- Medical Devices

- Medical Carts Market

Medical Carts Market Size, Share, and Growth Forecast 2026 - 2033

Medical Carts Market by Product (Mobile Computing Carts, Medication Carts, Medical Storage Columns, Cabinets & Accessories, Wall-mounted Workstations, Others), Application (Anesthesia, Emergency, Others), End-user (Hospitals, Ambulatory Surgical Centers, Physician Offices or Clinics, Others), Regional Analysis, 2026 - 2033

Medical Carts Market Size and Trend Analysis

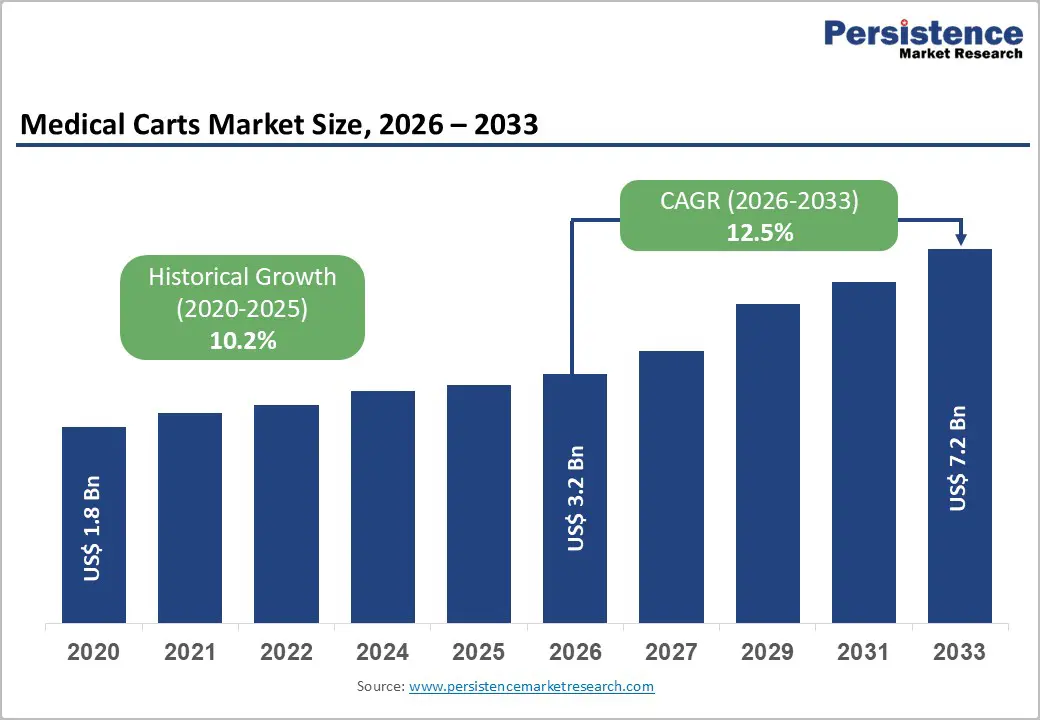

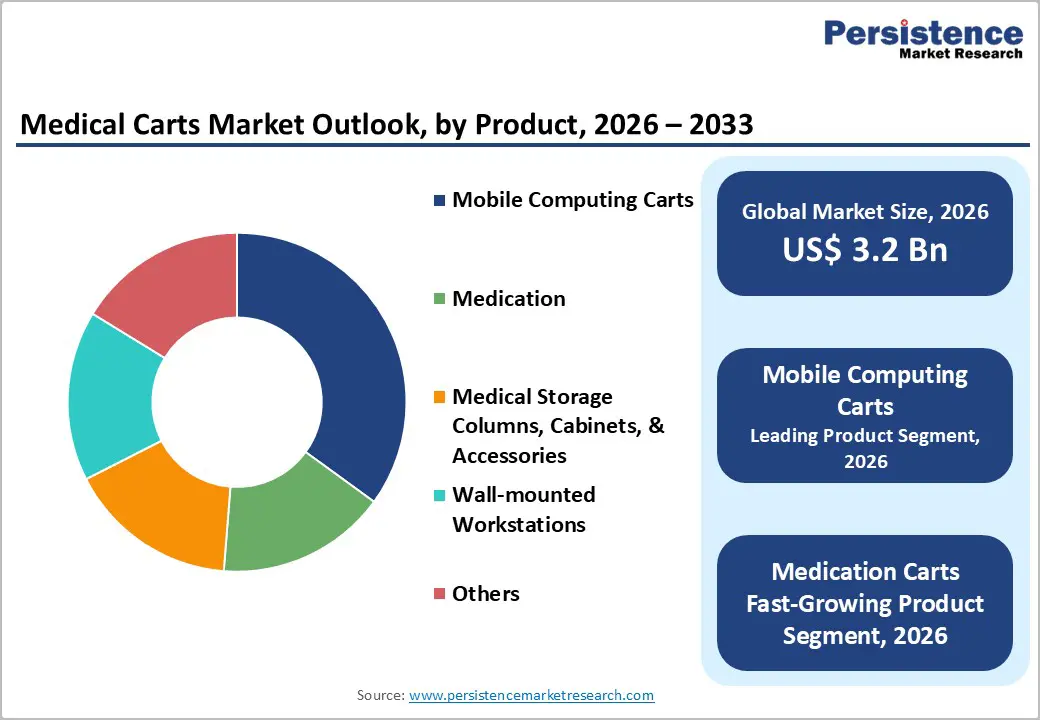

The global medical carts market size is expected to be valued at US$ 3.2 billion in 2026 and projected to reach US$ 7.2 billion by 2033, growing at a CAGR of 12.5% between 2026 and 2033. The market expansion is driven by the escalating adoption of electronic medical records (EMR) and electronic health records (EHR) systems across healthcare facilities, with digital medical records now representing the standard in 90% of healthcare settings.

The rapid integration of telemedicine capabilities and wireless connectivity into mobile computing carts has enabled healthcare providers to access patient data at point-of-care, substantially improving workflow efficiency and medication safety. Additionally, the expanding prevalence of musculoskeletal injuries, rising geriatric population demographics, and increasing emphasis on nursing efficiency and patient safety have substantially elevated demand for advanced medical cart solutions across hospitals, ambulatory surgical centers, and physician offices globally.

Key Industry Highlights:

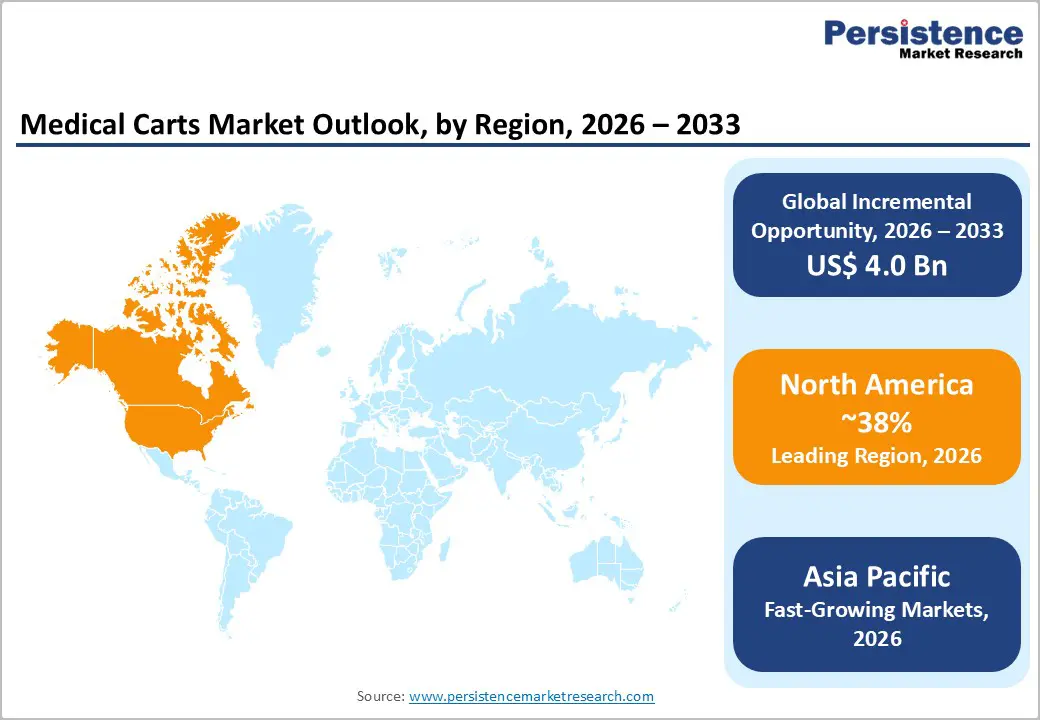

- North America maintains market dominance with 38-46% regional share, anchored by exceptional healthcare infrastructure, universal EMR/EHR adoption (90% of facilities), and premium technology deployment supporting sustained growth and innovation investment across hospital and ambulatory settings.

- Mobile Computing Carts command 35% market dominance, featuring wireless connectivity, EHR integration, touchscreen interfaces, barcode scanners, and RFID readers, enabling point-of-care clinical documentation, medication safety, and patient engagement across healthcare facilities.

- Emergency/Crash Cart Applications represent around 41.7% market share, providing rapid-access life-saving equipment, cardiac medications, resuscitation supplies, and defibrillators organized for immediate accessibility during critical emergencies and code situations.

- Ambulatory Surgical Centers represent fastest-growing segment with transitioning EHR adoption, private equity consolidation, and value-based care requirements driving demand for compact, cost-optimized mobile workstation solutions tailored to outpatient surgical environments.

| Global Market Attributes | Key Insights |

|---|---|

| Medical Carts Market Size (2026E) | US$ 3.2 billion |

| Market Value Forecast (2033F) | US$ 7.2 billion |

| Projected Growth CAGR (2026 - 2033) | 12.5% |

| Historical Market Growth (2020 - 2025) | 10.2% |

Market Dynamics

Drivers - Rapid Electronic Medical Records Adoption and Digital Health Transformation Across Healthcare Systems

The medical carts market is experiencing exceptional growth driven by the comprehensive adoption of electronic medical records (EMR) and electronic health records (EHR) systems across global healthcare facilities. With digital medical records now representing the standard in approximately 90% of healthcare facilities, the demand for mobile computing carts capable of seamless EHR integration has accelerated substantially. Mobile computing carts equipped with wireless connectivity, touchscreen interfaces, barcode scanners, and RFID readers enable healthcare professionals to access critical patient information, medication histories, and real-time clinical alerts at the point-of-care without returning to centralized workstations. The integration of barcode-labeled medication administration (BCMA) systems with mobile carts has demonstrated significant improvements in medication safety, reducing adverse medication errors and enhancing patient outcomes. Healthcare organizations worldwide are prioritizing technology solutions that facilitate efficient documentation, streamlined medication delivery, and improved clinical collaboration among multidisciplinary care teams.

Telemedicine Integration and Growing Demand for Mobile Point-of-Care Solutions

Technological advancement in medical cart design has fundamentally transformed point-of-care delivery capabilities, with modern carts incorporating telemedicine functionalities, dual-monitor configurations, and ergonomic height adjustment systems. The emergence of telehealth services and remote patient monitoring requirements, particularly accelerated during and after the COVID-19 pandemic, has substantially elevated procurement of mobile computing carts equipped with video conferencing capabilities. Healthcare providers are increasingly deploying mobile carts with tablet-compatible platforms, wireless patient monitoring integration, and secure remote consultation features to facilitate virtual patient engagement, specialist consultations, and continuity-of-care in resource-constrained and geographically remote settings. The design evolution toward lightweight, compact, and easily maneuverable carts has enabled utilization across diverse healthcare environments including hospital wards, intensive care units, emergency departments, and home healthcare settings. The incorporation of lithium iron phosphate batteries with extended operational capacity ensures reliable continuous performance throughout extended clinical shifts without requiring frequent recharging.

Restraint -High Initial Capital Costs and Maintenance Expenses Limit Market Accessibility

The medical carts market faces significant constraints from elevated device costs and substantial ongoing maintenance expenses that restrict adoption in resource-constrained healthcare environments. Advanced medical carts incorporating integrated computing systems, wireless connectivity, barcode scanning, and RFID technology command premium pricing that challenges budget allocation decisions in smaller healthcare facilities, ambulatory surgical centers, and healthcare systems in emerging economies. Beyond initial capital expenditure, healthcare organizations must invest substantially in staff training, software licensing, system integration with existing electronic health record platforms, and ongoing technical support, creating cumulative financial burdens. The complexity of integrating advanced medical carts with diverse healthcare information technology ecosystems requires specialized technical expertise that may be unavailable in developing regions, further limiting market penetration in price-sensitive markets.

Skilled Workforce Requirements and Complex Integration Challenges with Legacy Systems

The deployment of technologically sophisticated medical carts necessitates comprehensive staff training programs and organizational change management initiatives that create substantial implementation barriers. Healthcare professionals require extensive education on proper cart utilization, medication dispensing procedures, electronic medication administration record (eMAR) systems, and infection control protocols using anti-microbial surfaces. Many healthcare facilities operate legacy systems incompatible with modern mobile computing carts, requiring costly system upgrades or replacement before cart deployment becomes feasible. The availability of skilled biomedical technicians and information technology specialists capable of managing complex cart technologies remains limited in developing nations and rural healthcare settings, creating operational sustainability challenges and deterring investment in advanced solutions.

Opportunities - Expansion of Ambulatory Surgical Centers and Physician Offices Creating High-Growth Segments

Ambulatory surgical centers (ASCs) and independent physician offices represent the fastest-growing end-user segments for medical carts, creating substantial market opportunities for manufacturers. While historically remaining reliant on paper documentation, ASCs are rapidly transitioning toward digital health records driven by private equity consolidation, health system affiliations, and increasing competition requiring standardized clinical data collection. The strategic migration toward value-based care models demands comprehensive digital documentation systems that demonstrate quality outcomes and cost-effectiveness compared to hospital-based procedures. Modern ASC-appropriate medical carts featuring compact design, streamlined workflows, and cost-optimized configurations present significant growth potential. Emerging market trends indicate that physician offices increasingly adopt comprehensive mobile medical carts for medication management, patient engagement, and telemedicine consultations, with a projected 17.4% CAGR growth during the forecast period. Companies developing cost-effective, space-efficient solutions tailored to ASC and physician office requirements are positioned to capture substantial market share as regulatory pressure and competitive dynamics accelerate digital transformation.

Category-wise Analysis

Product Type Insights

Mobile Computing Carts represent the dominant segment in the medical carts market, commanding approximately 35% market share in 2025, reflecting their essential role in enabling clinicians to access patient information at point-of-care. Mobile computing carts powered by advanced lithium iron phosphate battery technology provide healthcare professionals with integrated systems combining clinical documentation, medication management, and patient engagement capabilities. Modern mobile computing carts incorporate wireless connectivity, dual-monitor configurations, touchscreen interfaces, barcode scanners, and RFID readers, enabling seamless integration with electronic health record systems and real-time access to diagnostic imaging. Ergotron’s market-leading platform has evolved over 40 years of healthcare ergonomic innovation, with products including the LX Pro next-generation cart and Mosaic LCD/Laptop configurations providing flexible solutions for diverse clinical applications. Capsa Healthcare’s product portfolio encompasses comprehensive mobile computing workstations optimized for medication delivery, treatment procedures, and clinical documentation. The increasing adoption of telemedicine capabilities, patient engagement features, and anti-microbial surfaces in mobile computing carts continues to drive segment expansion and pricing optimization.

Application Type Insights

Emergency care applications command the leading segment position within medical carts market, commanding approximately 41.7% market share in 2024, driven by critical demand for rapid-access emergency supplies and medication delivery during cardiac and traumatic emergencies. Crash carts or emergency trolleys represent essential mobile units equipped with life-saving equipment, defibrillators, cardiac medications, and resuscitation supplies organized in designated compartments enabling rapid healthcare provider access during code blue situations. Standardized crash cart configurations include defibrillators, electrocardiogram (ECG) leads, blood pressure monitoring equipment, emergency medications including epinephrine, atropine, lidocaine, and vasopressors, resuscitation supplies, and airway management equipment. The emphasis on crash cart management protocols, regular equipment verification, and medication expiration date monitoring has elevated requirements for organized, accessible cart design and inventory tracking systems. Healthcare facilities are increasingly adopting customizable emergency cart configurations tailored to specific departmental requirements including cardiac, pediatric, trauma, and neonatal emergency variations. Anesthesia applications and general clinical care applications represent additional significant segments within the medical carts market, with specialized configurations optimized for perioperative workflows and ward-based care delivery.

End-user Insights

Hospitals maintain dominant market leadership for medical carts, accounting for approximately 36-37% market share, reflecting their centrality in performing complex surgical procedures and acute care interventions. Major teaching hospitals and academic medical centers operate sophisticated point-of-care technology environments with hundreds of mobile computing carts deployed across emergency departments, intensive care units, operating suites, and general ward areas. Hospitals have systematically implemented EHR-compatible mobile carts to facilitate compliance with barcode-labeled medication administration (BCMA) requirements and electronic medication administration record (eMAR) protocols improving medication safety and reducing adverse events. However, Ambulatory Surgical Centers (ASCs) represent the fastest-growing end-user segment, expanding at growth rates substantially exceeding hospital trajectories. Regional Insights

Regional Insights

North America Medical Carts Market Trends

North America Medical Carts Market Trends demonstrate the region’s prominent leadership driven by advanced healthcare infrastructure, strong technology adoption, and increasing demand for efficient clinical workflows. Hospitals and ambulatory care centers are rapidly integrating mobile computing carts and smart medication carts to support electronic health records (EHR) access at the point of care, enhance medication safety, and improve staff productivity. The region’s emphasis on digital transformation, interoperability of devices, and real-time data documentation accelerates demand for connected medical cart solutions. Robust investments in healthcare IT, favorable reimbursement frameworks, and stringent regulations promoting patient safety further support widespread adoption. Additionally, the prevalence of chronic diseases, the needs of the aging population, and high procedural volumes fuel ongoing modernization of clinical spaces with wall-mounted workstations and storage solutions. Overall, North America continues to dominate the medical carts market by combining technological innovation with strong institutional support for improving care delivery and operational efficiency.

Asia Pacific Medical Carts Market Trends

Asia Pacific Medical Carts Market Trends show strong emerging growth driven by expanding healthcare infrastructure, rising investments in digital health, and increasing demand for efficient clinical workflows. Countries such as China, India, Japan, and Southeast Asian nations are upgrading hospitals and clinics to improve patient care and operational efficiency, prompting higher adoption of mobile computing carts, medication carts, and wall-mounted workstations. Growth in medical tourism and government healthcare initiatives is accelerating the procurement of advanced medical cart solutions.

Additionally, rising awareness of medication safety, electronic health record integration, and point-of-care documentation is encouraging healthcare facilities to implement connected and smart cart systems. Local manufacturers and global suppliers are expanding their presence to cater to cost-sensitive and tier-2 and tier-3 market segments. Overall, Asia Pacific is emerging rapidly as a high-growth region for medical carts, supported by healthcare modernization, increasing clinical procedures, and rising adoption of health IT solutions.

Competitive Landscape

The medical carts market is characterized by a moderately consolidated structure, where large healthcare technology players hold a significant share through broad product portfolios, strong global distribution networks, and sustained investments in research and development. These players typically offer integrated solutions covering mobile computing carts, medication management carts, emergency carts, and wall-mounted workstations, enabling them to serve diverse clinical needs across hospital departments. At the same time, the market remains partially fragmented, with regional and niche manufacturers competing through application-specific designs, customization, and localized pricing strategies.

Key Market Developments

- In May 2024, Altus Industries Inc. introduced AI-powered mobile medical carts featuring connectivity for location tracking, AI detection of patient risks like fall attempts, real-time alerts, and camera monitoring to enhance remote patient care and prevent injuries.

- In September 2025, Sky Labs launched CART BP, a ring-type cuffless blood pressure monitor worn on the finger, enabling continuous 24-hour monitoring, including nighttime measurements, with app integration for calendar-based data visualization and health insights.

Companies Covered in Medical Carts Market

- Ergotron, Inc.

- ITD GmbH

- Capsa Healthcare

- Enovate Medical

- TOUCHPOINT MEDICAL INC.

- JACO Inc.

- Advantech Co., Ltd.

- Harloff Manufacturing Co.

- Medline Industries Inc.

- Armstrong Medical Inc.

- McKesson Medical-Surgical Inc.

- Omnicell Inc.

- Altus Health System

- CompuCaddy

- GCX Corporation

Frequently Asked Questions

The global medical carts market is projected to reach US$ 3.2 billion in 2026.

Growth is driven by widespread EHR/EMR adoption, telemedicine expansion, aging populations, nursing efficiency needs, and smart cart technologies.

North America leads the market, while Asia Pacific is the fastest-growing region.

Key opportunities include ASC expansion, emerging Asia Pacific healthcare infrastructure growth, and AI-enabled, cloud-connected smart carts.

Ergotron Inc., Capsa Healthcare, Enovate Medical, and TOUCHPOINT MEDICAL holds dominant market positions.