- Sporting Goods & Equipment

- North America Hockey Rinks Market

North America Hockey Rinks Market Size, Share, Trends and Growth Forecast, 2025 - 2032

North America Hockey Rinks Market by Rink Type (Refrigerated Ice Rinks, Synthetic Ice Rinks), Material (Concrete, HDPE, UHMW Polyethylene), Application (Ice Hockey, Park & Recreation, Residential, Seasonal, Others), and Regional Analysis for 2025 - 2032

North America Hockey Rinks Market Share and Trends Analysis

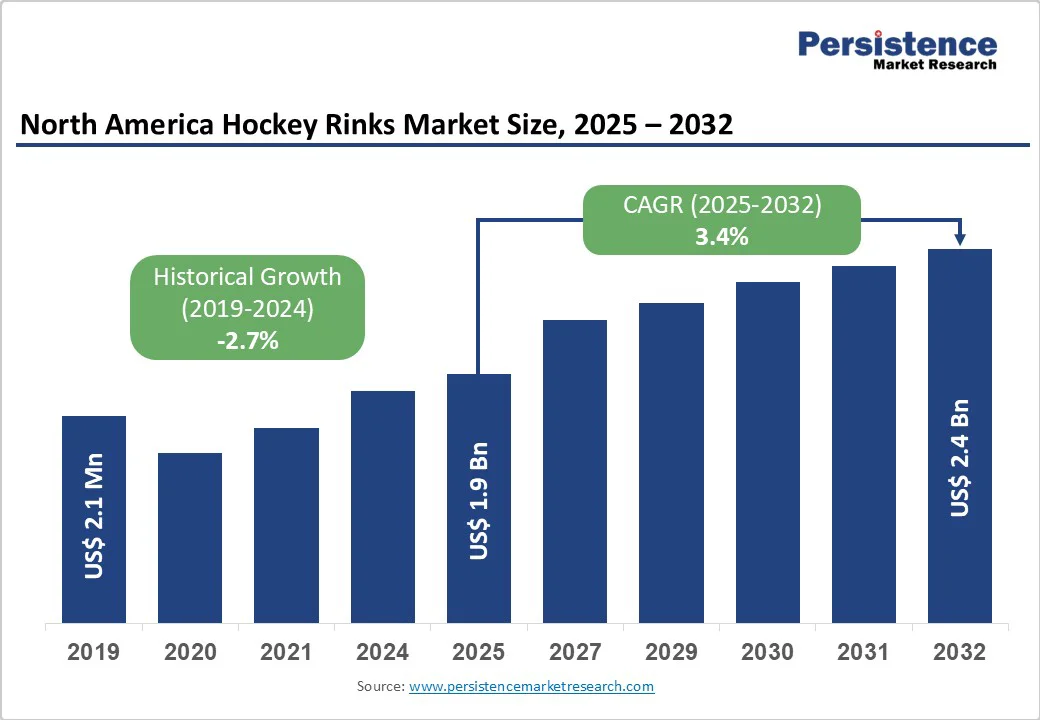

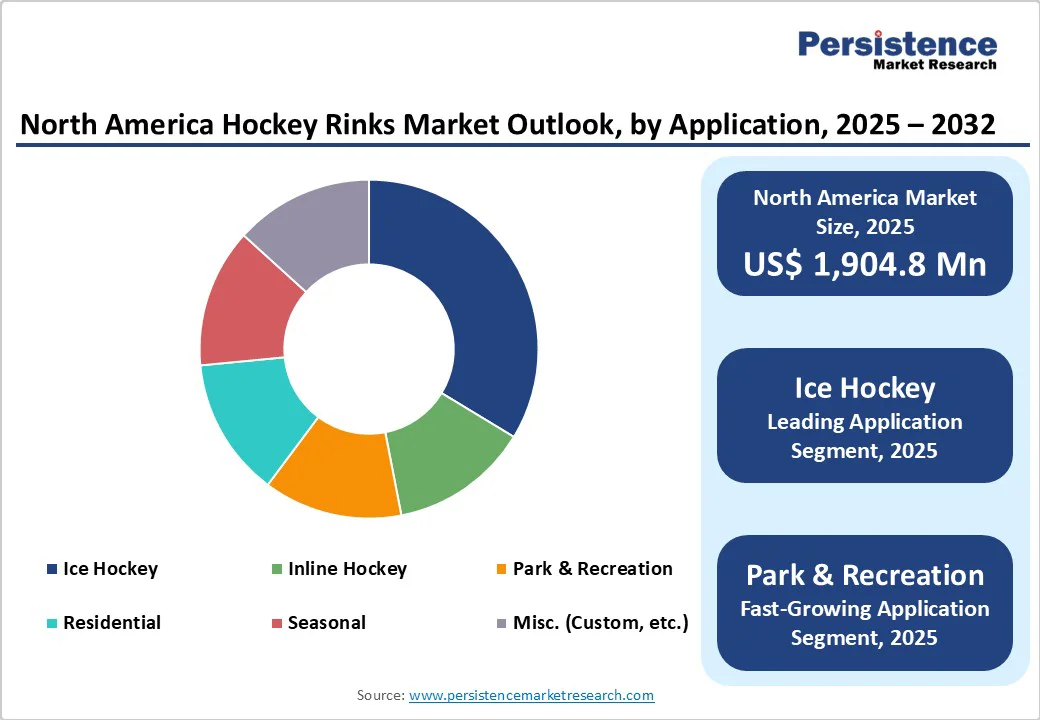

North America hockey rinks market size is likely to be valued at US$ 1.9 billion in 2025, and is projected to reach US$ 2.4 billion by 2032, growing at a CAGR of 3.4% during the forecast period 2025-2032. Regulatory support for youth sports and efforts to enhance the accessibility of hockey are further reinforcing the long-term market outlook.

Key Industry?Highlights:

- Dominant Rink Type: Refrigerated ice rinks are likely to dominate with around 92% market share in 2025, as they are preferred for professional and indoor league games.

- Fastest-growing Rink Type: Synthetic rinks are set to be the fastest-growing through 2032, since they require lower capital and operating costs and flexible installation options.

- Leading Material: Concrete will remain the leading material for rink construction with about 92.6% revenue share in 2025, ensuring durability and consistent ice quality.

- Dominant Application: Ice hockey is set to dominate with 74.5% of the North America hockey rinks market revenue share in 2025, driven by structured leagues, youth programs, and professional usage.

- Opportunity Landscape: The market shows opportunities in synthetic/modular rinks and green facility standards, enhancing energy efficiency, accessibility, and community engagement.

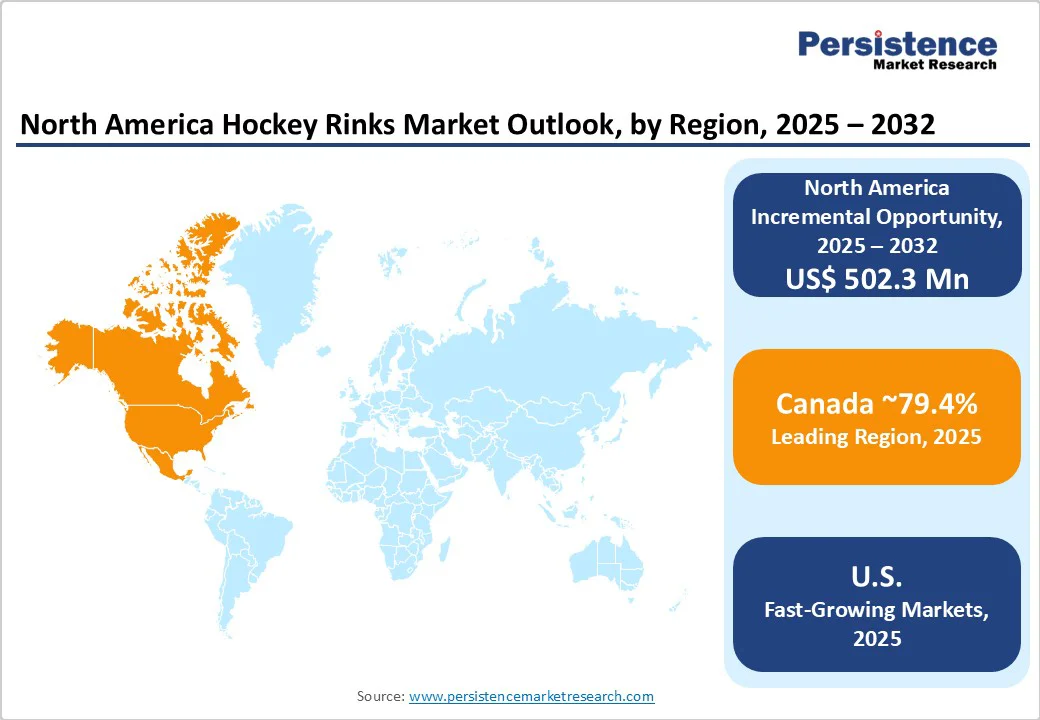

- Regional Dynamics: Canada rules the market, housing nearly 80% of the rinks in North America, followed by the U.S. at 20.6%.

| Key Insights | Details |

|---|---|

|

North America Hockey Rinks Market Size (2025E) |

US$ 1.9 Bn |

|

Market Value Forecast (2032F) |

US$ 2.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

-2.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Modernization and Energy Efficiency Initiatives

Modernization is a central theme, underpinned by a shift from inefficient to efficient energy technologies in rink operations. Traditional rinks report annual energy consumption of 1,000 MWh, with refrigeration accounting for 43% and heating 26%. Conversely, rinks equipped with advanced technologies reduce total consumption to 460 MWh yearly, while refrigeration’s share rises to 65% and ventilation, including miscellaneous uses, makes up 22%. This transition yields significant operational savings, regulatory compliance, and environmental benefits, directly boosting capital reinvestment and facility upgrades throughout the region.

Sustained engagement in ice hockey, particularly youth and community-level participation, remains a fundamental driver for rink demand. In the U.S., organized by USA Hockey, the country counts 555,935 registered players (2021/22 data), including 322,003 junior participants and 75,832 female players. The enduring legacy of the sport, anchored by near-century-old organizations, supports a robust infrastructure - 1,535 indoors and 1,000 outdoor rinks across a population of 324 million. Leadership, high-profile leagues, and international success (top-ranked U.S. women’s hockey, 5th-ranked men’s hockey) all reinforce the need for facility maintenance and expansion, translating to a consistent pipeline of demand for rink construction, upgrades, and services.

Capital and Operational Cost Barriers

Significant initial capital investment, recurring maintenance, and the escalating costs of utilities, insurance, and labor challenge both private and municipal rink operators. The upfront costs of efficient refrigeration and advanced construction materials, while mitigating long-term expense, can delay adoption for smaller market participants. Regulatory compliance, particularly regarding energy consumption, safety standards, and environmental impact, can introduce additional complexity and hinder immediate market entry or expansion.

Simultaneously competing winter sports and recreational activities, industry consolidation, and fluctuating weather patterns for outdoor facilities contribute to volatile utilization rates and revenue predictability. Long-term decline in U.S. ski areas, for example, spotlights structural challenges that can also threaten hockey infrastructure. Rinks in climates experiencing warmer winters face higher operational costs and uncertain usage windows for outdoor facilities, introducing additional market risks and impacting investor confidence.

Expansion of Synthetic and Modular Rinks

The rise of synthetic ice rinks and modular construction technology creates actionable opportunities for operators and investors. These solutions can reduce reliance on traditional refrigeration, cut energy expenditures, and permit rapid setup in spaces previously unsuited for hockey. Companies that develop materials with enhanced durability and skating performance stand to benefit from these shifts. Modular rinks can also facilitate event-based models, allowing for temporary or mobile installations at festivals, fairs, or in regions with limited permanent infrastructure. Governments and sponsors can leverage such formats to promote physical activity, support grassroots initiatives, and encourage broader engagement with sport. The ability to offer year-round skating without significant climatic dependency addresses unmet needs in underserved market segments and climatic zones.

Emerging environmental standards and norms for green sports facilities are catalyzing product innovation and service differentiation. Operators that invest in renewable energy integration, advanced building management systems (BMS), and digitally optimized maintenance routines realize competitive advantages through lower costs, improved corporate image, and access to incentive programs. Moreover, advanced analytics and remote monitoring platforms enable predictive maintenance and better asset lifecycle management, reducing unplanned downtime and operational overhead. Integration with community wellness and smart city initiatives opens up new partnership and funding pathways, positioning innovative providers for future growth and collaboration with public stakeholders.

Category-wise Analysis

Rink Type Insights

Refrigerated ice rinks are anticipated to dominate, accounting for approximately 92% share in 2025. This dominance stems from their ability to deliver premium ice quality, host professional or organized league play, and enable year-round operation in indoor facilities. Because of their higher performance, they remain the preferred choice for flagship arenas, competitive use, and high-capacity operations.

Synthetic rinks are expanding as they require substantially lower capital and operating costs compared to mechanical refrigeration. Their lower maintenance burden and ease of installation make them appealing in municipalities or private contexts where full refrigerated systems are impractical. Particularly in regions with lower ambient thermal loads or where seasonal use is intended, such rinks attract incremental adoption. Although starting from a small base, the growth potential of this segment is significant for the forecast period 2025-2032.

Material Insights

Concrete is the standard material for the ice slab and sub-base in traditional refrigerated rinks, prized for durability, thermal mass, and consistent ice properties. It is expected to hold a 92.6 % hockey rinks market share in 2025, as most professional and permanent facilities use concrete slabs, often embedded with piping and insulation layers.

High-density polyethylene (HDPE) is seeing faster adoption, especially in modular or synthetic rink systems. Its advantages include lightweight construction, modular installation, portability for seasonal or temporary setups, and lower initial capital outlay. It enables turnkey synthetic surfaces or overlay options in non-concrete environments. As synthetic rink use increases, HDPE usage rises in tandem.

Application Insights

Ice hockey applications are slated to dominate with about 74.5% share in 2025. The structured league systems, professional, collegiate, amateur, school programs, and youth systems drive most rink construction, as ice hockey remains the core use case supporting demand for premium ice surfaces and scheduling priority in facility design.

Park & recreation use is expanding, driven by municipal investments in public skating, multi-season flotation zones, and recreational ice offerings. Flexible recreational installations allow municipalities to justify rink projects as public amenity enhancements, especially in colder regions. As a result, recreational use of hockey rinks in North America is rising at a notable rate and is expected to continue growing from 2025 to 2032.

Country Insights

Canada Hockey Rinks Market Trends

Canada dominates the North America hockey rink market, holding close to 80% share, driven by its strong hockey culture and dense rink infrastructure, with approximately 2,860 indoor and 5,000 outdoor rinks recorded in 2021/22. This extensive network supports ongoing replacement and new rink construction in both remote and growing areas. The Canadian government has been integrating hockey into public policy and regional development for decades, ensuring consistent investment in facilities. Key growth factors include municipal and provincial funding, backing from national organizations such as Hockey Canada, and community revitalization efforts in colder regions. Regulatory frameworks of the country also emphasize energy efficiency and environmental compliance through provincial codes and permit regimes. The market features specialists in rink construction, modular system providers, and energy services companies.

United States Hockey Rinks Market Trends

The U.S. holds approximately 20.6% of the North America hockey rink market share, operating about 1,535 indoor and 1,000 outdoor rinks that serve 555,935 registered players, including 322,003 juniors. However, the country’s per-capita rink density remains lower than Canada’s due to diverse geography and population distribution. Youth development programs, facility modernization grants, and rink construction in emerging regions such as the Sun Belt states drive market activity. Regulatory agencies enforce refrigerant standards of the U.S. Environmental Protection Agency (EPA), energy efficiency codes, and local permitting to maintain compliance in new projects. Public-private partnerships (PPPs), municipal collaborations, and commercial turnkey providers actively manage investments and facility upgrades. The market can most likely expand by targeting underserved areas and updating ageing infrastructure to support growing participation.

Competitive Landscape

The North America hockey rink market structure is fragmented, with the top key players collectively holding around 33% of the market share. Leading companies focus on constructing and operating indoor and outdoor rinks, offering refrigerated and synthetic surfaces, and providing related services such as athlete training and maintenance solutions. Market participants are competing on factors such as technology adoption, rink design, energy efficiency, and multi-functional facility offerings. Strategic partnerships, regional expansions, and investment in state-of-the-art facilities are common approaches to strengthen market positioning and capture niche segments within the broader, fragmented landscape.

Key Industry Developments

- In October 2025, Enterprise, the NHL, and the NHLPA announced a multiyear extension of their North American partnership, reinforcing brand visibility across hockey arenas. The deal ensures continued in-arena advertising through digitally enhanced dasherboards and broadcast integrations, enhancing fan engagement across rink environments. This partnership supports commercial activities within hockey facilities and strengthens the overall value ecosystem surrounding North American hockey rinks.

- In October 2025, the first all-girls hockey rink in Atlantic Canada officially opened in Cape Breton, Nova Scotia, representing a significant milestone for female athletes in the region. This new facility is designed exclusively to support and encourage girls' participation in hockey by providing a safe and empowering environment free from the challenges often faced in co-ed settings. It offers specialized programming tailored to female players of all ages and skill levels, helping to foster development, confidence, and enjoyment of the sport.

- In July 2025, the newly opened Wings Arena in Stamford, Connecticut, established a state-of-the-art hub for ice hockey and athlete development. The facility combines year-round hockey training programs by EN Hockey with advanced rehabilitation and performance services from Matterhorn Fit, creating an integrated environment for skill development, recovery, and athletic performance. This development strengthens regional hockey infrastructure in North America and provides a model for multi-functional rinks that serve both competitive athletes and community users.

Companies Covered in North America Hockey Rinks Market

- Glice

- Xtraice Home

- PolyGlide Ice

- KwikRink Synthetic Ice

- HockeyShot

- SmartRink

- Skate Anytime

- D1 Backyard Rinks

- Synthetic Ice Solutions

- Custom Ice Inc.

- Cascadia Sport Systems Inc.

- Iron Sleek Inc

- CTC Group Canada Inc.

- Total Sport Solutions Inc.

Frequently Asked Questions

The North America hockey rinks market is projected to reach US$ 1.9 billion in 2025.

A few of the leading players in the market are Glice, Xtraice Home, PolyGlide Ice, and KwikRink Synthetic Ice.

Modernization and energy efficiency initiatives, sustained youth and community participation, and supportive government and institutional policies are driving the market.

The market is poised to witness a CAGR of 3.4% from 2025 to 2032.

Key market opportunities include the expansion of synthetic and modular rinks for flexible, year-round use and the adoption of green facility standards with smart infrastructure for operational efficiency and sustainability.