- LED & Lighting (Optoelectronics)

- LED Lighting Controllers Market

LED Lighting Controllers Market Size, Share, and Growth Forecast 2026 – 2033

LED Lighting Controllers Market by Connectivity (Wired LED Lighting Controller, Wireless LED Lighting Controller), by Technology (Sensor, Dimmer, Day Light Harvesting, Time Scheduling), by End‑User (Residential, Commercial, Government, Street Lighting), by Regional Analysis, 2026–2033

LED Lighting Controllers Market Size and Trend Analysis

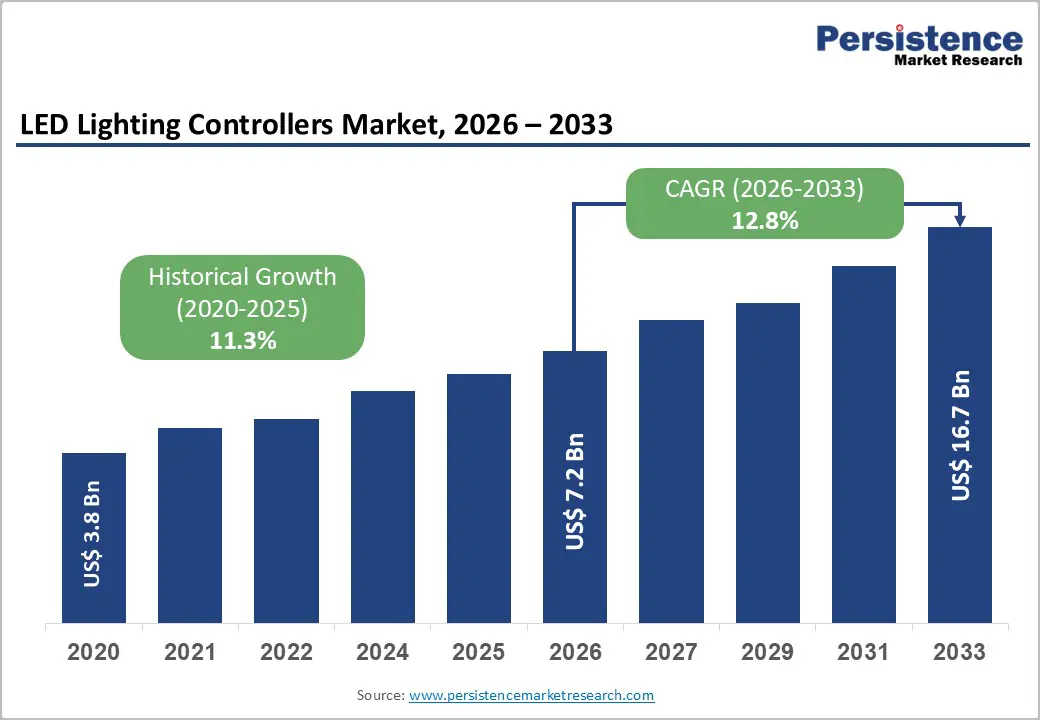

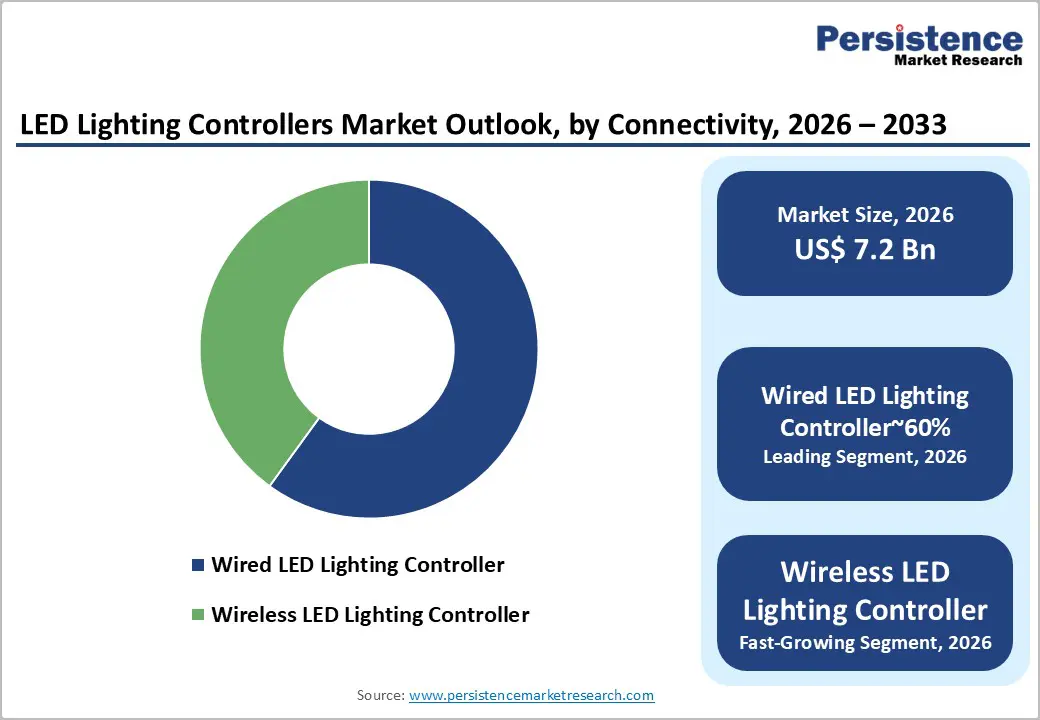

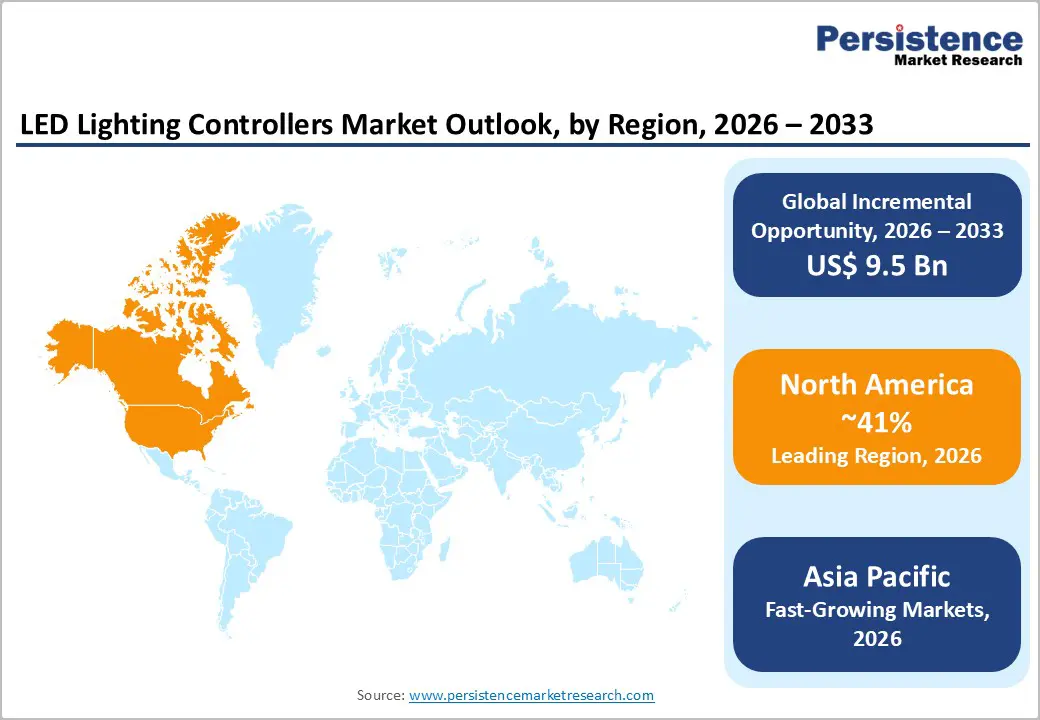

The global LED lighting controllers market size is likely to be valued at US$7.2 billion in 2026 and is expected to reach US$16.7 billion by 2033, growing at a CAGR of 12.8% during the forecast period from 2026 to 2033. This rapid expansion is driven by the global shift toward energy-efficient LED lighting, the proliferation of smart buildings and smart cities, and the integration of IoT-enabled controls that allow precise, automated management of illumination levels.

Key Market Highlights

- Leading region: North America leads the LED lighting controllers market with 41% market share, supported by stringent energy-efficiency regulations, advanced smart-building ecosystems, and widespread adoption of networked controls in commercial, industrial, and municipal projects.

- Fastest-growing region: Asia Pacific is the fastest-growing region, with a rising CAGR of 13.7%, driven by urbanization, infrastructure modernization, and government-led LED street-lighting programs in China, India, and ASEAN economies.

- Dominant segment from any category: The wired LED lighting controller segment dominates the connectivity category, accounting for around 60% of global demand due to its reliability, low latency, and compatibility with large-scale commercial and industrial installations.

- Fastest-growing segment from any category: The wireless LED lighting controller segment is one of the fastest-growing, driven by easy installation, retrofitting advantages, and integration with smart-home and smart-building platforms using Bluetooth Mesh, Zigbee, and Wi-Fi.

- Key market opportunity: The integration of LED lighting controllers into smart-city street-lighting networks and daylight-harvesting systems represent a major long-term opportunity, as municipalities and building owners seek energy savings, remote management, and data-driven decision-making

| Key Insights | Details |

|---|---|

|

LED Lighting Controllers Market Size (2026E) |

US$ 7.2 Billion |

|

Market Value Forecast (2033F) |

US$ 16.7 Billion |

|

Projected Growth CAGR (2026–2033) |

12.8% |

|

Historical Market Growth (2020–2025) |

11.3% |

Market Dynamics

Market Growth Drivers

Rising adoption of smart buildings and smart-home ecosystems

A primary driver of the LED lighting controllers market is the rapid adoption of smart buildings and smart-home ecosystems, which rely heavily on connected lighting controls to optimize energy use, occupant comfort, and operational efficiency. Industry-specific bodies such as the DesignLights Consortium (DLC) and ASHRAE highlight that networked lighting controls can reduce lighting-related energy consumption by 30% in commercial and institutional buildings through occupancy sensing, dimming, and time-based scheduling.

In residential settings, voice-assisted, app-based, and scene-control solutions from brands such as Philips Hue, Lutron, and Cree are making wireless LED lighting controllers a standard feature in new homes and retrofits. As smart-home penetration rises, supported by broadband coverage, low-cost wireless modules, and cloud platforms, demand for integrated LED lighting controllers is expected to grow in parallel.

Stringent energy-efficiency regulations and green-building standards

Another major driver is the tightening of energy-efficiency regulations and green-building standards worldwide. Programs such as ENERGY STAR, EU Ecodesign, Title 24 in California, and BREEAM/LEED certification frameworks increasingly require advanced lighting controls as a condition for compliance or higher ratings. For example, ASHRAE 90.1 and IECC codes mandate automatic shutoff, occupancy sensors, and daylight-harvesting controls in many commercial and institutional spaces, directly boosting demand for sensor-based, dimming, and time-scheduling LED controllers.

Municipalities are also rolling out LED street-lighting modernization programs that pair high-efficiency luminaires with centralized controllers capable of remote dimming, fault monitoring, and energy data analytics. These regulatory and policy-driven mandates compel building owners and utilities to invest in LED lighting controllers, thereby reinforcing long-term market growth.

Market Restraints

High initial investment and compatibility issues

One of the main restraints on the LED lighting controllers market is the higher upfront cost of advanced control systems compared with basic on/off switches or simple dimmers. While energy savings and maintenance benefits often justify the investment over time, budget-constrained projects, especially in price-sensitive residential and emerging-market segments, may delay adoption.

In addition, compatibility issues between different LED drivers, luminaires, and control protocols (e.g., 0–10 V, DALI, Zigbee, Bluetooth Mesh) can complicate system design and commissioning, leading to integration delays and higher engineering costs. Can these factors slow the penetration of sophisticated controllers in legacy installations and small-scale projects, constraining near-term growth in certain segments.

Cybersecurity and interoperability concerns

Another restraint is growing concern around cybersecurity and interoperability in connected lighting-control systems. As LED lighting controllers become part of building-automation networks and smart-city platforms, they are exposed to cyber threats, including unauthorized access, data breaches, and malicious firmware updates. Industry-focused white papers from building-automation associations warn that poorly secured IoT-enabled controllers can serve as entry points into broader IT and OT networks, prompting cautious adoption in critical infrastructure and government facilities.

At the same time, the fragmentation of wireless protocols and vendor-specific ecosystems can limit interoperability, forcing end users to lock into single suppliers or invest in middleware solutions. Until universal security standards and open-protocol frameworks gain wider traction, these concerns will continue to temper growth in highly networked LED lighting controllers.

Market Opportunities

Expansion of wireless and IoT-enabled LED lighting controllers

A major opportunity lies in the expansion of wireless and IoT-enabled LED lighting controllers, which are gaining share due to easy installation, flexible retrofitting, and seamless integration with smart-home and smart-Building platforms. Industry-specific analyses indicate that wireless LED lighting controllers are growing faster than wired counterparts, supported by Bluetooth Mesh, Zigbee, Wi-Fi, and Thread-based ecosystems that enable mesh networking, remote monitoring, and over-the-air updates.

In residential and small-commercial projects, wireless controllers eliminate the need for extensive conduit runs and rewiring, significantly reducing installation time and labor costs. As chipset prices decline and cloud-based management platforms mature, wireless LED lighting controllers are expected to penetrate multi-family housing, retail, hospitality, and light industrial segments, creating a high-growth revenue pocket for vendors.

Growth of daylight harvesting and advanced sensor-based controls

Another key opportunity is the rising deployment of daylight harvesting and advanced sensor-based controls in commercial, institutional, and public-infrastructure projects. Studies cited by lighting-control associations show that daylight-harvesting systems using photo-sensors and continuous dimming can reduce lighting energy consumption by 40% in perimeter-daylit spaces such as offices, schools, and retail environments.

LED lighting controllers that combine occupancy sensors, photo-sensors, and time-scheduling algorithms are increasingly integrated into building-management systems (BMS) to deliver granular control, real-time analytics, and compliance reporting. In street-lighting applications, adaptive controllers that dim lamps during low-traffic hours or in favorable weather are being adopted under smart-city programs, further expanding the addressable market for sensor-driven LED lighting controllers.

Category-wise Insights

By Connectivity Analysis

Within the connectivity category, the wired LED lighting controller segment holds the largest market share, estimated at around 60% of global demand. This leadership is rooted in the high reliability, low latency, and established compatibility with the electrical infrastructure of wired systems in large-scale commercial, industrial, and institutional installations. Wired controllers based on standards such as 0–10 V, DALI, and DMX are widely used in office buildings, hospitals, universities, and manufacturing plants, where stable communication and predictable performance are critical.

Industry-focused market-analysis reports from lighting-control associations indicate that wired LED lighting controllers remain the default choice for new construction projects and mission-critical facilities, despite the growing appeal of wireless alternatives. As long as building codes and facility-management practices favor hard-wired control networks, this segment is expected to retain its dominant position.

By Technology Analysis

Among technology segments, the dimmer LED lighting controller category is the largest, accounting for roughly 40% of the global LED lighting controllers market. This dominance reflects the ubiquitous need for light-level adjustment in residential, commercial, and hospitality environments, where dimming improves ambiance, occupant comfort, and energy savings.

LED-compatible dimmers that support phase-cut, 0–10 V, DALI, and PWM interfaces are widely deployed in living rooms, dining areas, conference rooms, and hotel lobbies, enabling scene-based lighting and personalized user experiences. Technical guidance from lighting-engineering bodies emphasizes that dimming can extend LED lamp life and reduce energy use by up to 20% when properly implemented. As smart-home platforms integrate dimming controls into voice-assisted ecosystems, the dimmer segment is expected to remain a core technology pillar of the LED lighting-controller market.

By End-User Analysis

Within the end-user category, the commercial segment is the largest, with an estimated market share of about 40% of global demand for LED lighting controllers. This leadership stems from the high energy intensity of office buildings, retail spaces, hotels, and healthcare facilities, where lighting accounts for a significant portion of total electricity consumption. Commercial building codes such as ASHRAE 90.1 and IECC mandate automatic shutoff, occupancy sensing, and daylight-harvesting controls, driving widespread adoption of sensor-based, dimming, and time-scheduling LED controllers.

Industry-specific data from building-automation associations show that networked lighting controls can cut commercial-lighting energy use by 30%, making them a cost-effective investment for property owners and facility managers. As smart-building initiatives expand in North America, Europe, and Asia Pacific, the commercial segment is expected to remain the primary revenue driver for LED lighting controllers.

Regional Insights

North America LED Lighting Controllers Trends

In North America, the LED lighting controllers market is led by the United States, where stringent energy-efficiency regulations, advanced building- automation ecosystems, and a mature smart-home market drive strong demand. ENERGY STAR-qualified LED lighting controllers, DLC-listed networked controls, and Title 24-compliant systems are widely adopted in commercial, industrial, and municipal projects, supported by federal and state-level incentives for energy-saving retrofits.

Major lighting-control vendors such as Lutron Electronics, Eaton, Hubbell Lighting, Acuity Brands, and Cree have established extensive distribution and service networks across the region, offering integrated solutions for smart offices, retail chains, and smart-city street-lighting programs. The U.S. innovation ecosystem, including Silicon-Valley-linked IoT platforms and cloud-based building-management systems, further accelerates the deployment of connected LED lighting controllers.

Europe LED Lighting Controllers Trends

In Europe, the LED lighting controllers market is shaped by harmonized energy-efficiency directives, green-building standards, and national smart-city initiatives. Countries such as Germany, the United Kingdom, France, and Spain have implemented EU-level regulations on energy performance of buildings (EPBD) and ecodesign requirements, which encourage the use of advanced lighting controls in residential, commercial, and public-infrastructure projects.

German and Scandinavian utilities, for instance, are rolling out LED-street-lighting controllers with remote monitoring, adaptive dimming, and data-logging capabilities to meet carbon-reduction targets. At the same time, European lighting-control associations promote open standards such as DALI and KNX, which enhance interoperability and system longevity. As EU Green Deal-linked policies push for deep energy savings in buildings and cities, LED lighting controllers are expected to play a central role in European decarbonization strategies.

Asia Pacific LED Lighting Controllers Trends

In Asia Pacific, the LED lighting controllers market is experiencing rapid growth, driven by urbanization, infrastructure modernization, and government-led LED-street-lighting programs. China, Japan, India, and ASEAN economies such as Vietnam and Indonesia are expanding commercial real-estate, industrial parks, and smart-city projects, all of which require energy-efficient lighting controls.

Indian and Chinese national programs promoting LED street-lighting upgrades have created large-scale demand for centralized LED lighting controllers capable of remote dimming, fault detection, and energy-data reporting. Local manufacturers in China and India are producing cost-competitive wired and wireless controllers, supporting both domestic adoption and exports. As ASEAN nations invest in smart-city infrastructure, the Asia Pacific region is poised to become one of the fastest-growing markets for LED lighting controllers globally

Competitive Landscape

The global LED lighting controllers market is moderately consolidated, with a small group of multinational leaders holding significant market share, while a large number of regional and niche players serve local and specialized applications. Major companies such as Hubbell Lighting, Inc., GE Lighting, LLC, OSRAM Licht AG, Royal Philips N.V., Acuity Brands Lighting, Inc., Eaton Corporation, Schneider Electric S.E., Honeywell International, Lutron Electronics, and Cree, Inc. compete on technology differentiation, global service networks, and integrated smart-building solutions.

These leaders invest heavily in R&D to develop advanced wireless protocols, open-API platforms, and AI-driven lighting-control algorithms that improve energy savings and user experience. Emerging business-model trends include subscription-based lighting-as-a-service (LaaS), performance-based contracts, and cloud-managed control platforms, which allow operators to optimize energy use and predict maintenance needs. At the same time, local manufacturers in Asia Pacific and Latin America are expanding through cost-competitive offerings and regional partnerships, intensifying price competition in standard-product segments.

Companies Covered in LED Lighting Controllers Market

- Hubbell Lighting, Inc.

- GE Lighting, LLC

- OSRAM Licht AG

- Royal Philips N.V.

- Acuity Brands Lighting, Inc.

- Eaton Corporation

- Schneider Electric S.E.

- Honeywell International

- Lutron Electronics

- Cree, Inc.

- Signify Holding (Philips Lighting)

- Legrand

- ams‑OSRAM International GmbH

- Leviton Manufacturing Co., Inc.

- Digital Lumens Incorporated

Frequently Asked Questions

The global LED lighting controllers market is projected to reach US$ 16.7 Billion by 2033, growing at a CAGR of 12.8% from 2026 to 2033, driven by smart‑building adoption, energy‑efficiency regulations, and expansion of wireless and IoT‑enabled controls.

Key demand drivers include rising adoption of smart buildings and smart‑home ecosystems, stringent energy‑efficiency regulations, green‑building standards, and government‑led LED‑street‑lighting modernization programs, all of which favor advanced LED lighting controllers with dimming, sensing, and scheduling capabilities.

The wired LED lighting controller segment dominates the connectivity category, accounting for around 60–65% of global demand due to its high reliability, low latency, and compatibility with large‑scale commercial and industrial installations.

North America leads the LED lighting controllers market, supported by stringent energy‑efficiency codes, advanced smart‑building ecosystems, and widespread deployment of networked lighting controls in commercial, industrial, and municipal projects.

A key growth opportunity lies in the integration of LED lighting controllers into smart‑city street‑lighting networks and daylight‑harvesting systems, enabling remote dimming, energy‑data analytics, and compliance with decarbonization targets.

Leading players include Hubbell Lighting, Inc., GE Lighting, LLC, OSRAM Licht AG, Royal Philips N.V., Acuity Brands Lighting, Inc., Eaton Corporation, Schneider Electric S.E., Honeywell International, Lutron Electronics, and Cree, Inc., among others.