- Medical Devices

- Orthopedic Braces and Supports Market

Orthopedic Braces and Supports Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Orthopedic Braces and Supports Market by Product Type (Ankle Braces and Supports, Foot Walkers and Orthoses, Knee Braces and Supports, Hip Back and Spine Braces and Supports, Facial Braces and Supports, Elbow Braces and Supports, Hand and Wrist Braces and Supports, Shoulder Braces Supports), Application, Orthopedic Braces Type, End-user, and Regional Analysis, from 2026 - 2033

Orthopedic Braces and Supports Market Share and Trends Analysis

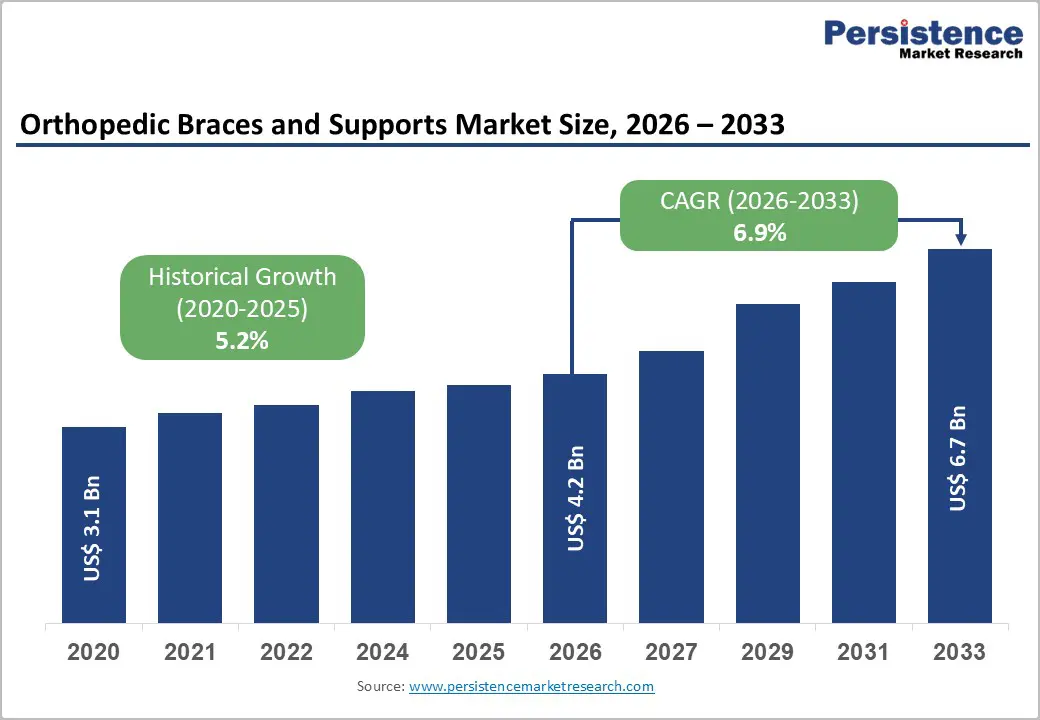

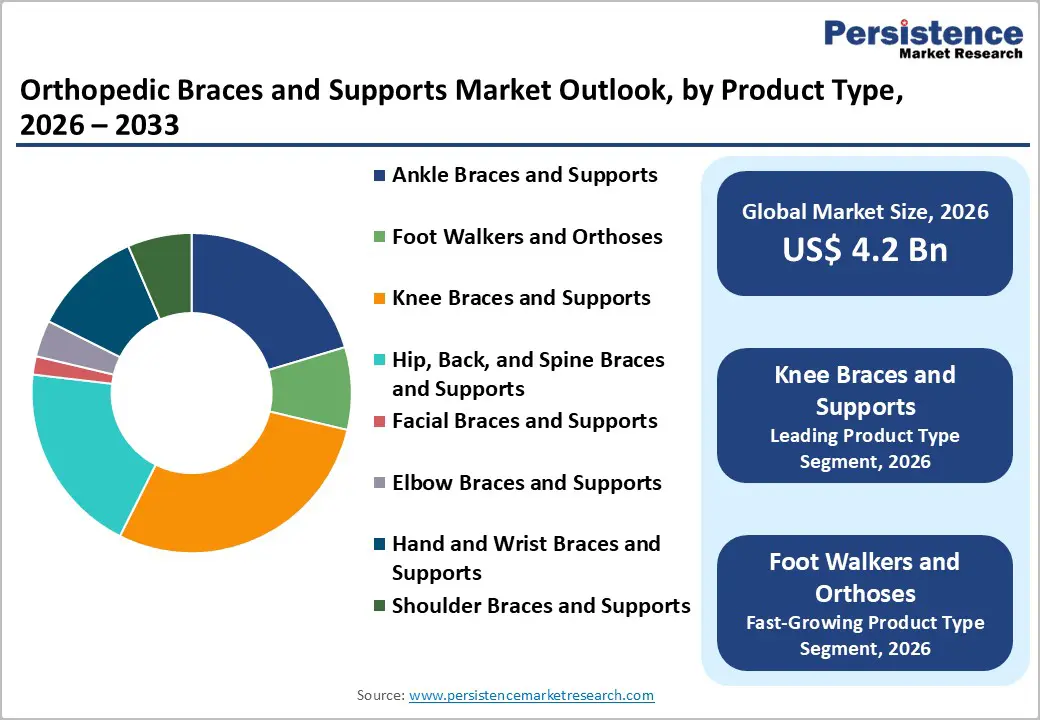

The global orthopedic braces and supports market size is expected to be valued at US$ 4.2 billion in 2026 and projected to reach US$ 6.7 billion by 2033. The market is projected to record a CAGR of 6.9% during the forecast period from 2026 to 2033.

The global market is expanding steadily, driven by the rising incidence of sports-related injuries, age-associated musculoskeletal disorders, and road traffic accidents. Growing prevalence of osteoarthritis, ligament tears, fractures, and post-surgical rehabilitation needs has increased reliance on braces and supports as effective non-invasive solutions. These products are widely used to stabilize joints, reduce pain, improve mobility, and support recovery across hospitals, rehabilitation centers, and homecare settings.

Key Industry Highlights

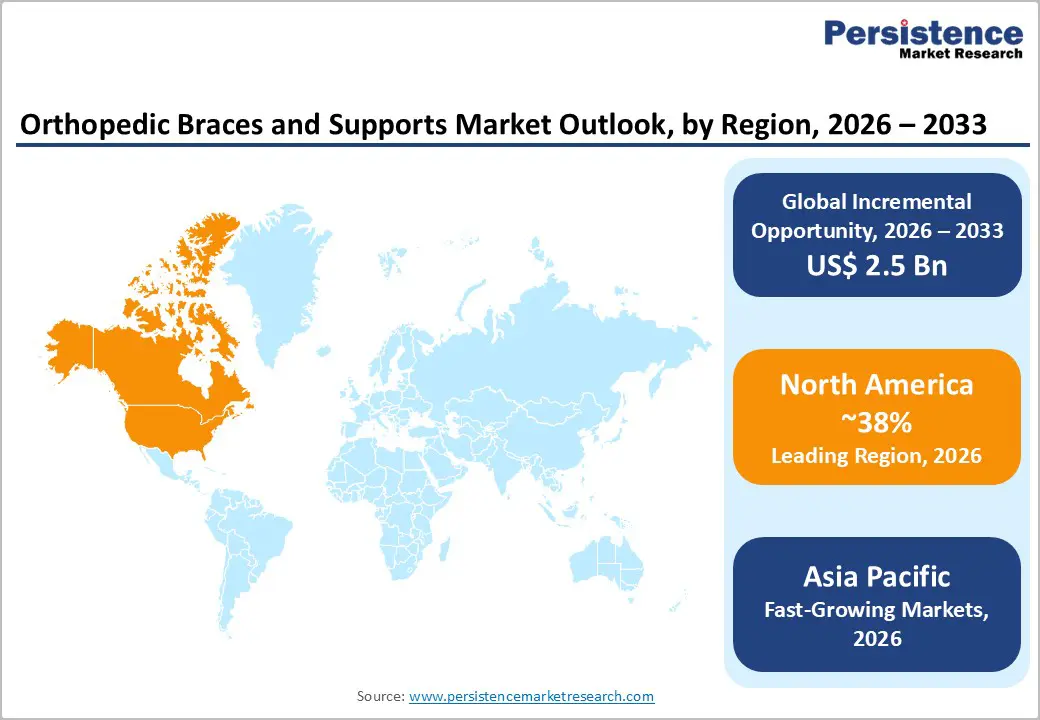

- Leading Region: North America leads due to advanced healthcare, high musculoskeletal disorder prevalence, strong reimbursement, and established orthopedic care.

- Fastest Growing Region: Asia Pacific grows fastest, driven by rising sports injuries, aging population, expanding healthcare, and growing awareness.

- Dominant Segment: Knee braces and supports dominate, widely used for injury prevention, osteoarthritis, and post-surgical rehabilitation across age groups.

- Fastest Growing Segment: Foot walkers and orthoses grow fastest, driven by increasing diabetes, mobility issues, and post-surgery rehabilitation demand.

| Key Insights | Details |

|---|---|

|

Orthopedic Braces and Supports Market Size (2026E) |

US$ 4.2 Bn |

|

Market Value Forecast (2033F) |

US$ 6.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Dynamics

Driver - Increasing Cases of Musculoskeletal Disorders to Foster Demand

Increasing prevalence of musculoskeletal issues is a key driver for the orthopedic braces and supports market, especially in areas having aging populations as well as rising rates of obesity and physical inactivity. Based on figures published by the U.S. Bureau of Labor Statistics, musculoskeletal diseases accounted for 30% of all worker injuries and illnesses in 2018.

The World Health Organization (WHO) published that musculoskeletal diseases are the leading cause of disability across the globe. The Centers for Disease Control and Prevention (CDC) stated that one in every four adults in the U.S. have been diagnosed with arthritis.

The economic burden of musculoskeletal problems emphasizes the market opportunity for orthopedic braces and supports. The National Institute for Occupational Safety and Health (NIOSH) estimates that work-related musculoskeletal diseases account for about 70 million physician office visits in the U.S. each year.

Rising Prevalence of Arthritis and Obesity to Bolster Sales

Arthritis is one of the leading chronic conditions mainly affecting the older adults. Increasing arthritis cases, owing to the aging global population, is estimated to surge demand for orthopedic braces. These devices assist in managing pain, support joints, and enhance mobility for arthritis sufferers.

Osteoarthritis is alone responsible for a significant portion of the global burden of musculoskeletal diseases as several individuals seek non-invasive treatment options like braces for symptom relief. The rapidly rising obesity rates further push sales of orthopedic braces and supports as it increases the risk of developing various orthopedic issues.

In the U.S., obesity is responsible for several chronic conditions that increase the requirement for braces. With an estimated 300,000 obesity-related deaths annually, the associated orthopedic challenges further drive demand for effective brace solutions.

Restraints - Limited Reimbursement Policies to Hamper Growth

Limited reimbursement regulations are likely to negatively impact the orthopedic back support product demand by restraining patient access to this key medical equipment. Several countries still classify orthopedic braces and support as non-essential or over-the-counter items, thereby limiting their insurance coverage.

It results in patients shouldering the entire cost that can be expensive, especially for those who require long-term or several braces for chronic illnesses like arthritis or post-surgical recuperation. Potential customers, particularly those having lower incomes, may opt for less expensive alternatives or avoid acquiring these devices entirely. It may further limit orthopedic braces and supports market growth.

Healthcare practitioners may be less likely to offer orthopedic braces and supports if they are aware that patients would have to pay out-of-pocket due to limited insurance coverage. This lack of reimbursement thereby hampers market innovation as manufacturers may be hesitant to spend on producing innovative or customized items if insurance will not cover them. The absence of financial support from insurance companies combined with the increased demand for orthopedic devices creates a gap between need and accessibility.

Opportunity - High Popularity of Online Channels to Create New Prospects

Increasing popularity of online channels is substantially contributing to the expansion of orthopedic braces and supports market. As consumers turn to e-commerce platforms for the purchase of healthcare products, including orthopedic braces, online retail has become a crucial channel for market growth.

As patients seek convenience, they are turning to e-commerce channels that offer consumers the ability to browse and purchase a wide range of products from home. Benefits provided by online channels like easy access to consumer reviews, competitive pricing, and detailed product specifications influence purchasing decisions. Online retail enables manufacturers to reach a wide consumer base, including those residing in remote locations, thereby enhancing engagement through targeted digital marketing strategies.

Product Commercialization by Manufacturers to Foster Innovations

Product commercialization is becoming a significant factor pushing orthopedic braces and supports market revenue. Key manufacturers are continuously innovating and launching new products as demand for specialized, effective, and comfortable orthopedic solutions rises. Businesses are diversifying their product portfolios by introducing unique solutions designed for specific conditions like sport injuries, post-surgery rehabilitation, and osteoarthritis.

Product commercialization is further being driven by strategic partnerships and investments. Companies like Ultra Athlete and Tandem Sport are extending their reach by integrating their products into athletic markets. Increasing availability of over the counter (OTC) orthopedic supports has made these products accessible. Emerging areas are also seeing new product rollouts aimed at addressing the rising incidence of musculoskeletal disorders.

Category-wise Analysis

By Product Type Insights

Knee braces and supports represent the leading product type in the orthopedic braces and supports market, driven by the high global incidence of knee-related injuries and degenerative conditions. The knee joint is particularly vulnerable to stress from sports, obesity, aging, and occupational strain, resulting in widespread cases of ligament injuries, meniscal tears, and osteoarthritis. Knee braces are commonly prescribed for injury prevention, post-operative stabilization, and long-term management of chronic knee pain. Products such as functional, prophylactic, unloader, and rehabilitative knee braces address a broad spectrum of clinical needs, making them highly versatile across age groups. Increasing participation in sports, coupled with a growing elderly population suffering from knee osteoarthritis, sustains strong demand. Advancements in lightweight materials, adjustable designs, and improved comfort have further enhanced patient compliance, reinforcing knee braces as the dominant product segment within the global orthopedic braces and supports market.

By Application Insights

Orthopedic braces and supports are widely used across preventive care, post-operative rehabilitation, sports injury management, and chronic condition support, with preventive and therapeutic applications accounting for the largest usage. Growing public awareness of early intervention has encouraged individuals to use braces to stabilize joints, correct posture, and reduce injury risk before conditions worsen. Athletes and physically active populations increasingly adopt braces to prevent ligament strains, muscle tears, and overuse injuries during training and competition.

Among the aging population, braces play a critical role in managing arthritis, osteoporosis, and degenerative joint disorders by reducing pain, improving alignment, and preserving mobility. Post-surgical rehabilitation remains another important application, where braces support healing after ligament reconstruction, joint replacement, or fracture repair. The rising preference for non-invasive, home-based care further strengthens demand, as braces provide effective symptom management without medication or surgery. Collectively, these applications position orthopedic braces as essential tools across both preventive and long-term musculoskeletal care pathways.

Region-wise Insights

North America Orthopedic Braces and Supports Market Trends

North America holds a leading position in the orthopedic braces and supports market, driven by a high prevalence of musculoskeletal disorders, sports injuries, and age-related conditions. Knee and back braces dominate demand due to widespread osteoarthritis, ligament injuries, and post-surgical rehabilitation requirements. The region benefits from advanced healthcare infrastructure, well-established orthopedic clinics, and strong reimbursement policies, enabling greater access to braces and supports across hospitals, rehabilitation centers, and homecare settings.

The growing focus on non-invasive treatments and preventive care has led to higher adoption of braces among athletes and the aging population. Additionally, increasing integration of innovative materials, ergonomic designs, and smart technologies such as sensors for movement tracking enhances product effectiveness and patient compliance. Online sales channels are also expanding, providing convenient access and boosting market penetration. Continuous investments in research and development by leading manufacturers are further driving product innovation and sustaining North America’s market leadership in orthopedic supports.

Asia and Pacific Orthopedic Braces and Supports Market Trends

Asia Pacific is the fastest-growing region in the orthopedic braces and supports market, propelled by increasing musculoskeletal disorders, sports injuries, and age-related conditions. Rapid urbanization, rising disposable incomes, and growing awareness about non-surgical orthopedic care are driving adoption across China, India, Japan, and ASEAN countries. Knee braces, back supports, and foot orthoses are in high demand due to increasing prevalence of osteoarthritis, ligament injuries, and post-operative rehabilitation needs.

Expansion of private healthcare facilities, specialty orthopedic clinics, and rehabilitation centers is improving access to braces and supports. Local manufacturing and cost-effective distribution are enhancing affordability, particularly in middle-income countries. Rising awareness of preventive care among athletes and the elderly, coupled with the integration of lightweight materials and ergonomic designs, is further boosting adoption. Additionally, e-commerce and online retail channels are gaining traction, making products more accessible. These factors position Asia Pacific for rapid growth in the orthopedic braces and supports market in the coming years.

Competitive Landscape

The competitive landscape of the global orthopedic braces and supports market is characterized by the presence of established medical device companies alongside numerous regional manufacturers. Leading players are investing significantly in research and development to expand their product portfolios with advanced, lightweight, and ergonomically designed braces that enhance patient comfort and clinical outcomes. Many manufacturers are adopting localized production strategies to reduce manufacturing and logistics costs while improving supply chain efficiency and responsiveness to regional demand.

Competition is further intensified by frequent product innovations, including adjustable designs, breathable materials, and smart braces integrated with sensors for movement and recovery monitoring. Companies are also focusing on strategic partnerships, acquisitions, and expanded distribution networks to strengthen their market position. As awareness of non-invasive orthopedic support solutions grows, differentiation through technology, pricing, and product performance remains a key competitive strategy.

Key Industry Developments:

- In May 2024, Denmark-based, create it REAL, launched 3D printing service platform for custom orthopedics.

- In January 2024, Enovis’ DJO, based in Texas, announced the launch of DonJoy Roam OA Knee brace for osteoarthritis or other knee pain and instability.

- In December 2023, OrthoPediatrics, headquartered in Warsaw, introduced a new division specializing in pediatric braces.

Companies Covered in Orthopedic Braces and Supports Market

- DeRoyal Industries, Inc.

- BREG, Inc.

- Bauerfeind

- Frank Stubbs Company Inc.

- DJO, LLC (Enovis)

- McDavid

- Ottobock

- ÖssurFillauer LLC

- Weber Orthopedic LP

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 4.2 Bn in 2026.

Rising sports injuries, aging population, osteoarthritis prevalence, post-surgical rehabilitation demand, and preference for non-invasive treatment options.

The global market is expected to witness a CAGR of 6.9% between 2026 and 2033.

Smart braces with sensors, e-commerce expansion, homecare adoption, emerging markets growth, and demand for customized orthopedic support solutions.

North America is the leading region in the global orthopedic braces and supports market.