- Home Care & Utilities

- Pest Control Products and Services Market

Pest Control Products and Services Market Size, Share, and Growth Forecast 2026 - 2033

Pest Control Products and Services Market Services (Services, Products), Application (Insect Control, Rodent Control, Wildlife Control, Other Applications), End User (Residential, Commercial, Agricultural), and Regional Analysis 2026 - 2033

Pest Control Products and Services Market Size and Trend Analysis

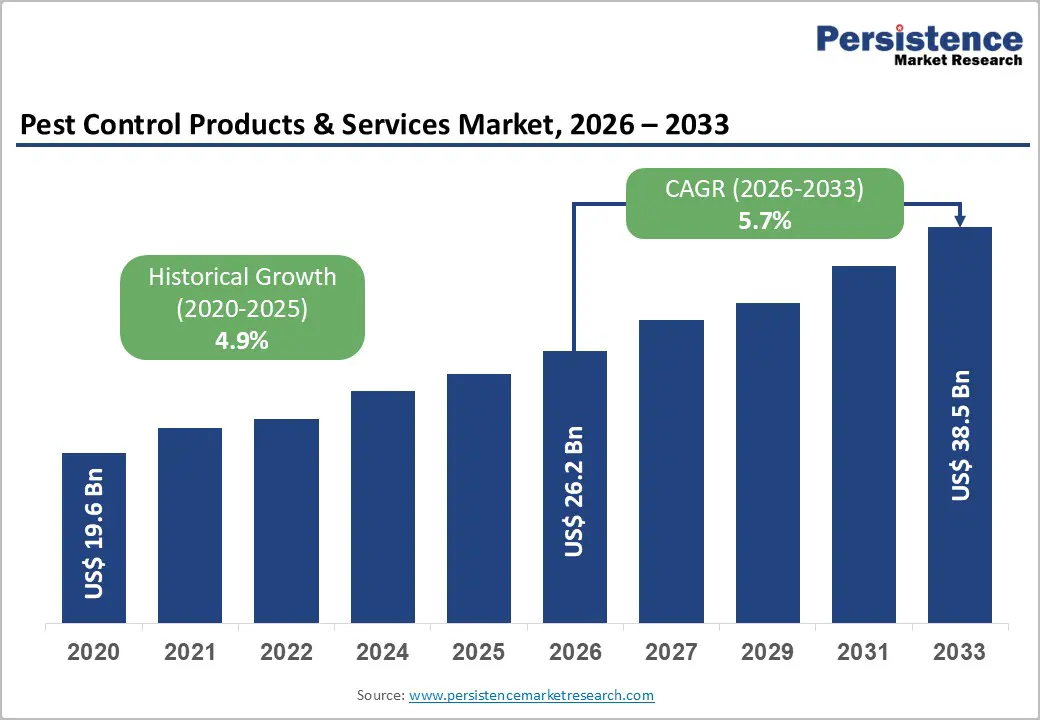

The global Pest Control Products and Services Market is projected to reach US$ 26.2 Billion in 2026 and is anticipated to grow to US$ 38.5 Billion by 2033, expanding at a CAGR of 5.7% between 2026 and 2033. Accelerating urbanization and densifying populations across developed and emerging markets are intensifying pest infestation pressures, driving substantial demand for professional pest management solutions.

Rising public health consciousness surrounding vector-borne diseases, including dengue and Lyme disease, alongside stringent regulatory frameworks mandating sanitation standards, fundamentally strengthens market expansion. Technological integration through IoT-enabled monitoring systems and biological control innovations represents a critical competitive differentiator, reshaping the industry landscape toward sustainable, effective pest management methodologies.

Key Market Highlights

- Services dominance continues with 62% market share while Products category accelerates expansion at 5% CAGR, demonstrating industry transition toward technology-integrated and sustainable pest management solutions addressing regulatory transformation requirements.

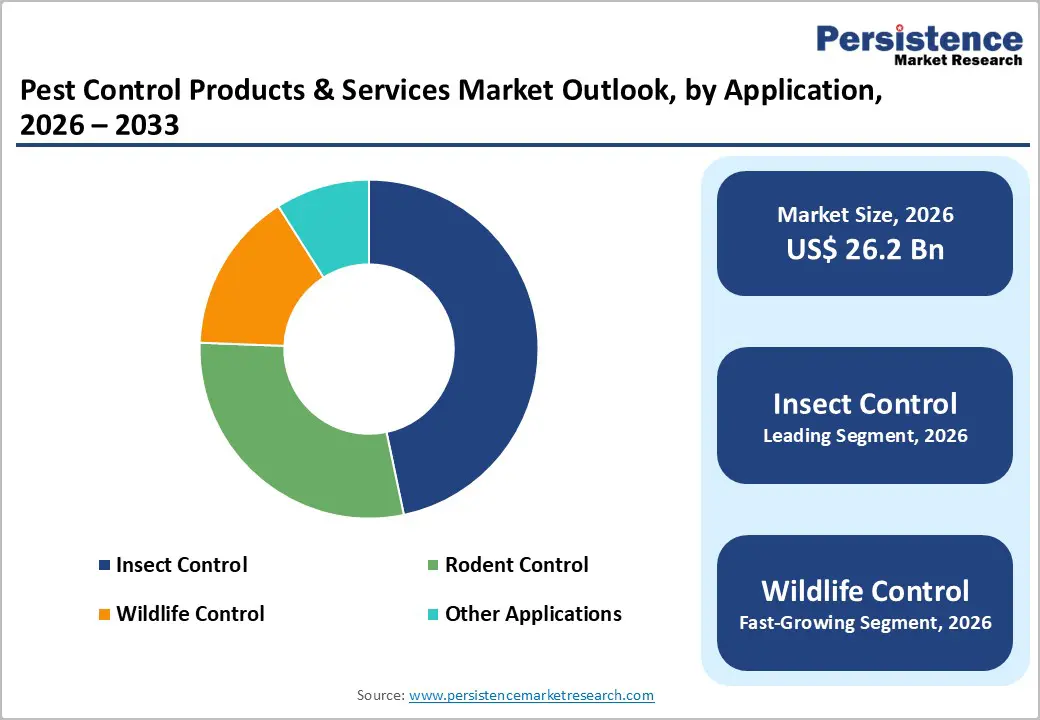

- Insect Control maintains market leadership with 47% share; Wildlife Control emerges as fastest-growing application segment at 6.9% CAGR, reflecting suburban sprawl and humanized wildlife removal preference shifts among residential consumers.

- Residential sector commands 40% end-user share with predictable subscription revenue models; Commercial applications expand at 5.7% CAGR driven by regulatory compliance imperatives, establishing differentiated growth trajectories across consumer segments.

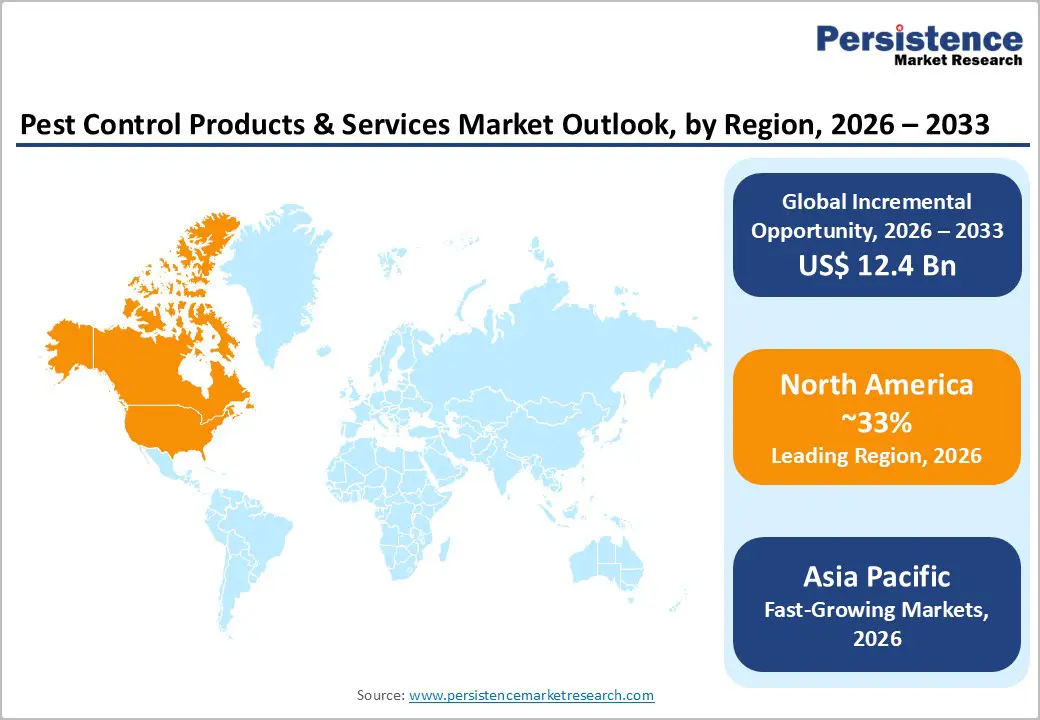

- North America retains 32% global market share with mature consolidation dynamics; Asia Pacific emerges as highest-growth region at 6.3% CAGR, presenting substantial market expansion opportunities concentrated in developing agricultural and commercial infrastructure segments.

- Strategic consolidation accelerates with 27.6% M&A volume increases and technology integration emerging as critical competitive differentiator, positioning market leaders leveraging AI-enabled monitoring, biopesticide portfolios, and integrated facility management capabilities.

| Key Insights | Details |

|---|---|

|

Pest Control Products & Services Market Size (2026E) |

US$ 26.2 billion |

|

Market Value Forecast (2033F) |

US$ 38.5 billion |

|

Projected Growth CAGR (2026-2033) |

5.7% |

|

Historical Market Growth (2020-2025) |

4.9% |

Market Dynamics Analysis

Market Drivers

Heightened Public Health Awareness and Disease Prevention Imperatives

Vector-borne disease transmission vectors have catalyzed fundamental consumer behavior shifts toward proactive pest prevention. Dengue fever incidence has increased 30-fold over five decades, affecting approximately 390 million individuals annually, while Lyme disease diagnoses exceeded 480,000 cases cumulatively in North America alone. Post-pandemic health consciousness has elevated hygiene standards across hospitality, healthcare, and food service industries. US commercial food facilities allocate US$15.2 billion annually for pest prevention infrastructure and services, representing mandatory operational expenditures rather than discretionary spending. Residential consumers increasingly recognize pest infestation's connection to respiratory allergies, asthma exacerbation, and contamination transmission, driving significant service adoption among health-conscious households earning above US$75,000 annually.

Stringent Regulatory Frameworks and Compliance Requirements

Governmental regulatory structures enforce increasingly rigorous pest control standards across jurisdictions. The EPA's expanded pesticide oversight regulations, combined with FIFRA compliance mandates, establish non-negotiable compliance thresholds for commercial pest management providers. European Union's Sustainable Use Directive restricts 41 active pesticide ingredients, compelling industry innovation toward biological and mechanical control methodologies. USDA agricultural sector regulations require documented pest management protocols across 895 million cultivated acres, establishing integrated pest management (IPM) adoption as mandatory farming practice. Regulatory-driven compliance costs represent 12-18% of total pest control service expenditures, creating substantial barriers to market entry while protecting established providers' competitive positioning and service value propositions.

Market Restraints

Chemical Pesticide Regulatory Restrictions and Phase-Out Mechanisms

Accelerating restrictions on conventional chemical pesticide formulations represent structural market headwinds affecting product manufacturers and service providers. The EPA's discontinuation of 52 pesticide active ingredients over the past decade has eliminated traditional control methodologies, requiring expensive reformulation investments. Substitute biological control products command 35-45% price premiums relative to conventional chemicals, reducing accessibility for price-sensitive residential and smallholder agricultural consumers. Supply chain disruptions affecting biopesticide production facilities have extended product lead times by 8-12 weeks, constraining market responsiveness and competitive service delivery timelines.

Fragmented Market Structure and Intense Price-Based Competition

The pest control market's extreme fragmentation characterized by 48,000+ independent operators across North America alone, creates relentless price-compression dynamics undermining service quality and profitability. Regional consolidators and multinational enterprises leverage scale advantages, undercutting independent operators by 15-25% on comparable service offerings. This competitive intensity constrains margins, limiting technology adoption investments and workforce skill development. Recurring revenue dependencies create customer churn risks when price-based competitors capture established client relationships.

Market Opportunities

Biological Control and Sustainable Pest Management Solutions

Biological pest control methodologies utilizing natural predators, parasites, and microbial agents represent high-growth market segments expanding at 7.2% CAGR through 2033. Regulatory tailwinds favoring chemical elimination, combined with consumer willingness to pay 20-30% premiums for eco-friendly solutions, establish substantial monetization potential. Residential consumers increasingly adopt predatory insect introductions, nematode applications, and botanical extract formulations, representing accessible market segments for specialized service providers and product manufacturers.

Smart Pest Management Technology Integration

IoT-enabled monitoring systems, AI-powered infestation detection algorithms, and real-time pest activity dashboards represent emerging technology convergences reshaping service delivery models. Smart trap technologies utilizing electronic sensors and cloud-based reporting infrastructure enable predictive pest prevention rather than reactive response modalities. Commercial property managers operating 15+ facility portfolios demonstrate 34% service adoption rate increases when deployed with integrated monitoring platforms. The smart pest management technology segment representing substantial monetization opportunities for software developers, hardware manufacturers, and technology-enabled service providers.

Segmentation Analysis

Offering Analysis

Services constitute the dominant offering category, commanding 62% global market share with valuation reaching approximately US$16.2 billion in 2026. Chemical control services represent the largest subcategory, leveraging extensive provider networks and strong customer familiarity with conventional pest elimination methods. Commercial applications drive demand, with food processing, hospitality, and healthcare facilities accounting for nearly 68% of professional service revenues, while mechanical and specialized services address complex infestations requiring technical expertise and advanced equipment deployment and regulatory compliance requirements globally across markets.

Product offerings, though secondary, are expanding at a faster 5% CAGR. Insecticides dominate products with 41% share, followed by rodenticides addressing persistent infestations. Mechanical products, including electronic traps and monitoring devices, grow at 6.2% CAGR, while biological and botanical formulations gain traction amid sustainability-focused regulations and evolving consumer preference shifts.

Application Analysis

Insect control applications dominate the market landscape, commanding 47% global share with valuation exceeding US$12.3 billion in 2026. Mosquitoes, cockroaches, termites, and bed bugs drive primary service and product demand globally. Vector-borne disease concerns, including dengue transmission and Zika prevention, elevate spending across residential and municipal segments. Seasonal pest activity patterns, peaking during spring and summer months, create predictable revenue cycles, workforce planning requirements, and capacity utilization challenges for professional pest control providers across developed and emerging regional markets globally.

Wildlife control applications are expanding at 6.9% CAGR, driven by suburban sprawl encroaching on natural habitats and rising human wildlife interactions. Raccoon, squirrel, and bat removal generate premium margins, while humane, regulation mandated practices require specialized expertise and equipment, limiting competitive entry and favoring certified wildlife service providers globally increasingly.

End User Analysis

Residential consumers represent the largest end user category, commanding 40% market share with approximately US$10.4 billion projected valuation in 2026. Single family residential pest control service adoption exceeds 45% in developed markets, reflecting strong familiarity with professional solutions. Subscription based recurring models generate predictable revenues, with average customer lifetime values exceeding US$8,000 across five year relationships. Documented infestations trigger rapid response, with 72% of affected households engaging professional services within thirty days after initial pest detection and inspection processes globally.

Commercial applications expand at 5.7% CAGR due to regulatory compliance across hospitality, healthcare, and food services. Agricultural intensification in developing economies drives demand. India’s sector employs 58% workforce across 169 million hectares. Farmers spend US$12.8 billion annually, while precision agriculture and climate driven pest pressures support 6.4% CAGR growth globally.

Regional Market Insights

North America

North America maintains commanding 32% global market share, with regional valuation reaching approximately US$8.4 billion in 2026. The United States dominates regional dynamics, accounting for nearly 87% of revenues, supported by mature residential and commercial service penetration exceeding 62% and 71% respectively. EPA regulatory frameworks and state level pesticide restrictions in California and New York are accelerating transition toward sustainable control methods. Major providers including Rollins Inc., Terminix Global Holdings, and Rentokil Initial collectively command roughly 28% share, while technology adoption drives competition, with operators investing 8–12% of service revenues.

North America’s mature market is characterized by accelerating consolidation, with M&A volumes rising 27.6% year over year during 2024. Sponsor backed buyers pursue roll up strategies targeting regional operators at 8–12x EBITDA multiples, while real estate activity, aging homeowners, and higher indoor time sustain residential demand growth despite macroeconomic uncertainty.

Europe Regional

Europe represents the second largest regional market, accounting for approximately 24% global market share with valuation reaching US$6.3 billion in 2026 and expanding to US$8.1 billion by 2033. Germany, United Kingdom, and France collectively contribute 58% of regional revenues, supported by stringent sanitation regulations, food safety mandates, and established professional service infrastructure. The EU Sustainable Use Directive restricts synthetic pesticide applications across numerous active ingredients, accelerating adoption of biological control methods and integrated pest management, while market maturity moderates growth to 4.9% CAGR and elevates research investment requirements across Europe.

European market dynamics prioritize service quality and regulatory compliance over price competition. Premium pricing reflects elevated standards, certifications, and environmental responsibility commitments. Commercial property management shows 34% professional service adoption, while residential adoption remains limited at 28%, constrained by higher costs and reliance on do it yourself pest control solutions.

Asia Pacific Regional Analysis

Asia Pacific represents the highest growth regional market, expanding at 6.3% CAGR with valuation reaching US$4.2 billion in 2026 and projected to US$6.5 billion by 2033. China and India contribute 64% of regional revenues, driven by rapid urbanization and rising food safety awareness across commercial sectors. China’s market accelerates at 8.6% CAGR, supported by commercial property expansion and real estate development generating US$140 billion annually. India’s residential penetration remains low at 12%, creating significant expansion potential as middle class growth and health awareness increase. Japan shows mature residential commercial adoption.

Regional dynamics emphasize service accessibility expansion through mobile platforms and localized networks. Manufacturing sector demand, led by food processing and pharmaceuticals, accounts for 41% of commercial revenues. Agricultural opportunities strengthen as precision agriculture adoption accelerates across China, India, and Southeast Asia facing intensifying crop production pressures and rising climate volatility.

Competitive Landscape

Strategic Developments

- In March 2024, BASF's regional product expansion introducing 12 novel microbial and botanical-based formulations targets expanding agricultural and residential markets across China and India. Regional pricing strategies emphasizing 18-22% cost reductions relative to synthetic alternatives optimize market accessibility for price-sensitive smallholder farmers.

Business Strategies

Market leaders emphasize innovation-driven competitive differentiation through technology integration, cost structure optimization, and geographic footprint expansion. Dominant strategic themes prioritize recurring revenue model development, leveraging subscription-based service architectures generating predictable cash flows and elevated customer lifetime values. Key differentiators include integrated pest management expertise, specialized wildlife removal capabilities, and biopesticide product portfolios addressing regulatory transition requirements. Emerging business model trends emphasize franchise system expansion among regional consolidators, franchisee network leveraging to accelerate geographic penetration with capital-efficient deployment mechanisms.

Companies Covered in Pest Control Products and Services Market

- Autoliv Inc.

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- Magna International

- Aptiv PLC

- Hyundai Mobis

- Thyssenkrupp

- Brose Fahrzeugteile

- GESTAMP

- ArcelorMittal

- Novellus

- Continental AG

- Taiga Motors

- Tianjin Lishen Battery

Frequently Asked Questions

The global Pest Control Products and Services Market is projected at US$ 26.2 Billion in 2026, expanding to US$ 38.5 Billion by 2033, reflecting substantial market scale supporting diverse provider ecosystems and emerging technology integration opportunities.

Urbanization intensification, vector-borne disease prevention imperatives, and stringent regulatory compliance requirements represent primary market drivers, collectively generating 68% of market expansion momentum across residential, commercial, and agricultural applications.

The market is anticipated to expand at 5.7% CAGR between 2026 and 2033.

Biological control adoption, smart pest management technology integration, and precision-driven agricultural pest solutions represent the most compelling monetization opportunities, as sustainability mandates, digital monitoring, and yield optimization increasingly reshape demand across residential, commercial, and agricultural pest management ecosystems.

Market leadership is concentrated among consolidated operators including Rollins Inc., Rentokil Initial, Terminix Global Holdings, Ecolab Inc., FMC Corporation, and BASF SE, collectively commanding approximately 30-34% global market share through integrated service platforms and product portfolios.