- Oil & Gas

- Land Drilling Rigs Market

Land Drilling Rigs Market Size, Share, and Growth Forecast, 2025 - 2032

Land Drilling Rigs Market by Rig Type (Conventional, Mobile, Automated, Modular), Application (Oil Drilling, Gas Exploration, Geothermal Drilling, Mining, Construction, Others), Drive Mode (Mechanical, Electrical, Compound), and Regional Analysis for 2025 - 2032

Land Drilling Rigs Market Share and Trends Analysis

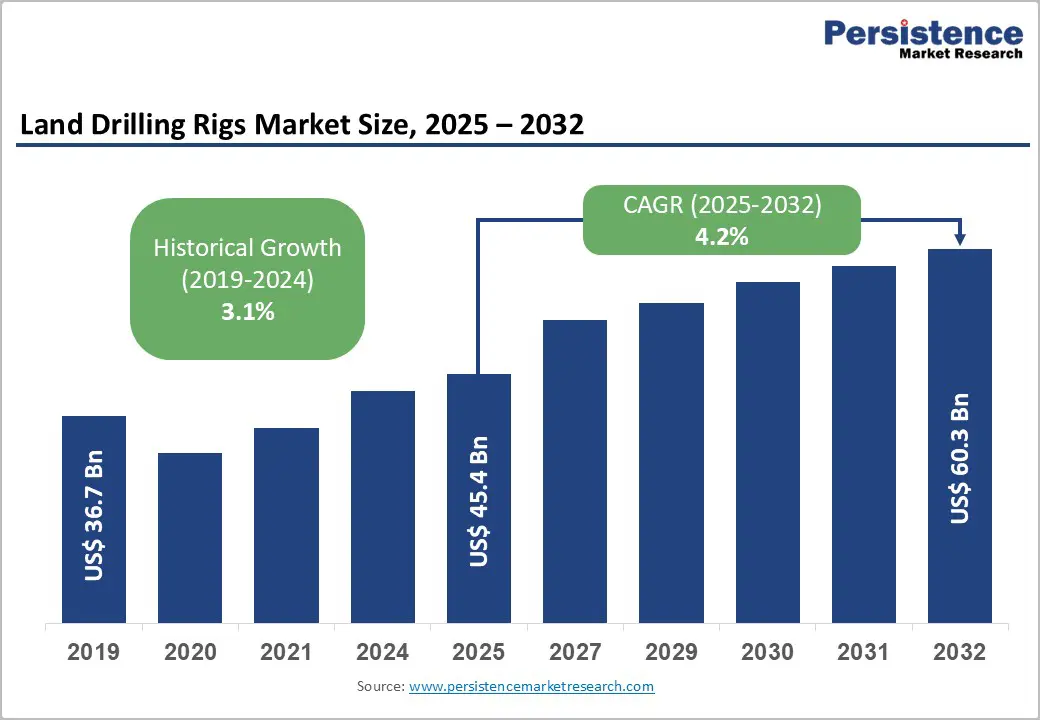

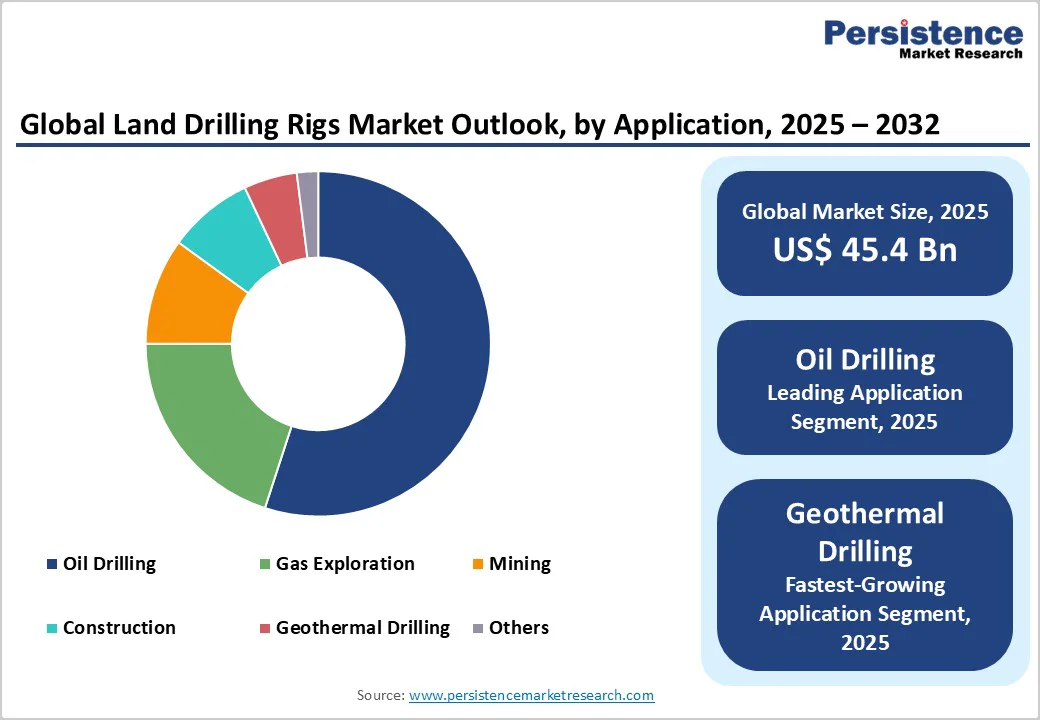

The global land drilling rig market is expected to be valued at US$45.4 billion in 2025. It is estimated to reach US$60.3 billion by 2032, growing at a CAGR of 4.2% during the forecast period 2025 - 2032, driven by soaring energy demand and technological advancements in drilling equipment.

The growth trajectory of the market is further supported by increased onshore exploration activities, rising production from shale oil and gas reserves, and the adoption of automated and mobile rigs that enhance operational efficiency and reduce downtime. Investments in infrastructure and regulatory incentives to boost domestic energy production further consolidate market expansion.

Key Industry Highlights

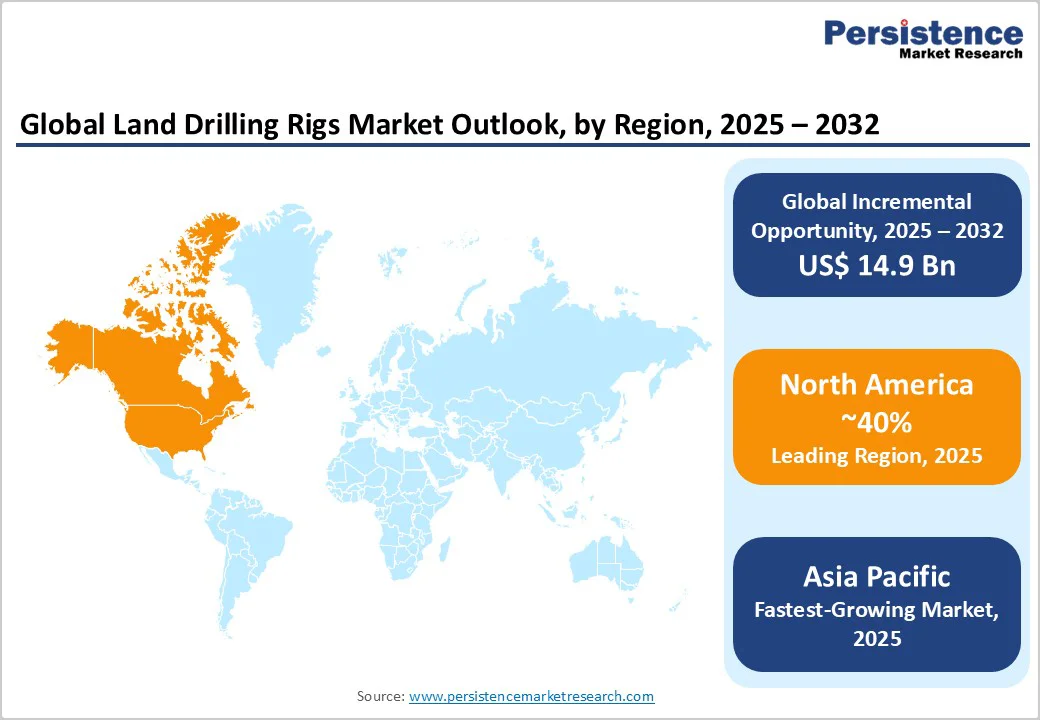

- Regional Dominance: North America leads the market with an estimated 40% share in 2025, supported by shale oil & gas production and innovation-driven investments.

- Fastest-growing Regional Market: Asia Pacific is set to be the fastest-growing regional market from 2025 to 2032, fueled by widespread oil and gas exploration activities and favorable energy policies.

- Leading Rig Type: Mobile rigs are slated to capture market share in 2025, on account of their flexibility and rapid deployment capabilities.

- Leading Applications: Oil drilling is poised to dominate applications with a 55% share in 2025, while geothermal drilling is likely to showcase the highest 2025 - 2032 CAGR.

- Drive Mode Dominance: Mechanical rigs are expected to capture nearly half of the market revenue share in 2025, whereas electrical rigs will post the fastest CAGR through 2032, driven by the shift to cleaner energy and operational precision.

- Market Structure: The land drilling rig market is moderately concentrated, with the top companies controlling 55-60% and focusing on digitalization and sustainability.

- Competitive Developments: Key developments include the launch of automated rigs, acquisitions to expand digital operations, and geographic expansions targeting emerging economies.

- January 2025: China launched a national megaproject to develop a 15,000-meter ultra-deep intelligent drilling rig, aiming to secure energy resources and advance deep-Earth exploration, led by the Chinese Academy of Geological Sciences.

| Key Insights | Details |

|---|---|

| Land Drilling Rigs Market Size (2025E) | US$45.4 Bn |

| Market Value Forecast (2032F) | US$60.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Advancements in Automated and Mobile Drilling Rigs

The steady integration of automation and digitalization in land drilling rigs is a critical niche driver shaping market growth. Advances such as real-time monitoring, predictive maintenance, and IoT-enabled smart rigs are increasing operational efficiency and safety while significantly reducing non-productive time. These technological improvements align with industry demands for operational cost reduction and environmentally responsible drilling practices.

The U.S. Department of Energy (DOE) and industry bodies such as the International Association of Drilling Contractors (IADC) report an increase in rig uptime due to automation efforts. With global energy demand projected to grow annually by 2-3%, leveraging smart rigs becomes indispensable, especially in mature markets such as North America and emerging Asia Pacific economies that are rapidly adopting these technologies.

Regulatory Compliance and Environmental Restrictions

Stringent environmental regulations pose a structural challenge, particularly in regions with sensitive ecological zones and high public scrutiny toward fossil fuel extraction. Compliance with emission standards and mandates to reduce water use in drilling operations increases costs, according to government regulatory impact assessments from the U.S. Environmental Protection Agency (EPA) and the European Environment Agency (EEA).

Delays in permitting and increased expenditure on environmental impact mitigation restrict market expansion, especially in Europe and parts of Asia, where regulatory frameworks are tightening. These constraints necessitate investments in greener drilling technologies and adaptive operational strategies, creating a pressing need for compliance-oriented innovation and partnership with regulatory bodies to mitigate market risks effectively.

Expansion in Unconventional Onshore Reserves and Emerging Markets

The exploitation of unconventional reserves, primarily tight oil and shale gas, is emerging as a lucrative opportunity for land drilling rig companies and operators. Countries such as India, Brazil, and Argentina are unlocking significant reserves through government-backed exploration initiatives and policy reforms favoring domestic resource development.

With Asia Pacific expected to grow its market share to approximately 25% by 2025, driven by exploration activities and adoption of cost-efficient rigs, investment opportunities abound in this region. Infrastructure development, coupled with digital drilling solutions tailored for complex geology, is positioning these markets as strategic growth areas. Private and public sector investments exceeding billions in emerging markets further underscore the forward momentum.

Category-Wise Analysis

Rig Type Insights

Mobile rigs are the unequivocal leaders in 2025, commanding an estimated 40% of the land-drilling rig market revenue share. This dominance is attributable to their operational flexibility across diverse terrains, fast mobilization capabilities, and adaptability to both conventional and unconventional drilling projects.

Mobile rigs provide essential agility in onshore drilling environments, particularly for shale oil and gas plays, where rapid relocation between well sites is economically and operationally advantageous. Their design supports modular upgrades, enabling integration with modern automation and digital technologies, further solidifying their market preference.

The prevailing competitive landscape sees mobile rig manufacturers investing heavily in engineering enhancements to reduce rig move times and enhance drilling precision.

The fastest-growing rig type segment from 2025 to 2032 is likely to be automated rigs, fueled by the increasing adoption of robotics, IoT, and real-time data analytics within land drilling operations. Automation improves safety by reducing human exposure to hazardous environments and enhances operational efficiency through predictive maintenance and optimized drilling parameters.

The integration of AI-driven control systems in automated rigs enables higher drilling accuracy and resource optimization. Market investment is increasingly funneled toward R&D in remote-operated rigs and advanced sensor technologies, heralding a shift toward fully autonomous drilling operations.

Application Insights

Oil drilling stands as the leading application in 2025, accounting for an estimated 55% share of the market. This preeminence is driven by continuous upstream investments, particularly in shale oil basins across North America, supported by technological advancements that enable economically viable drilling in previously inaccessible formations.

The demand for oil rigs is further bolstered by consistent global energy consumption and policies favoring domestic oil production to reduce import dependence. Operators are increasingly opting for rigs capable of multi-well pad drilling to maximize output and efficiency, thus driving demand for sophisticated rig designs within this segment.

The fastest-growing application from 2025 to 2032 is projected to be geothermal drilling. The rapid growth of this segment aligns with global decarbonization efforts and commitments under the Paris Agreement to increase renewable energy capacity. Geothermal energy exploration requires specialized rigs capable of drilling high-temperature, high-pressure wells, which are a focus area of technological innovation.

Investments by governments and the private sector in geothermal projects, notably in the Asia-Pacific and European markets, offer ample growth opportunities. The geothermal segment represents an actionable nexus for companies expanding portfolio diversification toward sustainable energy solutions.

Drive Mode Insights

Mechanical drive rigs are expected to maintain leadership, with a 2025 market share of approximately 50%, primarily driven by their established presence and cost-effectiveness in developing economies.

Mechanical drives offer proven reliability across various geological conditions and are typically favored for their simpler maintenance requirements. Despite incremental innovations, mechanical drive systems face increasing pressure from emerging alternatives with superior energy profiles.

Electrical rigs represent the fastest-growing drive mode, with a robust 2025 - 2032 CAGR. Their growth is principally driven by stringent environmental regulations that favor lower emissions and greater energy efficiency.

Electrical drives enable precise control over drilling parameters, improving drilling accuracy and reducing operational disruptions. Their compatibility with hybrid and renewable energy sources aligns with the broader industry trend toward sustainability. Leading markets adopting electrical rigs showcase enhanced operational productivity and notably reduced carbon footprints.

Regional Insights

North America Land Drilling Rigs Market Trends

North America is poised to retain its position as the dominant regional market, with an approximate 40% share by 2025. The U.S. and Canada’s vast shale oil and gas reserves continue to underpin this leadership, with significant investments in advanced drilling technologies fostering competitive advantages.

The region’s infrastructure robustness, combined with supportive regulatory frameworks that incentivize domestic energy production, catalyzes market growth. Regulatory bodies such as the U.S. Bureau of Land Management (BLM) and Pipeline and Hazardous Materials Safety Administration (PHMSA) are fostering safer, environmentally responsible operations through updated compliance standards.

North America is experiencing an innovation-rich ecosystem where drilling automation, digital twin technologies, and green drilling practices are rapidly being adopted. Competitive landscape players include technology-centric firms aggressively integrating IoT and AI to optimize real-time drilling.

Furthermore, investment trends reveal significant funding in clean energy initiatives, including geothermal applications, positioning the region as both an energy and technology leader.

Europe Land Drilling Rigs Market Trends

Europe holds an estimated 15% market share in 2025, characterized by moderate growth through 2032. Key countries such as Germany, the U.K., France, and Spain drive market activity, focusing heavily on compliance with stringent environmental and safety regulations that elevate operational standards.

The European Union’s regulatory harmonization efforts strongly influence market dynamics by enforcing emission reduction mandates and incentivizing renewable energy projects, particularly geothermal drilling.

Operationally, market players have adapted by incorporating environmentally sensitive rig designs and operational protocols, often collaborating closely with regulatory agencies. Investment opportunities are increasingly centered on energy transition technologies, with rising geothermal and unconventional drilling projects signaling an expanding market segment.

Competitive strategies emphasize compliance consulting and technological retrofitting to meet evolving regulations, fostering a market environment that prioritizes sustainable growth.

Asia Pacific Land Drilling Rigs Market Trends

Asia Pacific is emerging as the fastest-growing regional market for land drilling rigs through 2032. Growth is mainly attributable to the surging energy demand in China, India, and the ASEAN countries, alongside rising industrialization and infrastructure development.

The regional market benefits from competitive manufacturing bases and favorable government policies that promote domestic drilling and foreign collaborations. Evolving regulatory frameworks are fostering sustainable resource extraction balanced with environmental stewardship.

Competition is dynamic, with indigenous rig manufacturers and foreign technology providers forming joint ventures and strategic partnerships. Investment dynamics highlight increased capital flow into advanced land drilling rigs, digitalization technologies, and capacity expansion to tap emerging unconventional resources. The growth path of the market here indicates significant opportunities for market entrants and incumbents alike.

Competitive Landscape

The global land drilling rigs market landscape exhibits a moderately concentrated competitive structure, with the top tier of companies collectively controlling between 55% and 60% of the revenues.

National Oilwell Varco, Nabors Industries, Helmerich & Payne, Schlumberger, and Weatherford International lead the charge, distinguished by their expansive technology portfolios, global service networks, and strategic alliances. These companies invest heavily in R&D, propelling innovation in automation, digital integration, and eco-efficient rig systems.

While the major players dominate, the market remains highly fragmented, with regional players addressing localized needs with cost-effective rig solutions. This dual dialectic fosters a competitive environment where scalability, technological differentiation, and regulatory compliance are essential success factors. Strategic moves by market leaders often include mergers and acquisitions to augment technological breadth and geographic footprint.

Key Industry Developments

- In September 2025, Caturus Energy and Nabors Industries deployed the PACE-X Ultra™ X33, the most powerful onshore drilling rig in the U.S., designed for complex well designs with laterals up to 4 miles and depths exceeding 14,000 feet. This rig features a one-million-pound mast rating, 35,000 feet of racking capacity, and three 2,000-horsepower mud pumps with 10,000 psi pressure, enhancing drilling efficiency and safety. The rig also uses Cat® Dynamic Gas Blending technology to substitute natural gas for diesel, improving fuel efficiency and reducing emissions.

- In September 2025, National Oilwell Varco (NOV) launched the AgitatorX2, a dual friction reduction system designed to improve drilling efficiency in extended laterals by reducing drillstring friction and enhancing weight transfer to the bit. Its unique zero-pressure drop feature maximizes hydraulic efficiency and maintains real-time downhole communication, crucial for long wellbores. Field tests in North and South America demonstrated up to a 29% increase in the sliding rate of penetration (ROP) and improved tool face control.

- In May 2025, SLB agreed to sell a 70% stake in its land drilling rigs business in Kuwait and Oman to ADNOC Drilling, covering eight fully operational rigs under contract to national oil companies in these countries. This partnership signifies strong regional collaboration and aligns with SLB's growth strategy in the Middle East and North Africa. The transaction is pending regulatory approvals and is expected to close by Q1 2026. Both companies aim to enhance operational performance and expand strategic energy sector partnerships in the region.

Companies Covered in Land Drilling Rigs Market

- National Oilwell Varco, Inc.

- Helmerich & Payne, Inc.

- Nabors Industries Ltd.

- Schlumberger Limited

- Weatherford International PLC

- Saipem SpA

- KCA Deutag

- Archer Ltd.

- China Oilfield Services Limited (COSL)

- Patterson-UTI Energy, Inc.

- Transocean Ltd.

- Valaris Limited

- Baker Hughes Company

- Halliburton Company

- Petroleum Development Oman (PDO)

Frequently Asked Questions

The global land drilling rigs market is projected to reach US$45.4 Billion in 2025.

Soaring energy demand globally, technological advancements in drilling equipment, and increased onshore exploration activities are driving the market.

The land drilling rigs market is poised to witness a CAGR of 4.2% from 2025 to 2032.

Rising production from shale oil and gas reserves, the adoption of automated and mobile rigs that enhance operational efficiency and reduce downtime, and investments in infrastructure and regulatory incentives to boost domestic energy production are key market opportunities.

National Oilwell Varco, Inc., Helmerich & Payne, Inc., Nabors Industries Ltd., and Schlumberger Limited are some of the top players in the land drilling rigs market.