- HVAC

- Ventilation System Market

Ventilation System Market Size, Share, and Growth Forecast, 2026 - 2033

Ventilation System Market By System Type (Mechanical Ventilation, Centralized Ventilation, Others), Product Type (Energy Recovery Ventilators (ERVs), Heat Recovery Ventilators (HRVs), Others), Application and Regional Analysis for 2026 - 2033

Ventilation System Market Size and Trends Analysis

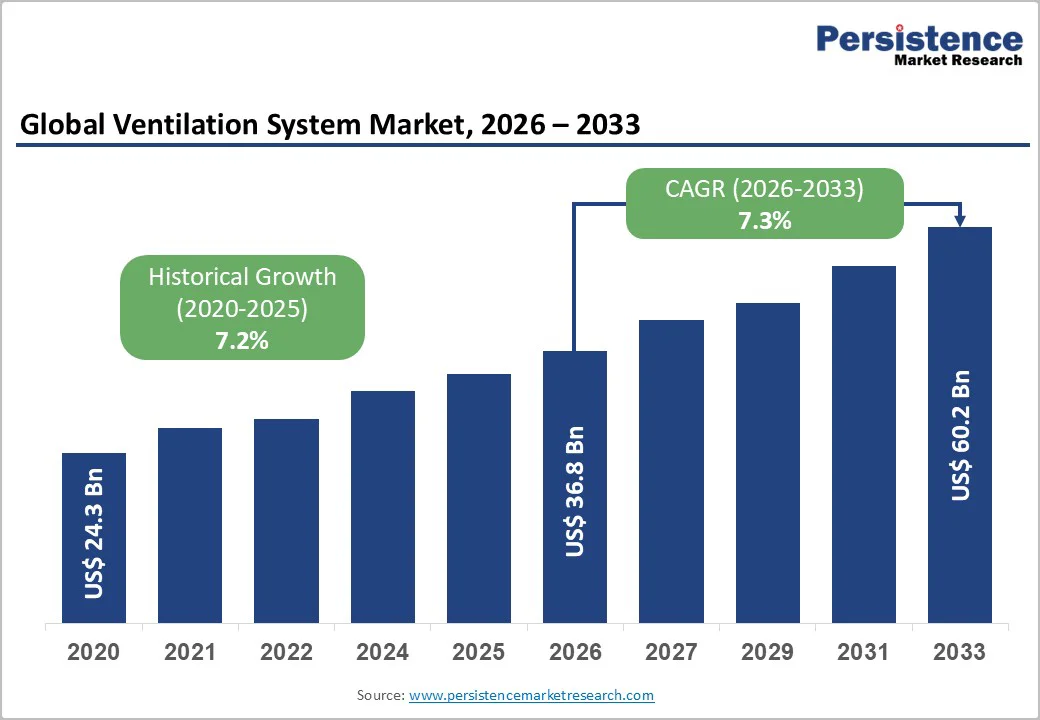

The global ventilation system market size is likely to be valued at US$36.8 Billion in 2026 and is expected to reach US$60.2 Billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033, driven by broader adoption of energy-efficient building systems, tightening indoor air quality (IAQ) regulations, and rising construction spending from the foundation of market expansion.

Demand patterns remain strongly linked to urbanization trends and the need for health-focused ventilation solutions in residential, commercial, and industrial infrastructure. The sector continues to transition toward smart, sensor-enabled systems, reinforcing its long-term growth potential.

Key Industry Highlights

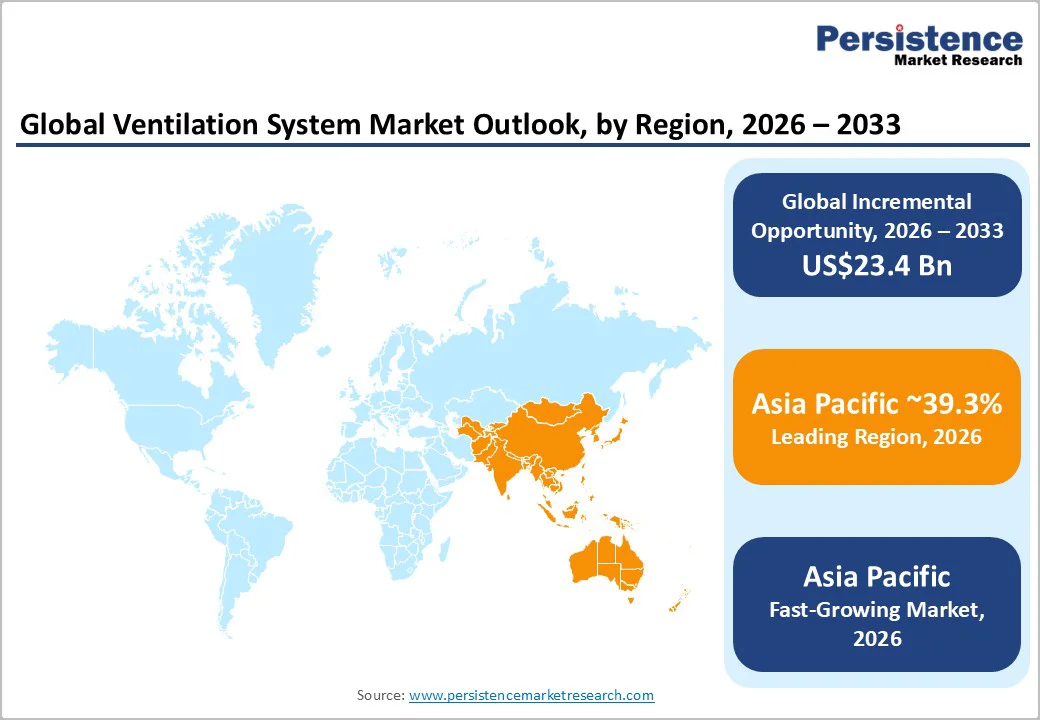

- Leading Region: Asia Pacific is anticipated to hold around 39.3% of the global ventilation systems market share, driven by large-scale construction activity, strong manufacturing capacity, and rapid urban development.

- Fastest-growing Region: Asia Pacific, led by India and ASEAN, is anticipated to record the highest regional growth rates due to housing expansion, healthcare construction, and rising IAQ standards.

- Investment Plans: Strong investment momentum in public-sector retrofits, digital IAQ platforms, and energy-recovery ventilation (ERV/HRV) upgrades, particularly in North America and Europe, as governments accelerate building-performance modernization.

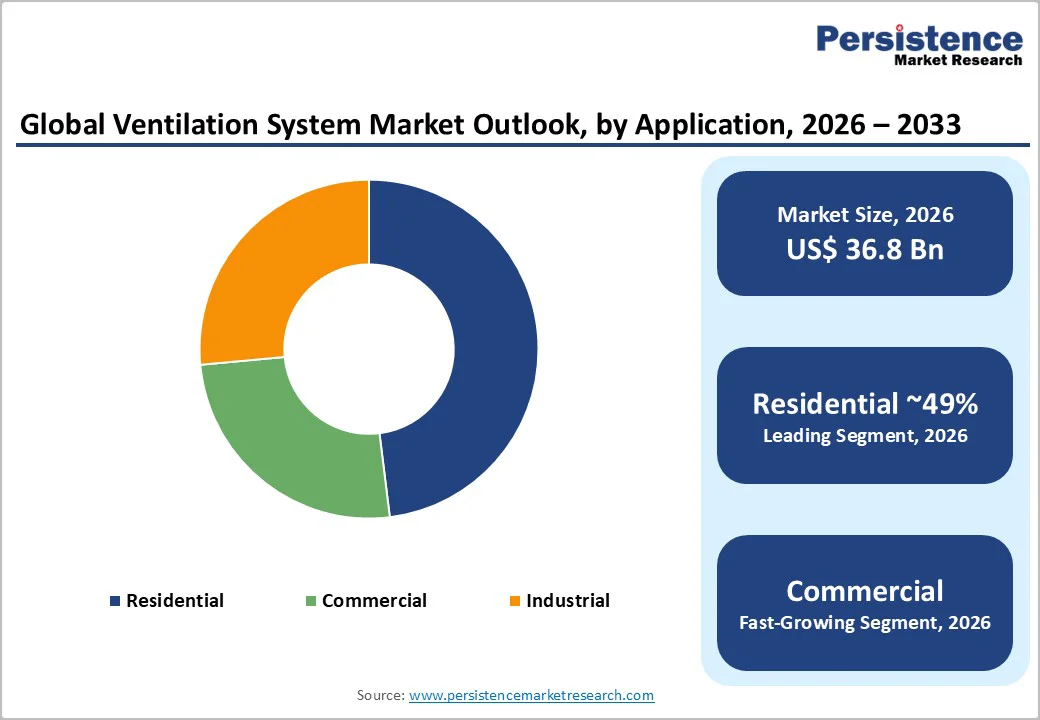

- Leading Application: Residential ventilation solutions are anticipated to account for a market share of 49% in 2026, due to regulatory obligations, complex building requirements, and increased IAQ monitoring adoption in offices, educational facilities, and public infrastructure.

- Leading System Type: Mechanical ventilation systems are anticipated to account for a market share of 63% in 2026, due to higher specification requirements, integrated controls, and dominance in commercial, healthcare, and multi-family buildings.

| Key Insights | Details |

|---|---|

| Ventilation System Market Size (2026E) | US$36.8 Bn |

| Market Value Forecast (2033F) | US$60.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Strengthening Indoor Air Quality Regulations

Regulations introduced across key economies that target pollutant reduction inside enclosed spaces are a major force shaping this market. Public health agencies and occupational safety authorities have intensified monitoring requirements for particulate matter, carbon dioxide levels, and humidity thresholds in buildings.

Industry reports show that ventilation-related compliance spending has risen steadily over the past several years. The integration of mechanical ventilation with energy recovery technologies helps buildings meet minimum ventilation rates while maintaining operational efficiency.

Expansion of Residential and Commercial Construction

Urban housing shortages and infrastructure investments form a critical demand driver. Several countries have approved major residential development programs, and commercial real estate investment has been gradually rising in metropolitan regions.

Multi-story residential complexes, mixed-use buildings, and new office structures increasingly incorporate mechanical ventilation as a core design component. Market insights indicate that ventilation installations account for a growing share of mechanical, electrical, and plumbing (MEP) budgets in new buildings. Builders are shifting toward prefabricated ventilation units that minimize on-site installation time.

Technological Advancements and Smart Ventilation

Digital integration within HVAC systems is accelerating the adoption of smart ventilation solutions. Sensor-driven systems capable of air-quality tracking, automated airflow adjustments, and real-time energy optimization are gaining prominence in commercial properties and high-performance residential buildings.

Modern systems use cloud-connected controllers that allow centralized monitoring across multiple facilities. Studies indicate a measurable reduction in energy consumption when smart ventilation is combined with energy recovery ventilators. Manufacturers are investing in improved fan technologies, variable-speed drives, and low-noise components, which enhance system efficiency and prolong equipment lifecycle.

Barrier Analysis - High Initial Installation Costs

Ventilation systems, particularly centralized and smart-enabled models, tend to involve high capital costs due to specialized components, ductwork requirements, and integration needs with other HVAC elements. Cost pressures intensify in commercial complexes where zoning, filtration, and energy recovery modules add complexity.

Retail, small businesses, and price-sensitive residential buyers often delay ventilation upgrades due to budget constraints. These financial barriers slow adoption in regions with moderate building compliance enforcement, limiting the market’s transition toward advanced systems.

Supply Chain and Skilled Labor Constraints

Manufacturers depend on a consistent supply of motors, fans, sensors, and electronic controllers. Volatility in component availability can create production delays and cost fluctuations. Skilled labor shortages in the HVAC installation and maintenance workforce also challenge market expansion.

Specialized technicians are required to install and balance ventilation systems, particularly those integrated with intelligent controls. Project timelines can extend due to limited technical expertise, which directly influences operational efficiency for contractors and end-users.

Opportunity Analysis - Growing Adoption of Energy-Efficient and Green Buildings

Sustainable construction certifications encourage the use of advanced ventilation systems that reduce energy consumption while ensuring healthy indoor environments. Energy recovery systems and demand-controlled ventilation are becoming standard features in green buildings.

Governments are offering incentives for retrofitting older structures with efficient ventilation equipment, opening a sizable refurbishment opportunity. This segment presents significant revenue potential as property owners prioritize compliance and reduced operating expenses.

Expansion across Emerging Economies

Rapid industrialization and urban development create a high demand for modern ventilation systems across emerging markets. Rising disposable income, migration to urban centers, and increased construction of retail, manufacturing, and residential facilities stimulate market growth.

These regions are adopting new IAQ policies, setting the stage for a sizable long-term adoption wave. Market estimates indicate that emerging economies could account for a considerable portion of global ventilation system installations during the forecast period.

Integration of Ventilation with Building Automation

As building management systems evolve, ventilation technologies that integrate seamlessly into automation platforms present an attractive growth pathway. System integrators and OEMs are collaborating to develop interoperable ventilation components that communicate with energy management software. These solutions improve fault detection, operational visibility, and building compliance tracking.

Category-wise Analysis

Application Insights

Residential ventilation is anticipated to be the largest segment in 2026, holding an estimated market share of 49%, due to the global scale of single-family and multi-family housing units. Mechanical ventilation requirements for tighter building envelopes, combined with broader adoption of balanced ventilation systems and whole-house ERV/HRV installations, maintain the segment’s leadership position.

In many national and regional building-ventilation analyses, the residential sector consistently appears as a dominant contributor to market value. Examples include bathroom and kitchen exhaust systems, decentralized mechanical ventilation, and whole-house systems designed to meet evolving energy and IAQ codes. High replacement frequency, standardized installation practices, and the growth of healthy-home programs further support its substantial market share.

Commercial ventilation systems are likely to represent the fastest-growing application segment, driven by modernization of HVAC assets, IAQ-driven upgrades, and smart-building adoption. Institutional and corporate facilities increasingly specify enhanced ventilation performance to meet health guidelines, improve occupant comfort, and qualify for green-building certifications such as WELL and LEED.

This segment benefits from higher average selling prices, longer service contracts, and integration with controls and monitoring systems. Growth is strongest in large metropolitan markets across the U.S., Europe, and Asia-Pacific, where commercial real estate portfolios continue upgrading ventilation performance as part of broader energy-efficiency and ESG strategies.

System Type Insights

Mechanical ventilation systems, including centralized AHUs, ducted systems, and decentralized mechanical units, are anticipated to hold 63% of the share in 2026, due to their engineering complexity, integration with HVAC systems, and key role in achieving measurable IAQ and energy-recovery performance.

Mechanical systems dominate spending within commercial, healthcare, and multifamily projects, where performance documentation and compliance with ventilation codes are critical. These systems command higher unit prices and generate recurring service revenue. Their prominence reflects the industry’s shift toward data-driven ventilation design and the need for reliable, controlled airflow in buildings with limited natural ventilation conditions.

Hybrid ventilation systems, combining natural airflow strategies with sensor-activated mechanical support, are growing rapidly as building owners aim to balance energy savings with comfort and compliance. Demand-controlled ventilation (DCV), which uses occupancy, CO2, or VOC sensors to modulate outdoor air intake, reduces energy use while meeting IAQ benchmarks.

DCV adoption is accelerating in new commercial construction and retrofit projects, particularly where full mechanical redesign is cost-prohibitive. The expansion of building-performance metrics and carbon-reduction targets further strengthens DCV’s position as one of the most compelling growth opportunities within system types.

Regional Insights

North America Ventilation System Market Trends - IAQ-Driven Upgrades and Code-Linked High-Efficiency Adoption

North America is a key market for ventilation systems, driven by a large commercial building base, ongoing infrastructure upgrades, and increasing adoption of indoor air quality (IAQ) technologies. The U.S. holds the largest regional revenue share, fueled by strict state and federal energy codes, frequent HVAC upgrades, and advanced system integration.

Demand is growing for energy recovery and heat recovery ventilators, IAQ monitoring platforms, and high-efficiency mechanical ventilation in schools, healthcare facilities, offices, and public buildings. Policies such as California’s Title 24, federal retrofit programs, and corporate sustainability initiatives further support market expansion.

A strong domestic manufacturing base, well-established distribution networks, and extensive service capabilities shorten lead times and ensure reliable aftermarket support, reinforcing the region’s operational foundation.

Ventilation system suppliers are increasingly integrating digital controls and energy-efficient technologies to meet evolving demand, while professional training and certification programs promote correct system design, installation, and commissioning.

Key growth drivers include tightening ventilation and energy codes that mandate measurable performance outcomes, rising public-sector investment in educational and healthcare retrofits, and government incentives for energy-recovery equipment and electrification strategies.

Vertical integration strategies combining equipment, monitoring platforms, and long-term service agreements are becoming central to market strategy, enabling suppliers to deliver end-to-end solutions and capture additional revenue streams.

Europe Ventilation System Market Trends - Regulation-Led Energy Recovery and Advanced Renovation Demand

Europe remains a high-value market for ventilation systems, driven by stringent energy-performance mandates, advanced building regulations, and national climate-action initiatives. Germany and the U.K. lead in high-specification ventilation design and installation, while France and Spain contribute through robust renovation activity and steady new-build volumes.

Region-wide directives focused on energy efficiency and decarbonization are supporting long-term demand for energy-recovery systems, air handling units, and advanced control architectures. Recent updates to European building-performance regulations are accelerating renovation cycles and expanding efficiency obligations, strengthening opportunities in residential, commercial, and institutional ventilation upgrades.

Market growth in Europe is fueled by performance requirements, accelerated renovation mandates, and increasing adoption of green-building certifications such as WELL and BREEAM. The ongoing transition toward electrification and low-GWP refrigerant technologies is reshaping integrated HVAC and ventilation designs.

Manufacturers are developing more efficient, regulation-compliant product portfolios to meet rising demand for sustainable and high-performance systems.

Investment opportunities are expanding in energy-recovery solutions for multi-family residential buildings, large-scale commercial retrofits, and sensor-enabled demand-controlled ventilation. Companies are responding with innovative product platforms, digital integration, and strategic partnerships to address evolving regulations and energy-recovery requirements.

These initiatives reinforce Europe’s position as a market focused on efficiency, sustainability, and advanced ventilation technologies.

Asia Pacific Ventilation System Market Trends - Construction-Led Expansion with Cost-Competitive Manufacturing

Asia Pacific is anticipated to represent the largest regional market by overall value, accounting for an estimated 39.3% share in 2026, supported by extensive new-construction activity, rapid urbanization, strong infrastructure investment, and a significant manufacturing base for ventilation components and complete systems.

Country-level performance varies significantly. China dominates in installation volume, driven by industrial ventilation needs and large commercial building deployments.

Japan remains the regional benchmark for product quality and technological innovation, supported by well-established standards for IAQ and building performance. India and the ASEAN countries exhibit some of the fastest growth rates due to rising urban populations, expansion of residential and commercial construction, increasing healthcare infrastructure, and growing policy attention toward air quality in metropolitan areas.

Key factors driving growth in the region include large and expanding construction pipelines, government policies supporting healthier buildings, and strong public-sector investment in urban infrastructure.

The availability of cost-effective local production enables companies to position products more aggressively, enhancing competitiveness and expanding accessibility in price-sensitive markets. Regulatory adoption varies across APAC, but several economies are gradually introducing energy-efficiency and IAQ standards that are expected to strengthen long-term demand for high-performance ventilation systems.

Competitive Landscape

The global ventilation system market comprises major OEMs, regional manufacturers, and a wide network of installers and distributors. Equipment-level concentration is moderate, with multinational firms dominating premium segments, while distribution and installation remain fragmented due to regional code differences.

Competitive edge relies on energy efficiency, advanced controls, digital monitoring, and lifecycle services. Asia Pacific leads in volume, with North America and Europe commanding higher prices. Key players focus on energy-recovery systems, digital integration, low-GWP equipment, localized support, compliance, bundled service offerings, and emerging subscription-based IAQ analytics as a new revenue stream.

Key Industry Developments

- In May 2025, Daikin Industries, Ltd. launched a new high-efficiency air-handling unit designed for large office buildings, expanding its centralized ventilation product line and reinforcing its commercial-building offering.

- In February 2024, Carrier initiated a joint-venture R&D and manufacturing facility targeting advanced HVAC and air-handling solutions, signaling its strategic push into high-volume ventilation production for emerging markets.

Companies Covered in Ventilation System Market

- Daikin Industries, Ltd.

- Carrier Global Corporation

- Johnson Controls International plc

- Panasonic Holdings Corporation

- Mitsubishi Electric Corporation

- Honeywell International Inc.

- Midea Group Co., Ltd.

- Greenheck Fan Corporation

- LG Electronics

- Twin City Fan & Blower / Nortek Air Solutions

- Zehnder Group

- Halton Group

- CaptiveAire Systems

- Soler & Palau (S&P)

- Trane Technologies

- Emerson Electric Co.

- Nortek Global HVAC

- Systemair AB

- Vent-Axia

- FläktGroup

Frequently Asked Questions

The global ventilation system market is estimated to reach US$36.8 Billion in 2026.

By 2033, the ventilation system market is projected to grow to US$60.2 Billion.

Key trends include widespread adoption of energy-recovery and high-efficiency ventilators, integration of IoT-based IAQ monitoring and controls, growing demand for mechanical and hybrid ventilation systems, and increasing focus on sustainable and energy-efficient solutions.

The commercial ventilation segment leads the market by value, driven by regulatory compliance, high-spec installations, and adoption of advanced IAQ solutions in offices, educational facilities, healthcare, and public buildings.

The market is expected to grow at a CAGR of 7.3% between 2026 and 2033.

Major players include Daikin Industries, Ltd., Carrier Global Corporation, Johnson Controls International plc, Panasonic Holdings Corporation, and Mitsubishi Electric Corporation.