- Food Ingredients & Additives

- Oat Flour Market

Oat Flour Market Size, Share, and Growth Forecast, 2025 - 2032

Oat Flour Market by Nature (Organic, Conventional), Distribution Channel (Direct, Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail), End-user (Breakfast Cereals, Bakery Products), and Regional Analysis for 2025 - 2032

Oat Flour Market Size and Trends Analysis

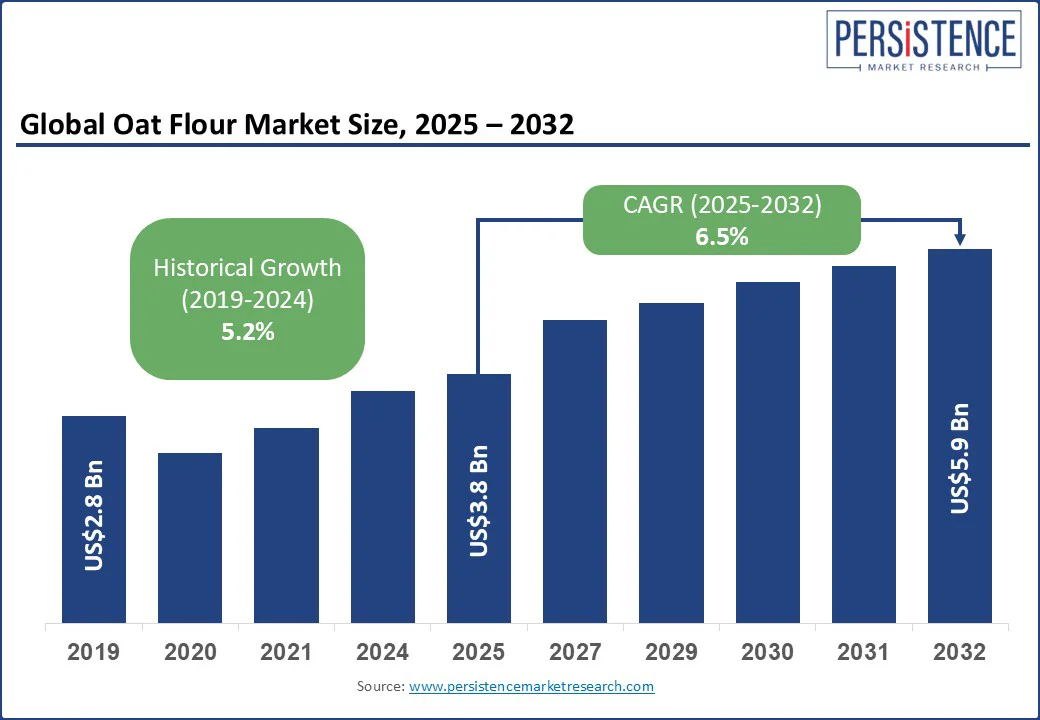

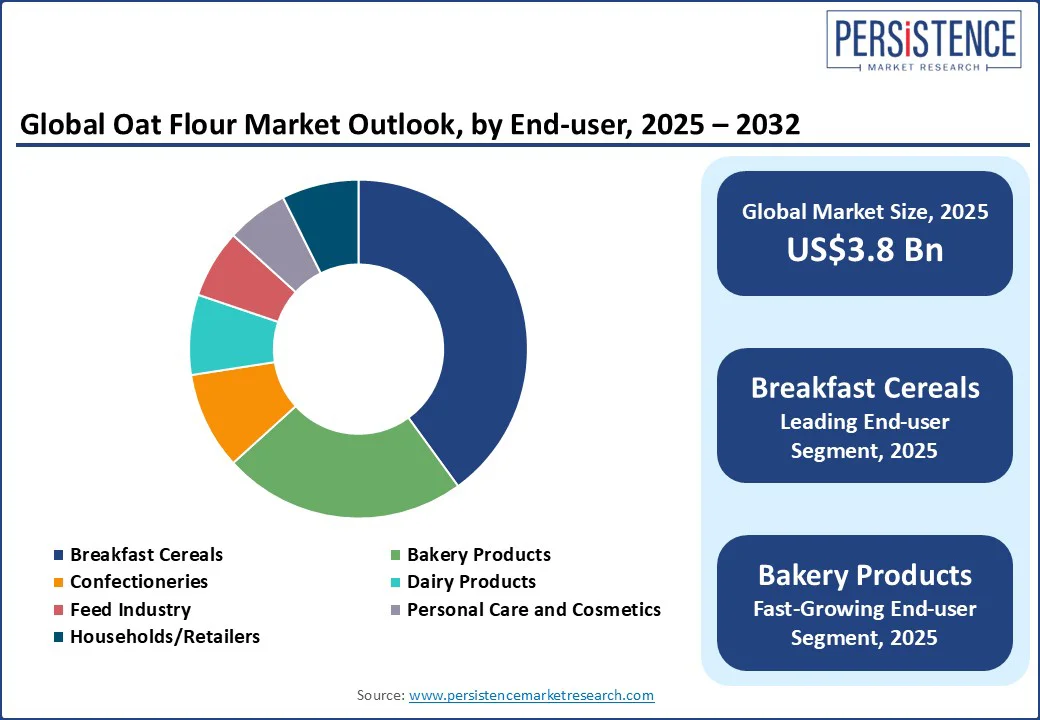

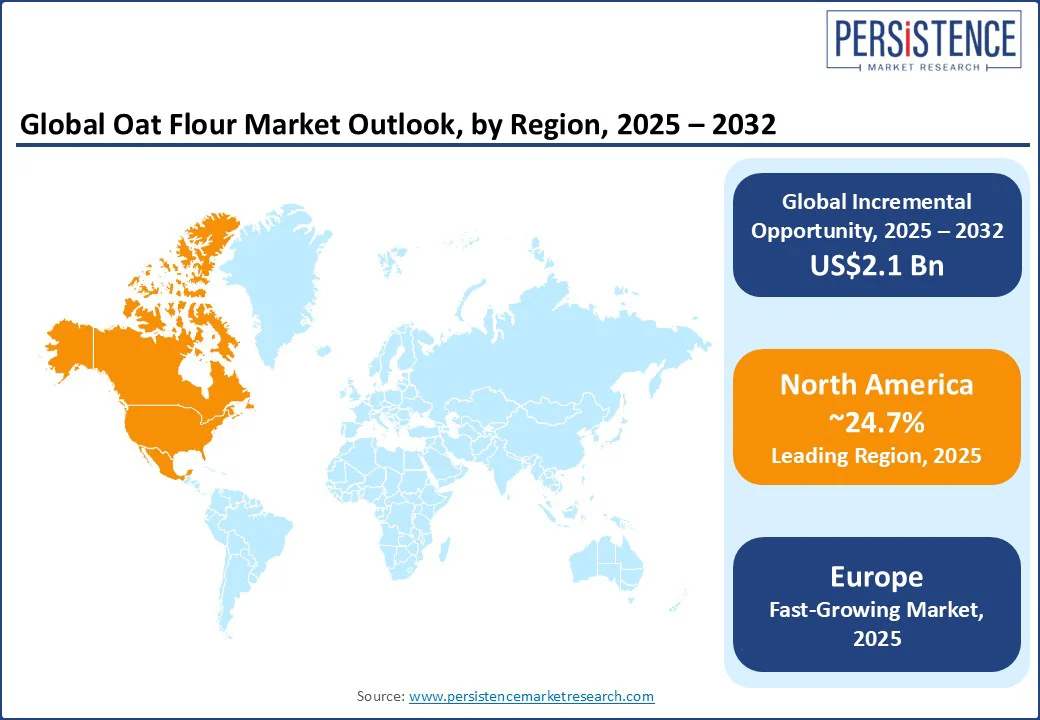

The global oat flour market size is likely to be valued at US$ 3.8 Bn in 2025 to US$ 5.9 Bn by 2032 and growing at a CAGR of 6.5% during the forecast period from 2025 to 2032.

The growth of the oat flour industry is fueled by increasing sustainability and clean-label trends globally. Leading companies are embracing targeted development, such as high-beta-glucan formulations and organic certifications to differentiate their products and gain high shares. Oat flour ingredients contain bran, germ, and the endosperm, and clinically, oat flour is highly popular for its anti-diabetic effects and lower cholesterol.

Key Industry Highlights

- Leading Region: North America, with around 24.7% share in 2025, augmented by established milling infrastructure and expansion of organic oat farming.

- Fastest-growing Region: Europe, bolstered by strict gluten-free regulations, rising clean-label preferences, and regional demand from health-conscious consumers.

- Local Sourcing Plan: Oat drink brand Alpro made a multi-million-pound investment in its U.K. operations to source 100% of its oats from local farmers in April 2025. Working with the Navara oat mill in Kettering, the company is sourcing most of its oats from farmers within 80 miles of the Mill.

- Dominant Nature: Organic, approximately 62.3% share in 2025, as consumers prioritize chemical-free farming, sustainability, and premium taste.

- Leading End-user: Breakfast cereals with nearly 39.2% share in 2025, due to oat flour’s natural fiber content, versatility in textures, and approved heart health claims.

|

Global Market Attribute |

Key Insights |

|

Oat Flour Market Size (2025E) |

US$ 3.8 Bn |

|

Market Value Forecast (2032F) |

US$ 5.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.2% |

Market Dynamics

Driver - Increasing Prevalence of Lifestyle Diseases Fuels Demand

Increasing awareness of oat flour’s role in regulating blood sugar and supporting cardiovascular health is becoming a key demand driver. This trend is especially evident in markets where lifestyle diseases are on the rise. Oat flour is naturally rich in beta-glucan, a soluble fiber that slows carbohydrate absorption, leading to a steady post-meal glucose response.

This functional benefit is increasingly showcased by health authorities, such as the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA). They allow approved heart health claims for products containing a sufficient daily intake of beta-glucan.

Cardiovascular health positioning is also effective among aging consumers and those managing high cholesterol. South Korea’s CJ CheilJedang, for example, recently introduced an oat flour bread enriched with extra beta-glucan.

The company promoted the product as a daily staple for heart care. The diabetes prevention narrative further extends the product’s appeal. In India and China, where Type 2 diabetes prevalence is rising, oat flour-based products are marketed for their low glycemic index and ability to help manage blood sugar.

Restraint - High Soluble Fiber Content Causes Digestive Discomfort

While oat flour is naturally gluten-free, it can trigger digestive discomfort in certain individuals due to its high soluble fiber content, particularly beta-glucan. For people with sensitive digestive systems, a sudden increase in oat flour consumption that causes bloating, gas, or changes in bowel movements discourages the user from repeating purchases. This is relevant for markets where consumers are not accustomed to high-fiber diets, making gradual dietary integration essential.

Another factor limiting the adoption is the risk of cross-contamination with gluten during processing. Oats are often milled in facilities that also handle wheat, barley, or rye, resulting in trace gluten presence. This poses a health risk for individuals with celiac disease or severe gluten intolerance, who require certified gluten-free oats. These concerns drive risk-averse consumers toward alternative gluten-free flours, including rice or almond flour, slowing oat flour’s penetration in the strict gluten-free segment.

Opportunity - As a Thickening Agent Spurs Growth in Plant-based Foods

Surging use of oat flour as a thickening agent in soups, sauces, and gravies is opening niche growth opportunities, specifically in the plant-based and clean-label food segments. Its fine texture allows it to blend smoothly without clumping, while its mild, slightly nutty flavor complements both savory and sweet applications. Unlike cornstarch or refined wheat flour, oat flour adds dietary fiber and protein, enabling food brands to market products with improved nutritional profiles.

It caters to the ongoing shift toward functional comfort foods, where indulgent items such as creamy mushroom soups are reformulated to provide benefits without compromising taste. In the ready-to-eat and meal kit segments, oat flour’s versatility is bolstering adoption. Brands are incorporating it into shelf-stable gravies and sauces as it withstands freezing and reheating without separating.

Category-wise Analysis

Nature Insights

In terms of nature, the market is bifurcated into organic and conventional. Out of these, the organic oat flour segment will likely account for about 62.3% of the share in 2025 as it is produced without synthetic pesticides or fertilizers, which resonates with consumers concerned about chemical residues in staple foods. This concern has become prominent in recent years following studies revealing trace pesticide contamination in non-organic oat products in markets, including the U.S. and EU, compelling several buyers to trade up to certified organic options. The premium positioning of organic oat flour also allows manufacturers to maintain high margins while targeting a loyal consumer base.

Conventional oat flour is seeing steady demand as it provides an affordable alternative to organic variants while still delivering the nutritional benefits that surge oat-based product adoption. For large-scale food manufacturers, the low price point of conventional flour allows for competitive retail pricing without sacrificing the high beta-glucan content and mild flavor that consumers expect. Conventional oat flour further benefits from a large supply base, as it is sourced from high-yield commercial farms without the certification and acreage limitations of organic production.

End-user Insights

By end-user, the market is divided into breakfast cereals, bakery products, confectioneries, dairy products, feed industry, personal care and cosmetics, and households/retailers. Among these, breakfast cereals are speculated to hold nearly 39.2% of the oat flour market share in 2025 due to the ingredient’s ability to provide a naturally creamy texture and mild flavor. This makes it easy to blend with other grains or form into extruded shapes for ready-to-eat cereals. Its beta-glucan content further enables manufacturers to market heart health benefits under approved claims in the U.S., Europe, and Australia. In these markets, regulatory frameworks permit such labeling.

Bakery products are projected to witness decent growth as oat flour delivers both functional and nutritional benefits that cater to the current consumer demands. Its fine texture and natural binding properties make it suitable for a wide range of applications, without requiring heavy modification of existing recipes. Oat flour can further replace part or all of the wheat flour in gluten-free recipes while still providing structure and moisture retention. This gluten-free adaptability is hence considered a key driver.

Regional Insights

North America Oat Flour Market Trends - Organic Products Gain Traction as Consumer Preference for Whole-grain Options Rise

North America is anticipated to account for approximately 24.7% of the share in 2025 due to the rising demand for gluten-free, plant-based, and clean-label products. The U.S. oat flour market is predicted to dominate through 2032 as consumers seek health-oriented baking, breakfast mixes, and snack formulations. Organic oat flour is experiencing steady growth as it appeals to consumers who link whole-grain and minimally processed products with better nutrition and environmental responsibility. This trend is evident in metropolitan areas where bakeries, foodservice outlets, and packaged goods companies are emphasizing organic certification on labels.

Conventional oat flour, however, continues to serve a large segment of industrial bakers and budget-driven retail brands, striking a balance between cost and nutritional content. Although demand is rising, supply chain stability remains a key concern. North America’s oat yields are vulnerable to climatic shifts, with droughts and wet harvest seasons impacting quantity and quality. Gluten-free bakeries in the U.S. have reported switching suppliers when shipments of organic gluten-free oat flour became inconsistent.

Europe Oat Flour Market Trends - Nordic Countries Witness Steady Growth Amid Gluten-free Diet Trends

Europe is poised to witness considerable growth, with Germany, the U.K., and France leading in terms of consumption and processing. This is attributed to a rising consumer shift toward organic, gluten-free, and clean-label products. At the same time, the presence of a well-developed milling infrastructure that caters to both large-scale food manufacturers and artisanal producers is pushing growth. Nordic countries, specifically Sweden, are exhibiting momentum, with oat flour use skyrocketing in baking due to the increasing popularity of vegan and gluten-free diets.

Europe’s strict gluten-free regulatory environment is another key factor influencing the market. European Union (EU) norms require oat-based products to contain less than 20 ppm of gluten, which has increased compliance costs and slowed product launches. Some new gluten-free entrants have withdrawn entirely due to annual compliance costs exceeding half a million dollars, while others have faced delays of up to six months before products could be released. These norms, while challenging for producers, also create a competitive advantage for established brands that have the resources to meet these standards consistently.

Asia Pacific Oat Flour Market Trends - Adoption in Infant Nutrition Surges in Australia and New Zealand

Asia Pacific has emerged as a key market for oat flour owing to rising health consciousness as consumers shift toward high-fiber and gluten-free products. Additionally, increasing awareness of celiac disease, interest in plant-based diets, and the adoption of Western-style baking trends in urban areas are propelling demand. In South Korea, cafés and boutique bakeries are introducing gluten-free muffins, pancakes, and breads made from oat flour, often marketed as healthier and trendier alternatives to wheat-based products.

In Australia and New Zealand, oat flour is making inroads into infant nutrition, with brands using it in baby food blends for its hypoallergenic profile and gentle digestibility. They are targeting parents seeking clean-label and minimally processed ingredients. Retail channels are broadening their oat flour ranges. Supermarkets such as Woolworths and Coles in Australia now dedicate more shelf space to gluten-free oat flours. In Japan, convenience store chains, including Seven-Eleven, stock single-serve oatmeal and granola formats using oat flour.

Competitive Landscape

The global oat flour market is characterized by a layered competitive structure, with large grain processors such as Richardson, Grain Millers, Morning Foods, and Blue Lake Milling controlling bulk supply for industrial use. Consumer-facing brands, including Bob’s Red Mill and Arrowhead Mills, lead packaged retail segments. This creates a divide where global processors influence pricing and availability through control of raw grain and milling capacity. Mid-sized specialty mills capture margins through organic or gluten-free positioning, and small brands compete by highlighting origin, milling techniques, or unique nutritional claims.

Key Industry Developments:

- In March 2025, researchers from Tecnológico Nacional de México, Universidad Autónoma del Estado de Hidalgo, and Benemérita Universidad Autónoma de Puebla published a study detailing the development of a gluten-free fettuccine-type pasta formulated with oat flour, quinoa flour, and cactus (Opuntia) cladode pulp. All new formulations had low carbohydrate levels and exhibited improved bioactive compound profiles, resulting up to 2.8-fold higher antioxidant activity compared to the control.

- In January 2024, Nature’s Path launched a new range of organic and high-quality flours at Natural Products Expo West. The flours are made of a wide variety of grains, including oats, processed through traditional low-temperature milling and mixed at low speed for the best results.

Companies Covered in Oat Flour Market

- The Hain Celestial Group, Inc.

- Naturex S.A.

- Bagrry’s India, Ltd.

- Richardson International Ltd.

- Bay State Milling Company

- Bob’s Red Mill Natural Foods

- Co-operative Bulk Handling Ltd. (Blue Lake Milling Pty.)

- Grain Millers, Inc.

- Morning Food

- Unigrain Pty Ltd

Frequently Asked Questions

The oat flour market is projected to reach US$ 3.8 Bn in 2025.

Rising consumer demand for gluten-free food and the integration of oat flour into convenient formats such as ready-to-eat cereals are the key market drivers.

The oat flour market is poised to witness a CAGR of 6.5% from 2025 to 2032.

Developments in oat flour-based thickening agents and expanding retail infrastructure in emerging countries are the key market opportunities.

The Hain Celestial Group, Inc., Naturex S.A., and Bagrry’s India, Ltd. are a few key market players.