- Advanced Materials

- Steep Slope Roofing Materials Market

Steep Slope Roofing Materials Market Size, Share, and Growth Forecast 2026 - 2033

Steep Slope Roofing Materials Market by Material Type (Asphalt Shingles, Metal Roofing, Wood Shingles, Clay Tiles, Slate, Wood, Others), End-user (Residential, Commercial, Institutional, Industrial), and Regional Analysis, 2026 - 2033

Steep Slope Roofing Materials Market Size and Trend Analysis

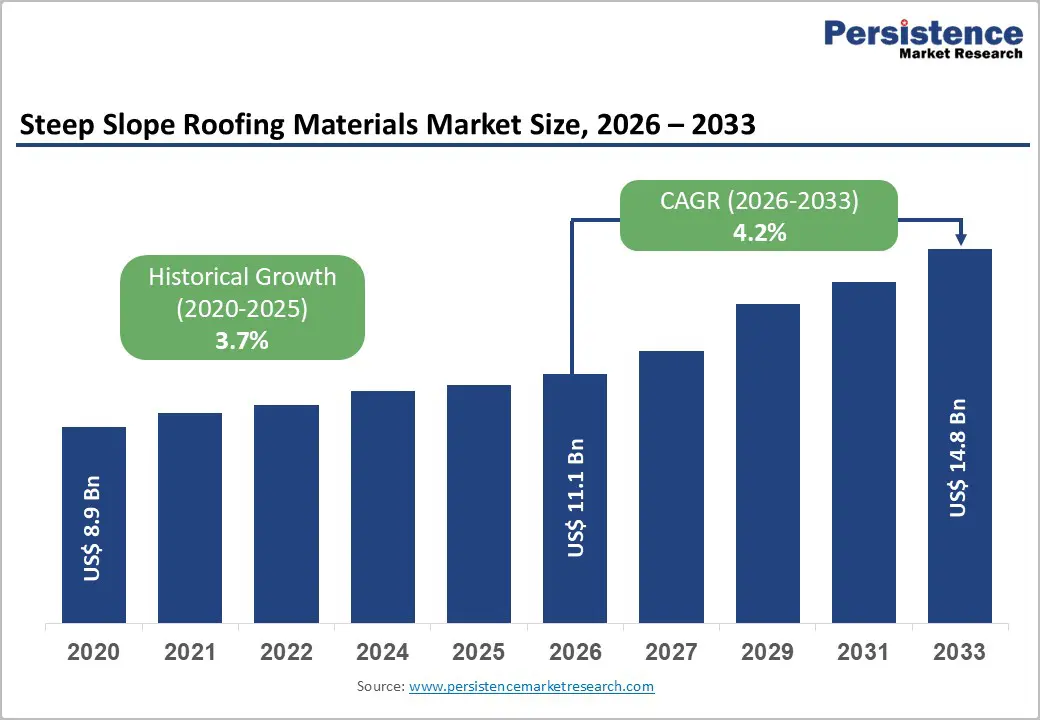

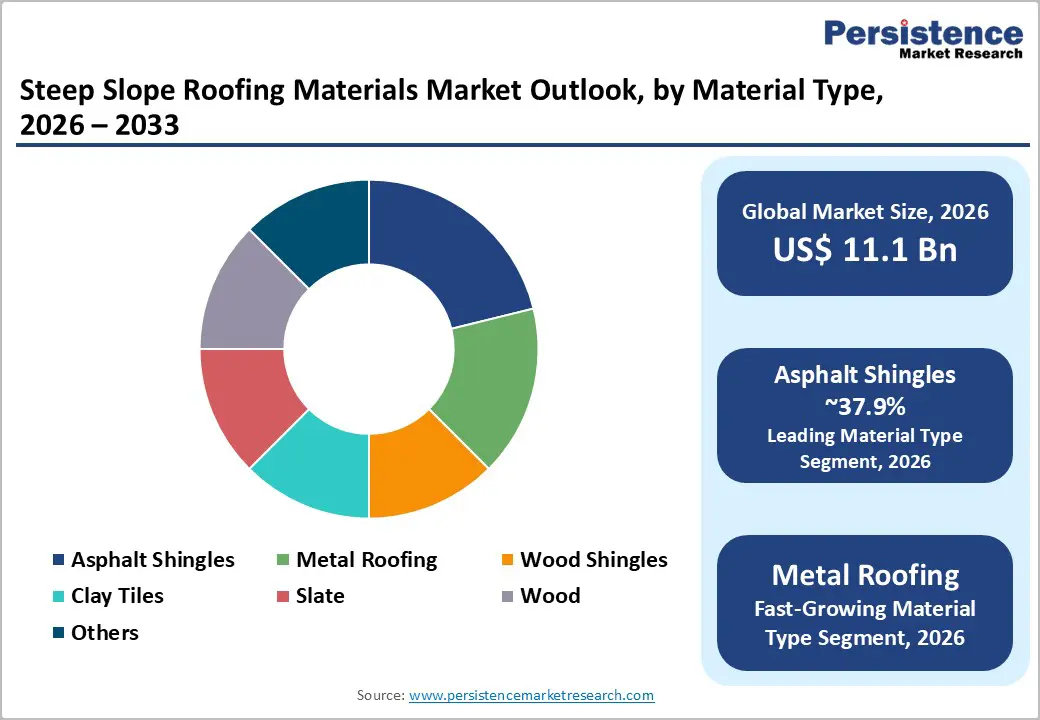

The global steep slope roofing materials market size is expected to be valued at US$ 11.1 billion in 2026 and projected to reach US$ 14.8 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

Market growth is driven by rising residential construction, increasing renovation activities, and growing preference for durable, weather-resistant roofing systems. Expanding urbanization in emerging economies and stricter building codes emphasizing energy efficiency and sustainability further support demand. Residential roofing remains the dominant application, supported by storm damage repairs and re-roofing cycles. Additionally, advancements such as cool and reflective roofing materials are improving thermal performance and reducing building energy consumption.

Key Market Highlights

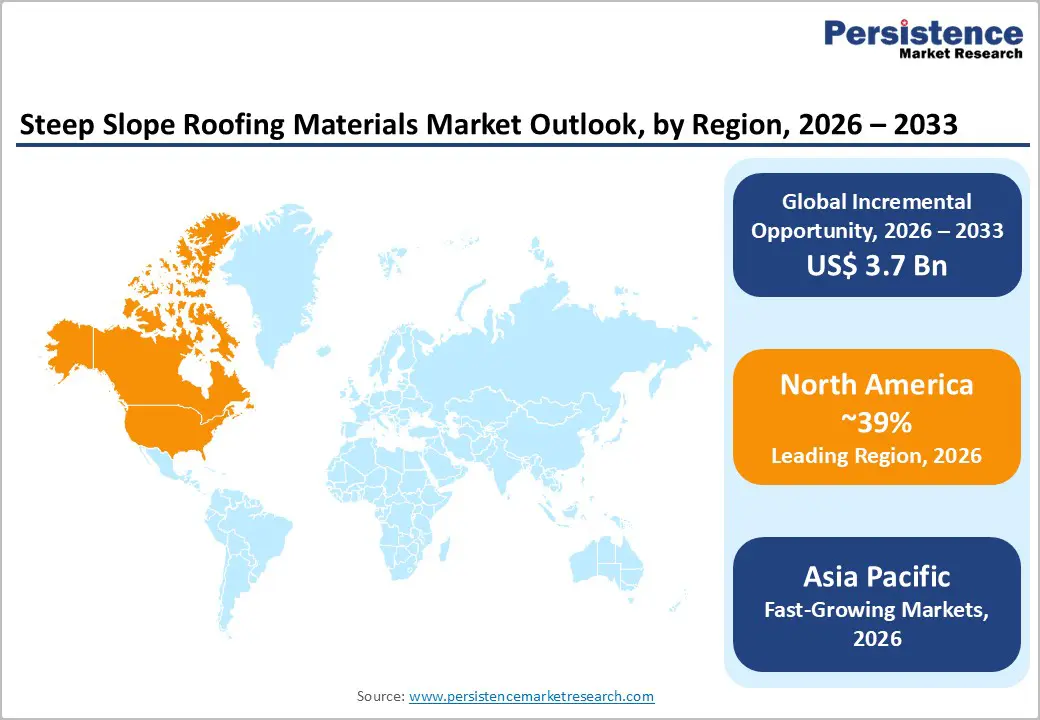

- Leading Region: North America leads the market with 39.3% share in 2025, supported by strong residential roofing demand, renovation activity, and energy-efficiency regulations.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization, housing expansion, and infrastructure development across major emerging economies.

- Leading Material Category: Asphalt shingles dominate the material landscape with a 37.9% share in 2025, owing to cost-effectiveness, ease of installation, and widespread residential use.

- Fastest-Growing Material Category: Metal roofing is the fastest-growing material segment, supported by superior durability, weather resistance, and alignment with sustainable building practices.

- Key Opportunity Area: Metal roofing adoption in institutional and public buildings presents a major opportunity, driven by solar integration mandates and stricter performance regulations.

| Global Market Attributes | Key Insights |

|---|---|

| Steep Slope Roofing Materials Size (2026E) | US$ 11.1 billion |

| Market Value Forecast (2033F) | US$ 14.8 billion |

| Projected Growth CAGR (2026 - 2033) | 4.2% |

| Historical Market Growth (2020 - 2025) | 3.7% |

Market Dynamics

Drivers - Increasing Residential Construction and Renovation Activity

Rising residential construction across both developed and emerging economies continues to strongly support demand for steep slope roofing materials. New housing developments and renovation projects consistently favor steep-slope roofs for their superior water drainage, durability, and visual appeal. Expanding suburban housing, replacement of aging roofs, and weather-related damage repairs sustain steady material demand across single-family and multi-family residential segments.

This trend remains reinforced by homeowner preference for long-lasting and impact-resistant roofing solutions that can withstand extreme weather conditions. Steep slope roofing materials offer extended service life and predictable replacement cycles, encouraging re-roofing investments. As residential construction remains a priority to address housing shortages, manufacturers benefit from recurring demand driven by both new installations and periodic roof replacements.

Rising Focus on Energy-Efficient and Sustainable Roofing Solutions

Increasing emphasis on energy efficiency and sustainability is accelerating the adoption of advanced steep slope roofing materials. Reflective coatings, cool asphalt shingles, and metal roofing systems help reduce heat absorption, improve indoor comfort, and lower cooling energy consumption. These benefits align with global efforts to reduce building-related emissions and improve long-term energy performance.

Supportive regulations, evolving building codes, and incentive programs further encourage the use of energy-efficient roofing solutions. Innovations integrating solar functionality and recyclable materials are gaining attention, combining environmental benefits with cost savings over the roof’s lifecycle. As sustainability becomes a key decision factor, demand for high-performance, energy-efficient steep slope roofing materials continues to expand steadily.

Restraints - Skilled Labor Shortages and Workforce Constraints

A sustained shortage of skilled roofing installers remains a key restraint for the steep slope roofing materials market. Aging workforces, declining vocational training enrollment, and limited entry of younger workers have reduced the availability of experienced labor. This shortage is particularly challenging for steep-slope installations, which require higher technical skill, safety expertise, and longer installation times compared to flat roofing systems.

Rising labor scarcity has also driven up installation costs, increasing overall project expenses and extending construction timelines. Contractors face capacity limitations, especially for complex or premium roofing systems, which can discourage adoption despite strong material demand. As labor availability directly impacts installation efficiency, workforce constraints continue to pressure contractor margins and slow market expansion.

Fluctuating Raw Material Prices and Cost Volatility

Volatility in raw material prices poses a significant restraint on the steep slope roofing materials market. Key inputs such as asphalt, steel, aluminum, and copper are subject to supply chain disruptions, geopolitical tensions, and energy price fluctuations. These factors create uncertainty in production costs, particularly for asphalt shingles and metal roofing products widely used in residential construction.

Frequent cost fluctuations limit pricing stability and complicate long-term planning for manufacturers and contractors. During economic slowdowns, rising material costs are harder to pass on to customers, leading to margin compression or deferred projects. As a result, unpredictable raw material pricing can suppress demand and restrict profitability across the value chain.

Opportunity - Advancements in Durable and High-Performance Metal Roofing

Technological advancements in metal roofing present strong growth opportunities within the steep slope roofing materials market. Metal roofs are gaining preference due to their long service life, superior resistance to fire and extreme weather, and lightweight properties that simplify installation. Rapid urban development and increasing construction activity are encouraging the adoption of recyclable and energy-efficient metal roofing systems in both new builds and retrofit projects.

Innovations in protective coatings and surface treatments are improving corrosion resistance and thermal performance, further expanding application potential. Growing emphasis on resilient and sustainable buildings supports increased metal roofing adoption, especially in regions prioritizing energy efficiency upgrades. Manufacturers investing in automated production and advanced material technologies are well-positioned to capture expanding demand.

Expansion of Institutional and Industrial Roofing Applications

Rising construction of institutional and industrial facilities offers significant opportunities for steep slope roofing material suppliers. Public buildings, educational institutions, and manufacturing facilities increasingly require durable roofing systems that comply with strict safety, energy efficiency, and sustainability regulations. Steep slope roofs using metal, slate, and advanced composite materials meet these requirements while providing long-term performance and reduced maintenance.

Infrastructure development and industrial expansion in emerging economies further support demand growth. Green building initiatives and evolving construction standards are accelerating the adoption of resilient roofing solutions across non-residential segments. As investment in institutional and industrial infrastructure increases, suppliers can unlock new revenue streams beyond traditional residential markets.

Category-wise Analysis

Material Type Insights

Asphalt shingles represent the leading material type in the steep slope roofing materials market, accounting for approximately 37.9% share in 2025. Their dominance is supported by cost-effectiveness, wide design availability, and ease of installation, making them the preferred choice for residential steep-slope roofs. Strong contractor familiarity, steady replacement demand, and compatibility with layered and laminated designs further reinforce their widespread adoption across mature housing markets.

Metal roofing is emerging as the fastest-growing material category due to its superior durability, resistance to extreme weather, and long service life. Growing awareness of lifecycle cost benefits, lightweight installation advantages, and suitability for energy-efficient and resilient building designs is accelerating adoption. Increasing use in premium residential and non-residential projects positions metal roofing as a key growth driver within the material landscape.

End-user Insights

The residential segment dominates end-use, holding around 59% share in 2025, driven by consistent new housing construction and predictable re-roofing cycles. High reliance on steep-slope designs for water drainage and storm resistance supports strong material demand. Aging housing stock, renovation activity, and preference for asphalt-based systems further strengthen residential dominance across developed and emerging regions.

Institutional and industrial applications are witnessing the fastest growth as building owners prioritize long-lasting, code-compliant roofing systems. Public infrastructure expansion, manufacturing facility development, and stricter performance standards are encouraging the adoption of durable steep-slope solutions. These segments increasingly favor materials that offer low maintenance, safety compliance, and sustainability benefits, expanding opportunities beyond traditional residential demand.

Regional Insights

North America Steep Slope Roofing Materials Market Trends

North America holds a significant share of the global steep slope roofing materials market, accounting for 39.3% of total demand. The region is heavily driven by residential roofing activity, where steep-slope designs are preferred for durability and effective water drainage. Asphalt shingles remain widely used due to affordability and ease of installation, supporting strong replacement demand across the aging housing stock.

Growth is reinforced by rising renovation activity, storm-related roof replacements, and increased focus on energy-efficient roofing solutions. Regulatory support for cool roofs, fortified roofing standards in hurricane-prone areas, and tax incentives for energy-efficient upgrades continue to strengthen market fundamentals across the region.

Europe Steep Slope Roofing Materials Market Trends

Europe’s steep slope roofing materials market is shaped by sustainability-focused regulations and strict building performance standards. The region is projected to grow at a 4.7% CAGR, supported by regulatory mandates encouraging energy efficiency, solar integration, and green roofing solutions across residential and non-residential buildings.

Countries such as Germany, France, the U.K., and Spain are driving the adoption of durable materials like metal, clay, and slate roofing. Harmonized EU policies and national climate regulations continue to promote long-lasting, low-maintenance roofing systems, supporting steady regional market expansion.

Asia Pacific Steep Slope Roofing Materials Market Trends

Asia Pacific represents a major demand hub, accounting for 36.8% of the global steep slope roofing materials market. Rapid urbanization, population growth, and expanding residential construction across China, India, Japan, and Southeast Asia underpin strong market momentum. Steep-slope roofs are increasingly favored for resilience and cost efficiency in varied climatic conditions.

The region is also witnessing rising adoption of metal roofing due to its lightweight structure and durability. Government-led housing initiatives, infrastructure expansion, and green building policies continue to accelerate demand, positioning the Asia Pacific as a critical growth engine for the global market.

Competitive Landscape

The steep slope roofing materials market is moderately consolidated, with leading participants commanding strong positions through established brands, extensive distribution networks, and broad product portfolios. Market leaders focus on expanding production capacity and strengthening supply chains to meet consistent residential demand. Product differentiation is achieved through enhanced durability, weather resistance, and compatibility with energy-efficient roofing systems, allowing companies to maintain competitive advantages in mature markets.

Competitive strategies increasingly emphasize innovation, sustainability, and operational efficiency. Investments in advanced materials, impact-resistant designs, and integrated roofing solutions support long-term positioning. In parallel, companies are adopting regional manufacturing, strategic acquisitions, and digital tools to improve installation efficiency, address labor constraints, and enhance contractor engagement across fragmented local markets.

Key Developments:

- In February 2025, Owens Corning announced the construction of a new shingle manufacturing facility in the southeastern U.S. The plant is expected to significantly expand laminate shingle production capacity, strengthen regional supply availability, and support faster delivery timelines to meet growing residential roofing demand.

- In January 2025, GAF Materials LLC entered a strategic partnership with the Insurance Institute for Business & Home Safety (IBHS) to promote FORTIFIED roofing standards. The collaboration focuses on improving roof resilience against extreme weather events and increasing the adoption of impact-resistant steep-slope roofing systems.

- In June 2024, Peak Roofing acquired Action Roofing to expand its service footprint and operational efficiency. The acquisition enhances installation capabilities, improves workforce utilization, and strengthens the company’s position in residential and commercial steep-slope roofing projects.

Companies Covered in Steep Slope Roofing Materials Market

- Owens Corning

- GAF Materials Corporation

- CertainTeed Corporation

- IKO Industries Ltd.

- Tamko Building Products, Inc.

- Atlas Roofing Corporation

- Malarkey Roofing Products

- PABCO Roofing Products

- Carlisle Companies Incorporated

- Boral Roofing LLC

- Eagle Roofing Products

- Polyglass U.S.A., Inc.

- Siplast, Inc.

- Icopal A/S / BMI Group

- Everest Industries Limited

Frequently Asked Questions

The global steep slope roofing materials market is expected to reach US$ 11.1 billion in 2026.

Rising residential construction and renovation activity drive demand, with the residential segment holding 59% share in 2025.

North America leads the market with a 39.3% share in 2025, supported by strong U.S. housing demand and energy regulations.

Expansion of metal roofing in institutional and public buildings offers strong opportunities due to solar integration and sustainability mandates.

Leaders include Owens Corning, GAF Materials Corporation, CertainTeed Corporation, and IKO Industries Ltd., focusing on innovations.