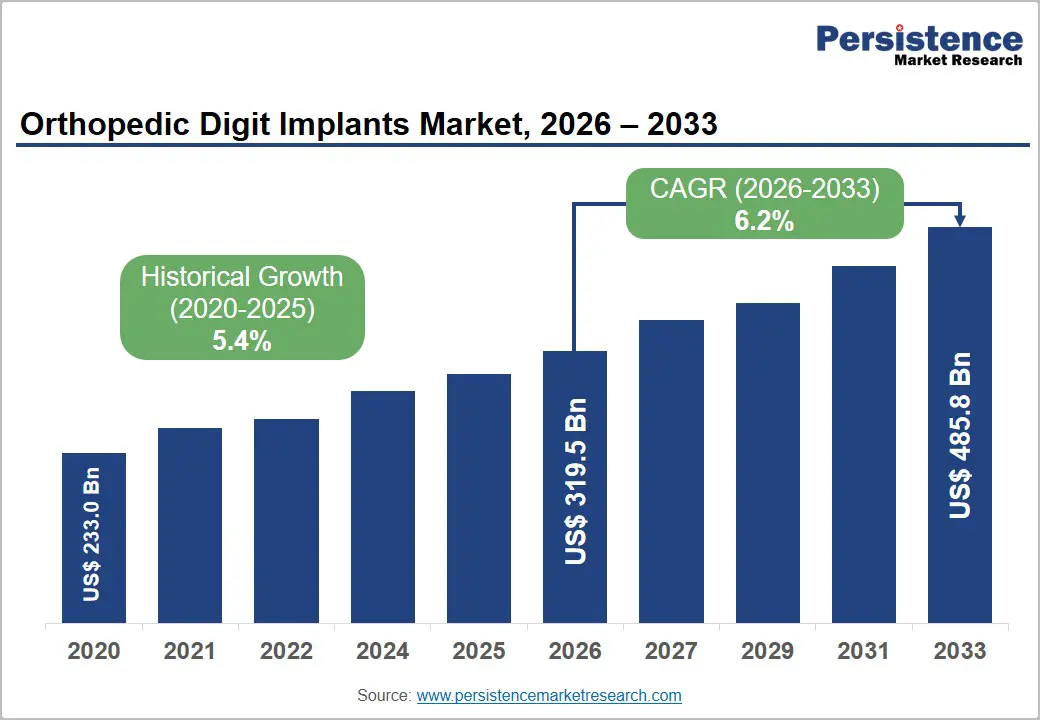

The global orthopedic digit implants market size is likely to be valued at US$319.5 million in 2026 and is expected to reach US$485.8 million by 2033, growing at a CAGR of 6.2% during the forecast period from 2026 to 2033, driven by the growing burden of musculoskeletal and degenerative joint disorders affecting the small joints of the hands and feet, alongside increasing demand for motion-preserving surgical solutions.

According to the World Health Organization (WHO), approximately 1.71 billion people worldwide live with musculoskeletal conditions, while osteoarthritis affected around 528 million people globally in the latest assessment, with hand joints among the commonly affected sites. Rising life expectancy, increasing incidence of arthritis-related deformities, advancements in biomaterials such as titanium and pyrocarbon, and greater adoption of outpatient orthopedic procedures continue to support market expansion and innovation in digit implant technologies.

Key Industry Highlights:

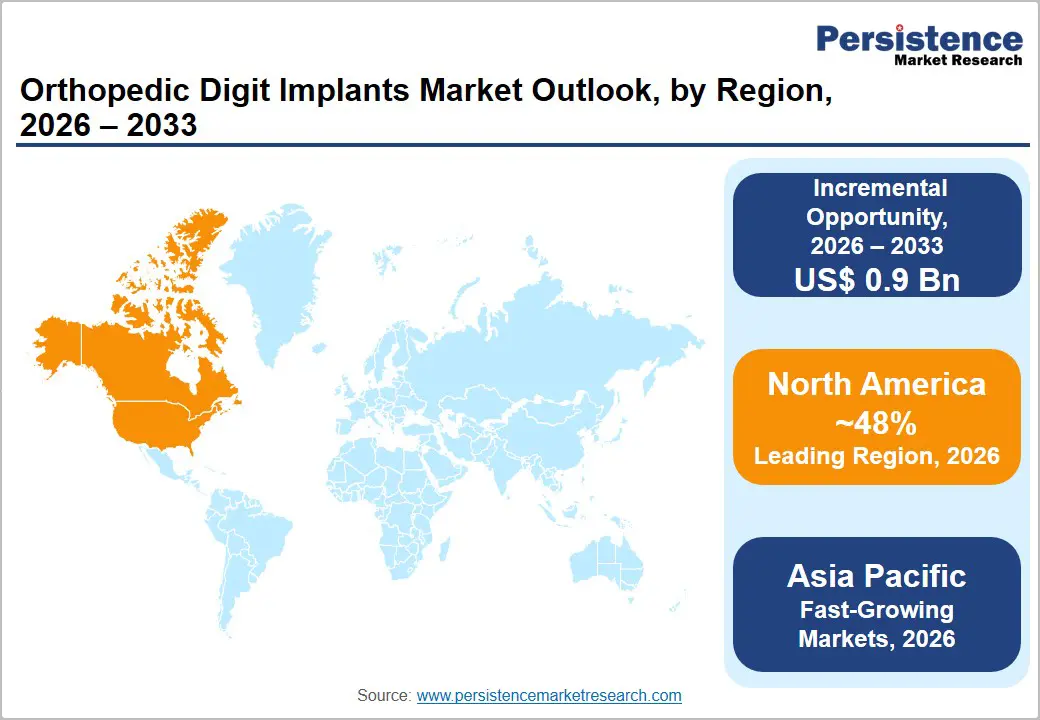

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 48% in 2026, driven by strong adoption of advanced small-joint reconstruction procedures and a well-established orthopedic care ecosystem.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by expanding orthopedic care access and increasing adoption of small-joint implant procedures across emerging economies.

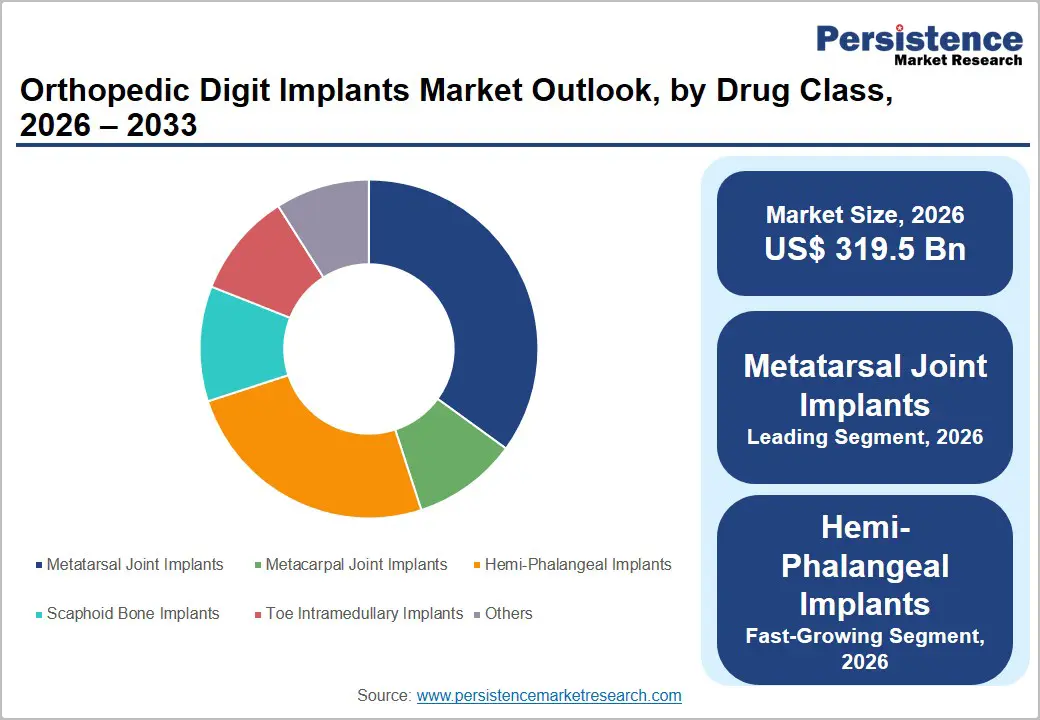

- Leading Product Type: Metatarsal joint implants are projected to represent the leading product type in 2026, accounting for 47% of the revenue share, driven by the high prevalence of forefoot disorders, established surgical procedures, and strong clinical adoption for weight-bearing joint reconstruction.

- Leading Material Type: Titanium is anticipated to be the leading material type, accounting for over 59% of the revenue share in 2026, supported by its superior biocompatibility, excellent osseointegration, high strength-to-weight ratio, and long-term clinical reliability.

- Key Opportunity: The growing adoption of personalized orthopedic care through 3D-printed, patient-specific digit implants and advanced motion-preserving technologies is creating significant growth opportunities across the orthopedic digit implants market.

DRO Analysis

Driver - Technological Advancements and Minimally Invasive Techniques

Modern implants manufactured from titanium, pyrocarbon, and advanced composites offer improved durability, biocompatibility, and anatomical fit, enhancing long-term clinical outcomes. Enhanced imaging systems, computer-assisted planning, and precision instrumentation enable surgeons to perform complex small-joint reconstructions with greater accuracy.

These innovations have improved implant positioning, reduced procedural variability, and increased confidence in motion-preserving alternatives to traditional fusion procedures. As healthcare providers increasingly seek solutions that restore functionality while minimizing complications, technological improvements continue to support broader adoption of orthopedic digit implants worldwide. Minimally invasive surgical techniques are accelerating market growth by reducing tissue disruption, postoperative pain, and recovery times.

Smaller incisions and refined surgical instruments allow procedures to be performed with greater precision while preserving surrounding anatomical structures. The growing shift toward ambulatory surgical centers and outpatient orthopedic procedures has increased demand for implants compatible with faster rehabilitation pathways. Patients increasingly prefer treatments that enable quicker return to daily activities and improved quality of life.

Restraint - Risk of Complications and Biocompatibility Issues

Potential complications include implant loosening, infection, joint instability, wear-related failures, and postoperative stiffness. Because finger and toe joints are small and subject to repetitive motion, achieving long-term implant stability can be challenging. Revision procedures may be required in cases of mechanical failure or inadequate fixation, increasing healthcare costs and patient burden.

Biocompatibility concerns also represent an important restraint in the market. Although modern materials have demonstrated strong clinical performance, some patients may experience inflammatory responses, allergic reactions, or tissue irritation related to implant components. Long-term wear debris generated by implant articulation can contribute to localized complications and affect implant survival. Regulatory agencies and healthcare providers maintain stringent requirements for safety, clinical evidence, and post-market monitoring, which can increase development timelines and costs for manufacturers.

Opportunity - Technological Convergence (3D Printing, Robotics, Bioresorbable Implants)

Three-dimensional printing enables the development of highly customized implants designed to match individual patient anatomy, improving fit, stability, and functional outcomes. Patient-specific solutions are particularly valuable in complex deformity correction and revision procedures where standard implants may provide limited effectiveness. Manufacturers are increasingly investing in additive manufacturing technologies to accelerate product development and improve implant personalization.

As healthcare providers seek more tailored treatment approaches, the adoption of 3D-printed orthopedic digit implants is expanding significantly across both developed and emerging healthcare markets. Robotics, digital planning platforms, and next-generation bioresorbable materials are transforming the market landscape. Robotic-assisted technologies can enhance surgical precision and improve reproducibility during delicate small-joint procedures.

Bioresorbable implants offer the potential to provide temporary structural support while gradually integrating with natural healing processes, reducing the need for implant removal procedures. The integration of these technologies supports improved clinical outcomes, shorter recovery periods, and greater procedural efficiency.

Category-wise Analysis

Product Type Insights

Metatarsal joint implants are expected to account for 47% of revenue in 2026, due to the high prevalence of forefoot disorders, including hallux rigidus, degenerative joint disease, and arthritis-related deformities affecting the metatarsophalangeal joints. These implants are widely utilized as they help preserve joint motion while reducing pain and improving mobility, making them an attractive alternative to joint fusion procedures. A notable example is the HemiCAP® Toe Classic System by Arthrosurface, which is widely used for first metatarsophalangeal joint resurfacing and is well established in the treatment of hallux rigidus and other forefoot disorders.

Hemi-phalangeal implants are likely to represent the fastest-growing segment, supported by increasing demand for motion-preserving treatments for finger joint disorders. These implants are commonly used in patients suffering from rheumatoid arthritis, osteoarthritis, traumatic injuries, and degenerative conditions affecting the small joints of the hand. For example, the Ascension PIP Hemi Arthroplasty System, which is designed to restore joint function while maintaining stability and mobility in proximal interphalangeal joint reconstruction procedures.

Material Type Insights

Titanium is projected to lead the market, capturing around 59% of the revenue share in 2026, supported by exceptional biocompatibility, high strength, corrosion resistance, and superior osseointegration properties. Titanium implants provide long-term structural stability while minimizing the risk of adverse biological reactions, making them highly suitable for both finger and toe joint reconstruction procedures. A prominent example includes the Stryker Hammertoe Fixation System, which utilizes titanium-based implant technology to provide durable fixation and support successful toe deformity correction procedures.

Silicon pyrocarbon is likely to be the fastest-growing material segment due to its unique biomechanical properties that closely resemble natural bone and cartilage behavior. The material offers excellent wear resistance, low-friction articulation, and enhanced joint preservation capabilities, making it particularly valuable in small-joint reconstruction of the fingers and hands. For instance, the Ascension PyroCarbon PIP Implant, which is widely recognized for its ability to restore finger joint function while supporting natural movement and long-term performance.

Regional Insights

North America Orthopedic Digit Implants Market Trends

North America is anticipated to be the leading region, accounting for a global market share of 48% in 2026, supported by high procedure volumes, advanced orthopedic care infrastructure, and strong adoption of motion-preserving surgical techniques. Demand is increasing as the prevalence of osteoarthritis, rheumatoid arthritis, and traumatic hand and foot injuries continues to rise among aging populations. For example, Stryker continues to expand its extremities portfolio through advanced solutions for foot and ankle reconstruction.

U.S. Orthopedic Digit Implants Market Trends

The U.S. is expected to dominate the regional market, accounting for approximately 80% of the North America market share in 2026, driven by its highly developed orthopedic ecosystem and strong reimbursement environment. Growing awareness of motion-preserving procedures is increasing demand for digit joint arthroplasty. Hospitals and ambulatory surgical centers are expanding their focus on minimally invasive extremity procedures. Surgeon preference is increasingly shifting toward advanced implant materials with proven long-term outcomes.

Canada Orthopedic Digit Implants Market Trends

Canada is likely to be a significant market for orthopedic digit implants, holding approximately 20% of the market share in 2026, supported by expanding access to specialized orthopedic care. The rising incidence of arthritis-related hand and foot disorders is contributing to procedure demand. Provincial healthcare systems are investing in improved surgical capacity and orthopedic services. Healthcare providers are increasingly adopting advanced implant technologies to improve patient outcomes. Growing awareness of functional restoration procedures is supporting treatment uptake.

Europe Orthopedic Digit Implants Market Trends

Europe is likely to be a significant market for orthopedic digit implants, due to strong clinical adoption, advanced healthcare systems, and increasing demand for joint-preserving procedures. The region benefits from a large elderly population and high prevalence of degenerative musculoskeletal disorders. For instance, Smith+Nephew which maintains a strong presence in orthopedic reconstruction and extremities through continuous investment in advanced surgical technologies and orthopedic implant solutions.

U.K. Orthopedic Digit Implants Market Trends

The U.K. is likely to be a significant market for orthopedic digit implants, accounting for 15% of Europe market share in 2026. Increasing focus on preserving mobility and reducing recovery times is supporting implant adoption. Hospitals are expanding access to advanced orthopedic procedures. Improvements in surgical training and clinical pathways are enhancing treatment outcomes. Growing awareness among patients regarding joint replacement alternatives is contributing to demand. Healthcare providers are increasingly evaluating advanced implant technologies for small-joint reconstruction.

Germany Orthopedic Digit Implants Market Trends

Germany is anticipated to dominate the regional market, accounting for around 37% of the Europe market share in 2026, due to its strong healthcare infrastructure and high surgical procedure volumes. Demand for digit implants is supported by the increasing prevalence of osteoarthritis and age-related joint disorders. The country has a well-established network of orthopedic specialists and advanced surgical centers. Adoption of innovative implant materials continues to rise. German healthcare providers emphasize long-term clinical outcomes and functional restoration.

Asia Pacific Orthopedic Digit Implants Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by the expanding healthcare infrastructure, increasing healthcare expenditure, and rising awareness of advanced orthopedic procedures. Growing elderly populations and increasing incidence of arthritis and traumatic injuries are creating significant demand for digit reconstruction solutions. A notable example includes Zimmer Biomet, which has strengthened its footprint across Asia Pacific through ongoing investments in orthopedic innovation, surgeon education, and extremity reconstruction solutions.

China Orthopedic Digit Implants Market Trends

China is projected to dominate the regional market, holding around 30% of the regional market share in 2026, due to rapid healthcare modernization and expanding orthopedic services. The rising prevalence of musculoskeletal disorders is increasing demand for reconstructive procedures. Government initiatives supporting healthcare access are improving treatment availability. Domestic medical device manufacturers are strengthening local production capabilities. Hospitals are increasingly adopting advanced orthopedic technologies.

India Orthopedic Digit Implants Market Trends

India is expected to emerge as a significant market, accounting for approximately 22% of the regional share in 2026, due to expanding healthcare infrastructure and increasing access to specialized orthopedic care. Rising incidence of arthritis, trauma cases, and age-related joint disorders is supporting demand for digit implants. Private hospitals are investing in advanced orthopedic technologies and surgical capabilities. Medical tourism is contributing to procedure volumes in major healthcare centers. Growing awareness of motion-preserving treatment options is encouraging adoption.

Competitive Landscape

The global orthopedic digit implants market exhibits a moderately fragmented structure, driven by the presence of established orthopedic device manufacturers alongside specialized extremity reconstruction companies focused on hand, wrist, foot, and ankle procedures. Market growth is supported by increasing demand for motion-preserving implants, advancements in biomaterials, and rising adoption of minimally invasive orthopedic techniques.

With key leaders, including Stryker, Zimmer Biomet, Smith & Nephew, DePuy Synthes, Arthrex, Acumed, Extremity Medical, and Paragon 28, the market remains highly innovation-driven. These players compete through product portfolio expansion, advanced titanium and pyrocarbon implant technologies, strategic partnerships with healthcare providers, surgeon education programs, and geographic expansion initiatives.

Key Industry Developments:

- In December 2025, Acumed announced the first successful surgery using its Acu-Loc NEXT System, advancing upper-extremity fixation technology and reinforcing its position in hand and wrist orthopedic reconstruction.

Companies Covered in Orthopedic Digit Implants Market

- Extremity Medical LLC

- Stryker

- Zimmer Biomet

- Smith & Nephew

- Depuy Synthes

- Arthrex Inc

- Acumed LLC

- Anika Therapeutics, Inc.

- VILEX, LLC

- Paragon 28

Frequently Asked Questions

The global orthopedic digit implants market is projected to reach US$319.5 million in 2026.

The orthopedic digit implants market is driven by the rising prevalence of osteoarthritis and rheumatoid arthritis, increasing demand for motion-preserving procedures, and advancements in implant materials and surgical techniques.

The orthopedic digit implants market is expected to grow at a CAGR of 6.2% from 2026 to 2033.

Key opportunities lie in the development of 3D-printed patient-specific implants, robotic-assisted surgeries, and next-generation biomaterials for improved digit joint reconstruction outcomes.

Extremity Medical LLC, Stryker, Zimmer, Smith & Nephew, and Depuy Synthes are the leading players.