- HVAC

- North America HVAC Equipment Market

North America HVAC Equipment Market Size, Share, and Growth Forecast, 2026 – 2033

North America HVAC Equipment Market by Equipment Type (Heating Equipment, Ventilation Equipment, Air Conditioning Equipment), Building (Office Buildings, Others), End-user (Residential, Commercial, Industrial), and Regional Analysis for 2026 – 2033

North America HVAC Equipment Market Size and Trends Analysis

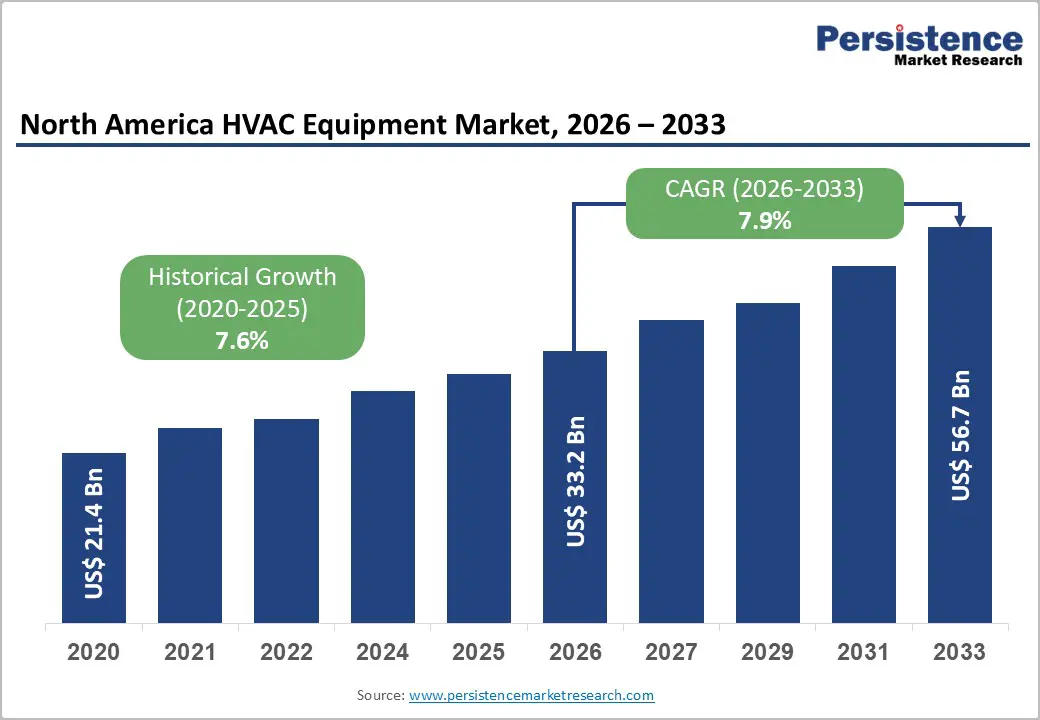

The North America HVAC equipment market size is likely to be valued at US$33.2 billion in 2026 and is expected to reach US$56.7 billion by 2033, growing at a CAGR of 7.9% during the forecast period from 2026 to 2033, driven by stringent energy-efficiency regulations, accelerated replacement of aging HVAC systems, and a rising emphasis on indoor air quality (IAQ) following heightened health and safety awareness.

Increasing adoption of heat pumps, smart and connected HVAC systems, and low-GWP refrigerants is reshaping product demand across the region. Factors such as climate variability, growing urbanization, smart building integration, and favorable incentive programs in the U.S. and Canada continue to strengthen the market outlook, positioning North America as a mature yet innovative market.

Digitalization and predictive maintenance technologies are enhancing system efficiency, reliability, and lifecycle performance across end-user segments.

Key Industry Highlights:

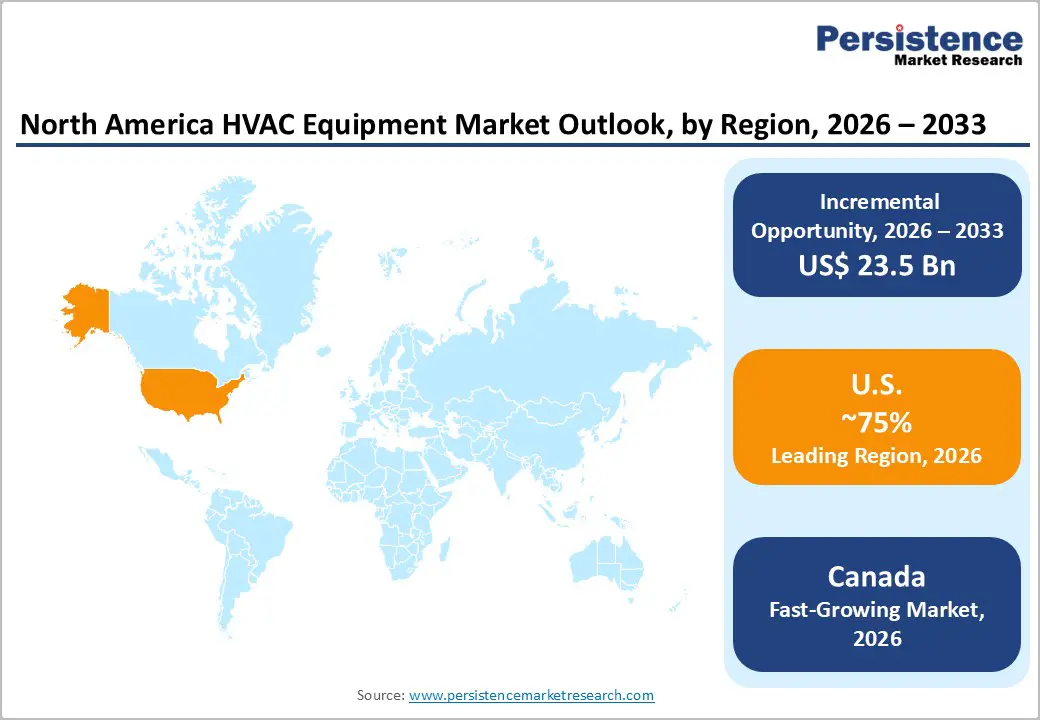

- Leading Region: The U.S. is anticipated to be the leading region, accounting for a market share of 75% in 2026, driven by strong construction activity, extreme weather demand, and supportive energy-efficiency and refrigerant regulations.

- Fastest-growing Region: Canada is likely to be the fastest-growing region, supported by diverse climate-driven demand, strong energy-efficiency regulations, and growing adoption of smart and sustainable building technologies.

- Leading Equipment Type: Heating equipment is projected to represent the leading equipment type in 2026, accounting for 40% of the revenue share, driven by cold-climate demand and efficiency-driven replacements.

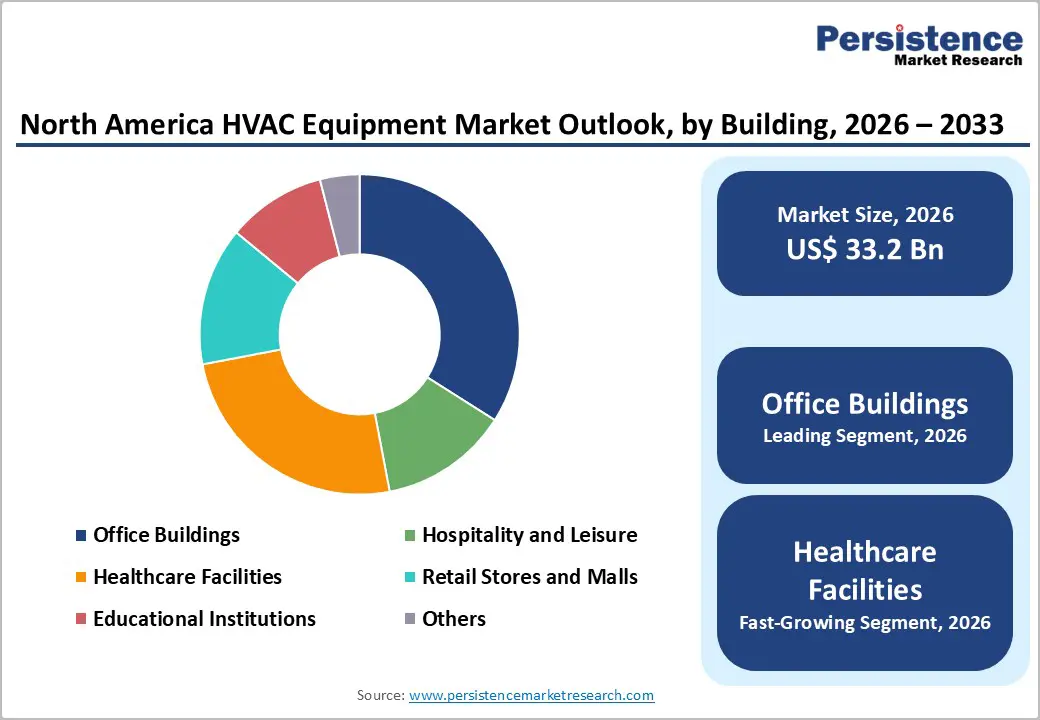

- Leading Building: Office buildings are anticipated to be the leading building type, accounting for over 35% of the revenue share in 2026, supported by commercial retrofits and energy management upgrades.

- Leading End-user: The residential segment is projected to represent the leading end-user type in 2026, accounting for 45% of the revenue share, driven by widespread home installations and replacement demand.

| Key Insights | Details |

|---|---|

| North America HVAC Equipment Market Size (2026E) | US$33.2 Bn |

| Market Value Forecast (2033F) | US$56.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements and Indoor Air Quality Focus

Modern HVAC systems increasingly incorporate smart and connected technologies, including IoT-enabled sensors, AI-based predictive maintenance, and advanced building automation systems. These innovations enable real-time monitoring of temperature, humidity, airflow, and energy consumption, allowing operators to optimize performance, reduce energy costs, and extend system lifespan.

Variable refrigerant flow (VRF) technology and high-efficiency heat pumps are gaining traction due to their ability to provide precise climate control and reduce energy consumption, aligning with regional energy-efficiency regulations. Technological advancements also support remote diagnostics, automated fault detection, and predictive servicing, reducing downtime for commercial and institutional buildings.

Indoor air quality (IAQ) has emerged as a critical focus in the North America HVAC equipment market, particularly in the wake of the COVID-19 pandemic and heightened health awareness. Commercial spaces, healthcare facilities, educational institutions, and residential buildings are prioritizing improved ventilation, filtration, and air purification systems to mitigate airborne contaminants, allergens, and pathogens. Advanced technologies, such as HEPA filtration, ultraviolet germicidal irradiation (UVGI), and electrostatic air purifiers, are increasingly integrated into HVAC systems to enhance IAQ.

Smart controls allow continuous monitoring of CO levels, particulate matter, and humidity, ensuring optimal air quality and occupant comfort. Regulatory and certification programs, including ASHRAE standards and well building guidelines, reinforce IAQ requirements in building design and retrofits.

Regulatory Compliance and Transition Challenges

Manufacturers and end-users must navigate a complex and evolving landscape of energy, environmental, and safety standards. In the U.S., the Department of Energy (DOE) enforces strict minimum efficiency performance standards for air conditioners, heat pumps, and furnaces, while the Environmental Protection Agency (EPA) regulates refrigerants under programs such as the Significant New Alternatives Policy (SNAP) to limit the use of high global warming potential (GWP) substances. Canada imposes similar standards through federal and provincial codes, focusing on energy efficiency and emissions reduction. Compliance with these regulations often requires redesigning products, upgrading manufacturing facilities, and conducting extensive testing to meet certification requirements. These measures increase production costs and create barriers for smaller manufacturers or new entrants.

Transition challenges also act as a restraint, particularly during the shift from traditional HVAC systems to energy-efficient, low-GWP, and smart technologies. Building owners and facility managers face high upfront costs when retrofitting older systems to comply with new regulatory mandates, including incentives or rebates that do not fully offset installation expenses.

The adoption of advanced HVAC technologies such as variable refrigerant flow (VRF) systems, heat pumps, and IoT-enabled equipment requires skilled labor, specialized installation, and ongoing maintenance, creating additional operational challenges. Supply chain disruptions and component shortages, particularly for advanced compressors, heat exchangers, and electronic controls, complicate transitions. The phase-out of conventional refrigerants under EPA and DOE regulations necessitates careful handling, retrofitting, or replacement of existing equipment, which can delay adoption and increase costs.

Heat Pump Electrification and Incentives

Heat pumps, which provide both heating and cooling by transferring thermal energy rather than generating it through combustion, offer a sustainable alternative to traditional fossil fuel-based systems. In the U.S., rising electricity adoption, coupled with declining natural gas use in residential and commercial buildings, is encouraging the transition toward electrified HVAC solutions. Technological advancements in variable-speed compressors, enhanced refrigerants with low global warming potential (GWP), and inverter-driven systems have improved heat pump efficiency, reliability, and adaptability in colder climates. Canada’s diverse climate also drives demand for high-performance heat pumps capable of maintaining indoor comfort in extreme temperatures.

Incentive programs amplify the adoption of heat pump technologies, making the transition financially viable for homeowners, businesses, and institutions. In the U.S., the Inflation Reduction Act (IRA) provides substantial tax credits and rebates for high-efficiency heat pumps, encouraging the replacement of aging fossil fuel-based systems. Utilities also offer performance-based incentives, rebates, and financing schemes that reduce upfront costs and accelerate deployment in residential, commercial, and industrial buildings.

Similarly, Canada provides federal and provincial programs, such as the Canada Greener Homes Grant, which support the installation of efficient heat pumps in homes and public buildings. These incentives, combined with regulatory support and growing consumer awareness of energy savings, drive market expansion while helping to achieve regional carbon reduction targets.

Category-wise Analysis

Equipment Type Insights

Heating equipment is expected to lead the North America HVAC equipment market, accounting for approximately 40% of revenue in 2026, driven by colder climates in parts of the U.S. and Canada, where reliable furnaces and heat pumps are essential for residential and commercial heating. Demand is bolstered by energy-efficiency transitions, regulatory mandates, and incentive programs promoting the replacement of older, inefficient heating systems. For example, Carrier Corporation has actively expanded its high-efficiency furnace and heat pump offerings across North America, integrating smart thermostats and low-GWP refrigerants to comply with DOE and EPA standards. The segment benefits from strong adoption in both newly constructed homes and commercial buildings undergoing retrofits.

The air conditioning equipment segment is expected to be the fastest-growing segment in 2026, supported by increasing temperatures, urbanization, and growing commercial development. Advanced technologies such as variable refrigerant flow (VRF) systems, inverter-driven compressors, and smart connected AC units are driving the adoption.

For example, Daikin Industries Ltd. introduced energy-efficient VRF air conditioning solutions capable of providing precise climate control for commercial buildings, including office complexes and hospitals, while significantly reducing energy consumption. Urban heat islands and higher occupancy buildings have intensified the need for efficient air conditioning, particularly in commercial and institutional spaces.

Building Type Insights

Office buildings are projected to lead the market, capturing around 35% of the revenue share in 2026, supported by commercial retrofits, energy management initiatives, and rising corporate sustainability goals. Corporations are increasingly upgrading their HVAC systems to improve energy efficiency, reduce operating costs, and maintain regulatory compliance.

For example, Trane Technologies has implemented advanced HVAC solutions, including smart thermostats, VRF systems, and efficient chillers in large office buildings across the U.S., providing enhanced energy management and occupant comfort. The leading share is also supported by continuous growth in the commercial construction sector and corporate emphasis on ESG (environmental, social, and governance) commitments, which often include high-efficiency HVAC deployments.

Healthcare facilities are likely to be the fastest-growing building type in 2026, driven by stringent indoor air quality (IAQ) requirements and post-pandemic upgrades for ventilation and filtration systems. Hospitals and medical centers increasingly require HVAC systems capable of advanced filtration, humidity control, and reliable airflow to prevent contamination and maintain patient safety. For example, Lennox International Inc. has provided high-efficiency air handling units and ventilation systems tailored for healthcare facilities, ensuring compliance with ASHRAE and CDC guidelines.

The growth is supported by ongoing investments in new hospitals, renovation of older facilities, and stricter IAQ standards in North America. Regulatory compliance and the focus on patient health drive continuous adoption of technologically advanced HVAC systems.

End-user Type Insights

The residential segment is expected to lead, accounting for approximately 45% of the revenue in 2026, driven by widespread home installations, retrofits, and replacement demand. Energy-efficient heating and cooling systems are increasingly adopted due to federal and state incentives, tax rebates, and utility-sponsored programs.

For example, Rheem Manufacturing Company Inc. has expanded its residential HVAC portfolio with high-efficiency furnaces, air conditioners, and heat pumps that meet DOE and ENERGY STAR standards, driving consistent adoption across homes. The segment benefits from population growth, new housing developments, and the need to replace aging equipment, especially in colder regions of the U.S. and Canada.

The commercial segment is likely to represent the fastest-growing segment, supported by office, retail, and institutional projects emphasizing sustainability, comfort, and operational efficiency. Companies and institutions increasingly invest in advanced HVAC technologies such as VRF systems, smart building controls, and energy-efficient chillers to reduce costs and comply with regulatory requirements. For example, Johnson Controls International PLC delivered integrated building management and HVAC solutions for commercial spaces, combining energy efficiency, real-time monitoring, and predictive maintenance. Growth in commercial construction, retrofits, and ESG-driven sustainability initiatives contributes to the rapid expansion of the segment.

Regional Insights

U.S. HVAC Equipment Market Trends

The U.S. is anticipated to be the leading region, accounting for a market share of 75% in 2026, driven by technological innovation, energy efficiency mandates, and evolving consumer expectations. Regulatory frameworks, including DOE minimum efficiency standards, EPA refrigerant rules, and incentives under the Inflation Reduction Act (IRA), are encouraging the adoption of high-efficiency HVAC systems across residential, commercial, and industrial segments. Electrification trends, particularly through heat pumps, are accelerating as building owners shift away from fossil fuel-based heating solutions, while smart thermostats, IoT-enabled HVAC systems, and predictive maintenance technologies are reshaping product offerings.

The U.S. market includes increasing adoption of variable refrigerant flow (VRF) systems, modular chillers, and energy-efficient furnaces tailored to meet regional climate requirements. For example, Trane Technologies has launched innovative VRF solutions and connected HVAC systems that optimize energy use while improving occupant comfort in commercial buildings.

Incentives and rebates offered by federal and state programs are accelerating the replacement of aging systems, supporting both sustainability goals and operational cost reduction. The growth of smart buildings and commercial retrofits is driving demand for integrated HVAC controls and predictive analytics tools that monitor energy consumption and maintenance needs.

Canada HVAC Equipment Market Trends

Canada is likely to be the fastest-growing region, due to diverse climatic conditions, energy efficiency mandates, and increasing awareness of indoor air quality (IAQ). The Canadian federal government, along with provincial authorities, has implemented stringent energy-efficiency regulations and incentives, such as the Canada Greener Homes Grant, promoting the adoption of high-efficiency heating and cooling systems. Residential demand remains strong, particularly for furnaces, heat pumps, and air conditioners, as homeowners replace aging systems to comply with federal and provincial standards. Commercial and institutional sectors are also expanding their HVAC infrastructure, focusing on retrofits, smart building integration, and energy management solutions.

Technological advancements and sustainability initiatives are the key trends shaping Canada’s HVAC market. For example, Daikin Industries Ltd. introduced high-efficiency heat pumps and VRF systems tailored for Canada’s varying climate zones, integrating smart controls for energy optimization and improved comfort. Electrification of heating through heat pumps is gaining traction as an alternative to gas-fired furnaces, supported by government incentives and environmental policies targeting carbon reduction. Smart HVAC systems with IoT-enabled monitoring, predictive maintenance, and remote control features are being increasingly adopted in commercial buildings, schools, and hospitals.

Competitive Landscape

The North America HVAC Equipment market exhibits a moderately fragmented structure, driven by a mix of large multinational manufacturers and numerous regional and niche players competing across residential, commercial, and industrial segments. Hold significant influence with broad product portfolios that span heating, cooling, ventilation, and smart HVAC systems, leveraging strong R&D capabilities, energy efficiency innovations, and expansive distribution networks to maintain market presence.

With key leaders including Carrier Global Corporation, Trane Technologies plc, Daikin Industries Ltd., Johnson Controls International plc, and Lennox International Inc., competition in the North America HVAC equipment market is shaped by innovation, strategic expansion, and product differentiation strategies. These players compete through continued investment in energy efficient and smart systems, adoption of connected HVAC technologies, and enhancement of service models that integrate predictive maintenance and digital controls.

Key Industry Developments:

- In January 2026, SPX Technologies, Inc. completed the acquisition of Thermolec Ltd. for approximately US$140 million, strengthening its HVAC segment with highly complementary custom electric heating solutions. The acquisition expanded SPX’s Electric Heat portfolio by integrating Thermolec’s expertise in electric duct heating, boilers, and related HVAC solutions across commercial, multi-family residential, and light industrial applications. Since Thermolec generated most of its revenue in Canada, SPX plans to accelerate growth by expanding Thermolec’s presence in the U.S. market while leveraging its strong Canadian customer base to enhance Marley Engineered Products’ regional reach.

- In February 2025, Lennox International Inc. launched its “Lennox Powered by Samsung” mini-split and Varix™ variable refrigerant flow (VRF) product lineups through its joint venture, Samsung Lennox HVAC North America. The new ductless heat pump systems targeted the growing residential and commercial demand for energy-efficient, low-GWP, and smart HVAC solutions across the U.S. and Canada. The mini-split systems offered room-to-room comfort, variable-capacity operation, SmartThings app connectivity, and eligibility for federal energy-efficiency tax credits, while the Varix™ VRF lineup addressed multi-zone commercial applications with flexible control and reduced operating costs.

Companies Covered in North America HVAC Equipment Market

- Johnson Controls International PLC

- Daikin Industries Ltd

- Lennox International Inc.

- Electrolux AB

- Emerson Electric Co.

- Carrier Corporation

- Rheem Manufacturing Company Inc.

- Uponor Corp.

- Ingersoll Rand Inc. (Trane Inc.)

- Nortek Global HVAC, LLC

Frequently Asked Questions

The North America HVAC equipment market is projected to reach US$33.2 billion in 2026.

The North America HVAC equipment market is driven by stringent energy-efficiency regulations, replacement of aging systems, rising focus on indoor air quality, climate variability, and growing adoption of smart and electrified HVAC technologies.

The North America HVAC equipment market is expected to grow at a CAGR of 7.9% from 2026 to 2033.

Key market opportunities include the electrification of heat pumps driven by incentives, the growth of smart and connected HVAC systems, the retrofitting of aging buildings, and the increasing demand for advanced indoor air quality solutions.

Johnson Controls International PLC, Daikin Industries Ltd, Lennox International Inc., and Electrolux AB are the leading players.