- Industrial Machinery

- Mine Ventilation System Market

Mine Ventilation System Market Size, Share, and Growth Forecast 2026 - 2033

Mine Ventilation System Market by System Type (Mechanical Ventilation, Natural Ventilation, Hybrid Ventilation), Component (Fans & Blowers, Ducts & Air Channels, Sensors & Monitoring Systems, Others), Device (Primary Ventilation System, Secondary Ventilation System, Auxiliary Ventilation System), End-user (Mining, Construction), and Regional Analysis, 2026 - 2033

Mine Ventilation System Market Size and Trend Analysis

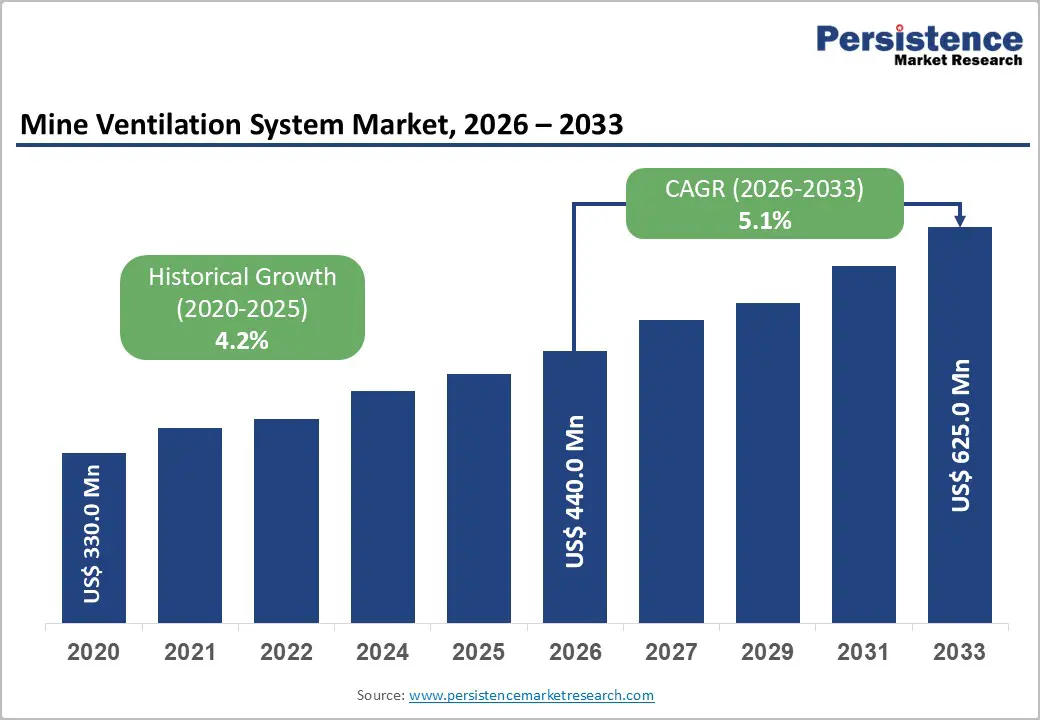

The global mine ventilation system market size is expected to be valued at US$ 462.8 million in 2026 and projected to reach US$ 691.3 million by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

The market is driven by stringent safety regulations worldwide that require advanced ventilation to mitigate underground hazards. Regulatory bodies like MSHA in the US enforce air quality standards, improving miner safety, while deeper mining operations globally demand effective systems for gas dilution and temperature control. Growing investments in automation and smart ventilation, such as China’s 17% increase in coal-mine spending, further support market growth.

Key Industry Highlights:

- Leading Region: North America leads the mine ventilation system market with 36.8% share in 2025, supported by strict MSHA regulations and advanced ventilation upgrades.

- Fastest-Growing Region: Asia Pacific, holding 34.5% share in 2025, remains the fastest-growing hub driven by expanding underground mining and rising automation adoption.

- Leading System Type: Mechanical Ventilation dominates with a 67.9% share in 2025, ensuring controlled airflow, gas dilution, and compliance in deep hazardous mines.

- Fastest-Growing System Category: Hybrid and automated ventilation systems are growing rapidly as mines prioritize energy efficiency and real-time airflow optimization.

- Key Technology Opportunity: Ventilation-on-Demand (VOD) is a major growth opportunity, enabling smart airflow control while significantly reducing energy consumption in deep underground operations.

| Key Insights | Details |

|---|---|

| Mine Ventilation System Size (2026E) | US$ 462.8 million |

| Market Value Forecast (2033F) | US$ 691.3 million |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 5.2% |

Market Dynamics

Drivers - Stricter Safety Regulations Driving Demand for Advanced Mine Ventilation Systems

Global regulatory focus on miner safety is propelling demand for modern ventilation solutions. In the US, MSHA data demonstrates that enhanced airflow monitoring and compliance with the MINER Act have significantly reduced underground incidents. Similarly, the International Labour Organization (ILO) emphasizes proper ventilation to minimize respiratory hazards from gases such as methane. These regulations are prompting mining operators worldwide to invest in upgraded, reliable ventilation systems to ensure safety and operational continuity.

Many countries are actively enforcing compliance, driving large-scale equipment upgrades. For instance, in Australia, government reports indicate that approximately 85% of underground mines had modernized their ventilation systems by 2024. This regulatory push is increasing demand for efficient, durable equipment, prompting manufacturers to innovate and expand their offerings to meet stringent safety standards.

Expansion of Deeper and Mechanized Underground Mining Increasing Ventilation System Adoption

The growth of deeper underground mines is creating a pressing need for more powerful and scalable ventilation systems. Mechanized operations, especially in the Asia-Pacific region, require a continuous supply of fresh air to maintain safe working conditions and optimize productivity. The China National Coal Association reports a 22% increase in imports of ventilation equipment into India, reflecting rising demand driven by increased coal and mineral extraction.

As mining operations extend deeper and become more mechanized, conventional ventilation solutions are often insufficient. This trend encourages investment in advanced systems that control gas concentrations, dust, and temperature in confined underground spaces.

Restraints - High Capital Investment and Operational Costs Limiting Ventilation System Adoption

Implementing advanced mine ventilation systems requires significant capital expenditure, creating a barrier for smaller and mid-sized mining operators. High-performance fans, sensors, and automation technologies require substantial upfront investment and often compete with budget allocations for extraction and other operational priorities. In addition, deep underground mines consume significant energy to operate ventilation systems, and older legacy setups tend to be inefficient, further increasing operating expenses.

These high costs often delay modernization or expansion of ventilation infrastructure, particularly in regions where mining profitability is tightly constrained. As a result, operators may continue to rely on outdated systems that do not fully comply with safety regulations, thereby restricting overall market growth. The need for cost-effective yet reliable solutions is becoming a critical challenge for vendors and end-users alike.

Shortage of Skilled Workforce Hindering Effective Operation and Maintenance of Advanced Systems

The adoption of modern mine ventilation solutions is constrained by a global shortage of trained personnel to operate and maintain complex systems. Advanced setups, including IoT-enabled and automated controls, require specialized technical knowledge that is often lacking in mining workforces. This gap forces companies to rely on external consultants or service providers, increasing operational costs and delaying modernization efforts.

Without sufficiently skilled staff, routine maintenance, troubleshooting, and optimization of ventilation systems become challenging, compromising safety and efficiency. Mining companies face the dual challenge of investing in sophisticated equipment while simultaneously ensuring the availability of qualified personnel to manage it effectively, which limits the speed and scale of market adoption.

Opportunities - Rising Adoption of Automation and IoT-Enabled Smart Ventilation Systems

The increasing integration of automation and IoT technologies in mining operations presents significant growth opportunities for the mine ventilation system market. Smart ventilation systems enable real-time monitoring of airflow, gas concentrations, temperature, and dust levels, improving safety and operational efficiency. Companies can optimize energy usage and reduce costs by controlling airflow based on actual demand, known as ventilation-on-demand (VOD), which is gaining traction globally, particularly in deep and mechanized mines.

Mining operators are actively investing in these intelligent solutions to comply with stringent safety regulations and enhance productivity. The adoption of digital monitoring and predictive maintenance tools also enables quicker responses to potential hazards, reducing downtime and improving worker safety. Vendors providing scalable, smart ventilation solutions are therefore well positioned to capture growing market demand.

Expansion of Deep Underground Mining Operations Driving Ventilation System Demand

Global trends toward deeper and more mechanized underground mining are fueling demand for advanced ventilation systems. Deeper mines experience higher temperatures, dust levels, and hazardous gas concentrations, such as methane, requiring robust ventilation to ensure safe operations. The Asia-Pacific region, particularly China and India, is experiencing rapid growth in coal and metal mining, driving demand for robust, scalable ventilation solutions to ensure operational continuity and worker safety.

This trend creates opportunities for manufacturers and service providers to offer high-capacity fans, advanced sensors, and integrated control systems capable of handling complex underground environments. As mining operations continue to deepen and expand worldwide, the requirement for efficient, reliable ventilation solutions is expected to accelerate, offering significant long-term growth potential.

Category-wise Analysis

System Type Insights

Mechanical Ventilation leads the market with a 67.9% share in 2025, owing to its reliability in delivering controlled airflow in hazardous underground environments. High-capacity fans and blowers provide essential gas dilution and temperature control, ensuring compliance with regulatory standards such as MSHA. Mechanical systems are particularly prevalent in deep coal and metal mines, where natural ventilation is insufficient due to geographic or structural constraints. Their proven efficiency and safety advantages make them the preferred choice among mining operators globally.

Hybrid and automated ventilation systems are emerging as the fastest-growing segment. These solutions combine mechanical and natural methods or integrate smart sensors and automation to optimize airflow in real time. Adoption is accelerating in deep and mechanized mines, particularly in the Asia-Pacific region, where a focus on energy efficiency, operational safety, and digital monitoring is driving increased adoption of advanced hybrid systems.

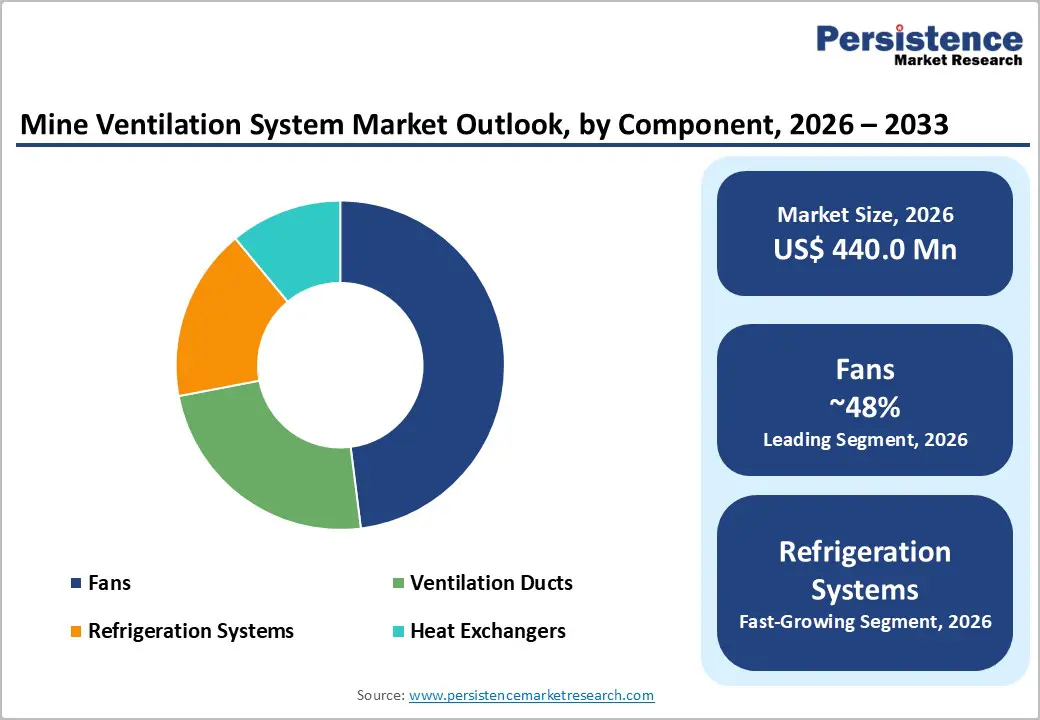

Component Insights

Fans & blowers account for 40% of the 2025 market, forming the core of mine ventilation systems by generating airflow through primary and auxiliary tunnels. Modular designs from players like TLT-Turbo achieve up to 90% efficiency, making them vital for energy-intensive mining operations. Their scalability allows operators to configure complex networks in deep and expansive underground mines, supporting both safety and productivity. The dominance of fans and blowers underscores their essential role in delivering reliable, consistent ventilation in critical mining environments.

Sensors, monitoring devices, and automation controls are the fastest-growing component segments. Advanced gas detection, temperature monitoring, and IoT-enabled control systems are increasingly deployed to dynamically optimize airflow, reduce energy consumption, and enhance real-time safety management. Growth is especially notable in newly mechanized and deeper mining projects, where precision ventilation is crucial for worker protection and operational efficiency.

Device Insights

Primary Ventilation Systems account for 45% of the 2025 market, forming the backbone of underground airflow by supplying fresh air to main tunnels. These systems are essential for meeting legal standards and ensuring the safety of miners in high-risk environments. Integration with advanced monitoring devices enhances their effectiveness, particularly in large-scale operations where maintaining continuous, reliable airflow is critical. The stronghold of primary systems reflects their foundational role in underground ventilation networks.

Auxiliary and secondary ventilation devices are the fastest-growing categories, designed to deliver fresh air to working faces and confined areas that primary systems cannot fully cover. Deployment is increasing in complex mine layouts and deep excavation projects, particularly in Asia-Pacific expansions. Real-time monitoring and flexible configuration allow these systems to adapt to dynamic underground conditions, improving safety and operational productivity in targeted zones.

End-user Insighs

The mining sector dominates with 85% share in 2025, as ventilation is indispensable for underground safety amid growing global production. Coal, metal, and mineral mines require continuous airflow to dilute gases, remove dust, and regulate temperature, making ventilation a regulatory and operational priority. Compliance with MSHA and EU safety standards further drives investment in robust systems, positioning mining as the primary end user of advanced ventilation solutions rather than construction or tunneling applications.

Construction and tunneling projects represent the fastest-growing end-user segment. While historically smaller in adoption, the expansion of underground urban infrastructure projects, metro systems, and deep civil works is creating new demand for flexible, modular ventilation solutions. These projects benefit from scalable fans, auxiliary systems, and smart monitoring devices to maintain safe working conditions in confined, subterranean spaces where airflow requirements are rising.

Regional Insights

North America Mine Ventilation System Market Trends

North America accounts for approximately 36.8% of the global mine ventilation system market in 2025, with the U.S. leading due to stringent MSHA regulations. These rules emphasize proper underground airflow, reducing violations and enhancing safety following the MINER Act. Innovation hubs in the U.S. are developing IoT-enabled monitoring systems that enable real-time tracking of gas levels, temperature, and dust in deep coal and gold mines. Federal funding supports modernization projects, ensuring compliance while promoting sustainable practices in mining operations.

Canada also contributes to regional growth, adopting advanced fans and modular ventilation systems for both coal and metal mining operations. The trend toward smart, automated ventilation is rising across North America, as operators seek energy efficiency and continuous regulatory compliance, solidifying the region’s dominance in both market share and technological adoption.

Europe Mine Ventilation System Market Trends

Europe’s mine ventilation system market is projected to grow at a CAGR of 6.1% during the forecast period, driven by strong regulatory frameworks and technological modernization. Germany and the UK lead in the deployment of high-efficiency fans, aligning with EU methane regulations that prohibit high-emission venting starting in 2027. France and Spain are investing in automation to facilitate the transition from coal mining and maintain safe underground operations, thereby fostering innovation and the sharing of best practices across borders.

The emphasis on energy-efficient ventilation and regulatory compliance encourages European operators to adopt smart monitoring and automated airflow solutions. Cross-border collaborations enable technology transfer, while deeper and mechanized mines increase demand for integrated ventilation systems that combine safety, productivity, and sustainability.

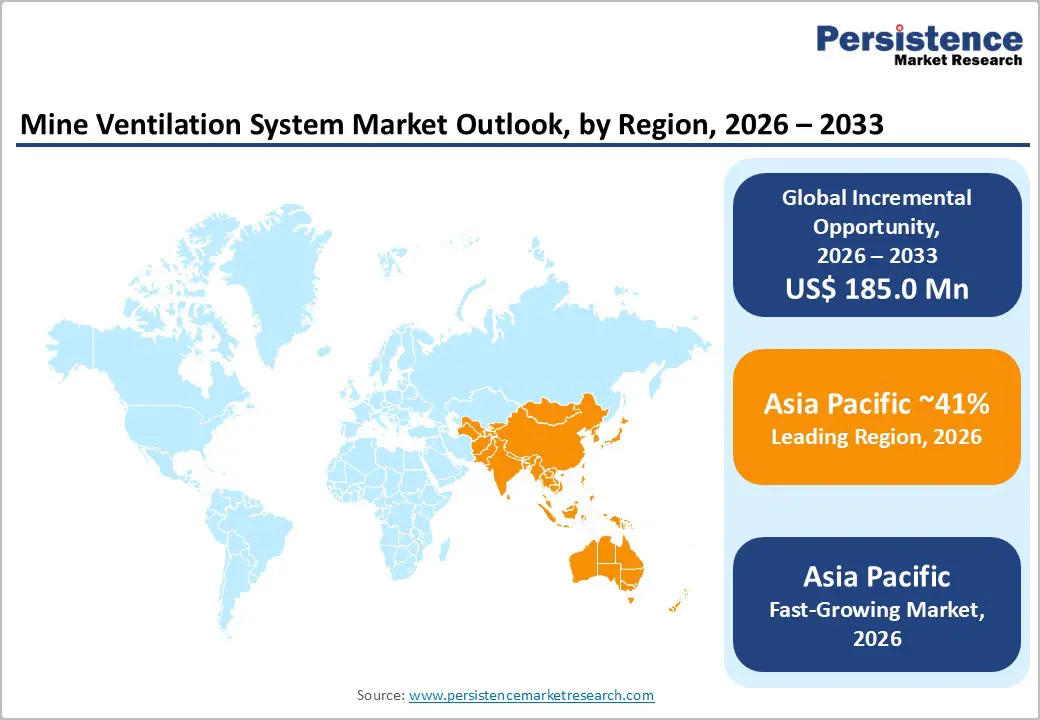

Asia Pacific Mine Ventilation System Market Trends

Asia-Pacific accounts for approximately 34.5% of the global market in 2025, led by China, which increased ventilation investments by 17% in 2024 to support its substantial coal output. Mechanized mining operations in India and ASEAN countries are leveraging local manufacturing capabilities to adopt cost-effective ventilation systems while maintaining safety standards. Japan contributes advanced precision technologies, particularly in automation and monitoring, supporting regional growth in both coal and metal mining sectors.

Urbanization and the expansion of underground infrastructure in the Asia-Pacific region drive further adoption of scalable ventilation solutions. Investments in smart monitoring, auxiliary systems, and high-capacity fans are increasing, enabling operators to efficiently manage deeper mines, improve safety, and reduce energy consumption. This combination of demand drivers positions the region as a critical growth hub for the global mine ventilation system market.

Competitive Landscape

The mine ventilation system market is moderately consolidated, with major players strengthening their positions through ongoing R&D in energy-efficient fans, automation, and advanced airflow-control technologies. Competitive strategies increasingly focus on enhancing safety compliance, improving system reliability, and delivering high-performance solutions for deeper and more mechanized underground operations.

Companies are also expanding through acquisitions, partnerships, and integration of IoT-enabled monitoring platforms. Key differentiators include modular system designs, digital ventilation controls, and long-term service contracts. Emerging business models such as ventilation-as-a-service are gaining traction, providing recurring revenue streams while helping mining operators reduce upfront costs.

Key Developments:

- In March 2025, Howden Group launched next-generation energy-efficient underground ventilation fans, reducing power consumption by nearly 40% while integrating IoT-based monitoring to enhance airflow control, safety compliance, and operational efficiency in deep mining environments.

- In November 2024, Epiroc introduced its Ventilation Control Kit, enabling real-time air quality monitoring and automated airflow adjustments in smart mines, supporting safer working conditions and improved productivity in increasingly mechanized underground operations.

- In 2024, TLT-Turbo advanced its modular mining fan portfolio, achieving up to 90% efficiency for primary ventilation applications, offering scalable designs that optimize airflow delivery, reduce energy costs, and strengthen safety performance in large underground mines.

Companies Covered in Mine Ventilation System Market

- Sandvik AB

- Epiroc AB

- Howden Group Ltd.

- ABB Ltd.

- TLT-Turbo GmbH

- Twin City Fan & Blower

- New York Blower Company

- ABC Industries

- Zitron

- ABC Ventilation Systems

- Clemcorp Australia

- Sibenergomash-BKZ

- Hurley Ventilation

- Parag Fans & Cooling Systems

- Chicago Blower

Frequently Asked Questions

The global mine ventilation system market is expected to reach US$ 462.8 million in 2026.

Stricter safety regulations, such as MSHA standards, are driving the adoption of advanced underground ventilation systems.

North America leads with 36.8% share in 2025, supported by strong regulatory enforcement and modernization.

Ventilation-on-Demand (VOD) systems offer major growth potential by improving efficiency and reducing energy consumption in deep mines.

Key manufacturers include Sandvik AB, Epiroc AB, Howden Group Ltd., TLT-Turbo GmbH, and Zitron.