- Healthcare Services

- Online Dermatology Consultation Market

Online Dermatology Consultation Market Size, Share, and Growth Forecast 2026 - 2033

Online Dermatology Consultation Market by Modality (Store-and-Forward Consultation, Real-Time (Video) Consultation, Hybrid Consultation), Service Type (Diagnosis, Treatment & Prescription, Follow-up Care, Cosmetic Consultation), Application (Acne, Psoriasis, Eczema, Skin Cancer Screening, Hair & Scalp Disorders), End-user (Homecare, Hospitals, Dermatology Clinics, Telehealth Providers), by Regional Analysis, 2026 - 2033

Online Dermatology Consultation Market Share and Trends Analysis

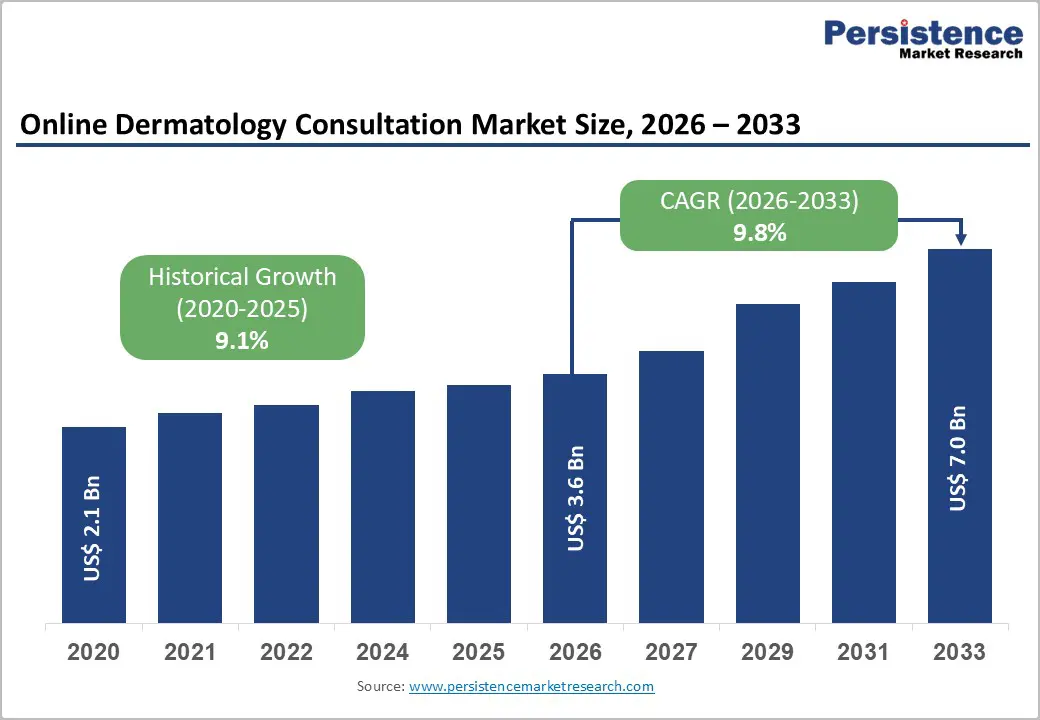

The global online dermatology consultation market size is expected to be valued at US$ 3.6 billion in 2026 and projected to reach US$ 7.0 billion by 2033, growing at a CAGR of 9.8% between 2026 and 2033. Robust adoption of telehealth during and after the COVID-19 pandemic, widespread smartphone and broadband penetration, and rising incidence of chronic and cosmetic skin conditions are accelerating digital access to dermatology expertise worldwide.

Governments and payers continue to institutionalize telemedicine reimbursement and cross-border e-health frameworks, which strengthen provider incentives to embed teledermatology into routine workflows. At the same time, clinical evidence shows that teledermatology achieves diagnostic accuracy comparable to in-person care for many conditions and significantly reduces wait times, enhancing both patient satisfaction and healthcare system efficiency.

Key Industry Highlights:

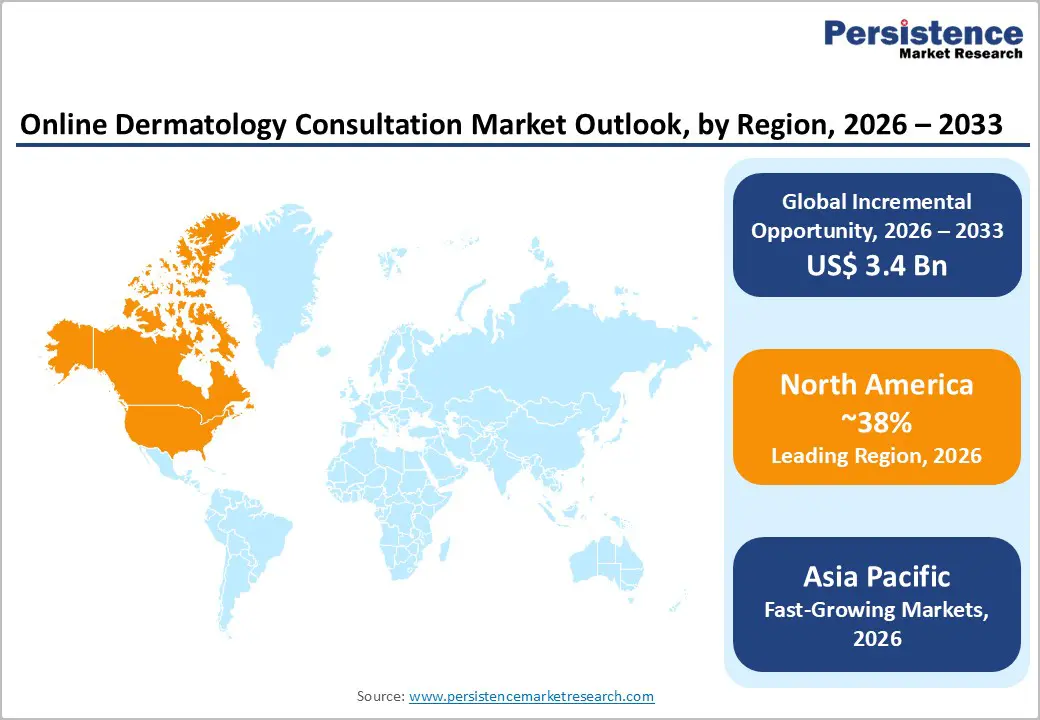

- North America remains the leading region in the online dermatology consultation market, supported by high telehealth penetration, strong payer reimbursement, and clear quality standards from organizations such as CMS, AAD, and ATA, which help institutionalize virtual dermatology in routine care pathways.

- The Asia Pacific region is the fastest-growing market, driven by rapid smartphone adoption, expanding internet access, supportive national telemedicine policies in countries such as China and India, and innovative local platforms that deliver affordable, mobile-first teledermatology across urban and rural populations.

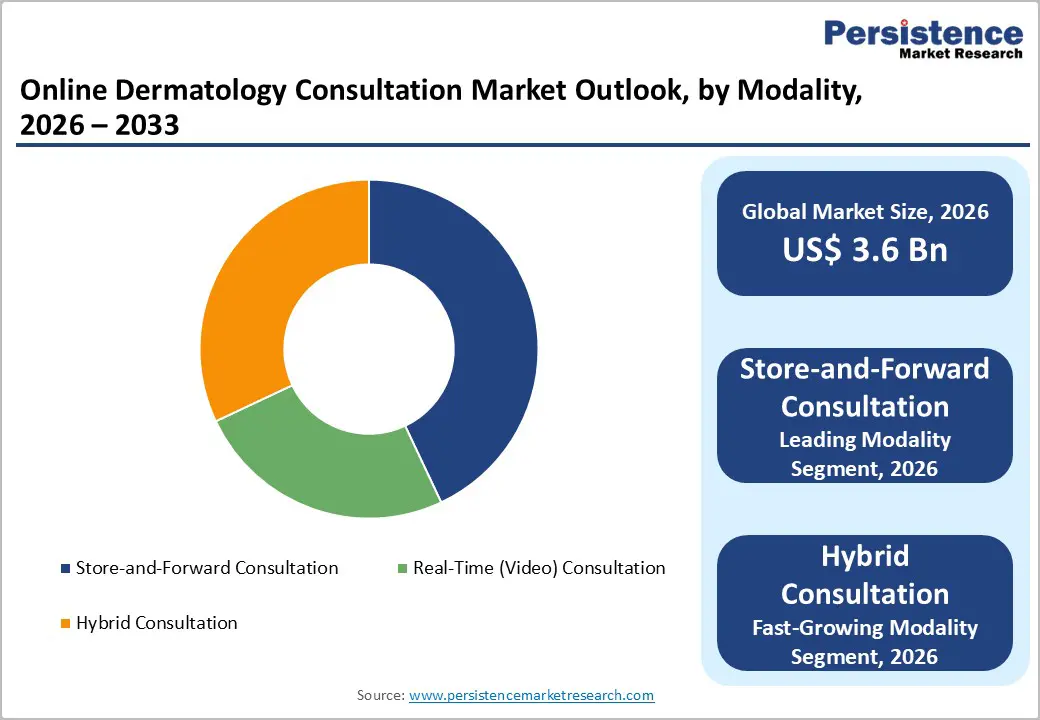

- Store-and-forward consultation is the dominant modality segment, holding about 43% share in 2025, as asynchronous image-based workflows enable efficient triage, shorter wait times, and comparable diagnostic accuracy, making this model attractive for hospitals, dermatology clinics, and primary care networks worldwide.

- Hybrid consultation models that blend store-and-forward, real-time (video) consultation, and in-person follow-up represent the fastest-growing segment, as providers seek flexible pathways to manage complex or high-risk skin conditions, leverage AI-enabled triage, and meet rising patient expectations for seamless omnichannel access to dermatology services.

- A major opportunity lies in expanding online dermatology consultation for high-burden conditions such as acne, psoriasis, eczema, and skin cancer screening in underserved regions, combining AI-supported triage, affordable mobile access, and supportive regulatory frameworks to address specialist shortages and improve early diagnosis and treatment outcomes.

| Key Insights | Details |

|---|---|

|

Online Dermatology Consultation Market Size (2026E) |

US$ 3.6 billion |

|

Market Value Forecast (2033F) |

US$ 7.0 billion |

|

Projected Growth CAGR (2026-2033) |

9.8% |

|

Historical Market Growth (2020-2025) |

9.1% |

Market Dynamics

Drivers - Rapid digital health adoption and skin disease burden

Rising global prevalence of dermatological disorders, coupled with digital health readiness, is a core driver for online dermatology consultation services. The World Health Organization (WHO) notes that skin diseases are among the most common human illnesses and are a leading cause of disability in many low- and middle-income countries, with conditions such as acne, eczema, and psoriasis affecting hundreds of millions of people. At the same time, the International Telecommunication Union (ITU) reports that over 4 billion people now use the internet, with smartphone-based access dominating in emerging markets, creating a natural channel for app-based teledermatology platforms. This combination of high unmet dermatology need and near-ubiquitous mobile connectivity enables patients to capture high-resolution images and seek care remotely, supporting strong, sustainable demand for remote consultations, particularly in home care and direct-to-consumer models.

Favorable telemedicine regulations and reimbursement expansion

Progressive telehealth regulation and reimbursement reforms significantly strengthen the growth outlook for the online dermatology consultation market. In the United States, emergency waivers during the COVID-19 public health emergency led the Centers for Medicare & Medicaid Services (CMS) to expand telehealth coverage, and many of these flexibilities are being extended or permanently ad/opted for virtual specialty care. The American Academy of Dermatology (AAD) has issued detailed teledermatology standards emphasizing access to board-certified dermatologists, appropriate licensure, and robust platform requirements, giving payers and health systems clearer quality benchmarks. In Europe, harmonization of digital health rules under frameworks such as the EU Digital Single Market and national e-health strategies has supported broader adoption of teleconsultation models within dermatology. As payers recognize comparable outcomes and reduced referral backlogs, reimbursement for store-and-forward and real-time video dermatology continues to expand, reinforcing long-term utilization.

Restraints - Unequal digital access and digital literacy gaps

Despite strong momentum, unequal access to reliable broadband, devices, and digital literacy constrains the reach of online dermatology consultation platforms. The ITU estimates that roughly 2.6 billion people remain offline globally, with significant gaps across rural areas of Africa and parts of the Asia Pacific, limiting the potential of image-heavy teledermatology applications that require stable connections and capable cameras. Even in high-income countries, older adults and marginalized populations may struggle with app navigation, image capture quality, or secure messaging tools, leading to lower engagement and inconsistent follow-through. These access and literacy barriers limit penetration among high-need groups and may require hybrid models, assisted capture in primary care, and targeted digital inclusion policies.

Regulatory, liability, and quality concerns

Regulatory complexity and medico-legal uncertainty remain key barriers, especially for cross-border and direct-to-consumer teledermatology services. The AAD stresses that teledermatology providers must maintain appropriate state or national licensure, ensure adequate liability coverage, and adhere to strict standards on prescribing, documentation, and quality assurance. Guidelines from organizations such as the American Telemedicine Association (ATA) highlight that store-and-forward and live-interactive modes must protect patient privacy, ensure secure data transmission, and include clear contingency plans for emergencies. Inconsistent rules across jurisdictions, concerns about misdiagnosis from poor-quality images, and scrutiny of business models that operate without oversight by board-certified dermatologists can slow platform expansion and increase compliance costs for market participants.

Opportunities - Scaling hybrid consultation models and AI-enhanced triage

Expanding hybrid consultation workflows that blend store-and-forward image review, real-time video follow-ups, and in-person escalation offers a significant opportunity for providers and platforms. Evidence from clinical studies indicates that store-and-forward teledermatology achieves diagnostic concordance comparable to face-to-face visits for many conditions and can substantially reduce wait times, especially for underserved populations. By layering AI-enabled image analysis, risk-based triage, and automated follow-up reminders, platforms can prioritize high-risk cases such as suspicious lesions for skin cancer screening, while routing routine acne or eczema cases to streamlined asynchronous care. Leading virtual care companies such as Teladoc Health are integrating specialty input, data-driven care coordination, and broader condition coverage, illustrating how hybrid models can deepen engagement and create differentiated value propositions for payers and health systems.

High-growth potential in Asia Pacific and emerging markets

The Asia Pacific region represents a compelling long-term opportunity for online dermatology consultation due to rising skin disease prevalence, large youth populations, and rapid digitalization. Industry analyses highlight that the Asia Pacific is the fastest-growing region for teledermatology, driven by smartphone penetration, low-cost mobile data, and government-backed digital health initiatives in countries such as China, India, and South Korea. In India, for example, the government released formal telemedicine guidelines in 2020, legitimizing teleconsultation across specialties and supporting the growth of private platforms. As local innovators combine AI-powered image capture, vernacular language interfaces, and integrated e-pharmacy delivery, online dermatology solutions can address access gaps across semi-urban and rural areas. This creates attractive opportunities for platform partnerships with hospitals, insurers, and telecom operators focused on affordable remote skin care.

Category-wise Analysis

Modality Insights

Within modality, store-and-forward consultation is the leading segment, accounting for an estimated 43% share of the online dermatology consultation market in 2025. The clinical literature consistently describes store-and-forward teledermatology as the most commonly used method, in which high-quality images and patient history are captured and securely transmitted for asynchronous specialist review. Studies show that this modality delivers diagnostic accuracy comparable to in-person care while reducing travel and wait times, particularly in primary care networks and community clinics serving low-income or remote populations.

The ability to batch cases, integrate with electronic health records, and require fewer scheduling resources than live video makes store-and-forward attractive for hospitals, dermatology clinics, and telehealth providers, reinforcing its dominant share even as hybrid consultation models grow rapidly.

Service Type Insights

In the service type segment, Diagnosis, Treatment & Prescription is expected to be the leading segment, likely capturing around 45% of the market share in 2025, as most users initially seek professional confirmation and therapy for acute or chronic skin complaints. Evidence from telemedicine programs indicates that a large proportion of teledermatology encounters involve diagnostic evaluation of rashes, lesions, or inflammatory conditions, followed by e-prescriptions for topical or systemic therapies where permissible.

Regulatory standards from the AAD emphasize that teledermatology platforms should allow the collection of adequate history and physical examination elements before prescribing, which has helped normalize virtual prescribing practices when appropriate safeguards are in place. As payers increasingly reimburse virtual specialty consults and e-prescriptions for dermatology, this comprehensive diagnostic and therapeutic service bundle remains the core revenue driver across platforms.

End User Analysis

Among end users, Homecare is anticipated to be the leading segment, accounting for an estimated 40% share in 2025, as consumers increasingly access dermatology services directly from home via mobile apps and web platforms. The COVID-19 pandemic accelerated consumer familiarity with virtual care, and many patients continue to prefer remote options for non-emergency skin concerns due to convenience, privacy, and reduced travel time. Large virtual care networks such as Teladoc Health and Amwell have expanded integrated care offerings that enable patients to consult dermatology specialists, receive prescriptions, and obtain follow-up guidance without in-person visits, reinforcing home-based use.

As connected devices, high-resolution smartphone cameras, and secure messaging become standard, homecare-centric delivery models are likely to remain the dominant locus of demand, complemented by hospitals, dermatology clinics, and specialized telehealth providers.

Regional Insights

North America Online Dermatology Consultation Market Trends and Insights

North America, led by the United States, represents the largest regional market, accounting for approximately 38% of the global online dermatology consultation market in 2025. The region benefits from a mature telehealth ecosystem, high broadband and smartphone penetration, and strong presence of virtual care leaders such as Teladoc Health, Amwell, Doctor On Demand, and MDLIVE, which all offer dermatology services within broader care portfolios. Regulatory support from agencies such as CMS, combined with state-level telemedicine parity laws and ongoing reimbursement for remote specialty consultations, has entrenched teledermatology in hospital and health system workflows.

Innovation in North America is also shaped by stringent professional guidelines and quality expectations. The AAD Teledermatology Standards outline requirements for access to board-certified dermatologists, appropriate licensure, platform capabilities, and prescription practices, prompting vendors to invest in robust clinical governance and data security. Health systems increasingly deploy integrated teledermatology pathways to reduce wait times for new dermatology referrals, while employers and payers promote virtual dermatology as part of comprehensive digital benefits. This combination of advanced regulatory frameworks, innovation-rich vendors, and payer support underpins North America’s continued leadership in this market.

Asia Pacific Online Dermatology Consultation Market Trends and Insights

The Asia Pacific region is the fastest-growing market for online dermatology consultation, supported by large populations, rising disposable incomes, and rapid digitalization in China, India, Japan, and ASEAN economies. Industry data indicate that store-and-forward modalities already dominate in several Asia Pacific markets, while hybrid consultation is the most lucrative and fastest-growing modality segment, reflecting the popularity of combining asynchronous image review with follow-up video or in-person visits. In India, the Ministry of Health and Family Welfare and NITI Aayog released national telemedicine guidelines in March 2020, providing a clear legal basis for teleconsultation and accelerating the growth of dermatology-focused platforms.

Asia Pacific also benefits from strong manufacturing and technology advantages. Regional startups and technology firms are leveraging AI-based skin analysis, low-cost smartphones, and local-language interfaces to build scalable teledermatology offerings tailored to diverse demographic and climatic conditions. Governments in countries such as China and South Korea are actively promoting digital health, including teledermatology, within national health strategies, helping address shortages of dermatologists in secondary cities and rural areas. As reimbursement mechanisms mature and partnerships with hospitals and telecom operators deepen, Asia Pacific is expected to post the highest CAGR through 2033, gradually closing the gap with North America and Europe.

Competitive Landscape

The online dermatology consultation market is highly competitive and characterized by the presence of multiple digital health platforms offering teledermatology services through mobile applications and web-based portals. Market participants focus on improving diagnostic accuracy through high-resolution image analysis, artificial intelligence integration, and secure data sharing. Service providers compete on factors such as consultation affordability, quick response time, user-friendly interfaces, and access to certified dermatologists. Strategic collaborations with healthcare providers, telehealth networks, and insurance organizations are also strengthening market reach.

Key Developments:

- In May 2025, Boots launched a nationwide dermatology training programme for pharmacists in collaboration with L’Oréal Groupe and the British Association of Dermatologists. The initiative aimed to enhance pharmacists’ ability to provide advice on common skin conditions such as acne, eczema, psoriasis, rosacea, and hyperpigmentation without requiring appointments.

- In September 2025, Sanofi launched “Real Skinformation,” an artificial intelligence-powered website designed to help healthcare professionals understand and address skincare trends and misinformation circulating on social media.

Companies Covered in Online Dermatology Consultation Market

- Teladoc Health

- Amwell

- Doctor On Demand

- Miiskin

- DirectDerm

- MDLIVE

- First Derm

- MetaOptima Technology

- ConferMED

- Doctoranytime

- HopeQure

- Neo Digital Skin Clinic

- DermatologistOnCall

- SkinIO

- Babylon Health

- SkinVision

- DermTech

Frequently Asked Questions

The global online dermatology consultation market is expected to reach approximately US$ 3.6 billion in 2026, reflecting sustained post‑pandemic telehealth adoption and growing integration of virtual dermatology services across health systems and consumer platforms worldwide.

Demand is primarily driven by rising global prevalence of skin diseases, widespread smartphone and internet access, supportive telemedicine reimbursement and regulatory frameworks, and evidence that teledermatology offers diagnostic accuracy comparable to in‑person visits while reducing wait times and improving patient convenience.

North America leads the market, supported by high digital health maturity, advanced broadband infrastructure, broad payer reimbursement for virtual specialty care, and established guidance from bodies such as CMS, AAD, and ATA that foster quality‑assured teledermatology deployment across health systems.

A major opportunity lies in scaling hybrid consultation models, and AI‑enhanced triage in high‑growth regions such as the Asia Pacific, enabling earlier detection of serious conditions like skin cancer, expanding access for rural populations, and delivering cost‑effective, personalized dermatology care at scale.

Key players include Teladoc Health, Amwell, Doctor On Demand, Miiskin, DirectDerm, MDLIVE, First Derm, MetaOptima Technology, ConferMED, Doctoranytime, HopeQure, Neo Digital Skin Clinic, DermatologistOnCall, SkinIO, Babylon Health, SkinVision, and DermTech, offering diverse virtual dermatology solutions across modalities and regions.