- Hardware & Software IT Services

- Materials Management Information System (MMIS) Market

Materials Management Information System (MMIS) Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Materials Management Information System (MMIS) Market by Component Type (Software, Services), End-User (Manufacturing, Healthcare, Logistics, E-Commerce), Deployment Type (Cloud-Based, On-Premise, Hybrid), and Regional Analysis for 2026 - 2033

Materials Management Information System (MMIS) Market Share and Trends Analysis

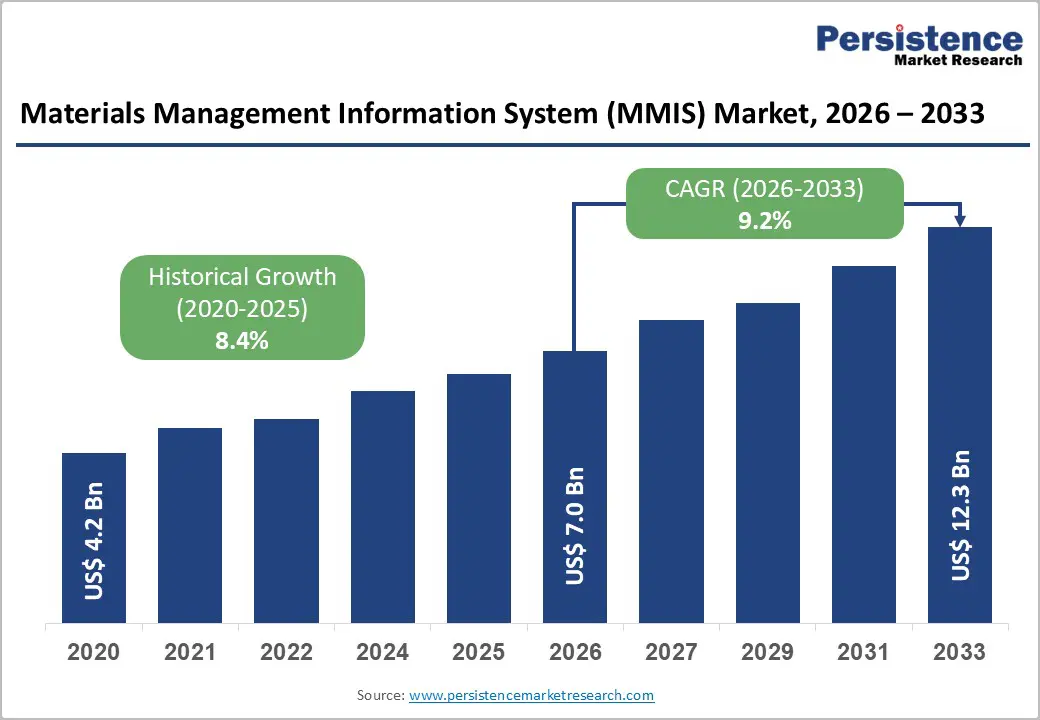

The global materials management information system (MMIS) market size is likely to be valued at US$ 7.0 billion in 2026, and is projected to reach US$ 12.3 billion by 2033, growing at a CAGR of 9.2% during the forecast period 2026 - 2033.

This robust expansion reflects the accelerating digital transformation across supply chain operations worldwide. Organizations are increasingly prioritizing real-time inventory visibility and data-driven decision-making to navigate complex global supply chains. The integration of advanced technologies, including artificial intelligence, Internet of Things sensors, and cloud computing platforms, is fundamentally reshaping materials management capabilities. The manufacturing, healthcare, and logistics sectors are leading implementation efforts, driven by the imperative to reduce operational costs, minimize waste, and achieve greater supply chain resilience amid persistent global uncertainties.

Key Industry Highlights

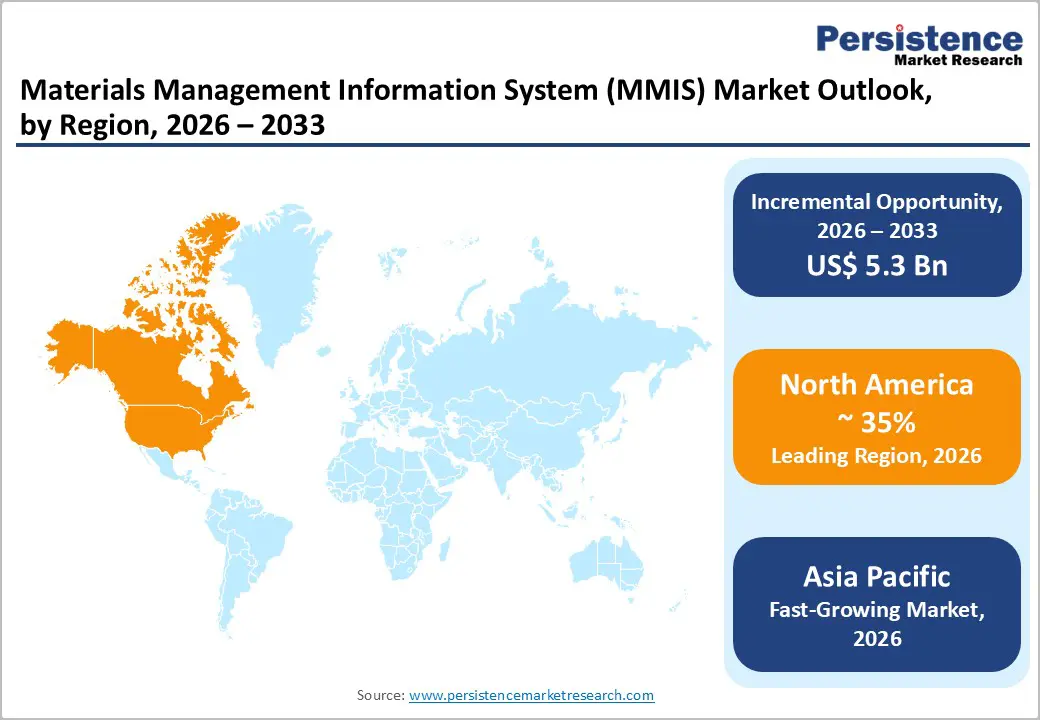

- Dominant Region: North America is expected to command a market share of roughly 35% in 2026, fueled by sustained investments in cutting-edge technologies.

- Fastest-growing Regional Market: The Asia Pacific market is poised to be the fastest-growing through 2033, underpinned by rapid industrialization and government-led digital transformation programs.

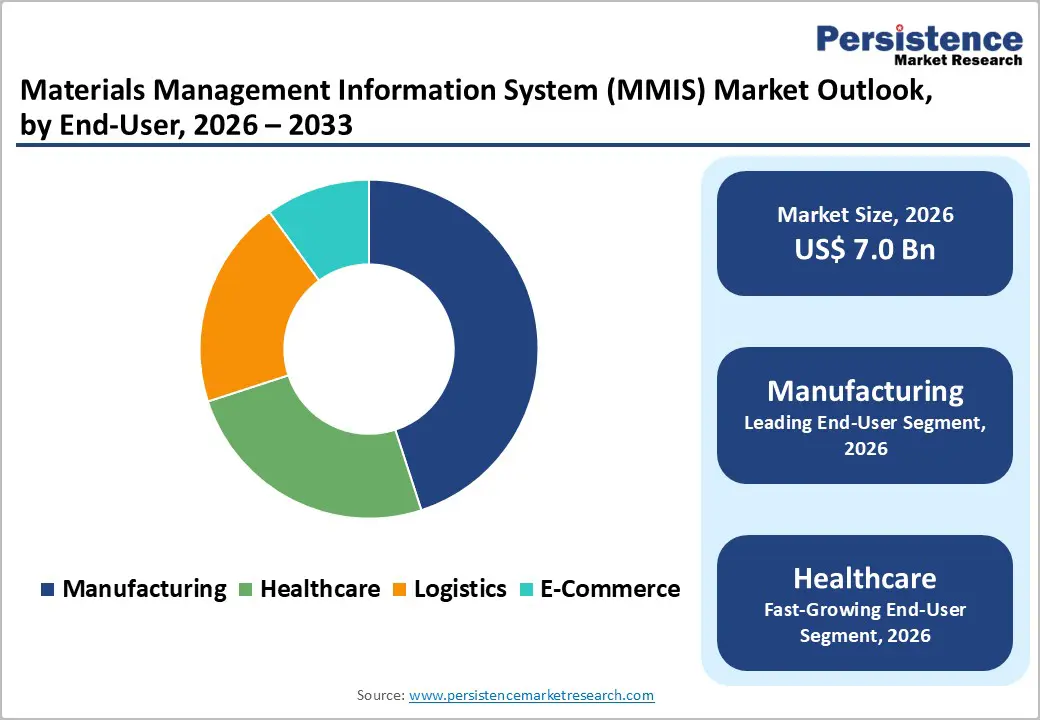

- Leading End-User: Manufacturing is slated to lead with an estimated 45% revenue share in 2026, on account of the heightening need for highly accurate inventory control solutions.

- Fastest-growing End-User: Healthcare is expected to post the highest CAGR through 2033, as advanced MMIS gains recognition for enhancing patient care quality and operational efficiency.

- Governmental Push: The Government of Nigeria launched the Nigeria Raw Materials Management Information System (RMMIS), a national digital platform providing real-time data on the country’s raw materials.

- September 2025: Oracle announced AI-powered enhancements in Fusion cloud supply chain & manufacturing applications, including advanced inventory management for healthcare that automates stock optimization, robotic material handling, and real-time cross-docking alerts.

| Key Insights | Details |

|---|---|

| Materials Management Information System (MMIS) Market Size (2026E) | US$ 7.0 Bn |

| Market Value Forecast (2033F) | US$ 12.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Supply Chain Visibility and Risk Mitigation Requirements

Supply chain visibility and risk mitigation are becoming central priorities for organizations seeking to streamline materials management. Businesses increasingly recognize the need for unified platforms that connect materials management functions with broader enterprise systems to address integration challenges. Materials management information systems support this shift by providing real-time tracking of materials throughout the supply chain, enabling organizations to anticipate disruptions and respond quickly when they occur. These platforms help companies monitor supplier reliability, track shipment movements, and maintain optimal inventory levels across diverse locations, thereby improving operational continuity and reducing waste.

Centralized access to supply chain data also enhances decision-making around sourcing strategies, procurement schedules, and resource allocation. MMIS tools allow stakeholders to assess performance and risk indicators in a single environment, supporting more accurate planning and prioritization. Regulatory expectations related to transparency and sustainability are further shaping adoption, as authorities in many regions increasingly encourage or mandate traceability and responsible sourcing practices in critical industries. In sectors where compliance requires detailed documentation of product origin, handling, and movement, MMIS deployments help organizations demonstrate adherence to these requirements while strengthening resilience and competitiveness in complex, globalized supply networks.

Cybersecurity Concerns and Data Privacy Regulations

MMIS platforms manage large volumes of sensitive operational data, including inventory records, supplier profiles, procurement workflows, and critical asset tracking information. The expanding cyber threat landscape creates significant concern for organizations evaluating these systems, particularly when they rely on cloud-based architectures and external hosting providers. Decision-makers must weigh the efficiency and scalability benefits of MMIS against the potential exposure of confidential business information, assessing both technical safeguards and vendor practices. Perceptions of security robustness strongly influence whether organizations proceed with deployment, delay investment, or limit the scope of implementation.

Industries subject to stringent data privacy and security regulations face additional layers of complexity when adopting MMIS solutions. Regulatory frameworks such as global privacy rules, healthcare confidentiality standards, and sector-specific data protection mandates require organizations to demonstrate strong controls over access, storage, and use of sensitive information. This reinforces the need for robust encryption, identity and access management, continuous monitoring, and well-documented audit trails. Compliance teams also prioritize data residency, ensuring that information remains within approved jurisdictions. Any indication of vulnerability or a widely publicized breach can erode stakeholder confidence, slowing adoption in sectors such as healthcare, financial services, and government that routinely handle highly confidential data.

Artificial Intelligence and Predictive Analytics Integration

The integration of artificial intelligence (AI) and machine learning (ML) presents a transformative opportunity for MMIS providers and end users. These technologies enable advanced demand forecasting, automated replenishment decisions, and predictive maintenance workflows, collectively enhancing operational efficiency and supply reliability. By embedding intelligent algorithms within materials management information systems, organizations can continuously optimize inventory policies, sourcing decisions, and material flows in response to changing conditions. This capability reduces manual intervention, improves planning accuracy, and strengthens alignment among procurement, operations, and finance.

Machine learning models interpret historical consumption trends, seasonal patterns, and external influencing factors to generate more precise demand signals, lowering the risk of stockouts while curbing excess inventory and associated carrying costs. In parallel, predictive maintenance capabilities support the early identification of equipment or asset issues, allowing maintenance teams to schedule interventions before failures disrupt operations. This promotes higher asset utilization and more stable production environments. As AI tools become easier to deploy and integrate, MMIS vendors that deliver embedded intelligence and clearly demonstrable performance improvements are positioned to gain a competitive edge, deepen customer relationships, and drive wider adoption across industries that prioritize resilience, cost efficiency, and data-driven decision-making.

Category-wise Analysis

Component Insights

Software is slated to be the leading segment with an approximate 70% of the MMIS market revenue share in 2026. Organizations often prioritize comprehensive software platforms that integrate procurement, inventory management, warehouse operations, and logistics tracking into unified systems. Modern MMIS software incorporates advanced analytics dashboards, mobile accessibility, and API connectivity enabling integration with complementary enterprise systems. Software solutions deliver immediate value through automation of manual processes, real-time visibility into inventory positions, and sophisticated reporting capabilities supporting data-driven decision-making. The shift toward subscription-based software-as-a-service models improves affordability and accelerates deployment timelines. Organizations value the flexibility to scale user licenses and functionality modules as operational requirements evolve, avoiding the constraints of traditional perpetual licensing models.

Services is likely to be the fastest-growing segment during the 2026 - 2033 forecast period. Organizations increasingly depend on specialized expertise for MMIS implementation, customization, and continuous optimization. Professional services such as consulting, system integration, and training are critical to maximize returns and drive strong user adoption. At the same time, managed services are gaining prominence as enterprises outsource monitoring, maintenance, and performance tuning, allowing internal IT teams to prioritize strategic initiatives. The rise of cloud-based deployments further fuels demand for migration support, security configuration, and multi-cloud management capabilities that ensure reliable, secure MMIS operations.

End-User Insights

Manufacturing is anticipated to secure an estimated 45% of the materials management information system market revenue share in 2026, owing to complex supply chains and the deepening urgency for highly accurate inventory control. The adoption of just-in-time practices makes synchronized material availability with production schedules essential, positioning MMIS as core operational infrastructure. Manufacturers use these systems to manage bills of materials, work-in-progress inventory, finished goods distribution, and supplier relationships, while integration with execution and enterprise planning platforms delivers end-to-end production visibility. Industry 4.0 programs that deploy IoT sensors and automation further extend MMIS value by enabling real-time monitoring and adaptive scheduling across manufacturing environments.

Healthcare is expected to be the fastest-growing segment during the 2026 - 2033 forecast period. As providers recognize that effective materials management directly supports patient care quality and operational efficiency. Hospitals and health systems deploy MMIS to secure timely availability of medical supplies, pharmaceuticals, and equipment while managing regulatory obligations and expiration tracking. Integration with clinical and patient monitoring systems enables more automated replenishment based on real-time consumption. The pandemic experience exposed weaknesses in healthcare supply chains, accelerating investment in advanced solutions that can support surge demand, lot and recall management, and tight integration with electronic health records, while built-in compliance features and comprehensive audit trails address the sector’s stringent regulatory environment.

Deployment Insights

Cloud-based is expected to lead with approximately 52% of the MMIS market revenues in 2026. Cloud-based deployment is gaining rapid traction as organizations seek more scalable, cost-efficient, and accessible alternatives to traditional on-premise MMIS installations. This model allows enterprises to avoid large upfront hardware investments by adopting subscription-based pricing that aligns with actual usage and user needs. It also supports remote and distributed workforces through secure, browser-based access across multiple locations. In addition, cloud platforms deliver automatic updates, ensuring continuous access to the latest features, security enhancements, and performance improvements while reducing the burden on internal IT teams.

On-premise is projected to be the fastest-growing segment from 2026 to 2033. On-premise deployment continues to hold a strong position, especially in sectors with strict data security expectations and prescriptive compliance obligations, such as financial services, government, and defense. Organizations in these areas often require full control over sensitive information and infrastructure, making internally hosted MMIS environments preferable. This approach allows teams to tailor security protocols, network configurations, and access controls to align closely with internal risk policies and regulatory interpretations.

Regional Insights

North America Materials Management Information System (MMIS) Market Trends

North America is set to capture a significant portion of the materials management information system market share at approximately 35% in 2026. The leadership is supported by early adoption and sustained technology investment. The United States underpins this dominance with advanced digital infrastructure, high levels of enterprise IT spending, and a strong concentration of large organizations managing complex supply chains. The region’s mature manufacturing base, extensive logistics networks, and sophisticated healthcare systems generate consistent demand for materials management solutions that enhance operational excellence and support regulatory compliance. Businesses increasingly prioritize integrated platforms that connect procurement, inventory, production, and distribution functions to achieve end-to-end visibility and greater supply chain resilience.

Growth is further underpinned by a strong focus on supply chain optimization, rapid adoption of cloud-based architectures, and ready access to experienced implementation partners. Regulatory expectations related to data security, supply chain transparency, and sustainability reporting encourage organizations to invest in compliant MMIS platforms that support detailed tracking and auditability across the value chain. Frameworks governing healthcare data protection and sector-specific standards strongly influence solution design and vendor selection. Investment priorities increasingly center on AI-enabled analytics, IoT integration for real-time monitoring, and blockchain-based traceability initiatives. The competitive landscape features a mix of global enterprise software leaders and agile startups specializing in specific verticals, deployment models, or advanced analytics capabilities, creating a dynamic environment for innovation and partnership.

Europe Materials Management Information System (MMIS) Market Trends

Europe is likely to hold around 25% of the MMIS market share in 2026 with Germany, the United Kingdom, France, and Spain act as core demand centers within the region. The region’s strong industrial base, particularly in automotive and industrial equipment, drives the need for precise materials planning, traceability, and inventory control. The sustainability directives and circular economy policies of the European Union (EU) have encouraged the adoption of systems that support waste reduction, recycling, and lifecycle tracking of materials, aligning MMIS capabilities with regulatory requirements and corporate environmental, social, & governance (ESG) objectives. Industry 4.0 programs that embed digital technologies into factories, combined with supply chain restructuring in the U.K. and broader resilience priorities after recent disruptions, further reinforce investment in advanced materials management platforms.

Germany’s manufacturing sector plays a pivotal role in regional MMIS deployment, using these systems to support smart factory initiatives, optimize supplier networks, and strengthen integration between production and logistics. Harmonized regulations across EU member states simplify cross-border compliance for multinational organizations, although stringent data protection rules add design and deployment considerations for cloud-based solutions. The competitive environment features strong European software vendors, such as SAP, operating alongside global providers, which helps sustain continuous innovation. Investment activity increasingly focuses on sustainability-oriented capabilities, cloud platforms tailored to small and mid-sized enterprises, and industry-specific configurations for automotive, pharmaceutical, and food processing applications.

Asia Pacific Materials Management Information System (MMIS) Market Trends

Asia Pacific is foreseen to emerge as the fastest-growing market for materials management information systems between 2026 and 2033. China, India, and ASEAN countries are driving regional expansion through rapid industrialization, rising manufacturing capacity, and government-led digital transformation programs. The region’s cost-competitive manufacturing base and deep integration into global supply chains increase the need for efficient materials planning, traceability, and inventory optimization, particularly in export-oriented sectors such as electronics, automotive components, and textiles. The proliferation of e-commerce and speedily expanding logistics infrastructure in the region has further boosted the demand for MMIS that can coordinate warehouse operations, fulfillment centers, and transportation networks across multiple countries.

Japan leads in advanced manufacturing integration by leveraging smart factory concepts and automation, while many emerging markets favor cloud-based MMIS deployments that provide lower upfront costs and faster implementation. Policy initiatives also play a decisive role, with large-scale regional trade, connectivity, and digital programs increasing cross-border supply chain complexity and raising the importance of end-to-end visibility solutions. Regulatory conditions differ significantly by country, and data localization and sovereignty rules in major markets such as China and India shape vendor deployment strategies and infrastructure decisions. Competitive dynamics feature global providers investing in regional data centers alongside local vendors developing market-specific functionality and language, resulting in a diverse solution landscape.

Competitive Landscape

The global materials management information system market landscape is moderately concentrated, led by vendors such as SAP SE (SAP), Oracle Corporation, Microsoft Corporation, International Business Machines (IBM), and Zoho Corporation, which together hold roughly 40% to 45% of the total revenues. These incumbents win by bundling procurement, inventory, and supplier workflows into broad enterprise resource planning (ERP) ecosystems, then scaling adoption through mature partner channels and proven implementation playbooks. To protect their positions, they invest heavily in research & development (R&D) to improve usability, add analytics, and strengthen integration across finance and operations.

Competition remains intense because buyers can also choose cloud-native and specialist providers that focus on faster deployment, configurable workflows, and Software-as-a-Service (SaaS) delivery. Several of these competitors differentiate through automation, mobile-first experiences, and open application programming interface (API) connectivity that reduces dependence on custom code. At the same time, leading suppliers accelerate strategic partnerships, mergers, and acquisitions to fill capability gaps, expand industry depth, and enter new geographies, which raises the pace of product convergence.

Key Industry Developments

- In October 2025, Mercedes-Benz India partnered with Zoho to launch SKYLine, a bespoke decentralized dealer management system (DMS) built on Zoho customer relationship management (CRM) and Qntrl workflow platform. SKYLine digitizes the full service lifecycle, from bookings and digital check-ins to skill-based technician assignments, real-time tracking, and feedback, granting dealer autonomy while integrating seamlessly with legacy headquarters systems via a custom middleware layer

- In June 2025, Precisely launched Intelligent Autocomplete for Automate Evolve, an AI-powered feature that auto-populates up to 300 SAP ERP master data fields. Unveiled at Trust '25, this early adopter solution transforms manual entry into streamlined review workflows, reducing errors and workload while enhancing API integration for robotic process automation (RPA) and integration Platform as a Service (iPaaS)..

- In June 2025, Oklahoma State University researchers enhanced the OK-EFRA ArcGIS tool to track 14 high-priority hazardous materials shipments statewide and provide county-specific risk maps for Local Emergency Planning Committees (LEPCs) and first responders. The updated application includes a 2018-2024 dashboard comparing storage/transport data, aiding equipment planning, evacuation strategies, and chemical response exercises across vulnerable sites such as schools and hospitals.

Companies Covered in Materials Management Information System (MMIS) Market

- SAP SE

- Oracle Corporation

- Blue Yonder

- Microsoft Corporation

- IBM Corporation

- Infor

- Tecsys Inc.

- Epicor Software Corporation

- NetSuite Inc.

- Caduceus Systems

- Netcom Data Systems

- Sage Group

- Syspro

- Zoho Corporation

- Synergy Logistics

Frequently Asked Questions

The global materials management information system (MMIS) market is projected to reach US$ 7.0 billion in 2026.

The escalating need for real-time supply chain visibility, inventory optimization, and regulatory-compliant traceability across complex, multi-site operations is driving the market.

The market is poised to witness a CAGR of 9.2% from 2026 to 2033.

Key opportunities lie in AI-enabled analytics, cloud-based deployments, and industry-specific solutions that enhance automation, predictive planning, and sustainability reporting for manufacturing and healthcare organizations.

SAP SE, Oracle Corporation, Microsoft Corporation, IBM Corporation, and Zoho Corporation are some of the key players in this market.