- Advanced Materials

- Nanomaterials Market

Nanomaterials Market Size, Share, and Growth Forecast, 2025 - 2032

Nanomaterials Market by Product Type (Metal Oxides, Non Metal Oxides, Carbon Nanotubes (CNTs), Carbon Black, Nanoparticles, Nanoclays, Nanofibers, Nanocomposites, Misc.), Material Type (Carbon-Based, Metal-Based, Metal & Non-metal Oxides, Polymeric Nanomaterials, Composite / Hybrid Nanomaterials, Ceramic-Based Nanomaterials, Misc.), Industry (Healthcare & Pharmaceuticals, Electronics & Electricals, Energy & Power, Others), and Regional Analysis for 2025 - 2032

Nanomaterials Market Size and Trends Analysis

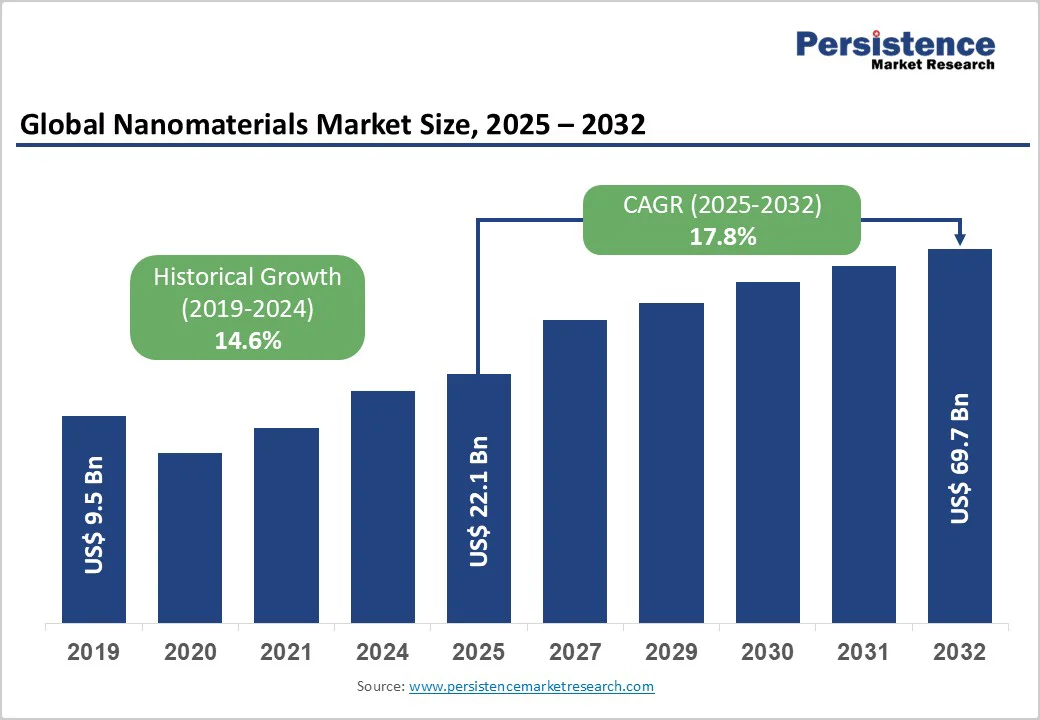

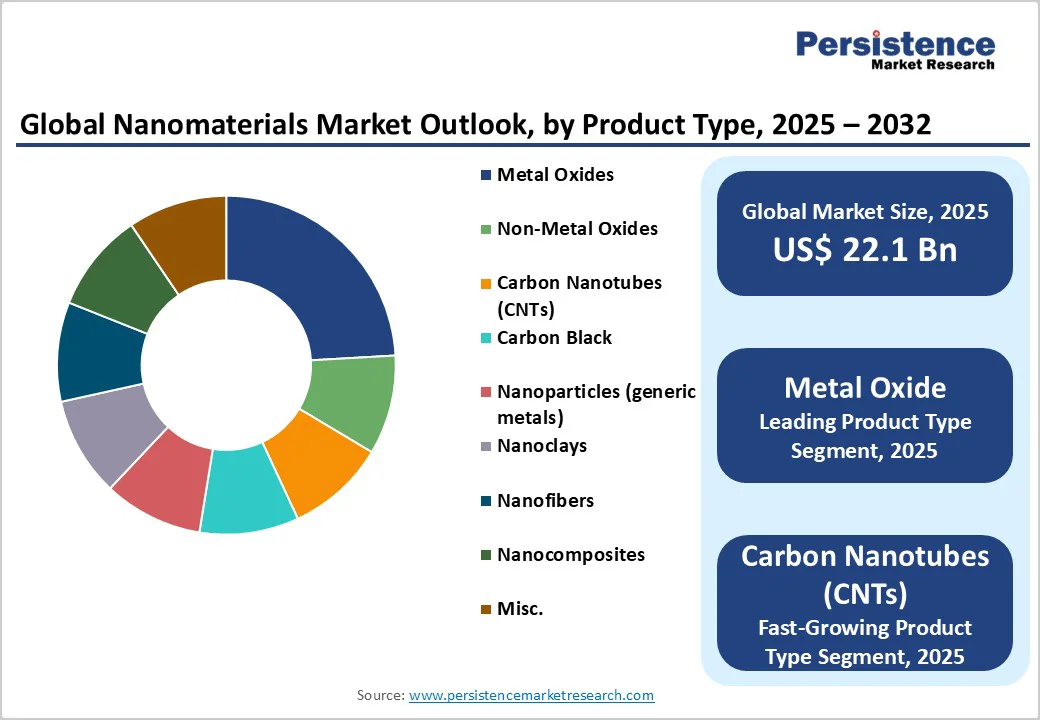

The global nanomaterials market size is likely to value at US$ 22.1 billion in 2025 and is projected to reach US$ 69.7 billion by 2032, growing at a CAGR of 17.8% between 2025 and 2032.

Advanced semiconductor fabrication requirements, expanding energy storage applications, and breakthrough healthcare innovations drive unprecedented demand for high-performance nanomaterials across electronics, automotive, and renewable energy sectors, positioning the market for sustained double-digit growth through technological convergence and industrial digitalization.

Key Industry Highlights:

- Metal Oxides lead product segments at 30% share, while Carbon Nanotubes achieve the fastest growth at 12% share through battery and electronics adoption

- Carbon-Based materials dominate at 32% material type share, with Metal-Based segments experiencing the highest growth rates in specialised applications

- Electronics & Electricals sector maintains 25.6% end-use leadership as the Energy & Power segment demonstrates the fastest expansion through renewable energy integration

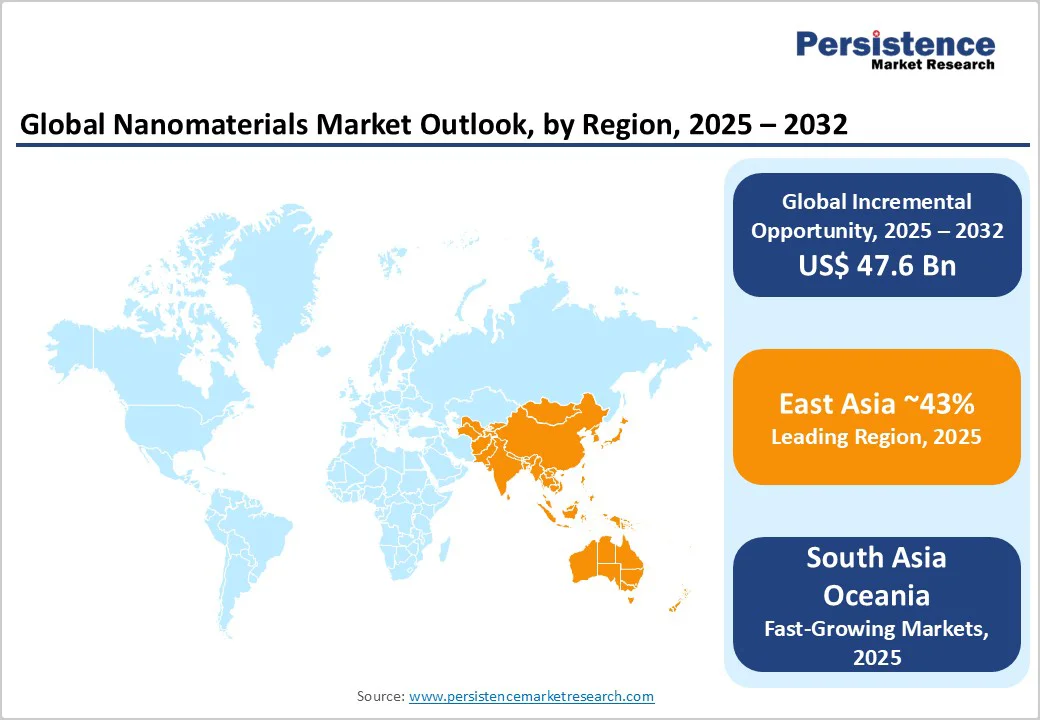

- East Asia commands 43% regional market share, led by China's manufacturing scale and Japan-South Korea technology expertise in electronics

- Strategic acquisitions exceed $2 billion valuations, including Daikin-OCSiAl partnership and major production capacity expansions across Europe and Asia

- Regulatory harmonization efforts through ISO and OECD create standardized frameworks, reducing compliance barriers for global market expansion.

| Key Insights | Details |

|---|---|

| Nanomaterials Market Size (2025E) | US$ 22.1 Bn |

| Market Value Forecast (2032F) | US$ 69.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 17.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 14.6% |

Market Dynamics

Driver - Advanced Material Integration Across Industrial Applications

Nanomaterials have become integral in high-performance sectors, including electronics, healthcare, and renewable energy. The transition toward nano-enabled coatings, sensors, and catalysts has accelerated with advancements in industrial nanofabrication.

According to data from the Semiconductor Industry Association (2024), global semiconductor sales exceeded US$627 billion, underscoring the increasing utilization of nanomaterials in chip manufacturing, wafer polishing, and nano-dielectric systems.

The impact is evident across electric mobility and renewable power systems, where nanocatalysts enhance efficiency by 30-45% compared to conventional materials. This industrial material transformation boosts precision, reliability, and functional efficiency, reinforcing nanomaterials’ role in next-generation manufacturing ecosystems...

Government Research Funding and Policy Support for Nanotechnology Innovation

Public funding directed toward nanotechnology R&D remains a pivotal growth enabler. According to the European Commission’s 2024 Horizon Europe framework, more than €1.1 billion was allocated to materials and nanotechnology research, focusing on semiconductor and environmental nanomaterials.

The U.S. National Nanotechnology Initiative (NNI) has disbursed cumulative funding exceeding US$ 29 billion since 2001, with recent allocations prioritizing energy, mobility, and healthcare innovations.

These coordinated efforts across North America, Europe, and Asia reinforce the commercialisation pipeline for nanocomposites and nanofibers. Market impact lies in improved innovation velocity and material scalability for industrial applications, particularly supportive of digital infrastructure, quantum computing, and sustainability engineering.

Electrification and Energy Storage Transformation

Nanomaterials play a critical role in global electrification initiatives linked to the EV transition and renewables integration. As per International Energy Agency (IEA) data from 2024, global EV sales crossed 14 million units, indicating robust demand for nanoscale electrode materials that offer superior charge density and durability.

Metal oxide nanomaterials enhance battery life cycles by up to 50% and lower degradation rates. Countries such as China and the U.S. have increased nanomaterial-based cathode capacity under their respective energy transition programs. This driver exemplifies the crossover between materials innovation and energy policy, directing nanomaterials toward scalable deployment across mobility and grid resilience applications.

Restraint - Cost and Scalability Challenges in Mass Production

Commercial adoption faces persistent challenges related to high production costs, limited synthesis scalability, and energy-intensive fabrication. Nanoparticle synthesis processes such as chemical vapor deposition and atomic layer deposition carry cost structures 3-5 times higher than traditional coatings or composites. Supply chain inefficiencies in rare raw materials such as titanium dioxide and carbon precursors accentuate production constraints, limiting mass-market access.

Regulatory Compliance and Environmental Risk Mitigation

Strict safety and environmental standards imposed by agencies like the European Chemicals Agency (ECHA) and the U.S. Environmental Protection Agency (EPA) create entry barriers for manufacturers. Toxicity concerns associated with nanoclays and carbon nanotubes necessitate advanced waste management and occupational safety protocols. Compliance costs have increased operating expenditures by 18-22% across mid-scale producers since 2023, restraining high-volume commercialization.

Opportunity- Integration with Semiconductor and Quantum Computing Technologies

Nanomaterials are positioned to enable breakthroughs in advanced semiconductor fabrication and quantum technology. Governments, such as through the U.S. CHIPS and Science Act, have pledged over US$ 52 billion toward reshoring semiconductor manufacturing, creating new procurement opportunities for nanoscale dielectrics, wafer diffusion layers, and conductive oxides.

By aligning with AI and quantum computing fabric architectures, nanomaterials can optimise transistor performance and thermal conductivity. The opportunity landscape includes localised supply chain partnerships, advanced material co-development, and digitized quality assurance platforms to integrate nanoscale components efficiently.

Sustainability-Oriented Manufacturing and Green Innovation

The global environmental agenda favoring decarbonization and circular materials has opened strategic adoption avenues for nanomaterials in renewable power, water purification, and emission-control applications.

Metal oxide nanocatalysts and carbon nanocomposites are instrumental in driving low-emission industrial systems. The United Nations Industrial Development Organisation (UNIDO) highlights sustainable nanotechnology as a key pillar for eco-industrial parks, with 40 Plus facilities in Asia and Europe adopting nano-enabled waste recovery technologies as of 2024. This presents a significant commercialization pathway for companies focusing on recyclability and energy-efficient nano-manufacturing.

Healthcare and Pharmaceutical Material Advancements

Medical nanomaterials continue to shape diagnostic imaging, targeted drug delivery, and tissue engineering. According to OECD Health Data 2024, global healthcare expenditure surpassed 9.8% of total GDP, with nanomedicine accounting for nearly US$ 200 billion in R&D value globally.

Carbon-based nanoparticles enable precise molecular diagnostics, while metal oxide nanostructures enhance antiviral coatings and implant performance. As policy frameworks prioritise healthcare innovation, nanomaterials offer actionable integration potential across life sciences and biotechnology markets.

Category-wise Analysis

Product Type Segment Insights

Metal Oxides (30%) dominate the market due to extensive utilization in coatings, cosmetics, and electronic devices. Their high conductivity, thermal stability, and catalytic efficiency make them indispensable in semiconductor wafer processing, lithium-ion battery electrodes, and anti-corrosion surfaces. The U.S. and Japan lead in titanium dioxide and zinc oxide-based nanomaterial production, supported by advanced supply chains and industrial R&D collaborations.

Carbon Nanotubes (CNTs) represent the fastest growing segment, accounting for about 12% of demand. Their exceptional mechanical strength and electrical conductivity drive adoption in energy storage, flexible electronics, and electric vehicle components.

The IEA’s EV Material Outlook 2025 emphasizes CNT integration for boosting electrode surface area and minimizing heat generation, marking a strategic material upgrade for next-gen batteries and composite structures.

Material Type Insights

Carbon-Based Nanomaterials (32%) lead globally, driven by strong uptake in electronics and structural composites. Graphene, carbon black, and CNTs are central to performance advancements in displays, sensors, and conductive polymers. Benchmark studies by NIST indicate that carbon-based materials achieve 3-4× higher tensile strength and 60% improved electrical feedback consistency, underscoring industrial scalability.

Metal-Based Nanomaterials are the fastest-growing due to widespread application in catalysts and nanoparticle dispersion technologies. These materials enhance chemical processing efficiency and surface reactivity, with notable adoption in automotive catalytic converters and hydrogen electrolyzers.

Governments in the Asia Pacific are funding localized nanoparticle research facilities for cobalt, nickel, and silver composites, reflecting an upward technological trajectory in precision manufacturing.

Industry Insights

Electronics & Electricals (25.6%) constitute the leading end-use sector. Nanomaterials are critical in semiconductor interconnects, photonic devices, sensors, and conductive systems. According to 2024 data from the Semiconductor Industry Association, surging global chip demand corresponded to expanded consumption of carbon nanotubes and metal oxides for transistor architecture and dielectric optimization.

These attributes reinforce nanomaterials’ indispensable role in miniaturization and functional efficiency.

Energy & Power represents the fastest-growing industry, led by energy storage, supercapacitors, solar photovoltaics, and EV batteries. Nanomaterials impart superior charge transfer capacity, reduced degradation, and high energy density.

Government energy programs such as China’s 13th Five-Year Plan and U.S. DOE Battery Materials Initiative support production-scale nanomaterial integration in battery chemistry and hydrogen storage. This sector drives long-term strategic adoption across clean energy value chains.

Regional Insights and Trends

North America Nanomaterials Market Trends

North America holds a market share of around 20% driven by a strong nanomaterials R&D base, supported by mature academic-industrial collaboration networks.

The U.S. dominates nanomaterial patents with >42% global share, with applications in semiconductors, defense composites, and advanced coatings. Federal funding under the CHIPS and Science Act (2022 - 2025) has redefined industrial nanotechnology priorities, directing investments toward domestic material supply chains and nano-enabled manufacturing. Canada’s National Research Council advances polymer nanocomposite developments for aerospace and cleantech industries.

Regulatory oversight from the EPA ensures compliance with nano-toxicity standards. Competitive differentiation lies in technological leadership and intellectual property concentration within major innovation clusters like Silicon Valley and Boston. Investment momentum is visible in EV battery nanomaterials and biosensor scale-up initiatives.

East Asia Nanomaterials Market Trends

Europe holds around 18% of the market share in 2025 and benefits from strong nanomaterial integration across automotive, aerospace, energy, and healthcare sectors. According to the European Nanotechnology Trade Report (2024), Germany, France, and the U.K. jointly account for nearly 70% of regional nanomaterial R&D expenditure.

Germany’s advanced manufacturing base channels nanomaterials into precision coatings and automotive applications, while France invests heavily in graphene-powered renewable systems. EU regulations under REACH ensure material safety and standardization, fostering transparency and sustainability.

Recent funding under Horizon Europe has enabled large pilot plants for ceramic and hybrid nanomaterials. Environment-oriented innovation in the region highlights the long-term shift toward carbon-neutral industrial production. Competitive dynamics remain moderately consolidated, supported by corporate sustainability frameworks and advanced lab-to-market commercialisation pathways.

East Asia Nanomaterials Market Trends

East Asia accounts for approximately 43% of global nanomaterial production and consumption, supported by government-backed industrial policies and a strong foundation in advanced manufacturing and technological capabilities. This region’s dominance is reinforced by well-established supply chains, significant investments in R&D, and leadership in key application sectors such as electronics, batteries, and automotive components.

China hosts over 40% of global nanomaterial capacity, focusing on carbon-based nanostructures and oxides for EVs and solar panels. Japan leads in precision nanoelectronics and ultra-thin coatings, supported by more than ¥3.9 trillion in annual R&D expenditure across the automotive and electronics sectors in 2023.

South Korea aligns its industrial diversification strategy with semiconductor materials innovation, boosting CNT and graphene adoption for battery and display production. Collaborative frameworks like China’s National Nanotechnology Initiative and South Korea’s

Nano-Convergence Platform reinforces regional dominance. Market structure is vertically integrated with strong supply chain localisation, ensuring high scalability for electronics and clean energy subsectors.

Competitive Landscape

The global nanomaterials market reflects an oligopolistic structure, characterised by a concentration of leading multinational manufacturers and specialised niche producers.

Key players such as Cabot Corporation, LG Chem, Evonik Industries, OCSiAl, Strem Chemicals, and American Elements dominate global supply through integrated production networks, patented technologies, and diversified product portfolios covering carbon nanotubes, metal oxides, and hybrid nanocomposites. These companies maintain strong vertical integration and extensive investment in R&D to ensure consistent quality, scalability, and regulatory compliance.

Competitive intensity is sustained by innovation-led differentiation, long-term supply contracts with semiconductor and energy industries, and expansion into high-value markets such as electronics, batteries, and biomedical applications.

Key Industry Developments:

- In May 2025, Researchers from Shinshu University, Japan, developed a low-cost multifunctional nanocomposite by embedding bimetallic and trimetallic molybdates into doped hollow carbon nanofibers. The material demonstrated high energy storage capacity for supercapacitors and effective catalytic activity for degrading industrial pollutants, offering a scalable and sustainable solution for both energy and environmental applications. This innovation highlights the growing role of nanomaterials in addressing global energy and pollution challenges.

- In August 2024, Evonik, in collaboration with KNAUER, enhanced its capabilities in scaling up lipid nanoparticle (LNP) formulations for mRNA and gene therapies. This advancement enables faster pre-clinical development, more efficient transition from small-scale prototypes to production-scale formulations and supports the growing demand for nucleic acid-based therapeutics, strengthening Evonik’s position in the nanomaterials market.

Companies Covered in Nanomaterials Market

- Strem Chemicals, Inc.

- American Elements

- Cabot Corporation

- LG Chem

- OCSiAl

- Evonik Industries

- Arkema

- US Research Nanomaterials, Inc.

- Nanocomposix, Inc.

- Nanoshel LLC

- SkySpring Nanomaterials, Inc.

- Nanophase Technologies Corporation

- Cytodiagnostics, Inc.

- Quantum Materials Corp.

- Inframat Advanced Materials.

Frequently Asked Questions

The global Nanomaterials market is projected to be valued at US$ 22.1 Bn in 2025.

The Metal Oxide segment is expected to hold around 30% market share in 2025, driven by its wide use in electronics, coatings, catalysts, bulk of current demand.

The market is poised to witness a CAGR of 17.8% from 2025 to 2032.

Rising adoption of nanomaterials across electronics, healthcare, energy storage, and industrial applications, coupled with government R&D funding and policy support, is accelerating innovation, efficiency, and large-scale commercialisation.

Expanding use in advanced semiconductor fabrication, quantum computing, sustainable manufacturing, renewable energy, and healthcare applications offers significant growth potential for nanomaterials.

The key market players in the global Nanomaterials market include key market players in the global Nanomaterials market include Strem Chemicals, Inc., American Elements, Cabot Corporation, LG Chem, OCSiAl, and Evonik Industries, representing the leading companies driving innovation and market growth.