- Industrial Goods & Service

- Land Survey Equipment Market

Land Survey Equipment Market Size, Share, and Growth Forecast 2025 - 2032

Land Survey Equipment Market by Component (Hardware, Software, Services), Application (Transportation, Energy & Power, Mining & Construction, Agriculture, Disaster Management, Others), End-Use Industry, and Regional Analysis for 2025 - 2032

Land Survey Equipment Market Share and Trends Analysis

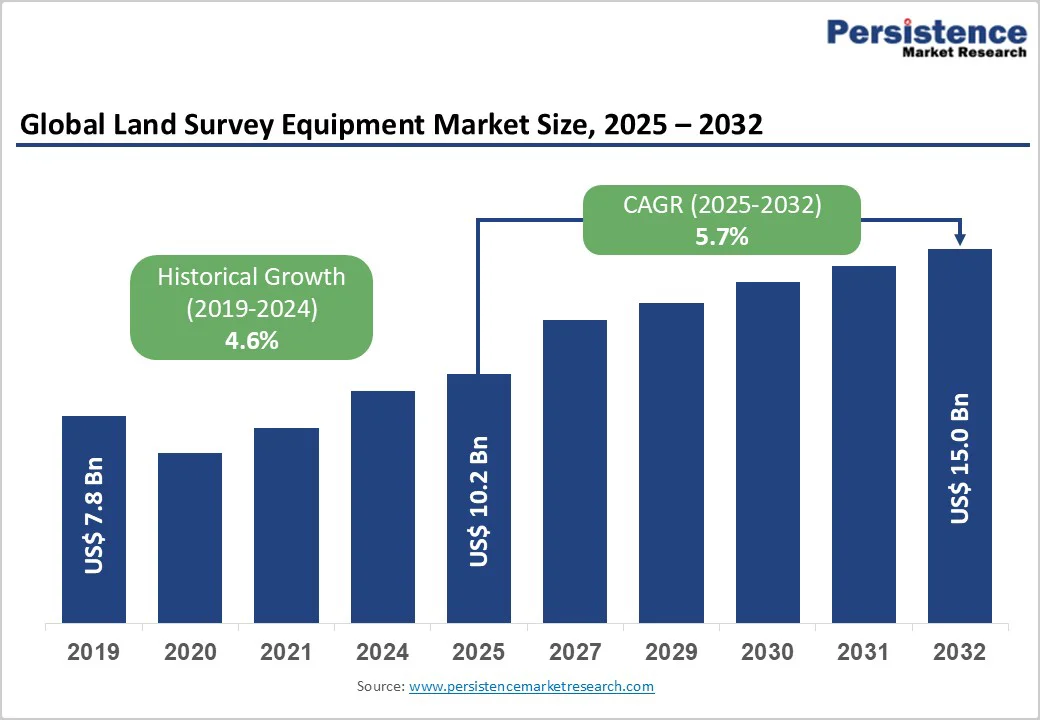

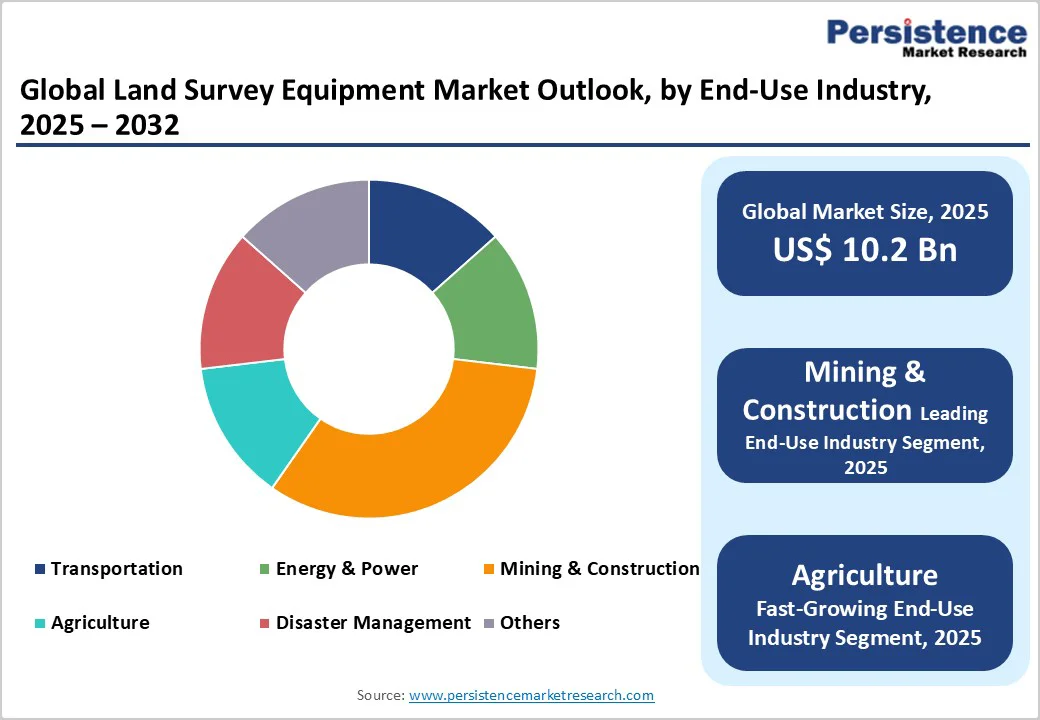

The global land survey equipment market size is likely to be valued at US$10.2 billion in 2025, and is projected to reach US$15.0 billion by 2032, growing at a CAGR of 5.7% during the forecast period 2025 - 2032.

Market expansion is driven by accelerating global infrastructure development, urbanization trends that require precise spatial data collection, and the widespread adoption of advanced surveying technologies, including Global Navigation Satellite Systems (GNSS), LiDAR, and unmanned aerial vehicles (UAVs).

Increasing digitalization through building information modeling (BIM) integration, construction automation initiatives, and regulatory compliance requirements across transportation, mining, energy, and agriculture sectors sustains consistent market demand globally.

Key Industry Highlights

- Leading Region: Asia Pacific leads with 37% market share in 2025, driven by rapid urbanization, massive infrastructure investments, and exponential expansion of the construction sector across China, India, and Southeast Asia.

- Fastest-growing Regional Market: The Asia Pacific market is expected to grow the fastest at approximately 6.8% CAGR through 2032, propelled by emerging market industrialization, government smart city initiatives, and construction modernization.

- Dominant Component: Hardware dominates at 31% market revenue share, delivering centimeter-level positioning accuracy, universal geographic deployment capability, and seamless integration with real-time kinematic (RTK) correction systems.

- Dominant Application: Inspection and monitoring applications dominate, capturing around 38% of the total market demand due to their diverse industrial requirements.

- Key Market Opportunity: Precision agriculture and drone-based surveying present a substantial market opportunity targeting 5 billion hectares of agricultural land, with substantial cost reductions.

| Key Insights | Details |

|---|---|

| Land Survey Equipment Market Size (2025E) | US$10.2 Bn |

| Market Value Forecast (2032F) | US$15.0 Bn |

| Projected Growth CAGR (2025 - 2032) | 5.7% |

| Historical Market Growth (2019 - 2024) | 4.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Accelerating Global Infrastructure Development and Urban Expansion

Global infrastructure investment is experiencing exceptional expansion, with governments and private entities allocating trillions of dollars toward transportation networks, power systems, water infrastructure, and smart city development.

For example, the surge in China's infrastructure investment has created a massive demand for precise surveying and spatial data collection. Global construction spending exceeded US$12 trillion annually during 2024 and 2025. Precise land survey equipment, such as GNSS systems, total stations, and 3D laser scanners, enables accurate site planning, boundary delineation, and volumetric calculations essential for infrastructure development.

The convergence of urbanization, infrastructure modernization, and regulatory compliance requirements is driving consistent demand for advanced surveying solutions across transportation, energy, mining, and construction sectors worldwide.

Rapid advancement in surveying technologies is fundamentally transforming industry practices, with GNSS providing centimeter-level accuracy, LiDAR enabling rapid point cloud capture, and UAV systems delivering cost-effective aerial data collection.

Surveyors are actively adopting drone technology for precise topographic mapping, while surveying companies are integrating geographic information systems (GIS) and 3D modeling for enhanced land assessment accuracy. The deployment of BIM is also accelerating across the construction and real estate sectors, requiring seamless integration of survey data to ensure accurate digital project representations.

Advanced surveying technologies, such as RTK systems, reduce surveying time by approximately 30 times compared to traditional methods while substantially improving accuracy and data richness, justifying technology investments and supporting sustained market expansion.

Shortage of Skilled Professionals and Technical Expertise Gaps

The surveying industry faces substantial workforce challenges with the limited availability of trained professionals proficient in operating advanced surveying instruments and processing complex geospatial data. Advanced equipment operation requires specialized certifications, manufacturer-specific training programs, and continuous professional development, which create skill gaps in the market.

Geographic distribution challenges concentrate expertise in developed urban centers, while rural and developing regions lack certified technicians capable of operating, calibrating, and analyzing equipment. Training program limitations and evolving technology complexity strain workforce development capabilities, creating bottlenecks that limit surveying project execution timelines and market expansion opportunities.

Expansion of Precision Agriculture and Drone-Based Surveying

Precision agriculture is demonstrating exceptional growth potential, driven by global population expansion toward 10 billion by 2050, which requires enhanced agricultural productivity through data-driven farming practices.

Agricultural drone applications, such as Normalized Difference Vegetation Index (NDVI) crop health monitoring, irrigation optimization, and yield forecasting, are creating substantial demand for specialized agricultural mapping and monitoring solutions. With global agrarian land area exceeding 5 billion hectares, the market presents a massive opportunity for cost-effective drone-based survey systems, multispectral sensors, and agricultural analytics platforms.

Government subsidies supporting agricultural modernization and climate-smart farming practices in emerging markets are creating favorable conditions for adoption. Drone surveying reduces agricultural surveying costs by 40% to 60% compared to traditional ground-based methods, accelerating technology adoption among commercial farms, agribusinesses, and agricultural development organizations worldwide.

Global mining operations are increasingly adopting advanced surveying technologies to improve safety, optimize operational efficiency, and monitor environmental compliance. Drone mining surveys capture high-resolution aerial data, enabling high-speed data collection while improving worker safety through remote operations that eliminate personnel exposure to hazardous mine environments.

Mining exploration projects are leveraging drone technology for cost-effective surveys at a fraction of traditional survey expenses, while operational planning and resource extraction optimization benefit from real-time 3D modeling and digital elevation models (DEMs).

Government mining regulations increasingly mandate advanced surveying for environmental protection and safety compliance, creating regulatory-driven demand for specialized mining survey equipment across established and emerging mining regions worldwide.

Category-wise Analysis

Component Insights

Global Navigation Satellite Systems represent the dominant hardware segment, commanding approximately 31% of the land survey equipment market revenue share in 2025. This dominance is due to their superior positioning accuracy and reliable centimeter-level precision when integrated with RTK correction systems.

These systems provide continuous, universal positioning capabilities independent of regional infrastructure, enabling effective deployment in both remote and urban environments. GNSS receivers are widely used for establishing control points, continuous site monitoring, and automated construction layout, supporting real-time operational guidance across diverse applications.

The market leadership of GNSS technology is further supported by its proven operational stability, compatibility with existing workflows, and demonstrated reliability under varied environmental conditions.

Emerging technology variants, such as dual-band RTK receivers with artificial intelligence processors, are attracting premium market positioning by offering enhanced redundancy and automated point cloud classification, expanding opportunities for advanced surveying and geospatial analysis.

Application Insights

Inspection and monitoring applications are expected to capture approximately 38% of the revenue share in 2025, driven by their critical role across diverse industrial sectors. These applications include construction site inspections, infrastructure integrity assessments, bridge and road network condition monitoring, and power line and pipeline inspections, all of which require versatile and reliable surveying equipment.

Real-time monitoring systems enable continuous operational oversight, early problem detection to prevent costly failures, and regulatory compliance documentation. Advanced drone technology has become integral in this segment, reducing inspection costs by 40% to 60% compared to traditional methods while improving data accuracy and safety by minimizing personnel exposure to hazardous environments.

As infrastructure investments and renewable energy initiatives grow worldwide, the demand for cost-effective, precise, and efficient inspection and monitoring solutions is expected to sustain consistent market growth through 2032 and beyond. North America currently leads with a significant market share, followed by rapid adoption in emerging economies driven by urbanization and infrastructure development programs.

End-Use Industry Insights

Mining and construction represent the largest end-use sector, accounting for approximately 40% of total demand, driven by consistent land survey equipment requirements throughout project lifecycles, including construction staking, site layout planning, boundary surveying, and as-built documentation.

The integration of BIM requires seamless incorporation of survey data to support accurate digital project representations, design coordination, and clash detection. Large-scale infrastructure projects, including highway networks, railway systems, bridge construction, and water infrastructure development, generate substantial demand for surveying equipment, which is essential for project planning and execution.

Global government infrastructure investment initiatives totaling trillions of dollars support sustained growth in the construction sector, securing its dominant market position through 2032.

Moreover, advances in GNSS, laser scanning, and drone technologies are enhancing surveying accuracy and efficiency, enabling mining and construction projects to optimize safety, operational precision, and regulatory compliance, particularly in emerging economies experiencing rapid urbanization and infrastructure modernization.

Regional Insights

North America Land Survey Equipment Market Trends

North America is a critical market for land survey equipment companies, on account of its established infrastructure networks requiring modernization, advanced technology adoption capabilities, and robust regulatory frameworks mandating surveying standards.

U.S. construction spending exceeded US$2 trillion in 2024, driving consistent surveying equipment demand across residential, commercial, and infrastructure development projects. Federal regulations and safety standards, including OSHA requirements and environmental compliance mandates, necessitate advanced surveying for construction planning and operational monitoring.

The regional market benefits from mature surveying industry infrastructure, a strong manufacturer presence, such as Trimble Inc. and Leica Geosystems, and advanced research capabilities that support continuous technology innovation.

Smart city initiatives across major metropolitan areas, including comprehensive 3D urban modeling and infrastructure digitalization, are driving demand for specialized surveying equipment. The aerospace & defense sector of North America also fuels the demand for premium surveying equipment for precision applications, while agricultural technology adoption accelerates, particularly across major farming regions.

Europe Land Survey Equipment Market Trends

Europe represents a mature land survey equipment market characterized by established industry practices, stringent regulatory standards, and advanced technology adoption. Germany leads the region with a 32.1% market share in 2025, supported by its position as a global engineering and construction technology center housing major operations of Hexagon AB and Topcon European facilities.

European Union (EU) initiatives, such as the Trans-European Networks for Transport (TEN-T) program, drive multi-year infrastructure projects that require extensive surveying infrastructure. The U.K., France, and Spain contribute significantly through strong construction sectors focused on commercial real estate, infrastructure renewal, and renewable energy developments.

Environmental monitoring and climate change adaptation further boost demand for specialized surveying applications in ecological assessment and sustainable infrastructure planning.

European manufacturers emphasize regulatory compliance, environmental sustainability, and precision engineering, reinforcing the region’s premium product positioning and technology leadership in global markets. The European land survey equipment market is projected to grow at an 8% CAGR from 2025 to 2032, reflecting continued modernization and investment in infrastructure and environmental technologies.

Asia Pacific Land Survey Equipment Market Trends

At 37%, Asia Pacific dominates the land survey equipment market share in 2025, powered by rapid urbanization, massive infrastructure investments, and manufacturing expansion.

China's urbanization rate reached 66.16% in 2023, fueling exceptional demand in construction, transportation, and utility network development. India targets urban development to accommodate 500 million new urban residents, driving substantial long-term demand for surveying equipment across metropolitan expansion projects.

Japan’s advanced manufacturing and precision engineering support surveying equipment innovation, while South Korea’s construction excellence and emerging Southeast Asian markets demonstrate significant growth potential.

Leading regional manufacturers, including Hi-Target, CHC Navigation, and Topcon, maintain competitive positioning through localized product offerings and participation in government localization programs. Government initiatives advancing smart city development and infrastructure modernization accelerate technology adoption across the region, supporting a projected regional CAGR of nearly 6% through 2032.

Competitive Landscape

The global land survey equipment market landscape exhibits moderate consolidation with leading manufacturers - Hexagon AB, Trimble Inc., and Topcon Corporation - collectively controlling approximately 55-60% of the revenues.

These companies leverage extensive geospatial technology expertise, established relationships with contractors, and comprehensive system integration capabilities to maintain leadership. Tier-two participants, including Leica Geosystems, FARO Technologies, and CHC Navigation, hold a combined 25-30% market share by focusing on specialized surveying technologies and innovative product interfaces.

Meanwhile, regional specialists such as South Surveying & Mapping Instrument Co., Ltd. benefit from government localization programs, and European startups advance photogrammetry cloud engines optimized for 5G edge computing environments.

Industry competition revolves around precision, technological innovation, software integration, and product reliability rather than price, with companies investing heavily in R&D to develop advanced GNSS, LiDAR, 3D laser scanning, and drone surveying solutions meeting the growing demands of infrastructure, construction, mining, and environmental monitoring sectors.

Key Industry Developments

- In October 2025, Leica Geosystems developed the AI-powered TS20 robotic total station, designed for faster, safer, and more reliable surveying in all weather conditions with IP66 protection. Featuring edge AI for error reduction, automatic target recognition, and seamless cloud connectivity, the TS20 enhances productivity while enabling easy integration into existing workflows. It also includes smart security features such as remote locking to prevent theft, setting a new standard for robotic total stations in construction and surveying applications.

- In August 2025, the Puducherry government launched a digital re-survey of land under the centrally-assisted NAKSHA Project to modernize outdated land records from the 1970s. Using drone-based aerial surveys and satellite technology, the initiative aims to improve land record accuracy, ownership verification, and transparency, issuing updated records with unique parcel IDs and integrating tax and planning data for better land management.

- In April 2025, Topcon Positioning Systems introduced the CR-H1, a handheld reality capture solution combining advanced GNSS technology with Pix4D's photogrammetry software to create accurate, full-color 3D point clouds using iPhone devices with integrated LiDAR. Designed for diverse applications such as construction verification, land surveying, and utilities mapping, the CR-H1 enables mobile, high-precision 3D data capture without a tripod.

Companies Covered in Land Survey Equipment Market

- Bosch Tools

- Deepwell

- Emlid Tech

- STONEX Srl

- Trimble Inc.

- Hexagon AB

- Shanghai Huace Navigation Technology Ltd.

- Guangdong Kolida Instrument Co., Ltd.

- VI Instruments

- Hi-Target

- Suzhou FOIF Co Ltd.

- Topcon Corporation

- U-Blox Holding

- Hudaco Industries

- CHC-Navigation

- Leica Geosystems

- FARO Technologies

Frequently Asked Questions

The global land survey equipment market is projected to reach US$ 10.2 billion in 2025.

Escalating global infrastructure investment, rapid urbanization, widespread GNSS, LiDAR, and UAV technology adoption, BIM integration requirements across construction projects, and regulatory compliance mandates for surveying accuracy and environmental monitoring are driving the market.

The market is poised to witness a CAGR of 5.7% from 2025 to 2032.

Precision agriculture and drone-based surveying present the highest-growth opportunities, as it targets 5 billion hectares agricultural land, delivers significant cost reductions, enables NDVI crop monitoring, irrigation optimization, and yield forecasting across farms worldwide.

Trimble Inc., Hexagon AB, and Topcon Corporation are the leading players in the market.