- Clothing, Footwear, & Accessories

- Online Apparel Market

Online Apparel Market Size, Share, and Growth Forecast, 2026 - 2033

Online Apparel Market by Product Type (Men's Apparel, Women's Apparel, Children's Apparel, Athletic Apparel), Price Range (Low, Medium, High), End-User (Women, Men, Kids), and Regional Analysis for 2026-2033

Online Apparel Market Share and Trends Analysis

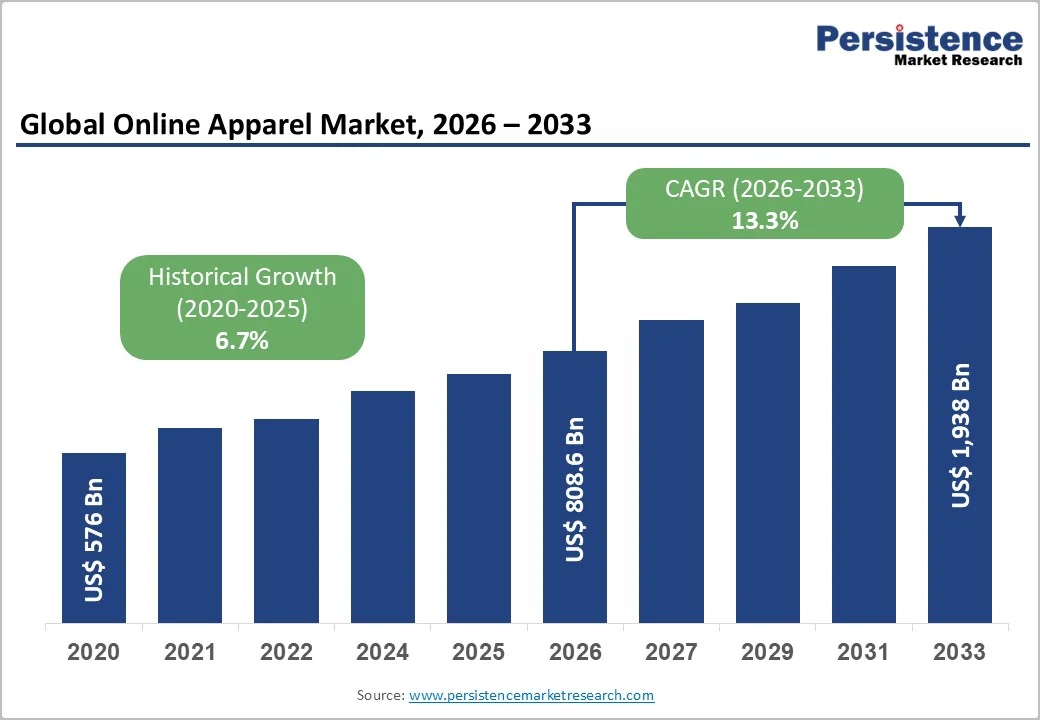

The global online apparel market size is likely to be valued at US$ 808.6 billion in 2026 and is estimated to reach US$ 1,938.0 billion by 2033, growing at a CAGR of 13.3% during the forecast period 2026−2033. This expansion reflects the rapid shift from offline to digital channels, rising smartphone and internet penetration, and higher comfort with cross-border fashion e-commerce. Structural drivers include digital payments, logistics optimization, and social-commerce ecosystems that shorten the path from discovery to purchase. At the same time, platform consolidation and regulatory scrutiny around data, returns, and sustainability are reshaping competitive strategies globally.

Key Industry Highlights

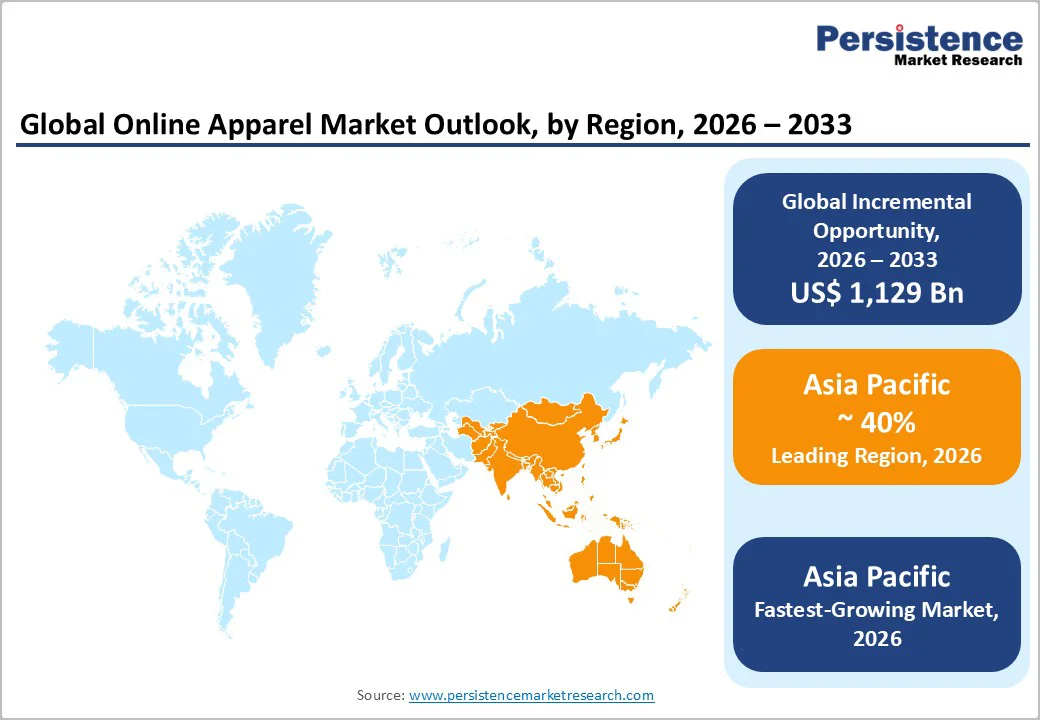

- Dominant Region: Asia Pacific is set to lead with around 40% market share in 2026 due to with huge, young consumer base with rapid digital adoption and rising spending power.

- Fastest-growing Regional Market: Asia Pacific is also likely to emerge as the fastest-growing regional market from 2026 to 2033, owing to strong local e-commerce ecosystems.

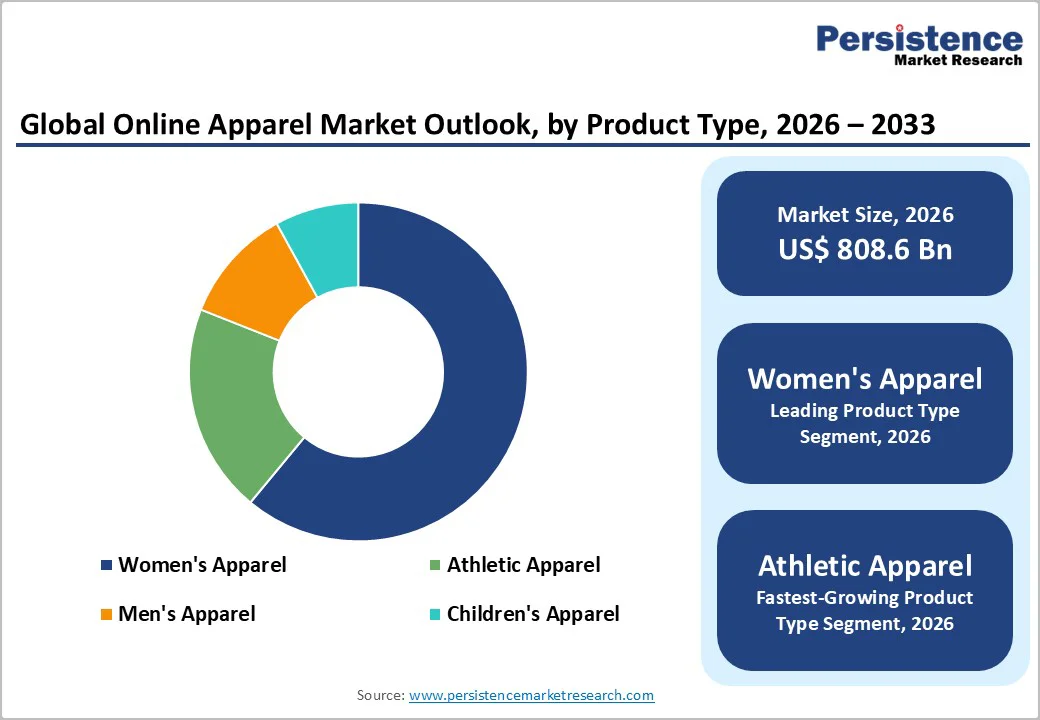

- Leading & Fastest-growing Product Type: Women’s apparel is slated to dominate with an approximate 61% market share in 2026, whereas athletic apparel is set to grow the fastest through 2033 as it sits at the intersection of health, lifestyle, and fashion.

- Leading & Fastest-growing Price Range: The low range segment is poised to leads with an estimated 46% revenue share in 2026, while high range apparel is expected to be the fastest-growing, since wealthy shoppers are increasingly buying luxury and premium fashion products digitally.

| Key Insights | Details |

|---|---|

|

Online Apparel Market Size (2026E) |

US$ 808.6 Bn |

|

Market Value Forecast (2033F) |

US$ 1,938.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

13.3% |

|

Historical Market Growth (CAGR 2020 to 2024) |

6.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Digital Access and Online Shopping Adoption

Rising digital access and online shopping adoption, which leads to more people being able to easily get online apparel, directly fuel the growth of the online apparel market growth. Widening digital penetration has created billions of connected consumers, especially in Asia, where online fashion already accounts for a substantial portion of total apparel sales, illustrating that e-commerce is now a primary, not secondary, purchasing channel. Improved digital payment systems, user-friendly shopping apps, and low-cost mobile data make it easy for urban and semi-urban shoppers to browse, compare, and order clothing at any time, which increases purchase frequency and basket size.

E-commerce platforms also leverage real-time inventory visibility, order tracking, and personalized recommendations to build trust and convenience. In several Asian markets, online already represents a substantial share of total fashion sales, demonstrating that e-commerce has moved from an experimental alternative to a primary buying channel, structurally shifting demand toward online apparel retailers and sustaining strong growth momentum.

High Return Rates, Logistics Complexity, and Margin Pressure

This is one of the fundamental operational challenges for online apparel retailers because the inability to try on clothing before purchase leads to significantly higher return rates than physical retail. This gap exists because customers cannot physically evaluate fit, fabric, or color before buying, often leading to "bracketing" ordering multiple sizes or styles with the intention of returning most of them, which doubles or triples the logistics burden.?

Rising labor, fuel, and packaging costs make these businesses even more difficult, particularly for smaller or less efficient players who lack the scale to absorb logistics expenses. As a result, weaker online apparel retailers may be forced to cut back on free return policies or charge restocking fees, which can hurt conversion and customer loyalty.

Omnichannel Integration and Data-Driven Retail Models

Omnichannel integration and data?driven retail models describe how brands blend online and offline channels into a single, seamless shopping experience to drive higher sales and better business. Traditional apparel retailers now let customers browse online, reserve items, and then click?and?collect in-store or have products shipped from the nearest store to reduce delivery times and inventory holding costs.

For online apparel platforms, this convergence creates partnership opportunities they can power brand webstores, list inventory on marketplaces, and provide last?mile logistics and technology. When players integrate data from websites, app, stores, social media, and customer service, they can forecast demand more accurately, optimize assortment and pricing by location, and run targeted promotions that increase conversion and reduce markdowns.

Category-wise Analysis

Product Type Insights

Women’s apparel is poised to be the leading product segment with an approximate 61% market share in 2026. On average, women buy clothes more frequently than men, which creates a sustainable demand for women's apparel. Women’s fashion spans a wider variety of categories, formal, casual, ethnic, athleisure, occasion wear, maternity, plus-size, and more, each with multiple styles, fits, and micro-trends so platforms allocate more digital shelf space and marketing for apparel designed for women.

Athletic apparel is likely to be the fastest-growing segment between 2026 and 2033, primarily as a result of it sitting at the intersection of health, lifestyle, and fashion. E-commerce platforms have risen to be the most efficient channel to serve the massive demand of athletic apparel, fueling momentum that makes this type of apparel a highly strategic growth area for online sellers. Average order values are typically higher than in basic casualwear because customers are willing to pay more for branded performance items and specialized products.

Price Range Insights

The low-range price segment is anticipated to lead with an approximate 46% of the online apparel market revenue share in 2026. A large number of digital shoppers are price sensitive and use of e-commerce primarily to access cheaper options than offline retail. Manufacturer-to-consumer or marketplace models minimize intermediaries and allow direct sourcing from large supplier networks, especially in Asia, which keeps prices low while still generating acceptable margins.

High-range apparel, on the other hand, is predicted to be the fastest-growing segment from 2026 to 2033. Shoppers with a higher paying capacity are exhibiting increasing comfort in buying luxury and premium fashion products digitally, and the online experience has become enriching enough to match their expectations for service, information, and risk reduction. Leading fashion houses such as Louis Vuitton, Gucci, and Chanel have fully optimized their own e-commerce sites and mobile apps, while several others are partnering with high-end marketplaces and online boutiques that curate premium assortments and maintain brand positioning.

End-User Insights

Women are expected to be the leading end-users, forecasted to hold a share of about 55% in 2026. Women account for both the largest share of fashion spending and the most intensive online shopping behavior. Women are also more responsive to digital discovery mechanisms that drive fashion e-commerce. Social media platforms such as Instagram and Pinterest are dominated by women’s fashion content, from influencer outfits to brand lookbooks and haul videos, which creates a constant stream of inspiration that directly links to product pages and shopping carts.

Men are set to represent the fastest-growing end-user segment through 2033. Online apparel platforms have also broadened men’s style offerings well beyond basics into street wear, athleisure, and occasion wear, supported by targeted digital marketing and influencer content aimed specifically at male shoppers. This has increased both purchase frequency and basket size, especially among younger men who are more trend-aware and comfortable experimenting with styles discovered through social media and creator content.

Regional Insights

Asia Pacific Online Apparel Market Trends

Asia Pacific is expected to command leadership, accounting for approximately 40% of the online apparel market share in 2026, underpinned by a vast, demographically young consumer population experiencing rapid digital adoption and accelerating disposable income growth across multiple countries. As urbanization intensifies and household incomes rise throughout the region, apparel has increasingly become a critical vehicle for personal identity expression and social status signalling that naturally redirect growing discretionary consumer spending toward fashion purchases accessed through digital platforms.

The Asia Pacific online apparel market is further strengthened by exceptionally mature and sophisticated local e-commerce ecosystems and fashion-specialist platforms that have invested substantially in competitive infrastructure and consumer experience optimization. Large regional marketplaces and fashion-focused retailers have constructed dense, integrated logistics networks spanning major metropolitan centers and secondary cities, deployed localized digital payment systems, and engineered highly customized user experiences featuring native language interfaces and culturally nuanced product assortments. This strategic infrastructure investment dramatically reduces friction in the online shopping journey, enabling seamless apparel purchasing across urban and semi-urban markets throughout the region.

Europe Online Apparel Market Trends

Europe stands as a key e-commerce apparel regional market, combining a digitally mature consumer base with robust retail and logistics infrastructure that supports seamless online fashion shopping. Markets such as the U.K., Germany, and France feature highly digital-savvy shoppers accustomed to reliable delivery services and intuitive platforms, enabling easy product browsing, comparison, and returns. This environment facilitates fast scaling for global and regional brands, ensuring consistent service quality across multiple countries and driving strong online sales growth.

The region also leads in sustainability and ethical fashion, with stringent regulations shaping apparel design, sourcing, and sales. European consumers increasingly prioritize transparency and responsible brand practices, propelling demand for eco-friendly products. This evolving market dynamic positions Europe as a trendsetter where regulatory emphasis and consumer values converge to drive demand for sustainable online fashion offerings and create competitive advantages for brands that meet these expectations.

North America Online Apparel Market Trends

North America occupies a strong position in the online apparel market landscape, driven by deeply ingrained digital shopping habits, advanced infrastructure, and a competitive retail landscape. Near-universal internet penetration and consumer comfort with online browsing, comparison, and purchasing across all age groups are supported by highly efficient logistics networks, offering fast, reliable delivery, including same-day and next-day options, and hassle-free returns.

The region's favorable regulatory and business environment further fuels market growth. Robust consumer protection laws, secure payment systems, and transparent return policies enhance shopper confidence, while supportive digital commerce policies encourage ongoing investment and innovation. The U.S., as the largest market, hosts major players such as Amazon, Nike, and Walmart, which capture significant market share and set industry standards in logistics, technology, and customer experience. This robust ecosystem fosters continuous market expansion and innovation, solidifying North America’s leadership in online apparel retail.

Competitive Landscape

The global online apparel market structure is moderately consolidated at the platform level but fragmented across brands, with global players such as Amazon, Alibaba, Shein, Zalando, and ASOS. These companies collectively hold 55% of the market share. The competitive landscape is characterized by a mix of established brands, emerging startups, and third-party marketplaces. Companies are increasingly focusing on differentiating themselves through unique value propositions, such as sustainable fashion, personalized shopping experiences, and innovative technologies. The intense competition drives continuous innovation and improvement in product offerings, customer service, and marketing strategies.

Key Industry Developments

- In November 2025, OpenAI introduced Shopping Research, a ChatGPT-powered tool that provides personalized, real-time product discovery by analyzing live data on pricing, availability, and reviews from trusted sources. Designed for complex shopping tasks, it offers tailored buyer guides and interactive feedback, helping users find the best product matches faster while maintaining user privacy and organic search results.

- In July 2025, Lululemon announced that it will enter India in the second half of 2026 through a franchise partnership with Tata CLiQ, featuring physical retail stores and online presence on Tata CLiQ Luxury and Fashion platforms. The launch includes its complete athleisure portfolio and wellness programs, marking the Canadian brand's first retail expansion in India as it capitalizes on rising demand for premium activewear in the region.

- In April 2025, Saks Fifth Avenue launched a curated multi-brand luxury storefront on Amazon Fashion called Luxury Stores at Amazon, featuring high-end brands like Dolce&Gabbana, Balmain, and Stella McCartney. This partnership aims to boost Amazon’s presence in the luxury fashion segment by offering exclusive merchandise with free shipping and an elevated shopping experience inspired by Saks' New York flagship store.

Companies Covered in Online Apparel Market

- Amazon

- Alibaba

- Zalando

- ASOS

- Boohoo Group

- JD.com

- Myntra

- Shein

- Farfetch

- Nordstrom

- Stitch Fix

- Revolve

- Lulus

- ModCloth

Frequently Asked Questions

The global online apparel market is projected to reach US$ 808.6 billion in 2026.

The market is driven mainly by rising due to growing comfort with online shopping, and proliferation of digital tools such as social media.

The market is poised to witness a CAGR of 13.3% from 2026 to 2033.

Key market opportunities include expanding into underpenetrated emerging markets, scaling premium/sustainable and niche categories online, and leveraging technologies.

Amazon, Alibaba, Shein, Zalando, and ASOS are some of the key players in the market.