- Electrical Equipment & Services

- Low Voltage Motor Control Center Market

Low Voltage Motor Control Center Market Size, Share, and Growth Forecast 2026 - 2033

Low Voltage Motor Control Center Market by Product Type (Conventional MCC, Intelligent MCC), by Component (Busbars, Circuit Breakers & Fuses, Overload Relays, Variable Speed Drives, Soft Starters, Others), End-user (Oil and Gas, Metal and Mining, Power Generation, Automotive and Transportation, Chemicals and Petrochemicals, Water and Wastewater, Food and Beverages, Others), and Regional Analysis, 2026 - 2033

Low Voltage Motor Control Center Market Size and Trend Analysis

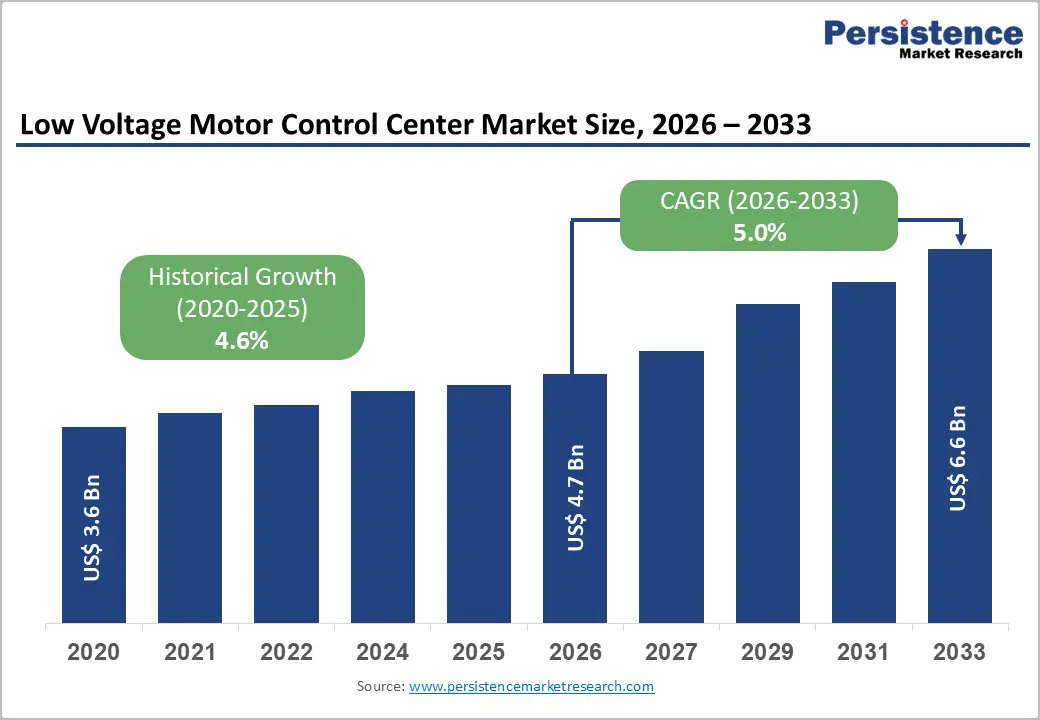

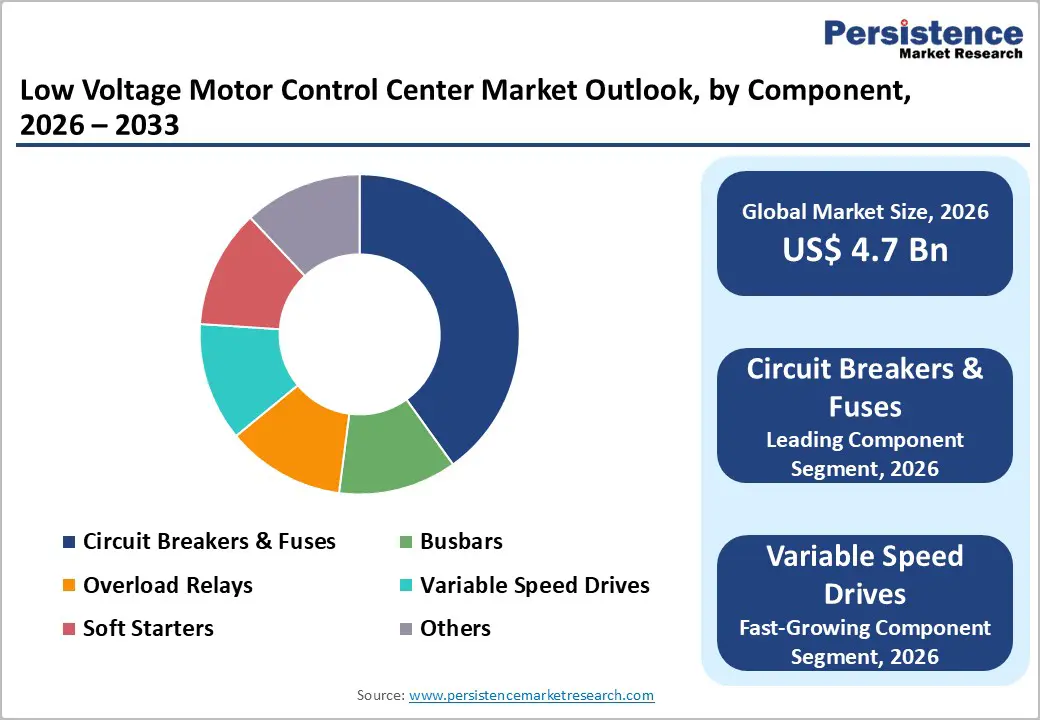

The global low voltage motor control center market size is expected to be valued at US$ 4.7 billion in 2026 and projected to reach US$ 6.6 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033. The market expansion is primarily driven by the growing demand for centralized motor control and protection systems across industrial facilities, combined with the accelerating adoption of intelligent automation technologies enabling real-time monitoring and predictive maintenance capabilities.

The global industrial automation transition is fundamentally reshaping motor control infrastructure, with organizations increasingly recognizing that advanced motor control centers provide substantial operational efficiency improvements, enhanced worker safety, and reduced energy consumption. Growing emphasis on predictive maintenance technologies, IoT integration, and smart grid solutions is substantially elevating demand for intelligent MCCs incorporating advanced diagnostic capabilities and remote monitoring features across diverse industrial sectors.

Key Industry Highlights:

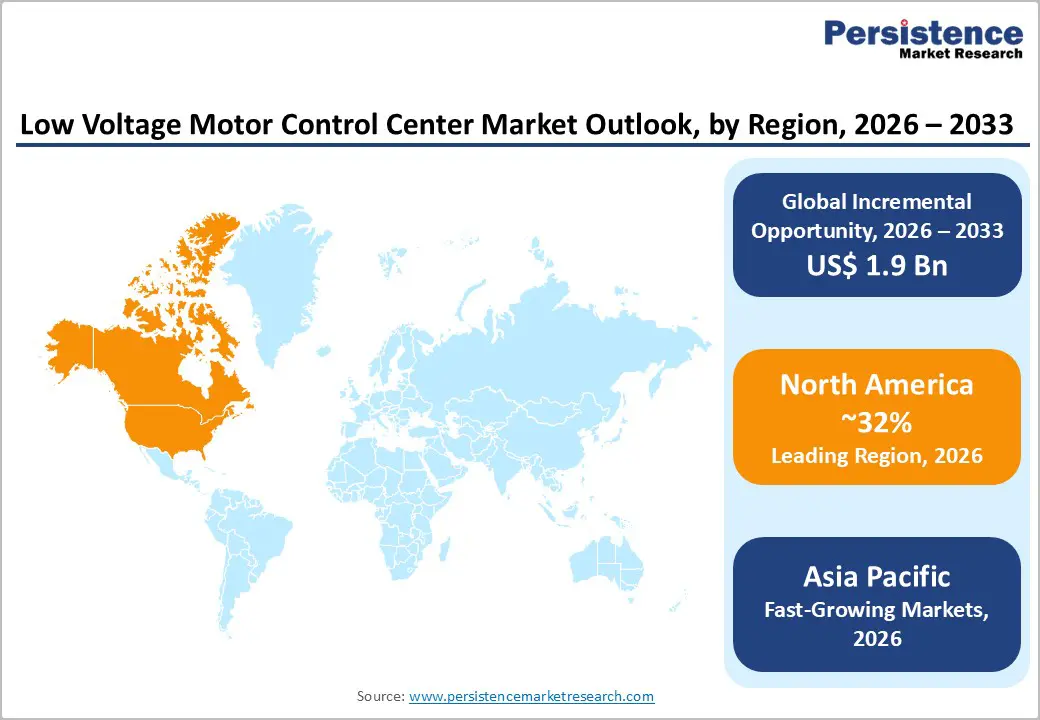

- Leading Region: North America leads the global Low Voltage Motor Control Center Market with approximately 32% share in 2025, supported by mature industrial infrastructure, substantial facility modernization investments, and emphasis on worker safety and regulatory compliance, driving MCC adoption.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expected to post approximately 6.8% CAGR through 2032, driven by rapid industrialization, expanding manufacturing capacity, and adoption of automation technologies across emerging economies.

- Dominant Segment from Product Type: Conventional MCC dominates with roughly 62% share in 2025, reflecting established reliability, proven performance across industrial applications, and cost advantages supporting widespread adoption.

- Fastest Growing Segment from Component: Variable Speed Drives is the fastest-growing segment, with an estimated 8.1% CAGR through 2033, fueled by emphasis on energy efficiency and integration with advanced automation systems requiring variable frequency drive technology.

- Key Market Opportunity: Intelligent MCC development for digital industrial ecosystems and Industry 4.0 implementation offers significant opportunity for establishing competitive differentiation and premium market positioning through advanced monitoring and predictive maintenance capabilities.

| Key Insights | Details |

|---|---|

|

Low Voltage Motor Control Center Market Size (2026E) |

US$ 4.7 billion |

|

Market Value Forecast (2033F) |

US$ 6.6 billion |

|

Projected Growth CAGR (2026-2033) |

5.0% |

|

Historical Market Growth (2020-2025) |

4.6% |

Market Dynamics

Drivers - Rapid Industrial Automation and Growing Demand for Centralized Motor Control Systems

Industrial automation expansion across manufacturing, oil and gas, chemical processing, and power generation sectors is driving sustained demand for advanced motor control centers enabling centralized management of complex electrical systems. Modern industrial operations require sophisticated control systems capable of managing multiple motors across diverse production processes while ensuring safety, efficiency, and reliability.

Global manufacturing investment in automation technologies is accelerating, with factories deploying increasingly complex machinery requiring comprehensive motor control solutions. The Industrial Internet of Things (IIoT) adoption is fundamentally transforming motor control requirements, with operators demanding real-time visibility into motor performance, predictive insights, and remote management capabilities. MCCs integrating with Building Management Systems (BMS) enable centralized monitoring and control of facility motors, translating to optimized energy consumption and improved operational efficiency.

Integration of Energy-Efficient Technologies and IoT-Enabled Smart Monitoring Capabilities

The rapid advancement of energy-efficient motor control technologies, including variable frequency drives (VFDs), soft starters, and intelligent monitoring systems, represents a transformational growth driver for the motor control center market. Modern MCCs incorporating VFDs enable precise motor speed control, reducing energy consumption by adjusting motor operation to match actual load requirements rather than operating continuously at full capacity. Intelligent MCCs equipped with advanced sensors, communication modules, and analytics capabilities can reduce energy costs by up to 20% through optimized motor operation and predictive maintenance scheduling.

The integration of IoT connectivity, AI-powered analytics, and cloud-enabled monitoring systems enables real-time motor performance diagnostics, early fault detection, and data-driven maintenance planning supporting reduced downtime and extended equipment lifespan. Manufacturers are developing modular MCC designs enabling rapid expansion or reconfiguration without significant operational disruption, supporting flexibility for evolving industrial requirements. The global emphasis on sustainability and carbon footprint reduction is accelerating adoption of energy-efficient motor control solutions, with companies increasingly prioritizing technologies supporting operational sustainability and cost optimization objectives.

Restraint - High Capital Investment and Complex System Implementation Requirements

Low voltage motor control center deployment requires substantial capital investment for manufacturing infrastructure, advanced control systems, and skilled technical expertise, creating barriers to entry for smaller manufacturers and constraining market accessibility. Integrated intelligent MCC systems incorporating advanced sensors, communication modules, and analytical capabilities require significant upfront capital expenditures, with complete system deployment often exceeding millions of dollars. The complexity of system integration, compatibility testing, and regulatory compliance necessitates specialized technical expertise and extended implementation timelines.

Smaller and medium-sized enterprises struggle to justify substantial investments in advanced MCCs due to limited budgets, uncertain return on investment timelines, and operational disruption risks during installation and deployment. The requirement for highly skilled technicians to install, program, and maintain sophisticated MCC systems creates labor constraints, particularly in developing economies with limited technical workforce availability.

Raw Material Price Volatility and Supply Chain Complexity

Motor control center manufacturing depends on diverse raw materials including copper windings, insulation compounds, semiconductors, and electronic components subject to significant price volatility and intermittent supply constraints. Copper prices have demonstrated substantial fluctuations, ranging across significant price bands, affecting production costs and manufacturer profitability throughout the supply chain.

Semiconductor component shortages and supply chain disruptions have elevated procurement complexity and extended lead times for MCC manufacturers. Advanced intelligent MCCs incorporating specialized electronic components face supply constraints exacerbated by geopolitical trade tensions and manufacturing capacity limitations. Manufacturers must maintain substantial raw material inventories and working capital reserves to manage supply uncertainties, elevating operational costs and financial risk exposure for smaller market participants.

Opportunity - Development of Intelligent MCC Solutions for Industrial Digitalization and Industry 4.0 Implementation

Significant growth opportunities exist for manufacturers developing advanced intelligent motor control centers optimized for digital industrial ecosystems and Industry 4.0 implementation across diverse manufacturing environments. The global transition toward smart factories, connected production systems, and data-driven operations creates substantial opportunities for MCC manufacturers developing integrated solutions with advanced monitoring, analytics, and automation capabilities. According to industry analysis, intelligent MCCs incorporating communication protocols, remote diagnostics, and predictive maintenance features are expanding at the fastest CAGR during forecast periods, driven by increasing recognition of digital technology’s transformational potential.

Manufacturers developing MCCs with seamless integration capabilities for SCADA systems, PLCs, and enterprise resource planning (ERP) platforms can establish competitive advantages and capture market share among industrial operators pursuing comprehensive digital transformation initiatives. Integration of artificial intelligence and machine learning capabilities supporting predictive maintenance scheduling, anomaly detection, and operational optimization can differentiate products and support premium pricing across diverse industrial segments.

Expansion in Oil and Gas, Mining, and Critical Infrastructure Applications Requiring Advanced Safety Features

The oil and gas sector, metal and mining operations, and critical infrastructure applications require advanced motor control solutions incorporating enhanced safety features, arc flash protection, and operational redundancy supporting mission-critical operations. According to Rockwell Automation analysis, arc flash hazards in oil and gas operations require specialized MCC designs incorporating arc-resistant construction, isolated compartments, and pressure-venting systems protecting personnel from catastrophic fault conditions. The emphasis on worker safety, regulatory compliance with evolving electrical safety standards, and operational continuity in hazardous environments creates sustained demand for specialized MCC solutions with advanced protection capabilities.

Manufacturers developing customized control centers optimized for extreme operating conditions, high-vibration environments, and distributed operations in remote locations can establish strong market positions serving these specialized segments. The increasing focus on remote monitoring capabilities and automated fault detection enables safe equipment operation without requiring personnel to work near energized equipment, supporting significant operational safety improvements. Government regulatory initiatives emphasizing occupational safety and machine protection compliance are accelerating adoption of advanced MCC solutions across energy, mining, and industrial sectors.

Category-wise Analysis

Product Type Insights

Within product type category, conventional MCC dominates the market with approximately 62% share in 2025, reflecting established technology adoption, proven reliability across decades of industrial application, and substantial cost advantages compared to advanced intelligent systems. Conventional MCCs provide fundamental motor control and protection capabilities meeting requirements across diverse industrial applications.

The robust construction and established reliability of conventional designs support their continued dominance among cost-conscious industrial operators prioritizing basic motor control and protection functionality. Conventional MCCs remain essential infrastructure across smaller industrial facilities, regional operations, and cost-constrained environments where sophisticated intelligent features are not critical operational requirements.

Component Insights

By component, circuit breakers & fuses represents the leading segment, commanding approximately 35% market share in 2025, reflecting their critical importance as fundamental protective devices preventing motor damage from overcurrents, short circuits, and fault conditions. Circuit breakers and fuses are essential components within every motor control center, providing rapid fault isolation and equipment protection across diverse industrial applications. The universal requirement for protective devices across all MCC installations ensures sustained demand for advanced circuit breaker technologies incorporating enhanced breaking capacity and rapid response characteristics.

The fastest-growing component segment is Variable Speed Drives, expected to expand at approximately 8.1% CAGR through 2033, driven by accelerating adoption of variable frequency drive technology supporting energy efficiency objectives, precise motor speed control, and integration with advanced automation systems enabling optimized industrial processes and reduced energy consumption.

End-user Insights

By end-user, the Oil and Gas segment emerges as the leading contributor to the global low voltage motor control center market, accounting for the largest share in 2025 due to its intensive motor-driven operations and stringent reliability requirements. Oil and gas facilities rely heavily on MCCs for controlling pumps, compressors, conveyors, and auxiliary systems across upstream, midstream, and downstream operations.

Continuous process environments, hazardous operating conditions, and high downtime costs necessitate robust motor protection, fault isolation, and high system availability. Low voltage MCCs play a critical role in ensuring operational continuity, electrical safety, and compliance with stringent industry standards. Ongoing investments in refinery upgrades, pipeline infrastructure, and digitalized process control systems further support sustained demand from this segment.

Regional Insights

North America Low Voltage Motor Control Center Market Trends and Insights

North America commands approximately 32% global market share in 2025, supported by mature industrial infrastructure, an established manufacturing base, and substantial investments in facility modernization and automation capabilities. The United States represents the region’s dominant market, with extensive industrial facilities, established utility infrastructure, and continuous investments in electrical system upgrades supporting sustained MCC demand. Major electrical equipment manufacturers including Rockwell Automation, Eaton, and Siemens, maintain significant manufacturing and research capabilities in North America, supporting product innovation and market leadership. The market growth is closely aligned with growth trends observed in the U.S. Variable Frequency Drive Market, which reinforces demand for advanced motor control architectures and integrated MCC solutions.

North American industrial operators are actively modernizing legacy motor control systems, with aging infrastructure and obsolete control panels undergoing systematic replacement with state-of-the-art MCCs. The region’s emphasis on worker safety, regulatory compliance with OSHA standards, and arc flash protection requirements drive adoption of advanced MCC designs incorporating enhanced safety features. Industrial automation initiatives and continuous investment in facility efficiency improvements support sustained demand for intelligent MCCs enabling real-time monitoring and predictive maintenance capabilities supporting operational excellence.

Europe Low Voltage Motor Control Center Market Trends and Insights

Europe represents a significant market, commanding approximately 28% global share in 2025, characterized by emphasis on energy efficiency, environmental sustainability, and stringent regulatory standards governing electrical equipment design and operation. Germany, the United Kingdom, France, and Spain maintain robust industrial bases with substantial motor control requirements supporting sustained MCC demand across manufacturing, chemical processing, and utility sectors. European manufacturers including Siemens AG and Schneider Electric leverage advanced technology capabilities and established customer relationships supporting market leadership across the region.

European regulatory frameworks emphasizing energy efficiency directives and environmental protection standards drive adoption of intelligent MCCs incorporating energy optimization features and sustainable component designs. The region’s industrial sector modernization initiatives and commercial infrastructure development support continued demand for advanced motor control solutions. The emphasis on Industry 4.0 adoption across European manufacturing facilities creates sustained opportunities for manufacturers developing MCCs with enhanced connectivity, advanced analytics, and integration capabilities supporting digital industrial ecosystems.

Asia Pacific Low Voltage Motor Control Center Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, projected to expand at approximately 6.8% CAGR through 2033, driven by rapid industrialization, expanding manufacturing capacity, and accelerating adoption of automation technologies across emerging economies including China, India, and Southeast Asia. China represents the largest market, with extensive manufacturing capacity and growing domestic consumption driven by industrial expansion and facility modernization initiatives. According to regional analysis, India demonstrates substantial market potential with expanding electrical infrastructure requirements and government emphasis on manufacturing excellence supporting sustained MCC adoption.

The region’s manufacturing advantages, including cost-effective production, skilled labor availability, and established supply chain infrastructure, position Asia Pacific as a center for global MCC manufacturing and distribution. Rapid urbanization across the region, increasing electrical infrastructure investment, and government initiatives supporting industrial development create substantial opportunities for MCC manufacturers offering cost-effective solutions meeting regional requirements. The expansion of data centers and telecommunications infrastructure across Asia Pacific creates emerging demand for advanced power management and motor control solutions supporting digital economy development.

Competitive Landscape

The global low voltage motor control center market is moderately consolidated, with a structured hierarchy dominated by large multinational suppliers supported by a long tail of regional and niche players. Market structure favors companies with integrated manufacturing, broad product portfolios, and global distribution networks, enabling consistent supply, cost efficiency, and long-term industrial partnerships. Competitive positioning is strongly influenced by technological depth, particularly in intelligent MCC architectures, digital connectivity, and modular system design.

Business strategies increasingly prioritize value-added solutions such as predictive maintenance compatibility, energy efficiency optimization, and lifecycle service offerings to strengthen customer retention. Regional players and emerging participants adopt focused strategies centered on application-specific solutions, customization, and localized service support to compete effectively against global incumbents. Across the market, differentiation is less price-driven and more reliant on system reliability, regulatory compliance, and integration capability within automated industrial environments, reinforcing entry barriers and sustaining moderate competitive intensity.

Key Market Developments

- April 2024: Rockwell Automation launched advanced FLEXLINE 3500 intelligent MCC incorporating AI-powered diagnostics, cloud connectivity, and real-time monitoring capabilities supporting predictive maintenance and operational optimization across diverse industrial applications.

- October 2024: Siemens launches SIMOCODE M-CP, compact motor management system for industrial switchboards and MCCs. Features Single Pair Ethernet, AI anomaly detection, scalable condition monitoring; reduces installation costs, optimizes space. Targets chemicals, mining, water treatment for efficient power control and fault protection.

- December 2025: Siemens board approves sale of Low Voltage Motors business to Innomotics India for Rs 2,200 crore via slump sale, closing June 2026 pending approvals.

Companies Covered in Low Voltage Motor Control Center Market

- ABB Ltd.

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric

- WEG

- Fuji Electric Co., Ltd.

- Powell Industries

- Rockwell Automation

- Eaton

- Marine Electricals

- Ingeteam S.A.

- Boerstn Electric Co., Ltd.

- Cape Electrical Supply Integration

- EAMFCO

- GT Engineering

- Legrand

- Rexnord Corporation

Frequently Asked Questions

The low voltage motor control center market is projected to reach US$ 4.7 billion in 2026, up from US$ 3.6 billion in 2020.

Key drivers include industrial automation growth, energy-efficient motor control adoption, intelligent monitoring integration, and stricter safety regulations.

North America leads the market with about 32% share in 2025.

Intelligent MCCs supporting Industry 4.0 and predictive maintenance represent the strongest opportunity.

Major players include Siemens, Schneider Electric, Rockwell Automation, ABB, Eaton, and Mitsubishi Electric.