- Home Appliances

- LED Desk Lamp Market

LED Desk Lamp Market Size, Share, and Growth Forecast, 2026 - 2033

LED Desk Lamp Market by Product Type (LED Desk Lamps, Smart LED Desk Lamps, Incandescent, Fluorescent), Application (Residential, Commercial, Industrial), Distribution Channel (Online, Offline), and Regional Analysis for 2026 - 2033

LED Desk Lamp Market Share and Trends Analysis

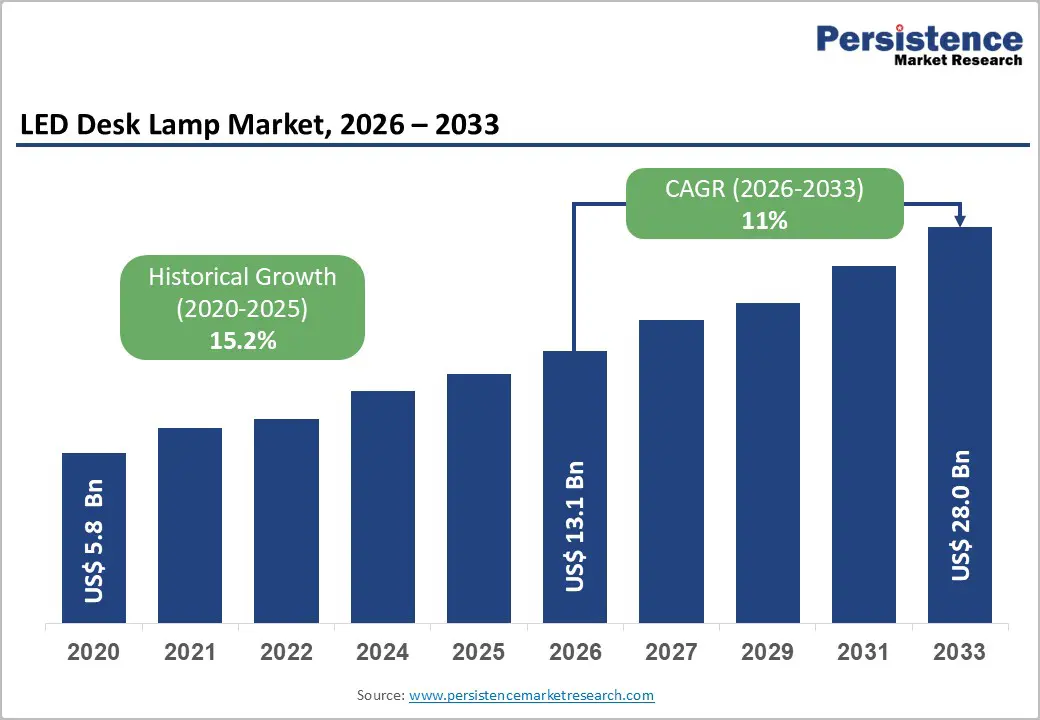

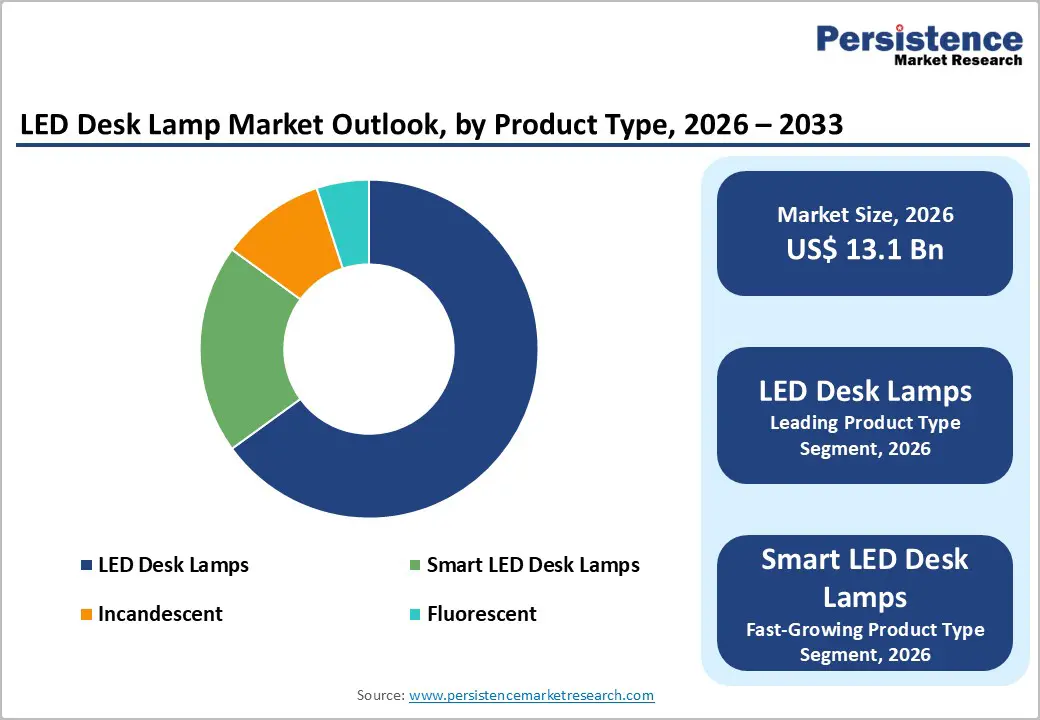

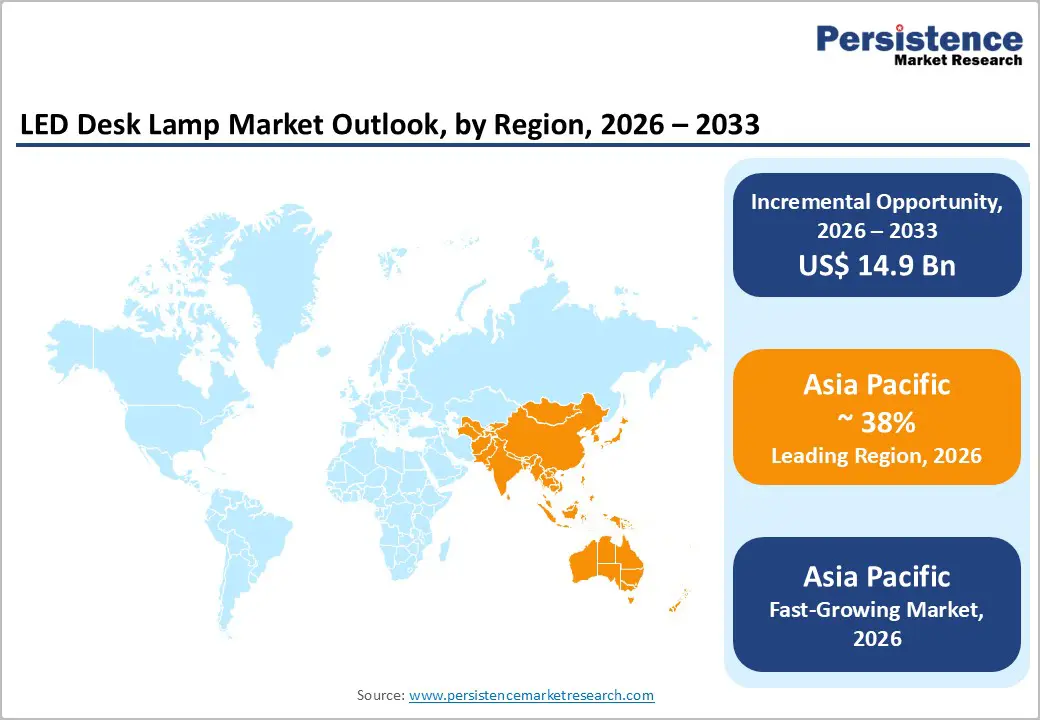

The global LED desk lamp market size is likely to be valued at US$ 13.1 billion in 2026, and is projected to reach US$ 28.0 billion by 2033, growing at a CAGR of 11% during the forecast period 2026 - 2033.

This robust expansion is driven by increasing adoption of energy-efficient lighting solutions in residential and commercial spaces, accelerated remote work trends requiring enhanced home office setups, and technological advancements in smart lighting integration. The market demonstrates strong momentum driven by growing consumer environmental consciousness and stringent energy-efficiency regulations across major economies, particularly in North America and Europe, where light-emitting diode (LED) technology adoption has become a standard requirement for new construction and renovation projects.

Key Industry Highlights

- Regional Dominance: The Asia Pacific market is likely to be both the leading and fastest-growing regional market through 2033, accounting for approximately 38% of the market share.

- Leading & Fastest-growing Product Type: LED desk lamps are slated to lead with an estimated 2026 share of 65%, while smart LED desk lamps are likely to be the fastest-growing over the 2026 - 2033 forecast period.

- Leading & Fastest-growing Application: Residential applications are set to hold an estimated 45% revenue share in 2026, with commercial applications growing the fastest during the 2026 - 2033 forecast period.

- Market Driver: Government regulations promoting energy-efficient lighting solutions have become a key catalyst for the adoption of LED desk lamps across major economies.

| Key Insights | Details |

|---|---|

| LED Desk Lamp Market Size (2026E) | US$ 13.1 Bn |

| Market Value Forecast (2033F) | US$ 28.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11% |

| Historical Market Growth (CAGR 2020 to 2025) | 15.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Energy Efficiency Mandates and Sustainability Initiatives

Government regulations that promote energy-efficient lighting solutions are catalyzing the adoption of LED desk lamps across economies. Authorities in North America, Europe, and parts of Asia have introduced strict performance standards that gradually remove inefficient products from the market and encourage the use of advanced alternatives such as LED technologies. At the same time, policy frameworks increasingly align with broader climate and energy-security objectives, which positions LED desk lamps as a practical option for households, schools, and offices that want to support national sustainability goals. This regulatory environment also gives manufacturers a clear direction for product development and encourages investment in efficient, durable, and compliant designs.

These policy shifts are reinforced by corporate sustainability programs and rising environmental awareness among end users across residential, educational, and commercial settings. Organizations are integrating energy-efficient lighting into their environmental, social, & governance (ESG) roadmaps to reduce operating costs, improve workplace conditions, and demonstrate responsible resource use. Consumers and students are also becoming more informed about the health, visual comfort, and environmental benefits of higher-quality lighting solutions, which increases their willingness to move from conventional desk lamps to LED-based products. Together, these trends are accelerating LED desk lamp penetration and reshaping the competitive landscape, favoring suppliers that can combine regulatory compliance with thoughtful design, strong service quality, and long-term value for users.

Market Fragmentation and Product Quality Inconsistency

The LED desk lamp market is highly fragmented, with many manufacturers following different quality standards, which often leads to confusion and buyer disappointment. In contrast to sectors that require strict certifications and technical approvals before launch, this category allows relatively easy entry for new suppliers, resulting in a wide range of product performance. This situation increases the risk that consumers may purchase lamps with poor design or weak components, even when packaging and marketing materials appear credible. From a strategic perspective, this underscores the importance of conducting due diligence on vendor capabilities, verifying compliance with relevant safety marks, and carefully reviewing technical documentation before making purchasing or sourcing decisions.

Quality concerns are not limited to basic visual impressions but also extend to technical aspects such as color rendering index (CRI) accuracy, LED durability, and the effectiveness of thermal management in protecting internal components. Consumer protection bodies and market surveillance authorities have reported that inconsistent testing practices and limited oversight, especially in cross-border online channels, allow products with overstated performance claims to reach end users. This inconsistency can harm the reputation of the entire category and slow the development of premium offerings, as customers become skeptical about promises related to lifetime, energy performance, and eye-comfort benefits.

Technological Innovation and the Integration of Smart Features

The desk lamps market presents several growth opportunities, particularly through technological innovation and the integration of smart features. The rising adoption of smart home ecosystems is creating strong potential for desk lamps that integrate seamlessly with home automation platforms, including systems for lighting, security, and energy management. As more households install connected devices, customers increasingly expect their desk lighting to function as part of a coordinated environment rather than as a standalone product. This shift allows manufacturers to reposition desk lamps from a basic utility item to a connected, value-added component of the smart home.

Lamps with features such as remote control through smartphone applications, voice activation via virtual assistants, and programmable light settings tailored to work, reading, or relaxation modes are gaining traction among both residential and professional users. These capabilities offer greater convenience and personalization, allowing users to adjust brightness, color temperature, and schedules to match their daily routines and visual comfort needs. The trend is encouraging manufacturers to increase investment in research & development (R&D), focusing on embedded sensors, connectivity modules, and software integration to deliver more advanced and differentiated offerings. For example, in June 2025, Govee launched the Table Lamp 2 Pro x Sound by JBL, a smart hybrid blending 210 customizable LED beads, music-reactive lighting, and compatibility with Alexa, Google Assistant, and Matter.

Category-wise Analysis

Product Type Insights

LED desk lamps are slated to maintain a dominant position in the market, with an estimated 2026 share exceeding 65%, primarily due to their energy efficiency, longevity, and decreasing price. The technological advancements in LED lighting have led to the development of lamps that offer a wide spectrum of color temperatures and brightness levels, catering to both task lighting and ambient lighting needs. Furthermore, the shift towards eco-friendly solutions has led to increased consumer preference for LED lamps, which have a lower environmental impact than traditional lighting technologies.

Smart LED desk lamps are likely to be the fastest-growing segment over the 2026 - 2033 forecast period. These lamps seamlessly integrate with major voice assistants, including Amazon Alexa, Google Assistant, and Apple HomeKit, enabling voice control and automation routines. Smart features include smartphone app control for brightness and color temperature adjustment, scheduling capabilities enabling automated lighting routines, presence detection for energy conservation, and integration with productivity applications. Premium models feature wireless charging pads, USB charging ports, and ambient light sensors that automatically optimize illumination based on environmental conditions.

Application Insights

Residential applications are expected to capture roughly 45% of the LED desk lamp market share in 2026, reflecting the fundamental role of desk lamps in home office setups, student study areas, and bedside reading. The residential segment has experienced accelerated growth following structural work-from-home trends, with homeowners investing in quality task lighting to support productive work environments. Consumer preferences emphasize aesthetic design compatibility with interior décor, adjustable brightness levels accommodating various activities, and energy efficiency reducing electricity costs. The segment exhibits strong growth in developed markets where remote work penetration remains elevated and in emerging economies experiencing middle-class expansion with associated housing improvements and educational investments.

Commercial is anticipated to be the fastest-growing segment during the 2026 - 2033 forecast period, driven by corporate office expansions, the proliferation of co-working spaces, and educational facility modernization programs. Businesses prioritize LED desk lamps for their durability, low maintenance requirements, and energy cost reductions, with return-on-investment calculations favoring LED technology despite higher upfront costs. In October 2025, for instance, BenQ launched the ScreenBar Pro in India, a monitor light bar with 3rd-gen ASYM-Light™ tech for glare-free desk illumination. It features ultrasonic auto-on/off, brightness/color-temperature levels, full-spectrum LEDs, and fits even curved monitors. The segment benefits from green building certification programs, including LEED and WELL Building Standard, which award points for energy-efficient lighting and occupant health considerations.

Distribution Channel Insights

The offline segment is likely to lead with an approximate 55% share of the LED desk lamp market in 2026, providing consumers with hands-on product evaluation, professional guidance, and immediate availability. Physical retail channels enable customers to assess build quality, test lighting characteristics, and receive expert recommendations tailored to specific application requirements. This channel remains particularly important for premium products where consumers seek assurance through physical inspection and for customers preferring in-person shopping experiences with immediate gratification rather than online ordering and delivery waiting periods.

Online retail is expected to be the fastest-growing segment during the 2026 - 2033 forecast period. E-commerce platforms, including Amazon, Alibaba, and specialized lighting retailers, provide extensive product selections, competitive pricing, customer reviews, and convenient home delivery. The digital channel enables manufacturers to reach consumers directly, reducing distribution costs and maintaining greater control over brand presentation and customer relationships.

Online retail particularly appeals to younger demographics, who are comfortable with digital purchasing and value the ability to compare specifications, read user experiences, and access detailed product information unavailable in physical retail environments.

Regional Insights

Asia Pacific LED Desk Lamp Market Trends

Asia Pacific is poised to be both the leading and fastest-growing regional market for LED desk lamps in 2026, accounting for approximately 38% of the global market share. Asia Pacific combines strong demand fundamentals with deep manufacturing strength across countries such as China, Japan, South Korea, India, and key ASEAN economies. China drives regional performance as both a major consumer base and the central production hub, shaping product availability, cost structures, and innovation cycles across the value chain.

Developed markets in the region, including Japan and South Korea, set the benchmark for advanced functionality and user-centric design, reinforcing expectations for features such as smart connectivity, eye-comfort modes, and refined aesthetics. India and several Southeast Asian markets offer substantial room for further penetration, supported by rising incomes, the expansion of the education sector, and government programs that promote efficient lighting solutions and improve access to quality study environments.

The market in Asia Pacific also benefits from highly developed manufacturing ecosystems with established supply chains, proximity to LED component producers, cost-competitive labour pools, and large-scale production capabilities that support competitive pricing and frequent product refresh cycles. Rapid urbanization and ongoing investment in housing and commercial real estate increase the need for modern lighting in homes, offices, and educational facilities, while government-backed improvements in schools and universities further expand the addressable base for study and task lighting. These conditions support sustained investment in capacity expansion, automation, smart and health-oriented features, and brand-building initiatives, making Asia Pacific the primary engine of long-term growth and competitive differentiation.

Europe LED Desk Lamp Market Trends

Europe is one of the most mature and structurally attractive markets for LED desk lamps, supported by strong economic fundamentals, advanced manufacturing capabilities, and an early shift toward energy-efficient lighting. Germany anchors regional demand as the largest economy, combining engineering expertise with strong sustainability and workplace ergonomics awareness, while the United Kingdom, France, and Spain also play important roles in shaping product and channel strategies. The European Union (EU) drives this technology transition through ambitious policy frameworks, including the eco-design Directive, which sets minimum efficiency thresholds and clear phase-out schedules for conventional lighting technologies.

The regulatory environment in Europe is also notable for its high degree of harmonization, which creates relatively uniform market conditions across member states and reduces compliance complexity for manufacturers operating in multiple countries. Directives such as the Restriction of Hazardous Substances (RoHS) and Waste Electrical and Electronic Equipment (WEEE) embed extended producer responsibility, recyclability expectations, and restrictions on hazardous inputs into product and supply-chain design, reinforcing the business case for durable, high-quality LED solutions with lower environmental impact.

North America LED Desk Lamp Market Trends

North America is one of the most advanced and commercially lucrative markets for LED desk lamps, combining high purchasing power, strong technology adoption, and a supportive policy environment. The United States drives most of the regional demand, supported by early and widespread LED adoption, an entrenched remote and hybrid work culture, and strong interest in optimizing home offices and study spaces. Energy-efficiency regulations at federal and state levels, together with building codes that increasingly favor efficient solutions in both new construction and major renovations, create a clear and sustained structural tailwind for LED desk lamps.

The regional competitive landscape reflects this maturity and includes a diverse mix of established lighting brands, major technology companies expanding into smart lighting, and niche players that specialize in ergonomic and wellness-focused products. A strong innovation base, supported by advanced research and development capabilities and rapid consumer adoption of new technologies, enables frequent product launches that address themes such as digital eye strain, circadian-support lighting, and personalized task illumination.

For market participants, this environment creates opportunities to position premium LED desk lamps that combine design, connectivity, and evidence-based health benefits, while also requiring clear differentiation on performance, user experience, and sustainability credentials to stand out in a crowded and discerning marketplace.

Competitive Landscape

The global LED desk lamp market structure is moderately fragmented, dominated by leading players such as Signify N.V., BenQ Corporation, IKEA Group, Panasonic Corporation and OttLite Technologies. These players collectively capture 35-40% of market share. While numerous regional and specialized manufacturers compete across various price segments and distribution channels. Market concentration varies by region and segment, with premium and smart lighting categories demonstrating higher consolidation around established brands possessing technological capabilities and brand recognition.

The competitive positioning reflects multiple strategic approaches: established lighting manufacturers leveraging brand heritage and distribution networks, consumer electronics companies extending into smart lighting leveraging IoT ecosystems, furniture and office supply companies offering integrated workspace solutions, and specialized ergonomic product developers focusing on health and wellness features. Chinese manufacturers dominate volume production and value segments through cost advantages, while Western and Japanese brands command premium positioning through quality differentiation, design innovation, and advanced feature integration.

Key Industry Developments

- In January 2026, Crompton Greaves Consumer Electricals launched 70W and 80W Dynaray LED Lamps, targeting India's domestic B2C lighting market exclusively. These higher-wattage additions to the Dynaray series expand options for brighter home illumination, aligning with local consumer needs without initial international rollout.

- In January 2026, IKEA unveiled the Varmblixt LED Lamp, a donut-shaped smart light with matt white glass for table or wall use, featuring smooth color-shifting via 12 preset hues. A Bilresa remote enables control out-of-box, while Dirigea hub adds Matter compatibility for smart homes, with a dimmable tubular pendant counterpart.

- In May 2025, amaran introduced Verge and Verge Max bi-color edge-lit LED panels for vloggers. Verge is a compact 26W desk light, while 22" Max delivers softbox-like 60W output in 9% depth. Both feature 2700-6500K tuning, app/Sidra/Stream Deck control, USB-C power, passive cooling, and versatile mounting.

Companies Covered in LED Desk Lamp Market

- Signify N.V. (Philips)

- BenQ Corporation

- IKEA Group

- Xiaomi Corporation

- TaoTronics (Sunvalleytek International Inc.)

- Panasonic Corporation

- Dyson Limited

- Herman Miller, Inc.

- Koncept Technologies

- OttLite Technologies

- Lumiy

- Yeelight (Qingdao Yeelink Information Technology Co.)

- Tomons

- Newhouse Lighting

- AUKEY

Frequently Asked Questions

The global LED desk lamp market is projected to reach US$ 13.1 billion in 2026.

The market is driven by rising demand for energy-efficient, sustainable lighting, combined with remote work-driven need for ergonomic eye-friendly task illumination and smart, connected features.

The market is poised to witness a CAGR of 11% from 2026 to 2033.

Key opportunities lie in smart/IoT‑enabled lamps, human‑centric and eye‑care designs, wireless/portable form factors, and expansion into high‑growth Asia‑Pacific and e‑commerce channels.

Signify N.V., BenQ Corporation, IKEA Group, Panasonic Corporation, and OttLite Technologies are some of the key players in the market.