- Food Packaging

- Bottled Water Packaging Market

Bottled Water Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Bottled Water Packaging Market By Material Type (Plastic (PET), Glass, Others), Distribution Channel (Retail Stores, Supermarkets & Hypermarkets, Others), Application, and Regional Analysis for 2025 - 2032

Bottled Water Packaging Market Size and Trends Analysis

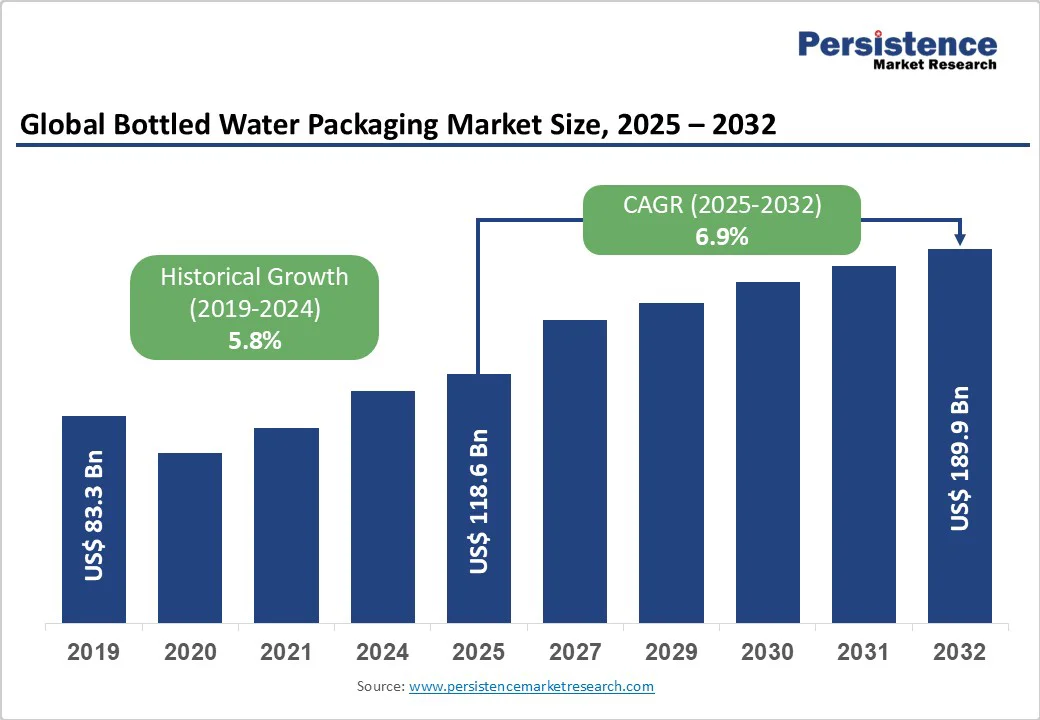

The global bottled water packaging market size was valued at US$118.6 Billion in 2025 and is projected to reach US$189.9 Billion by 2032, expanding at a CAGR of 6.9% between 2025 and 2032, driven by the steady increase in bottled water consumption worldwide, the growing preference for single-serve convenience formats, and rising consumer awareness regarding safe drinking water.

Sustainable packaging, such as recycled PET and aluminum, is transforming product strategies. Urbanization and changing lifestyles drive higher packaging demand, while regulations and brand recyclate commitments spur innovation in materials and circular systems.

Key Industry Highlights

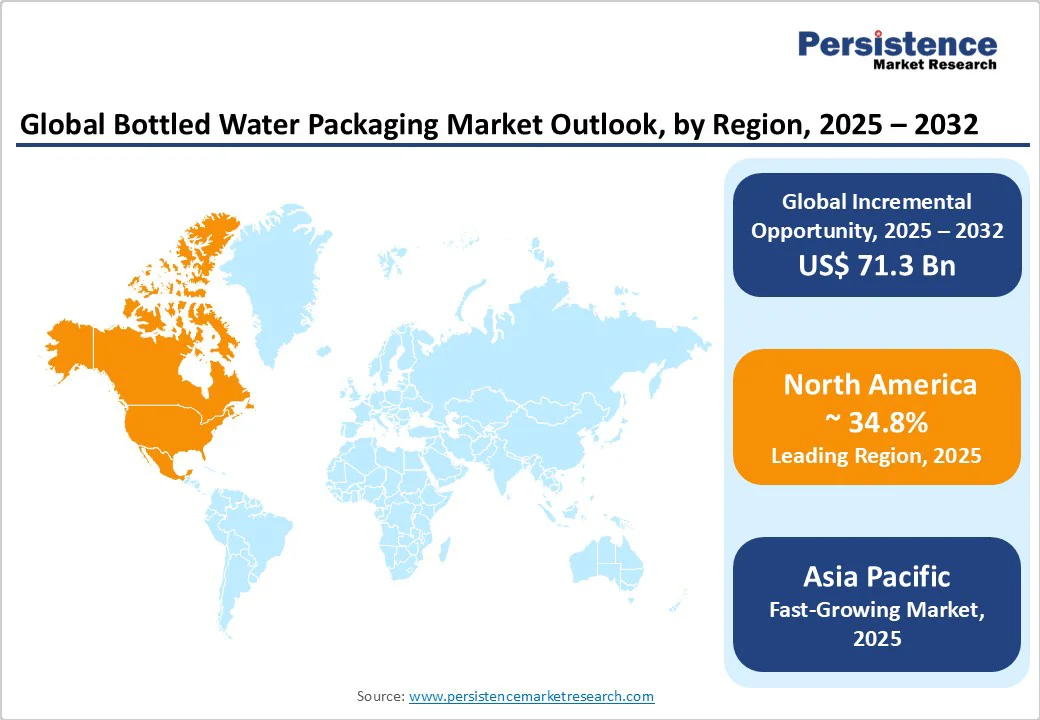

- Leading Region: North America accounts for approximately 34.8% of global market revenue in 2025, driven by high per-capita consumption, mature retail networks, and strong regulatory frameworks.

- Fastest-Growing Region: Asia Pacific, due to urbanization, rising middle-class income, and high reliance on bottled water in China, India, and ASEAN countries.

- Investment Plans: Major players are investing in rPET production lines, aluminum packaging expansion, and lightweight PET technology. Examples include Amcor and Ball Corporation expanding production capacity in North America and Europe.

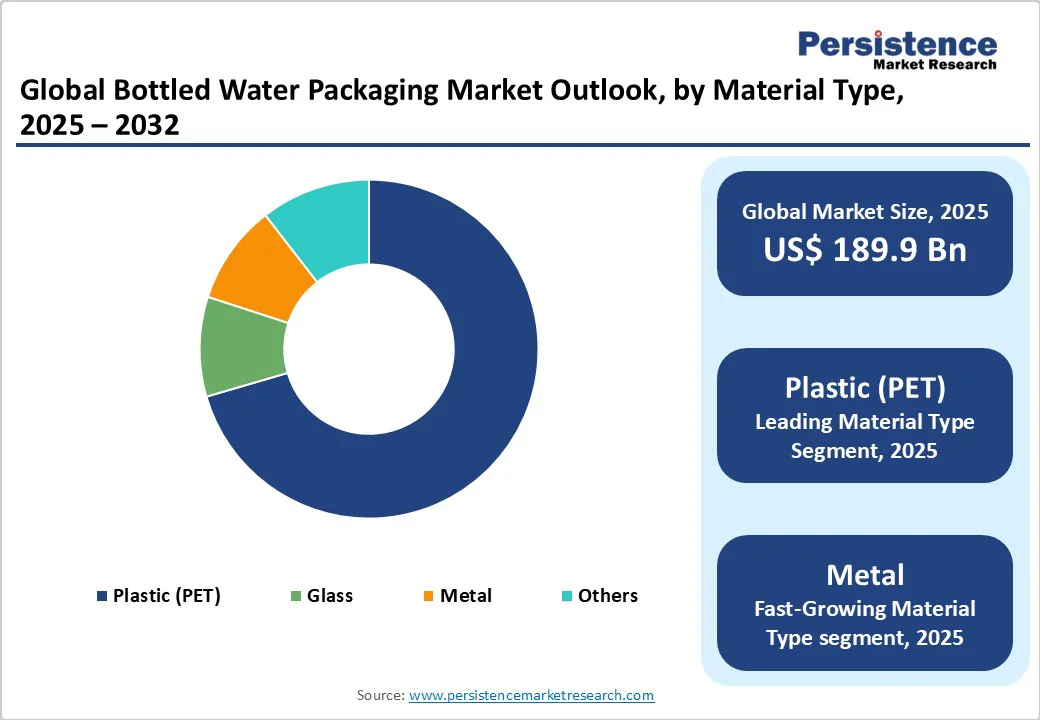

- Dominant Material Type: Plastic (PET) holds 74% of global revenue, supported by cost-efficiency, light weight, and scalability across single-serve and multipack formats.

- Dominant Distribution Channel: Retail and Supermarkets, over 37% of global sales, leveraging shelf visibility and multipack formats in mature markets.

| Key Insights | Details |

|---|---|

| Bottled Water Packaging Market Size (2025E) | US$118.6 Bn |

| Market Value Forecast (2032F) | US$189.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Bottled Water Consumption and Convenience Culture

Global per-capita bottled water consumption has surged due to urbanization, limited access to safe tap water, and health-driven substitution away from carbonated drinks. Still water dominates packaged formats, accounting for around 63% of total volume, reflecting consumer preference for affordability and simplicity.

The expansion of convenience retail channels and vending networks, coupled with single-serve packaging growth, continues to propel packaging volumes. In emerging economies, improvements in disposable income and public health awareness are further accelerating packaged water demand, directly benefiting packaging manufacturers across PET, glass, and aluminum categories.

Sustainability Regulations and rPET Adoption

Sustainability-focused legislation and brand commitments are reshaping the bottled water packaging landscape. The European Union’s Single-Use Plastics Directive and North America’s state-level Extended Producer Responsibility (EPR) policies are encouraging a transition toward circular materials such as rPET and recyclable aluminum.

Global brands, including Danone and Coca-Cola, have pledged to integrate up to 100% recycled plastic content in their bottles by 2025-2030. This structural transition is stimulating investment in recyclate processing, bottle-to-bottle infrastructure, and lightweight material engineering. It is also fostering higher-margin opportunities for converters that can provide certified, high-quality rPET and closed-loop packaging systems.

Barrier Analysis - Premiumization and Channel Evolution

The shift toward premium, flavored, and functional bottled waters has created demand for high-value packaging solutions. Functional and vitamin-enriched waters, with forecast growth rates above 9%, often use distinctive materials such as aluminum and glass to signal quality and sustainability.

The rise of e-commerce and direct-to-consumer models has reinforced this trend, as brands increasingly prioritize packaging aesthetics and durability for delivery logistics. Subscription-based hydration products and bulk online purchasing are generating new design requirements, such as resealable closures and compact multipacks, expanding the revenue potential for innovative packaging suppliers.

Raw Material Cost Volatility

Producers of PET, aluminum, and glass packaging face persistent raw material and energy price volatility. PET resin costs are closely tied to global crude oil markets, while energy prices strongly affect glass and metal packaging production.

Fluctuations in resin pricing, which have exceeded 20% in recent years, can compress converter margins, especially under fixed-price supply contracts. Small and mid-sized manufacturers with limited hedging capacity often experience constrained investment in sustainability and R&D during such periods, slowing their transition to eco-friendly production models.

Opportunity Analysis - Plastic Waste Regulations and Brand Risks

Global scrutiny over plastic waste and marine pollution presents reputational and financial risks to bottled water brands and their packaging suppliers. Extended Producer Responsibility schemes and deposit return systems in markets such as the EU, Canada, and select U.S. states have increased operational costs for compliance and collection.

Failure to meet recyclability or recycled-content mandates can lead to penalties and brand backlash, pushing companies to accelerate shifts to alternative materials and recycled inputs. These policy pressures, while positive for sustainability, temporarily elevate production and logistics expenses across the value chain.

Rapid Expansion of rPET Supply Chains

Plastic accounts for roughly 74% of global bottled water packaging value, equivalent to about US$90 Billion in 2025. If rPET penetration reaches even 30% of plastic packaging value by 2032, aligned with major corporate pledges, the addressable rPET market opportunity could approach US$44 Billion.

This transition presents substantial prospects for recyclers, resin producers, and packaging converters investing in advanced washing and pelletizing technology. The growing availability of food-grade rPET also enables premium pricing and brand differentiation for sustainable packaging.

Growth of Metal Packaging for Premium and Sustainable Brands

Aluminum cans and bottles are emerging as viable, high-value alternatives to plastic. Their near-infinite recyclability and strong consumer acceptance position metal as the fastest-growing packaging material, with a forecast CAGR of about 7.5%.

Beverage brands introducing canned water formats are targeting environmentally conscious consumers and on-the-go segments. The proliferation of metal packaging provides equipment manufacturers, material suppliers, and branding firms with opportunities to expand into the premium hydration market and capture sustainability-driven demand.

Digital and Lightweight Packaging Innovations

Technological advancements such as smart labeling, digital traceability, and lightweight engineering are revolutionizing packaging design. Smart packaging equipped with QR codes or NFC chips enhances transparency and supports anti-counterfeiting measures.

Lightweighting innovations, reducing PET weight per bottle by up to 25%, improve cost efficiency and reduce carbon emissions. Companies offering packaging-as-a-service, where design, materials, and digital tracking are integrated, stand to benefit from recurring revenue models and brand partnerships focused on supply-chain optimization.

Category-wise Analysis

Material Type Insights

Plastic, particularly PET (Polyethylene Terephthalate), dominates bottled water packaging, accounting for around 74% of global revenue, valued at nearly US$90 Billion. PET’s lightweight, low-cost, and mass-production-friendly nature makes it ideal for single-serve and multipack formats.

Major brands such as Coca-Cola’s Dasani and Nestlé Pure Life rely on PET for global distribution. Advances in PET technology, higher clarity, barrier coatings, and improved recyclability enhance shelf appeal and sustainability compliance. Investments in rPET are growing, with Danone targeting 50% rPET usage in its European portfolio by 2025.

Aluminum is the fastest-growing packaging segment, driven by recyclability, premium aesthetics, and durability. Brands such as LaCroix, Flow Water, and JUST Water are adopting aluminum cans and bottles to differentiate in crowded markets. Innovations such as lightweight foil forming, protective coatings, and custom embossing expand its use across still and sparkling water.

Aluminum’s global recycling rate exceeds 70%, offering circular packaging advantages, particularly in Europe and North America. For example, Flow Water uses aluminum to maintain mineral water integrity while reinforcing sustainability messaging, highlighting consumer preference for environmentally responsible packaging.

Distribution Channel Insights

Retail stores and supermarkets remain the leading distribution channel, accounting for over 37% of global bottled water packaging sales. Their dominance stems from high consumer footfall, wide shelf exposure, and accessibility, which drive volume. Packaging strategies here often focus on multipacks, promotional labels, and visually appealing designs to influence purchases.

For example, Nestlé Pure Life in the U.S. uses 6- and 12-pack PET bottles with vibrant seasonal labeling, while Perrier and San Pellegrino position premium glass bottles to attract upscale consumers. Retail dominance is strongest in North America and Europe, with chains such as Walmart, Carrefour, and Tesco setting packaging standards for shelf efficiency and brand visibility.

E-commerce is the fastest-growing channel, with a projected CAGR of 7.7% through 2032. Online platforms, direct-to-consumer brands, and subscription services are boosting demand for durable, ergonomically designed bottles suitable for shipping.

JUST Water and Flow Water leverage aluminum bottles and eco-friendly cartons optimized for transport, reducing breakage and enhancing sustainability messaging. Bulk packaging, such as 5L PET bottles or multipacks of 500mL bottles, is popular in subscriptions, driving innovations in closures, reinforced packaging, and lightweight designs. Growth in India, China, and Southeast Asia further accelerates packaging innovation for resilient delivery logistics.

Regional Insights

North America Bottled Water Packaging Market Trends - Mature Market Focused on Sustainability and Premium Packaging

North America contributes approximately 34.8% of global bottled water packaging revenue, making it the most mature and regulated regional market. The U.S. leads due to high per-capita consumption (over 42 gallons per person annually) and a strong culture of convenience.

Retail outlets and e-commerce platforms are both well-developed, supporting formats ranging from single-serve PET bottles to premium multipacks. Regulatory initiatives, including Extended Producer Responsibility (EPR) programs and state-level deposit return systems, have improved PET collection and recycling rates. The U.S. PET bottle collection rate reached 33% in 2023, encouraging broader use of recycled content.

Companies such as Amcor, Ball Corporation, and Berry Global maintain extensive production facilities, enabling just-in-time supply to major beverage brands. Investment is focused on rPET production, lightweighting technologies, and expansion of aluminum packaging lines to meet consumer demand for premium and sustainable options.

Premium and functional water brands, such as Essentia Water and Smartwater, leverage both PET and aluminum bottles to cater to niche consumer segments, combining aesthetic appeal with sustainability credentials.

Europe Bottled Water Packaging Market Trends - Regulation-Driven Innovation and Circular Packaging Leadership

Europe is one of the most established and regulation-intensive bottled water packaging markets. Countries such as Germany, France, and Italy maintain a strong mineral water culture, where premium glass packaging is often preferred for brand differentiation.

EU-wide legislation, including the Single-Use Plastics Directive and mandatory recycled-content targets by 2025, has accelerated innovation in recyclable and renewable materials. Germany’s and Nordic countries’ deposit return systems achieve recycling rates above 90%, providing a global benchmark for circular packaging models.

European converters, such as Sidel and ALPLA, are investing in rPET capacity, paper-based alternatives, and pilot reuse programs, particularly targeting the hospitality sector. Glass maintains a niche in premium mineral water, exemplified by brands such as Evian and Voss, which use reusable and aesthetically designed bottles.

Investment is concentrated in countries emphasizing sustainability and compliance, including France, the U.K., and Scandinavia, with initiatives such as pilot returnable bottle schemes for restaurants and cafes.

Asia Pacific Bottled Water Packaging Market Trends - Rapid Growth Fueled by Urbanization and Expanding PET Infrastructure

Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 8% through 2032, driven by population growth, urbanization, and concerns over drinking water safety. Key markets include China, India, and ASEAN nations, representing the largest share of incremental demand.

In China, rising middle-class income and urban lifestyle changes have led to growth in premium imports and differentiated packaging materials such as aluminum and glass. India is witnessing the rapid expansion of both single-serve and bulk PET water bottles, supported by urban demand and increasing retail penetration.

Southeast Asia’s fragmented municipal water systems contribute to heavy reliance on bottled water, driving PET bottle demand and related packaging innovation. Leading regional players are expanding PET bottling capacity, while multinational brands explore aluminum bottles and rPET adoption in urban centers.

Sustainability-focused initiatives, such as pilot recycling and bottle return programs, are being introduced in markets, including Singapore, Malaysia, and Thailand, indicating a gradual shift toward circular packaging. Investments also target lightweighting, digital labeling, and premium closures, aligning with consumer preferences for functional and eco-friendly water solutions.

Competitive Landscape

The global bottled water packaging market is moderately consolidated, with major players such as Amcor, Ball Corporation, ALPLA, Ardagh Group, Berry Global, and Sidel dominating through technological leadership, extensive manufacturing networks, and supply agreements with beverage giants. Regional converters maintain local presence, creating a blend of global consolidation and regional fragmentation.

Competition centers on sustainability, cost efficiency, and innovation in lightweight and recycled materials. Leading companies focus on three strategies: advancing sustainability via rPET and low-carbon practices, driving innovation in premium and functional packaging, and expanding geographically in emerging markets, including Asia and Latin America, to capture growth opportunities.

Key Industry Developments

- In February 2025, Ball Corporation announced plans to build a two-line aluminum can plant in Oregon and also acquired Florida Can Manufacturing, underscoring its bet on future North American growth in aluminum beverage packaging.

- In March 2025, Ball completed the sale of its aerospace business and repositioned itself as a dedicated aluminum-packaging company, aligning with its strategy to focus on low-carbon, high-value packaging for beverages, including bottled water.

Companies Covered in Bottled Water Packaging Market

- Amcor plc

- Ball Corporation

- Sidel (Tetra Laval Group)

- Ardagh Group

- Berry Global

- Plastipak Holdings

- ALPLA Werke GmbH

- Owens-Illinois (O-I)

- Silgan Holdings Inc.

- Graham Packaging Company

- Tetra Pak

- Ajanta Bottle Pvt. Ltd.

- PGP Glass Pvt. Ltd.

- Crown Holdings

- Nampak Ltd.

- Retal Industries

- Consol Glass

- Vetropack Holding AG

- RPC Group

- Vidrala S.A.

Frequently Asked Questions

The bottled water packaging market size in 2025 is estimated at US$118.6 Billion.

The bottled water packaging market is projected to reach US$189.9 Billion by 2032, reflecting steady growth driven by rising consumption and sustainability-focused packaging innovations.

Key trends are increased adoption of recycled PET (rPET) bottles and aluminum packaging for sustainability and growth of functional and premium water segments, emphasizing wellness and lifestyle appeal.

Plastic (PET) is the dominant material, accounting for 74% of market revenue, due to its low cost, light weight, and scalability across single-serve and multipack formats.

The bottled water packaging market is expected to grow at a CAGR of 6.9% from 2025 to 2032, driven by rising global bottled water consumption, urbanization, and sustainable packaging initiatives.

Major players include Amcor plc, Ball Corporation, Sidel (Tetra Laval Group), Ardagh Group, and Berry Global.