- Medical Devices

- Medical Warming Cabinets Market

Medical Warming Cabinets Market Size, Share, and Growth Forecast, 2026 – 2033

Medical Warming Cabinets by Product Type (Single Cavity, Multiple Cavity), Installation Format (Built-In, Countertop, Floor-Standing, Others), End-Use (Hospitals, Ambulatory Surgical Centers (ASCs), Clinics, Diagnostic Centers, Others), and Regional Analysis for 2026-2033

Medical Warming Cabinets Market Share and Trends Analysis

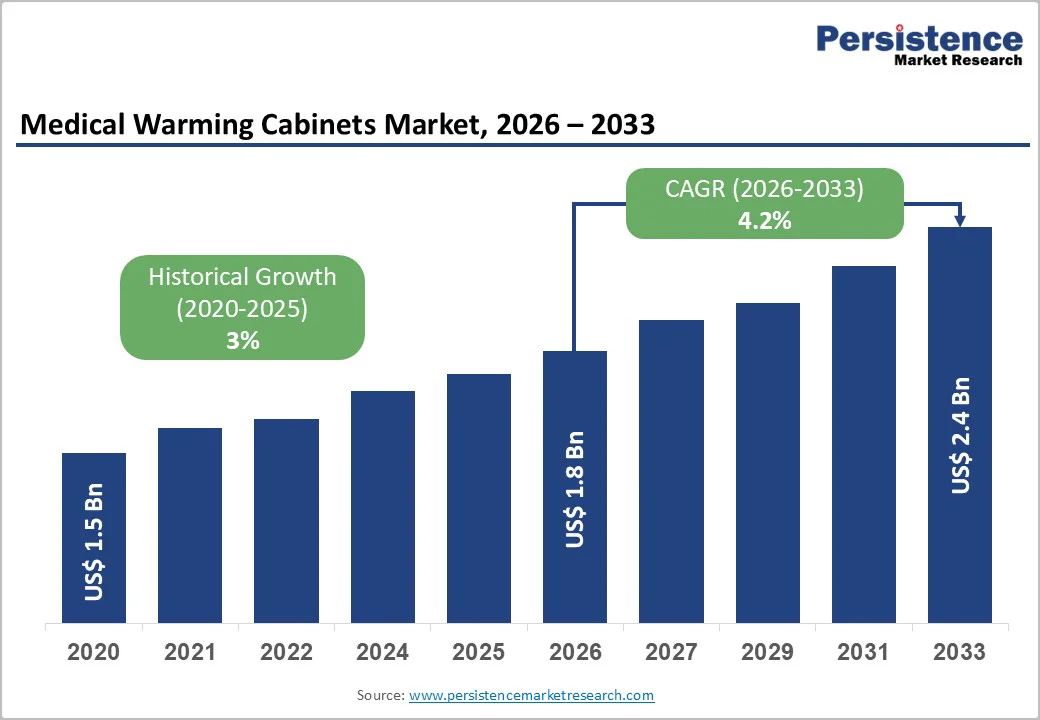

The global medical warming cabinets market size is likely to be valued at US$ 1.8 billion in 2026 and is projected to reach US$ 2.4 billion by 2033, growing at a CAGR of 4.2% during the forecast period 2026 - 2033. Investment in temperature-controlled storage solutions remains tightly linked to expanding surgical volumes, stringent infection prevention protocols, and the rising Imperative for patient safety in perioperative care. The growth is underpinned by healthcare infrastructure expansion, especially in emerging regions with rising surgical procedures and diagnostic activities. Regulatory compliance and technological innovation further reinforce demand across clinical end-use settings

Key Industry Highlights

- Dominant Product Type: Single-cavity warmers are anticipated to account for 55% of the revenue share in 2026, supported by their wide suitability for routine warming needs in hospitals and clinics.

- Rapidly Advancing Product Type: Multiple-cavity units are projected to expand at a 6.2% CAGR through 2033, driven by their rising adoption in high-volume surgical and emergency settings.

- Leading Installation Format: Floor-standing models are expected to command 48% of the revenue share in 2026, owing to their high-volume storage capacity and alignment with operational requirements.

- Fastest-growing Installation Format: Countertop units are set to grow at a 6.8% CAGR through 2033, supported by the increasing point-of-care usage across specialty centers, diagnostic units, and decentralized care facilities.

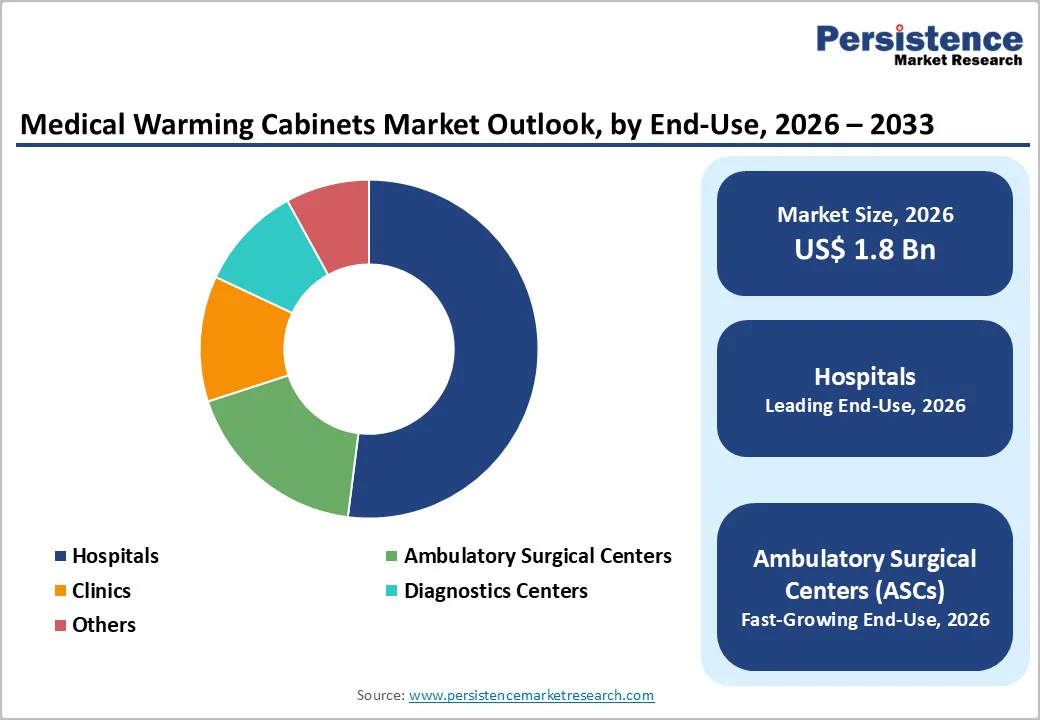

- Dominant End-User: Hospitals are projected to capture 52% of the end-use share in 2026, reflecting stringent perioperative warming protocols.

- Accelerating End-User: Ambulatory surgical centers (ASCs) are expected to record about 7.1% CAGR through 2033, driven by the shift toward outpatient procedures.

- Technology & Innovation Trend: IoT-enabled cabinets, energy efficiency, and digital monitoring drive product differentiation as healthcare facilities increasingly prioritize smart systems that support compliance, reduce operational burden, and enhance temperature accuracy.

| Key Insights | Details |

|---|---|

| Medical Warming Cabinets Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 2.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Surgical Demand, Infrastructure Growth, and Smart Technology Integration

The increasing volume of global surgical procedures, driven by aging populations and wider access to healthcare services, is strengthening the need for reliable temperature-controlled storage across clinical environments. Medical warming cabinets play a critical role in maintaining optimal temperatures for IV fluids, blankets, and surgical solutions, reducing perioperative risks and supporting compliance with safety standards. Simultaneously, rapid healthcare infrastructure development in emerging economies, particularly across Asia Pacific, is leading to the establishment of new hospitals, diagnostic centers, and outpatient facilities, each requiring modern warming systems to meet evolving infection-control and clinical-workflow requirements.

Advancements in digital connectivity, automation, and AI-driven technologies are also reshaping product expectations. In early 2025, for example, CAS and Cleveland Clinic formed a strategic alliance to accelerate clinical research by combining CAS's extensive scientific data with Cleveland Clinic's biomedical expertise and IBM Quantum System One computing power. The clinic’s AI-powered hypertension management system unveiled further illustrates the integration of predictive analytics and real-time monitoring in patient care. Together, these developments highlight the rising importance of IoT-enabled, automated, and data-driven warming solutions, supporting precision, operational efficiency, and timely equipment replacement, while reinforcing adoption across high-volume hospitals and mid-sized facilities globally.

Interoperability Gaps and Operational Integration Challenges

Despite steady technological advancement, medical warming cabinets often face integration challenges within increasingly digital healthcare environments. Many facilities operate a mix of legacy infrastructure and newer smart systems, making seamless connectivity with hospital information systems, asset tracking platforms, and centralized monitoring dashboards difficult. Limited interoperability can prevent real-time visibility of cabinet status, temperature compliance, and usage patterns, reducing the operational value of advanced features and slowing digital adoption, particularly in multi-site hospital networks.

In addition, clinical workflow alignment remains a practical challenge. Warming cabinets are used across operating rooms, ICUs, emergency departments, and outpatient settings, each with distinct usage patterns and staff responsibilities. Variability in placement, access protocols, and staff training can lead to inconsistent utilization and suboptimal performance. Facilities may hesitate to deploy advanced models if workflow disruptions, retraining requirements, or perceived complexity outweigh immediate efficiency gains. These integration and adoption hurdles can moderate upgrade cycles and limit the full realization of smart warming cabinet capabilities, even in well-funded healthcare systems.

Expansion of Outpatient Care, Portable Solutions, and Specialized Diagnostic Facilities

The accelerated shift toward outpatient care is creating strong demand for warming cabinets that suit the operational needs of ambulatory surgical centers and day-care facilities. These settings prioritize compact, efficient, and cost-effective units that support perioperative workflows without requiring large installation footprints. As outpatient procedures rise across developed healthcare systems, the need for reliable temperature-controlled storage becomes a critical procurement priority, strengthening adoption beyond traditional hospital environments and broadening the overall customer base.

At the same time, the market is benefiting from increasing interest in portable and modular warming solutions that address the needs of clinics, diagnostic centers, and emerging care models where mobility and space efficiency are essential. Growing numbers of diagnostic and specialty centers treating chronic and high-acuity conditions further expand the opportunity landscape, as these facilities rely on consistent warming capabilities for sensitive supplies. As a result, the opportune convergence of outpatient growth, portable system demand, and expanding diagnostic capacity creates new revenue pathways and encourages manufacturers to diversify product formats to capture wider market penetration

Category-wise Analysis

Product Type Insights

Single cavity cabinets are anticipated to dominate the product type segment with a 55% market share in 2026, driven by their widespread adoption in hospitals. Their simple design, ease of operation, and suitability for routine warming of blankets and fluids make them ideal for operating rooms, ICUs, and emergency departments. Facilities value these units for consistent performance, lower maintenance, and cost-effectiveness, ensuring reliable availability of temperature-sensitive items across clinical workflows.

Multiple cavity cabinets are projected to be the fastest-growing segment with a 6.5% CAGR through 2033, as they allow independent temperature control for different items within the same unit. Their multi-load capability meets rising demand in high-volume hospitals, ambulatory surgical centers, and specialty facilities. Growing procedural volumes, outpatient care expansion, and the need for advanced, high-throughput warming solutions further drive adoption in facilities seeking operational efficiency and versatile functionality.

Installation Format Insights

Floor-standing cabinets are projected to retain the largest market share at 48% in 2026 due to their exceptional capacity and durability. Large-scale healthcare institutions utilize these units as the primary infrastructure for high-volume environments such as operating rooms (ORs) and central sterile services departments (CSSDs). Medical teams rely on these robust systems to maintain precise thermal control for blankets, intravenous fluids, and irrigation solutions. By centralizing bulk storage, hospitals can effectively manage complex surgical schedules and ensure immediate availability of critical supplies. This reliability makes floor-standing models the standard choice for facilities that must support simultaneous procedures without logistical interruptions.

Countertop models are forecast to advance at a CAGR of 6.8% through 2033 as the healthcare landscape shifts toward decentralized care. ASCs and specialty clinics drive this expansion by seeking equipment that fits within limited architectural footprints. These compact units allow facility planners to install essential warming technology directly at the point of care without occupying valuable floor space. Modular designs enable staff to maintain operational efficiency while treating patients in smaller or remote departments. Consequently, decision-makers view these flexible solutions as a strategic investment to enhance patient comfort across a diverse range of treatment settings.

End-Use Insights

Hospitals are projected to remain the dominant end-use segment with a 52% of the medical warming cabinets market revenue share in 2026, supported by high surgical volumes, stringent perioperative workflows, and strict patient safety standards. Warming cabinets in operating rooms, ICUs, and emergency departments ensure temperature-sensitive items are readily available, helping maintain compliance and reduce perioperative risks. Hospitals rely on these systems to streamline operations and deliver consistent clinical outcomes. For example, Mayo Clinic in Rochester was recognized by Newsweek in late 2025 as the No. 1 Smart Hospital globally for 2026, highlighting leadership in AI, digital imaging, robotics, and telemedicine. Meanwhile, in November 2025, it launched Platform_Insights, providing healthcare organizations worldwide access to data-driven clinical insights, reinforcing the role of digital and smart solutions in operational efficiency.

Ambulatory surgical centers are expected to register the fastest growth with a 7.1% CAGR through 2033, fueled by the global expansion of outpatient procedures and diagnostic services outside traditional hospitals. Their flexible equipment requirements, smaller footprint, and cost-efficient designs make them ideal for adoption. Increasing surgical throughput and patient preference for outpatient care further enhance market potential, offering manufacturers an opportunity to diversify installations beyond hospital-centric settings.

Regional Insights

North America Medical Warming Cabinets Market Trends

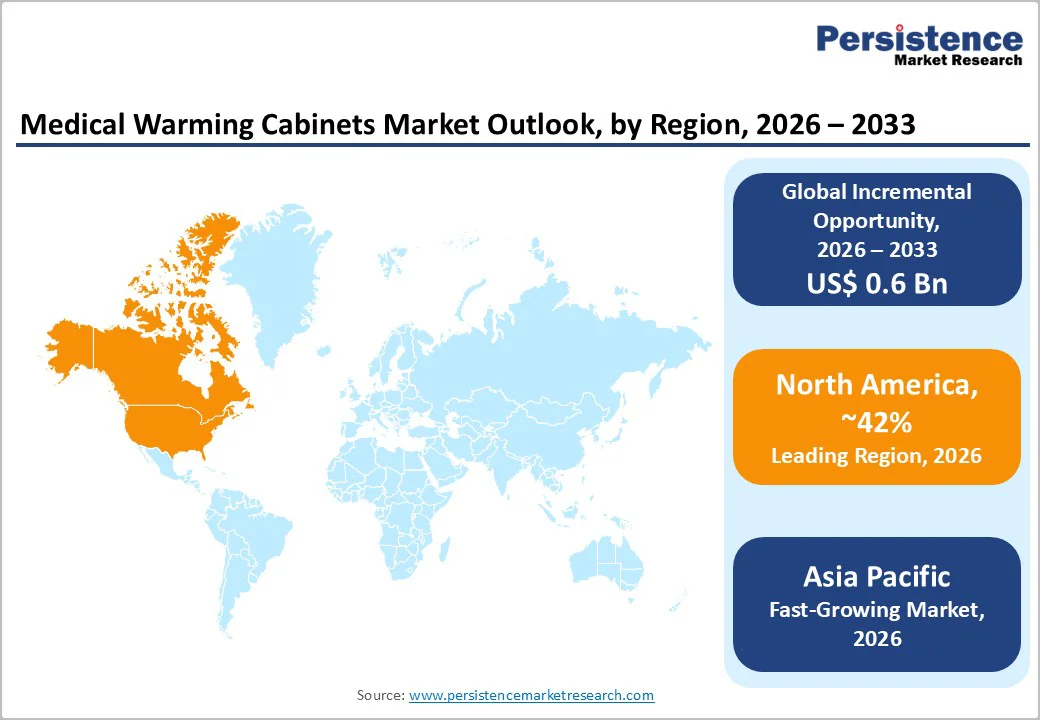

North America is poised to capture approximately 42% of the medical warming cabinets market share in 2026. This dominant position relies on sophisticated healthcare infrastructure and substantial procedural volumes across the region. The United States anchors this demand as hospitals and surgical centers prioritize compliance-oriented solutions for patient safety. Clinical teams require precise temperature management systems to enhance preoperative and postoperative care protocols. Canada complements this activity through continuous hospital expansion efforts and increasing surgical workloads. Furthermore, the rapid integration of digital temperature monitoring and energy-efficient technologies strengthens regional market leadership. Stakeholders are increasingly selecting advanced units that align with modern operational standards to ensure consistent clinical outcomes.

Demographic shifts such as an aging population and rising elective surgery rates are generating consistent capital equipment requirements. Stringent regulatory mandates regarding infection control and device safety compel administrators to enforce regular equipment replacement cycles. Consequently, advanced integrated health systems (AIHS) and emergency medical services (EMS) providers are accelerating their procurement activities. Established manufacturers sustain a robust competitive environment by offering differentiated product portfolios and extensive service networks. This synergy between infrastructure maturity and rigorous safety standards ultimately reinforces North America’s status as the primary revenue generator globally.

Europe Medical Warming Cabinets Market Trends

Europe is projected to secure roughly 28% of the global market, with Germany, the United Kingdom, France, and Spain acting as the primary engines of this expansion. The region maintains steady progress through harmonized regulatory frameworks such as Conformité Européenne (CE) marking and the European Union Medical Device Regulation (EU MDR). German healthcare providers lead expenditure on innovative equipment, while the UK emphasizes clinical safety to drive adoption rates. Simultaneously, France and Spain are modernizing surgical theaters to support expanding outpatient services. These strategic initiatives ensure that facilities across the continent can effectively meet evolving infrastructure requirements.

Administrators prioritize infection control and perioperative efficiency to sustain demand. A pivotal shift occurred in June 2025 when the European Commission adopted measures to exclude Chinese medical device manufacturers from public procurement contracts exceeding € 5 million. This policy reshapes competitive dynamics by creating substantial opportunities for compliant local and international vendors. Consequently, a fragmented landscape of regional players is developing differentiated offerings to capture this emerging revenue potential. Organizations are also directing capital toward digitally controlled, energy-efficient units to meet sustainability objectives. Continuous upgrades to operational protocols further bolster this trajectory as decision-makers integrate sophisticated technology to optimize workflows.

Asia Pacific Medical Warming Cabinets Market Trends

Asia Pacific is projected to achieve the fastest regional market expansion at a CAGR of 5.8% through 2033. This positive trajectory results from rapid healthcare infrastructure development and the proliferation of private hospital networks. China, India, and ASEAN member nations are aggressively increasing their medical budgets to support new facility construction. China dominates this landscape due to its immense patient population and escalating surgical case volumes. Simultaneously, India is witnessing a surge in private sector investment that is modernizing its care delivery systems. ASEAN countries are also upgrading their perioperative environments to meet international standards. Consequently, these macroeconomic factors are creating a fertile environment for the widespread adoption of medical warming cabinets across the region.

Rising awareness regarding patient safety is accelerating the demand for energy-efficient and intelligent warming technologies. Global corporations are strategically reinforcing their local operations to capture this growing market share. For instance, STERIS strengthened its Asia Pacific footprint by inaugurating a combined representative office and instrument management services (IMS) repair laboratory in Korea in early 2025. Such initiatives demonstrate a commitment to providing localized support and rapid service capabilities. Regional manufacturers are simultaneously gaining ground by offering cost-effective, modular designs that address specific budget constraints in emerging markets. As regulatory frameworks continue to mature, device approvals are becoming more streamlined, and rising healthcare expenditure combined with higher surgical throughput positions Asia Pacific as a critical high-growth hub for the market.

Competitive Landscape

The global medical warming cabinets market retains a moderately consolidated structure. Dominant organizations such as Stryker, STERIS, Belimed, Getinge, and Panasonic Healthcare control a substantial proportion of total revenue. These established enterprises capitalize on enduring relationships with hospitals and surgical centers to anchor their market position. They also utilize extensive regulatory expertise to ensure adherence to rigorous safety standards. Stakeholders increasingly value integrated systems that combine digital monitoring with energy efficiency. Consequently, continuous investment in R&D remains a critical strategic priority. This focus enables the introduction of advanced capabilities such as IoT connectivity and predictive maintenance, thereby securing technological leadership.

Regional manufacturers and niche specialists are effectively competing by targeting specific application segments. These entities often concentrate on developing compact countertop units or portable systems. They also engineer cost-effective configurations specifically designed for emerging economies. High entry barriers, including strict device certification requirements, limit the influx of new challengers. However, the rising trend of digitalization provides a unique entry point for software-focused firms. Industry experts anticipate that consolidation will gradually intensify as incumbents pursue geographical expansion through strategic mergers and acquisitions (M&A). Meanwhile, smaller innovators are collaborating to create modular, energy-efficient technologies that strengthen their resilience against larger rivals.

Key Industry Developments

In December 2025, Intelliguard launched its Mira Care™ RFID?enabled temperature?controlled cabinet at a major clinical meeting, integrating real?time temperature governance with inventory visibility for hospital and pharmacy operations. This solution enhances compliance and operational efficiency by linking temperature monitoring with automated inventory data and clinical workflows.

Companies Covered in Medical Warming Cabinets Market

• STERIS Corporation

• 3M Company

• Barkey GmbH & Co. KG

• MAC Medical Inc.

• Enthermics Medical Systems

• Skytron LLC

• Belimed AG

• Pedigo Products Inc.

• Medline Industries LP

• Thermo Fisher Scientific

• Labconco Corporation

• Helmer Scientific

• Hoshizaki Corporation

• Pelican Biothermal

Frequently Asked Questions

The global medical warming cabinets market is projected to reach US$ 1.8 billion in 2026.

Increasing surgical procedures, expansion of healthcare infrastructure, growing outpatient and diagnostic services, and rising adoption of digital and IoT-enabled warming solutions are key growth drivers.

The market is expected to grow at a CAGR of 4.2% from 2026 to 2033.

Expansion of ambulatory surgical centers, adoption of portable and modular cabinets, and growth of diagnostic and specialty care facilities present significant market opportunities.

Stryker, Steris, Belimed, Getinge, and Panasonic Healthcare are some of the key players in the market.